Introduction

The term bookkeeping means different things to different people:

-

Some people think that bookkeeping is the same as accounting. They assume that keeping a company’s books and preparing its financial statements and tax reports are all part of bookkeeping. Accountants do not share their view.

-

Others see bookkeeping as limited to recording transactions in journals or daybooks and then posting the amounts into accounts in ledgers. After the amounts are posted, the bookkeeping has ended and an accountant with a college degree takes over. The accountant will make adjusting entries and then prepare the financial statements and other reports.

-

The past distinctions between bookkeeping and accounting have become blurred with the use of computers and accounting software. For example, a person with little bookkeeping training can use the accounting software to record vendor invoices, prepare sales invoices, etc. and the software will update the accounts in the general ledger automatically. Once the format of the financial statements has been established, the software will be able to generate the financial statements with the click of a button.

-

At mid-size and larger corporations the term bookkeeping might be absent. Often corporations have accounting departments staffed with accounting clerks who process accounts payable, accounts receivable, payroll, etc. The accounting clerks will be supervised by one or more accountants.

Our explanation of bookkeeping attempts to provide you with an understanding of bookkeeping and its relationship with accounting. Our goal is to increase your knowledge and confidence in bookkeeping, accounting and business. In turn, we hope that you will become more valuable in your current and future roles.

WATCH NOW

Advance Your Career with Our PRO Training

Bookkeeping: Past and Present

Bookkeeping in the Old Days

Prior to computers and software, the bookkeeping for small businesses usually began by writing entries into journals. Journals were defined as the books of original entry. In order to reduce the amount of writing in a general journal, special journals or daybooks were introduced. The special or specialized journals consisted of a sales journal, purchases journal, cash receipts journal, and cash payments journal.

The company’s transactions were written in the journals in date order. Later, the amounts in the journals would be posted to the designated accounts located in the general ledger. Examples of accounts include Sales, Rent Expense, Wages Expense, Cash, Loans Payable, etc. Each account’s balance had to be calculated and the account balances were used in the company’s financial statements. In addition to the general ledger, a company may have had subsidiary ledgers for accounts such as Accounts Receivable.

Handwriting the many transactions into journals, rewriting the amounts in the accounts, and manually calculating the account balances would likely result in some incorrect amounts. To determine whether errors had occurred, the bookkeeper prepared a trial balance. A trial balance is an internal report that lists 1) each account name, and 2) each account’s balance in the appropriate debit column or credit column. If the total of the debit column did not equal the total of the credit column, there was at least one error occurring somewhere between the journal entry and the trial balance. Finding the one or more errors often meant spending hours retracing the entries and postings.

After locating and correcting the errors the bookkeeping phase was completed and the accounting phase began. It began with an accountant preparing adjusting entries so that the accounts reflected the accrual basis of accounting. Adjusting entries were necessary for the following reasons:

- additional revenues and assets may have been earned but were not recorded

- additional expenses and liabilities may have been incurred but were not recorded

- some of the amounts that had been recorded by the bookkeeper may have been prepayments which are no longer prepaid

- depreciation and other non-routine adjustments needed to be computed and recorded

After all of the adjustments were made, the accountant presented the adjusted account balances in the form of financial statements.

After each year’s financial statements were completed, closing entries were needed. The purpose of closing entries is to get the balances in all of the income statement accounts (revenues, expenses) to be zero before the start of the new accounting year. The net amount of the income statement account balances would ultimately be transferred to the proprietor’s capital account or to the stockholders’ retained earnings account.

Bookkeeping Today

The electronic speed of computers and accounting software gives the appearance that many of the bookkeeping and accounting tasks have been eliminated or are occurring simultaneously. For example, the preparation of a sales invoice will automatically update the relevant general ledger accounts (Sales, Accounts Receivable, Inventory, Cost of Goods Sold), update the customer’s detailed information, and store the information for the financial statements as well as other reports.

The accounting software has been written so that every transaction must have the debit amounts equal to the credit amounts. The electronic accuracy also eliminates the errors that had occurred when amounts were manually written, rewritten and calculated. As a result, the debits will always equal the credits and the trial balance will always be in balance. No longer will hours be spent looking for errors that occurred in a manual system.

CAUTION: While the accounting software is amazingly fast and accurate in processing the information that is entered, the software is unable to detect whether some transactions have been omitted, have been entered twice, or if incorrect accounts were used. Fraudulent transactions and amounts could also be entered if a company fails to have internal controls.

After the sales invoices, vendor invoices, payroll and other transactions have been processed for each accounting period, some adjusting entries are still required. The adjusting entries will involve:

- revenues and assets that were earned, but not yet entered into the software

- expenses and liabilities that were incurred, but not yet entered into the software

- prepayments that are no longer prepaid

- recording depreciation expense, bad debts expense, etc.

The adjusting entries will require a person to determine the amounts and the accounts. Without adjusting entries the accounting software will be producing incomplete, inaccurate, and perhaps misleading financial statements.

After the financial statements for the year are released, the software will transfer the balances from the income statement accounts to the sole proprietor’s capital account or to the stockholders’ retained earnings account. This allows for the following year’s income statement accounts to begin with zero balances. (The balance sheet accounts are not closed as their balances are carried forward to the next accounting year.)

Recording Transactions

Bookkeeping (and accounting) involves the recording of a company’s financial transactions. The transactions will have to be identified, approved, sorted and stored in a manner so they can be retrieved and presented in the company’s financial statements and other reports.

Here are a few examples of some of a company’s financial transactions:

- The purchase of supplies with cash.

- The purchase of merchandise on credit.

- The sale of merchandise on credit.

- Rent for the business office.

- Salaries and wages earned by employees.

- Buying equipment for the office.

- Borrowing money from a bank.

The transactions will be sorted into perhaps hundreds of accounts including Cash, Accounts Receivable, Loans Payable, Accounts Payable, Sales, Rent Expense, Salaries Expense, Wages Expense Dept 1, Wages Expense Dept 2, etc. The amounts in each of the accounts will be reported on the company’s financial statements in detail or in summary form.

With hundreds of accounts and perhaps thousands of transactions, it is clear that once a person learns the accounting software there will be efficiencies and better information available for managing a business.

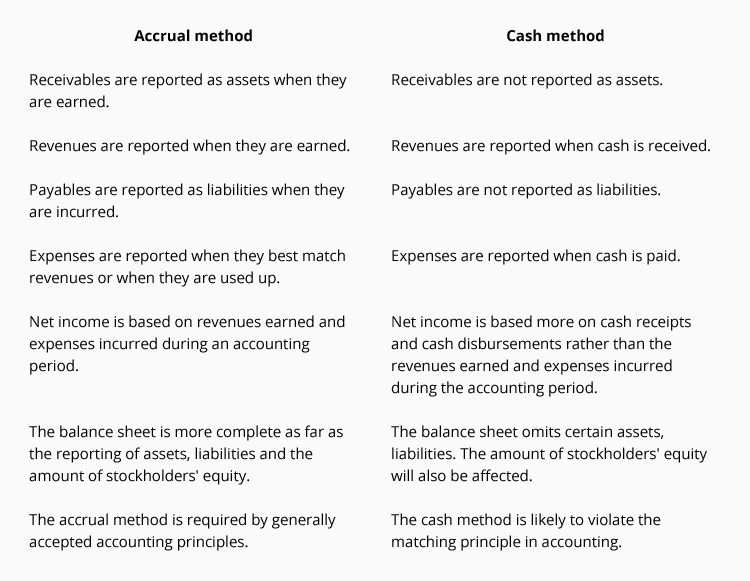

Accrual Method

There are two main methods of accounting (or bookkeeping):

- Accrual method

- Cash method

The accrual method of accounting is the preferred method because it provides:

- a more complete reporting of the company’s assets, liabilities, and stockholders’ equity at the end of an accounting period, and

- a more realistic reporting of a company’s revenues, expenses, and net income for a specific time interval such as a month, quarter or year.

As a result, US GAAP requires most corporations to use the accrual method of accounting.

The following table compares the accrual and cash methods of accounting:

Note: Some small companies may be allowed to use the cash method of accounting and in turn may experience an income tax benefit. Since our website does not provide income tax information, you should seek tax advice from a tax professional or from IRS.gov.

Revenues and Receivables

Under the accrual method, revenues are to be reported in the accounting period in which they are earned (which may be different from the period in which the money is received).

To illustrate the reporting of revenues under the accrual method, let’s assume that the hypothetical business Servco provides a service to a customer on December 27. Servco prepares a sales invoice for the agreed upon amount of $1,000. The invoice is dated December 27 and states that the amount is due in 30 days.

Under the accrual method, on December 27 Servco:

- has earned revenue of $1,000, and

- has earned a receivable of $1,000.

If Servco uses accounting software to prepare the invoice, the following will be recorded automatically as of December 27:

- the income statement account Service Revenues will be increased by $1,000, and

- the asset Accounts Receivable will be increased by $1,000

In addition to updating the general ledger accounts (which are used in preparing the financial statements), the software will update and store the customer’s information for generating an aging of accounts receivable and a statement of each customer’s activity.

Expenses and Payables

Under the accrual method, expenses should be reported on the income statement in the period in which they best match with the revenues. If a cause and effect relationship is not obvious, the expense should be reported on the income statement when the cost is used up or expires. In any event, the payment of cash is not the primary factor for determining the accounting period in which an expense is reported on the income statement.

To illustrate, let’s assume that Servco uses a temporary help agency at a cost of $200 in order to assist in earning revenues on December 27. The invoice from the temp agency is received on December 27, but it will not be paid until January 4.

Under the accrual method, on December 27 Servco:

- has incurred an expense of $200, and

- has incurred a liability of $200.

If accounting software is used to record the temp agency invoice, the following will occur automatically as of December 27:

- the income statement account Temporary Help Expense will be increased by $200, and

- the liability Accounts Payable will be increased by $200.

When Servco issues its check on January 4:

- the asset Cash will be decreased by $200, and

- the liability Accounts Payable will be decreased by $200.

Net Income

If Servco had only the two transactions described above, its net income under the accrual method for the day of December 27 will consist of the following:

- Earned revenue of $1,000

- Incurred an expense of $200

-

Earned a net income of $800 ($1,000 of revenues minus $200 of expenses).

[The cash method of accounting would have reported a much different picture:

- No revenue, expense or net income would have been reported on the December income statement.

- The revenues of $1,000 might be reported in February if the customer paid in 35 days.

- The expense of $200 will be reported in January when Servco pays the temp agency.]

Obviously, the accrual method does a better job of reporting what occurred on December 27, the date that Servco actually provided the services and incurred the expense.

Double-Entry, Debits and Credits

Double-Entry

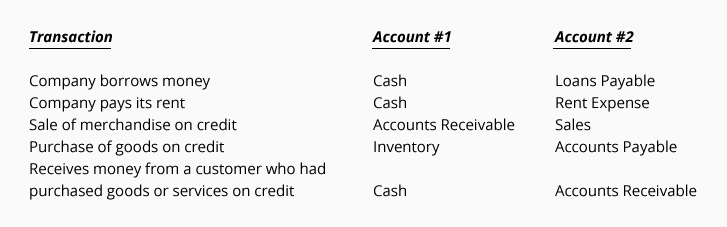

Except for some very small companies, the standard method for recording transactions is double entry. Double-entry bookkeeping or double-entry accounting means that every transaction will involve at least two accounts. To illustrate, here are a few transactions and the two accounts that will be affected:

Note: Double-entry bookkeeping means that every transaction will involve a minimum of two accounts.

Debits and Credits

The words debit and credit have been associated with double-entry bookkeeping and accounting for more than 500 years. Here are the meanings of those words:

debit: an entry on the left side of an account

credit: an entry on the right side of an account

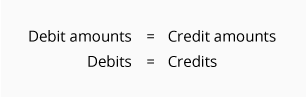

The debit and credit rule in double-entry bookkeeping can be stated several ways:

-

For each and every transaction, the total amount entered on the left side of an account (or accounts) must be equal to the total amount entered on the right side of another account (or accounts).

-

For each and every transaction, the total of the debit amounts must be equal to the total of the credit amounts.

-

Debits must equal credits.

In short…

Dependable accounting software will be written/coded to enforce the rule of debits equal to credits. In other words, a transaction will be accepted and processed only if the amount of the debits is equal to the amount of the credits.

The accuracy of accounting software will also ensure that the accounts and the trial balance will always be in balance. Here is an example of a partial trial balance:

Even though the accounting software has eliminated the clerical errors that occurred because amounts were handwritten and the account balances were calculated manually, some other errors can still occur. Here are some errors that will not be detected by the accounting software:

- An entire transaction (both the debit amount and the credit amount) was omitted.

- An entire transaction was entered twice.

- An incorrect amount was entered both as a debit and as a credit.

- An incorrect account was debited.

- An incorrect account was credited.

Even with the above errors, the trial balance will remain in balance. The reason is that the total of the debit balances will still be equal to the total of the credit balances.

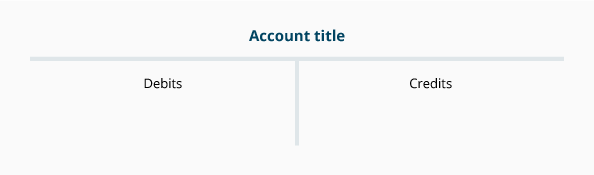

T-Accounts

To assist in visualizing the effect of recording a debit or credit amount and the resulting balances of general ledger accounts, it is helpful to draw a T-account, as shown here:

Debit amounts will be entered on the left side of the T-account, and credit amounts will be entered on the right side. The title of the account will appear at the top of each “T”.

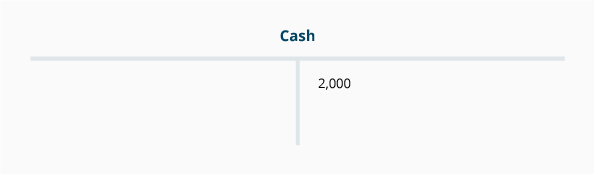

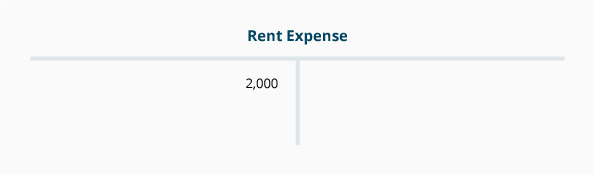

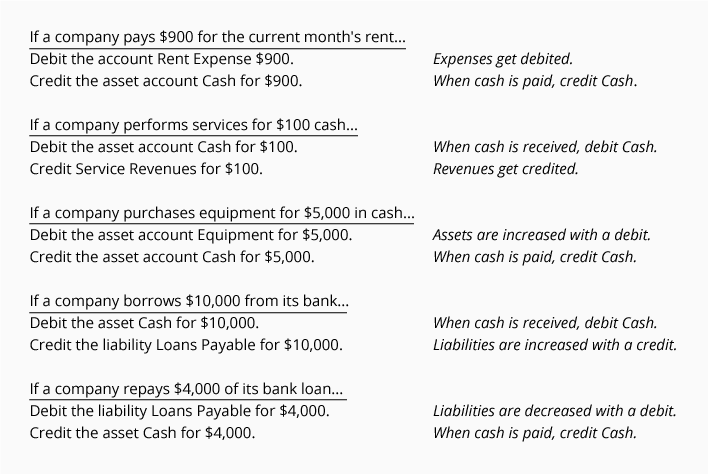

Since every transaction will involve at least two accounts, we recommend that you always begin by drawing two T-accounts. For example, if a company pays its rent of $2,000 for the current month, the transaction could be depicted with the following T-accounts:

Note that one T-account (Rent Expense) has a debit of 2,000 and that one T-account (Cash) has a credit amount of 2,000. Hence, the transaction had debits equal to credits.

General Ledger Accounts

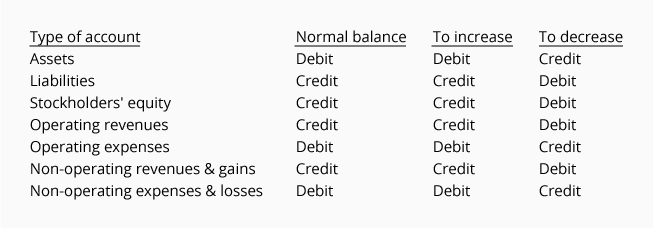

The accounts that are used to sort and store transactions are found in the company’s general ledger. The general ledger is often arranged according to the following seven classifications. (A few examples of the related account titles are shown in parentheses.)

- Assets (Cash, Accounts Receivable, Land, Equipment)

- Liabilities (Loans Payable, Accounts Payable, Bonds Payable)

- Stockholders’ equity (Common Stock, Retained Earnings)

- Operating revenues (Sales, Service Fees)

- Operating expenses (Salaries Expense, Rent Expense, Depreciation Expense)

- Non-operating revenues and gains (Investment Income, Gain on Disposal of Truck)

- Non-operating expenses and losses (Interest Expense, Loss on Disposal of Equipment)

Balance Sheet Accounts

The first three classifications are referred to as balance sheet accounts since the balances in these accounts are reported on the financial statement known as the balance sheet.

- Balance sheet accounts

- Assets

- Liabilities

- Stockholders’ (or Owner’s) equity

The balance sheet accounts are also known as permanent accounts (or real accounts) since the balances in these accounts will not be closed at the end of an accounting year. Instead, these account balances are carried forward to the next accounting year.

Income Statement Accounts

The four remaining classifications of accounts are referred to as income statement accounts since the amounts in these accounts will be reported on the financial statement known as the income statement.

- Income statement accounts

- Operating revenues

- Operating expenses

- Non-operating revenues and gains

- Non-operating expenses and losses

The income statement accounts are also known as temporary accounts since the balances in these accounts will be closed at the end of the accounting year. Each income statement account is closed in order to begin the next accounting year with a zero balance.

The year-end balances from all of the income statement accounts will be combined and entered as a single net amount in Retained Earnings (a balance sheet account within stockholders’ equity) or in a proprietor’s capital account.

Note: If an account has not had any activity in the current or recent periods, it is often omitted from the current general ledger.

Chart of Accounts

The chart of accounts is simply a list of all of the accounts that are available for recording transactions. This means that the number of accounts in the chart of accounts will be greater than the number of accounts in the general ledger. (The reason is that accounts with zero balances and no recent entries are often omitted from the general ledger until there is a transaction for the account.)

The chart of accounts is organized similar to the general ledger: balance sheet accounts followed by the income statement accounts. However, the chart of accounts does not contain any entries or account balances.

The chart of accounts allows you to find the name of an account, its account number, and perhaps a brief description. It is important to expand and/or alter the chart of accounts to accommodate the changes to an organization and when there is a need for improved reporting of information.

In some accounting software, the chart of accounts is also used to designate where an account will be reported in the financial statements.

Debits and Credits in the Accounts

If you already understand debits and credits, the following table summarizes how debits and credits are used in the accounts.

If you are not familiar with debits and credits or if you want a better understanding, we will provide a few insights to help you. You can also visit our Debits and Credits topic outline for further assistance.

Accounting Equation Can Help

The accounting equation is a central part of bookkeeping and accounting. It can also provide insights into debits and credits. The basic accounting equation is:

Assets = Liabilities + Stockholders’ equity (if a corporation)

or

Assets = Liabilities + Owner’s equity (if a sole proprietorship)

With double-entry accounting, the accounting equation should always be in balance. In other words, not only will debits be equal to credits, but the amount of assets will be equal to the amount of liabilities plus the amount of owner’s equity.

The accounting equation is also the framework of the balance sheet, one of the main financial statements. Hence the balance sheet must also be in balance.

We will use the accounting equation to explain why we sometimes debit an account and at other times we credit an account.

Assets are on the left side of the accounting equation.

Asset account balances should be on the left side of the accounts.

In the accounting equation you can see that assets are on the left side of the equation:

Earlier you learned that debit means left side. Recall our T-account that showed debits on the left side:

Hence, asset accounts such as Cash, Accounts Receivable, Inventory, and Equipment should have debit balances.

Liabilities are on the right side of the accounting equation.

Liability account balances should be on the right side of the accounts.

In the accounting equation you can see that liabilities are on the right side of the equation:

Earlier you learned that credit means right side. Recall our T-account that showed credits on the right side:

Thus liability accounts such as Accounts Payable, Notes Payable, Wages Payable, and Interest Payable should have credit balances.

Stockholders’ equity is on the right side of the accounting equation.

Stockholders’ equity account balances should be on the right side of the accounts.

In the accounting equation you can see that stockholders’ equity is on the right side of the equation:

Again, credit means right side and our T-account showed credits on the right side. This means that stockholders’ equity accounts such as Common Stock, Retained Earnings, and M J Smith, Capital should have credit balances.

Example

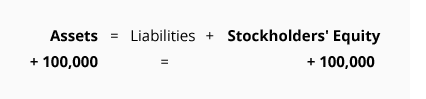

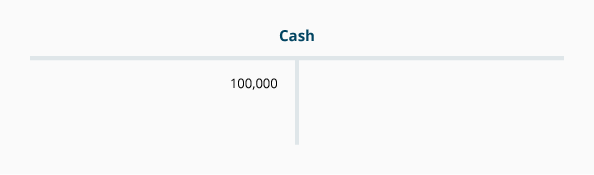

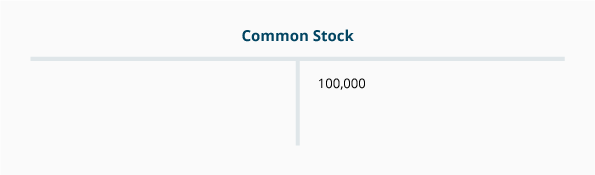

To demonstrate the debits and credits of double entry with a transaction, let’s assume that a new corporation is formed and the stockholders invest $100,000 in exchange for shares of common stock. There are two effects of this transaction:

- The corporation receives cash, which is recorded as a corporation asset.

- The corporation issues shares of common stock. The amount received for the shares will be recorded as part of the corporation’s stockholders’ equity.

Here’s how the transaction will impact the accounting equation and the company’s balance sheet:

Here is what will occur in the general ledger accounts:

If this transaction is entered in a general journal, it would appear as follows:

Revenues increase stockholders’ equity (which is on the right side of the accounting equation).

Therefore the balances in the revenue accounts will be on the right side.

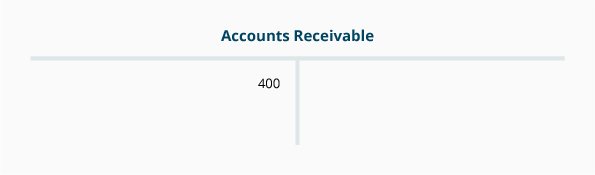

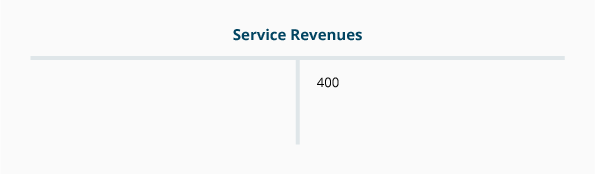

To illustrate, let’s assume that a company provides a service and bills the customer $400 with the amount due in 30 days. Two things occur:

- Revenues of $400 are earned and that causes stockholders’ equity to increase.

- The company earns the right to receive $400. This increases the company’s asset account Accounts Receivable.

Here’s the effect on the accounting equation and the company’s balance sheet as a result of earning the revenues:

Here is what occurs in the general ledger accounts:

Note: Even though stockholders’ equity will increase, the transaction is recorded in the account Service Revenues. The reason is that we want the amount of revenues to be reported on the current period’s income statement. (In other words, we temporarily credit Service Revenues instead of crediting the stockholders’ equity account Retained Earnings. At the end of the accounting year, the balances in all of the income statement accounts will be closed/transferred to Retained Earnings.)

If this transaction were entered in a general journal, it would appear as follows:

Expenses decrease stockholders’ equity (which is on the right side of the accounting equation).

Therefore expense accounts will have their balances on the left side.

To reduce the normal credit balance in stockholders’ equity accounts, a debit will be needed. Hence, the accounts such as Rent Expense, Advertising Expense, etc. will have their balances on the left side.

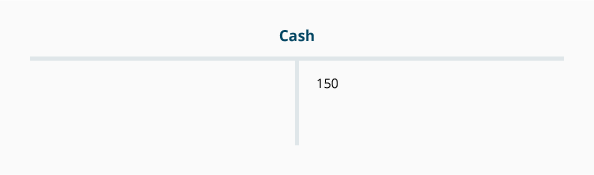

For example, when a company pays cash of $150 for advertising materials that are distributed immediately at a local event, two things occur:

- An expense of $150 occurred and the expense will cause stockholders’ equity to decrease.

- The company has reduced its asset Cash by $150.

The effect on the accounting equation and the company’s balance sheet is:

The effect on the company’s general ledger accounts is shown here:

Note: Even though this expense causes stockholders’ equity to decrease, the transaction is recorded in the account Advertising Expense. The reason is that we want the current period’s income statement to report this expense. (In other words, we temporarily debit Advertising Expense instead of debiting the stockholders’ equity account Retained Earnings. At the end of the accounting year, all of the balances in the income statement accounts will be closed/transferred to Retained Earnings.)

If this transaction were entered in a general journal, it would appear as follows:

A few tips about debits and credits:

- When cash is received, debit Cash.

- When cash is paid out, credit Cash.

- When revenues are earned, credit a revenue account.

- When expenses are incurred, debit an expense account.

Here are some common transactions with the appropriate debits and credits:

Asset Accounts

Asset accounts are one of the three major classifications of balance sheet accounts:

- Assets

- Liabilities

- Stockholders’ equity (or owner’s equity)

The ending balances in the balance sheet accounts will be carried forward to the next accounting year. Hence the balance sheet accounts are called permanent accounts or real accounts.

The asset accounts are usually listed first in the company’s chart of accounts and in the general ledger. In the general ledger the asset accounts will normally have debit balances.

The balances in some of the asset accounts will be combined and presented as a single amount when the balance sheet is prepared. For example, if a company has ten checking accounts, the balances will be combined and the total amount will be reported on the balance sheet as the asset Cash.

Assets include the things or resources that a company owns, that were acquired in a transaction, and have a future value that can be measured. Assets also include some costs that are prepaid or deferred and will become expenses as the costs are used up over time.

Here are some examples of asset accounts:

Descriptions of asset accounts

The following are brief descriptions of some common asset accounts.

Cash

Cash includes currency, coins, checking account balances, petty cash funds, and customers’ checks that have not yet been deposited. A company is likely to have a separate general ledger account for each checking account, petty cash fund, etc. but will combine the amounts and will report the total as Cash (or Cash and Cash Equivalents) on the balance sheet.

Short-term Investments

Short-term or temporary investments may include certificates of deposit, bonds, notes, etc. that will mature in less than one year. It may also include investments in the common or preferred stock of another corporation if the stock can be easily sold on a stock exchange.

Accounts Receivable

Accounts receivable is a right to receive an amount as the result of delivering goods or services on credit. Under the accrual method of accounting, Accounts Receivable is debited at the time of a credit sale. Later, when the customer pays the amount owed, the company will credit Accounts Receivable (and will debit Cash).

Allowance for Doubtful Accounts

The Allowance for Doubtful Accounts is a contra-asset account since its balance is intended to be a credit balance (or a zero balance). When the balance in this account is combined with the balance in Accounts Receivable, the resulting amount is known as the net realizable value of the receivables. The Allowance for Doubtful Accounts is used under the allowance method of reporting bad debts expense.

Accrued Revenues/Receivables

Under the accrual method of accounting, revenues are to be reported when goods or services have been delivered even if a sales invoice has not been generated. This account will report the amounts that a company has a right to receive but the sales invoices have yet to be prepared or entered in Accounts Receivable.

Prepaid Expenses

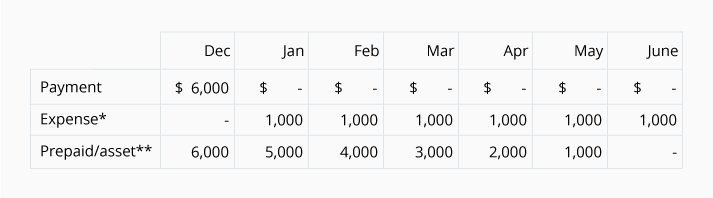

These are future expenses that have already been paid. The amounts appear as assets until the costs have been used up or expire. A common example of a prepaid expense is the payment for vehicle insurance. To illustrate this, let’s assume that on December 29, a new company pays $6,000 for the insurance covering its vehicles for the six-month period that will begin on January 1. As of December 31, the entire $6,000 will be a prepaid expense because none of the cost has expired. Since none of the cost expired in December, there is no insurance expense in December. The insurance expense will begin in January at a rate of $1,000 per month. This is depicted in the following chart:

*The expense is the amount that is expiring during the month.

**The prepaid amounts are the unexpired amounts and should be the balance in the asset account Prepaid Expenses or Prepaid Insurance at the end of each of the months.

Inventory

Inventory is the cost of goods that have been purchased or manufactured and have not yet been sold.

Supplies

Supplies could be office supplies, manufacturing supplies, packaging supplies or other supplies that are on hand. The cost of the supplies that remain on hand is reported as an asset.

Long-term Investments

This account or asset category will be reported on the balance sheet immediately following current assets. It may include investments in the common stock, preferred stock, and bonds of another corporation. It also includes real estate being held for sale and also the money that is restricted for a long-term purpose such as a building project or the repurchase of bonds payable. The cash surrender value of a life insurance policy owned by a company is also reported under this asset heading.

Land

This account represents the property portion of the balance sheet heading “Property, plant and equipment.” It reports the cost of land used in a business. Since land is assumed to last indefinitely, the cost of land is not depreciated.

Buildings

This account will report the cost of the building used in the business. The cost of buildings will be depreciated over their useful lives.

Equipment

This account reports the cost of the machinery and equipment used in the business. The cost of equipment will be depreciated over the equipment’s useful life.

Vehicles

This account reports the cost of trucks, trailers, and automobiles used in the business. The cost of vehicles is to be depreciated over the vehicles’ useful lives.

Furniture and Fixtures

This account reports the cost of desks, chairs, shelving, etc. that are used in the business. The cost of furniture and fixtures is to be depreciated over the useful lives.

Accumulated Depreciation

Accumulated Depreciation is known as a contra asset account because it has a credit balance instead of a debit balance that is typical for asset accounts. Whenever Depreciation Expense is debited for the periodic depreciation of the buildings, equipment, vehicles, etc. the account Accumulated Depreciation is credited. The credit balance in Accumulated Depreciation will continue to grow until an asset is sold or scrapped. However, the maximum amount of the credit balance is the cost of the asset(s).

Liability and Stockholders’ Equity Accounts

Liability Accounts

A company’s liability accounts appear in the chart of accounts, general ledger, and balance sheet immediately following the asset accounts. In the general ledger, the liability accounts will usually have credit balances.

Note: Liabilities are a company’s obligations. They are the amounts that the company owes. Liabilities also include amounts received from customers in advance of being earned.

Here are some examples of liability accounts:

- Short-term Loans Payable

- Current Portion of Long-term Debt

- Accounts Payable

- Accrued Expenses

- Unearned or Deferred Revenues

- Installment Loans Payable

- Mortgage Loans Payable

Descriptions of liability accounts

The following are brief descriptions of some common liability accounts.

Short-term Loans Payable

This account will report the amount of loans which will be due within one year of the date of the balance sheet.

Current Portion of Long-term Debt

This account or line description reports the principal portion of a long-term debt that will have to be paid within one year of the date of the balance sheet. (The portion of the debt that is not due within one year is reported as a noncurrent liability.)

Accounts Payable

Accounts Payable is the account containing the amounts owed to suppliers for invoices that have been approved and entered for payment. The balance in this account reports the amount of those invoices which are unpaid.

Accrued Expenses/Liabilities

Under the accrual method, the amounts in this account are owed but have not yet been recorded in Accounts Payable. This account could include the vendor invoices awaiting processing, employee wages and benefits earned but not yet recorded, and other expenses incurred but not yet recorded.

Unearned or Deferred Revenues

Unearned revenues reports the amounts received in advance of having been earned. For example, if a law firm requires that a client pay $4,000 in advance for future legal work, the law firm will record the cash of $4,000 and also the liability to deliver $4,000 of legal services. The law firm cannot report the $4,000 as revenue until it is earned. This liability account could have the title Unearned Revenues or Deferred Legal Fees. As the legal services are performed (earned), the law firm will reduce the liability account and will report the amount as revenues.

Installment Loans Payable

Installment loans are loans that require a series of payments. A common example is a three-year automobile loan that requires monthly payments. The principal due within one year of the balance sheet date will be reported as a current liability and the remainder of the principal owed will be reported as a noncurrent liability. (The future interest is not recorded as a liability, since it is not due or payable as of the date of the balance sheet.)

Mortgage Loans Payable

Mortgage loans are usually long-term loans with real estate pledged as collateral. The principal due within one year of the balance sheet date will be reported as a current liability and the remainder of the principal owed is reported as a noncurrent liability. (The future interest is not recorded as a liability, since it is not due or payable as of the date of the balance sheet.)

Stockholders’ Equity Accounts

The stockholders’ equity accounts of a corporation will appear in the chart of accounts, general ledger, and balance sheet immediately following the liability accounts. In the general ledger most of the stockholders’ equity accounts will have credit balances. The following are brief descriptions of typical stockholders’ equity accounts.

Paid-in Capital

Paid-in capital is a subheading within stockholders’ equity which indicates the amount paid to the corporation at the time that shares of stock were issued. Paid-in capital is also referred to as permanent capital. Every corporation will have common stock and a small percentage of corporations will have preferred stock in addition to common stock.

The paid-in capital accounts report the amounts received when the corporation’s stock was issued. Often there are two accounts for the common stock:

- Par value of the common stock, and

- Paid-in capital in excess of the par value of the common stock

If a corporation also issued preferred stock, there will also be two additional accounts.

Common Stock

If a corporation’s common stock has a par value or a stated value, only the par or stated value of the shares issued will be recorded in this account. However, if a corporation’s common stock has neither a par value nor a stated value, the entire amount received by the corporation at the time that the shares were issued will be recorded in this account.

Paid-in Capital in Excess of Par Value – Common Stock

When a corporation issues common stock, the amount received minus the par value or stated value is recorded in this account. (The par value of common stock is recorded in the account Common Stock.)

Retained Earnings

Generally, the amount of a corporation’s retained earnings is the cumulative amount of earnings (net income) since the corporation was formed minus the cumulative amount of dividends that have been declared since the corporation was formed.

The current accounting period’s earnings (or net income) will be added to this account and the current period’s dividends will be deducted.

Note: Revenues will cause retained earnings to increase, while expenses will cause retained earnings to decrease.

Retained earnings is a component of stockholders’ equity, but it is separate from paid-in capital. Hence, the amounts reported under retained earnings are not considered to be permanent capital.

Income Statement Accounts

The income statement accounts are categorized in a variety of ways. Here are the classifications we will be using:

- Operating revenues

- Operating expenses

- Other revenues and gains

- Other expenses and losses

The amounts in these accounts at the end of an accounting year will not be carried forward to the subsequent year. Rather, the balances in the income statement accounts will be transferred to Retained Earnings (for a corporation) or to the owner’s capital account (for a sole proprietorship). This will allow for all of the income statement accounts to begin each accounting year with zero balances. This explains why the income statement accounts are referred to as temporary accounts.

Operating Revenues

Operating revenues are the amounts earned from carrying out the company’s main activities. For example, the sales of merchandise are a retailer’s operating revenues.

A few examples of accounts for recording operating revenues include:

- Sales

- Sales Revenues

- Service Revenues

- Fees Earned

- Sales – Product Line #1

- Sales – Product Line #2

The revenue accounts are expected to have credit balances (since revenues cause the stockholders’ or owner’s equity to increase). Contra revenue accounts such as Sales Returns and Allowances and Sales Discounts will have debit balances.

Under the accrual method of accounting, revenues are reported as of the date the goods are sold or the services have been performed. If a service is provided on December 27, but the customer is allowed to pay in February, the revenues are reported on the income statement that includes December 27.

At the end of the accounting year, the balance in each of the accounts for recording operating revenues will be closed in order to start the next accounting year with a zero balance.

Operating Expenses

Operating expenses are the expenses incurred in earning operating revenues. For example, advertising expense is one of the operating expenses of a retailer.

A few of the many accounts used to record operating expenses include:

- Cost of Goods Sold

- Cost of Goods Sold – Product Line #1

- Salaries Expense

- Fringe Benefit Expense

- Rent Expense

- Utilities Expense

- Utilities Expense – Store #45

- Depreciation Expense – Buildings

- Depreciation Expense – Equipment

- Repairs Expense

The accounts for operating expenses should have debit balances.

Under the accrual method of accounting, the expenses should be reported in the same accounting period as the related revenues. If that is not certain, then an expense should be reported in the accounting period in which its cost expires or is used up.

Expenses are often organized by function such as manufacturing, selling, and general administrative. At other times expenses will be organized by responsibility such as Department #1, Sales Region #5, Warehouse #2, Legal Department, etc.

At the end of the accounting year, the balance in each of the accounts used for recording operating expenses will be closed in order to start the next accounting year with a zero balance.

Non-Operating Revenues and Gains

Revenues earned outside of a company’s main business activities are referred to as non-operating revenues or as other revenues. For example, the interest earned by a retailer on its idle cash balances is part of non-operating or other revenues.

Gains often occur when a company sells an asset that was used in the business, and the cash received was greater than the asset’s carrying amount on the company’s books. For example, if a company car is sold for $10,000 and its book value is $9,000, there will be a gain of $1,000.

The accounts that report non-operating revenues, other revenues, and gains are expected to have credit balances since they cause stockholders’ equity to increase.

Non-Operating Expenses and Losses

The expenses incurred in order to earn non-operating revenues are reported as non-operating expenses or other expenses. In addition, interest expense for a retailer is a non-operating expense or other expense. (On the other hand, the interest expense paid by a bank for the use of depositors’ money is one of the bank’s operating expenses.)

Losses are reported when a company disposes of a long-term asset for the cash, and the amount of cash received is less than the book value of the asset. For example, if a company car is sold for $7,500 and its book value is $9,000, a loss of $1,500 will be reported. Another example of a loss is the loss from a lawsuit.

The accounts for non-operating expenses and losses will have debit balances since they cause stockholders’ equity to decrease.

Recording Transactions

With sophisticated accounting software and inexpensive computers, it is no longer practical for most businesses to manually enter transactions into journals and then to post to the general ledger accounts and subsidiary ledger accounts. Today, software such as QuickBooks* will update the relevant accounts and provide more information with a minimum of data entry.

*QuickBooks is a registered trademark of Intuit Inc. AccountingCoach LLC is not affiliated with Intuit Inc. and does not receive any affiliate marketing commissions from Intuit.

In this section we will highlight how the accounting software will capture financial transactions and then automatically update the general ledger and store the information for management’s future use.

Accounts payable

When accounting software is used to enter the invoices received from suppliers (vendor invoices), the software will update Accounts Payable and will require that the account or accounts that should be debited be entered as well. The accounting software’s vendor files also allow a company to prepare purchase orders, receiving tickets and to pay the vendors’ invoices.

A company should have internal controls so that only legitimate invoices are recorded and paid.

Check writing

When the accounting software is used to write checks, the software will automatically credit the Cash account and will require that another account be designated for the debit. An additional benefit is that the amounts will move electronically and the account balances will be automatically calculated with speed and accuracy.

Again, a company should have internal controls to ensure that only legitimate payments are processed.

Sales on credit

When the accounting software is used to prepare a sales invoice for a customer who purchased on credit, the customer’s detail will be updated, the general ledger account Sales will be credited and the general ledger account Accounts Receivable will be debited. Statements for each customer and an aging of all of the accounts receivable can be printed with the click of a button.

Payroll

Another source of financial transactions is the company’s payroll. While many companies process payroll on their accounting software, others opt to outsource payroll to companies such as ADP, Paychex, Intuit, or local firms.

(AccountingCoach is not affiliated with any of these companies and it does not receive affiliate marketing commissions from any of them.)

Note: To learn more about payroll, visit our Explanation and Quiz for this topic.

Bank Reconciliation

The purpose of the bank reconciliation is to be certain that the financial statements are reporting the correct amount of cash and the proper amounts for any related accounts (since every transaction affects a minimum of two accounts).

The bank reconciliation process involves:

- Comparing the following amounts

- The balance on the bank statement

- The balance in the company’s general ledger account. (The account title might be Cash – checking.)

- Determining the reasons for the difference in the amounts shown in 1.

The common reasons for a difference between the bank balance and the general ledger book balance are:

- Outstanding checks (checks written but not yet clearing the bank)

- Deposits in transit (company receipts that are not yet deposited in the bank)

- Bank service charges and other bank fees

- Check printing charges

- Errors in entering amounts in the company’s general ledger

The outstanding checks and deposits in transit do not involve errors by either the company or the bank. Since these items are already recorded in the company’s accounts, no additional entries to the company’s general ledger accounts will be needed.

Bank charges, check printing fees and errors in the company’s accounts do require the company to make accounting entries. The company should make the entries before the financial statements are prepared since a minimum of two accounts have the incorrect balances (due to double-entry accounting). Here is an entry for a bank service charge that was listed on the bank statement:

If the reconciliation reveals that an incorrect amount has been recorded in the company’s Cash account, perhaps the easiest way to correct the error is to remove the incorrect amount and then enter the correct amount.

Accounting software is likely to include a feature for reconciling the bank statement.

Note: To learn more about bank reconciliation, visit our Explanation and Quiz for this topic.

Adjusting Entries

Why adjusting entries are needed

In order for a company’s financial statements to be complete and to reflect the accrual method of accounting, adjusting entries must be processed before the financial statements are issued. Here are three situations that describe why adjusting entries are needed:

Situation 1

Not all of a company’s financial transactions that pertain to an accounting period will have been processed by the accounting software as of the end of the accounting period. For example, the bill for the electricity used during December might not arrive until January 10. (The reason for the 10-day lag is that the electric utility reads the meters on January 1 in order to compute the electricity actually used in December. Next the utility has to prepare the bill and mail it to the company.)

Situation 2

Sometimes a bill is processed during the accounting period, but the amount represents the expense for one or more future accounting periods. For example, the bill for the insurance on the company’s vehicles might be $6,000 and covers the six-month period of January 1 through June 30. If the company is required to pay the $6,000 in advance at the end of December, the expense needs to be deferred so that $1,000 will appear on each of the monthly income statements for January through June.

Situation 3

Something similar to Situation 2 occurs when a company purchases equipment to be used in the business. Let’s assume that the equipment is acquired, paid for, and put into service on May 1. However, the equipment is expected to be used for ten years. If the cost of the equipment is $120,000 and will have no salvage value, then each month’s income statement needs to report $1,000 for 120 months in order to report depreciation expense under the straight-line method.

These three situations illustrate why adjusting entries need to be entered in the accounting software in order to have accurate financial statements. Unfortunately the accounting software cannot compute the amounts needed for the adjusting entries. A bookkeeper or accountant must review the situations and then determine the amounts needed in each adjusting entry.

Steps for Recording Adjusting Entries

Some of the necessary steps for recording adjusting entries are:

- You must identify the two or more accounts involved

- One of the accounts will be a balance sheet account

- The other account will be an income statement account

- You must calculate the amounts for the adjusting entries

- You will enter both of the accounts and the adjustment in the general journal

- You must designate which account will be debited and which will be credited.

Types of Adjusting Entries

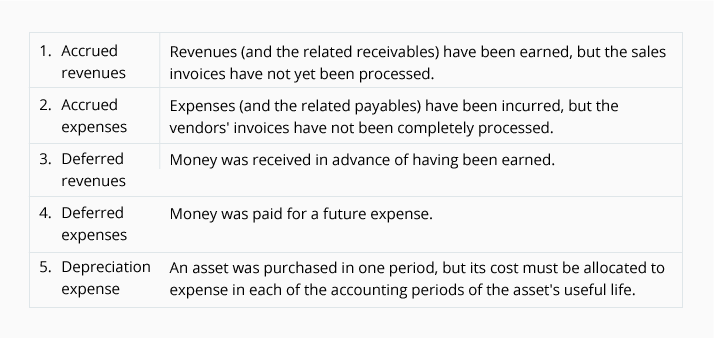

We will sort the adjusting entries into five categories:

1. Accrued revenues

Under the accrual method of accounting, a business is to report all of the revenues (and related receivables) that it has earned during an accounting period. A business may have earned fees from having provided services to clients, but the accounting records do not yet contain the revenues or the receivables. If that is the case, an accrual-type adjusting entry must be made in order for the financial statements to report the revenues and the related receivables.

If a business has earned $5,000 of revenues, but they are not recorded as of the end of the accounting period, the accrual-type adjusting entry will be as follows:

2. Accrued expenses

Under the accrual method of accounting, the financial statements of a business must report all of the expenses (and related payables) that it has incurred during an accounting period. For example, a business needs to report an expense that has occurred even if a supplier’s invoice has not yet been received.

To illustrate, let’s assume that a company utilized a worker from a temporary personnel agency on December 27. The company expects to receive an invoice on January 2 and remit payment on January 9. Since the expense and the payable occurred in December, the company needs to accrue the expense and liability as of December 31 with the following adjusting entry:

3. Deferred revenues

Under the accrual method of accounting, the amounts received in advance of being earned must be deferred to a liability account until they are earned.

Let’s assume that Servco Company receives $4,000 on December 10 for services it will provide at a later date. Prior to issuing its December financial statements, Servco must determine how much of the $4,000 has been earned as of December 31. The reason is that only the amount that has been earned can be included in December’s revenues. The amount that is not earned as of December 31 must be reported as a liability on the December 31 balance sheet.

If $3,000 has been earned, the Service Revenues account must include $3,000. The remaining $1,000 that has not been earned will be deferred to the following accounting period. The deferral will be evidenced by a credit of $1,000 in a liability account such as Deferred Revenues or Unearned Revenues.

The adjusting entry for this deferral depends on how the receipt of $4,000 was recorded on December 10. If the receipt of $4,000 was recorded with a credit to Service Revenues (and a debit to Cash), the December 31 adjusting entry will be:

If the entire receipt of $4,000 had been credited to Deferred Revenues on December 10 (along with a debit to Cash), the adjusting entry on December 31 would be:

4. Deferred expenses

Under the accrual method of accounting, any payments for future expenses must be deferred to an asset account until the expenses are used up or have expired.

To illustrate, let’s assume that a new company pays $6,000 on December 27 for the insurance on its vehicles for the six-month period beginning January 1. For December 27 through 31, the company should have an asset Prepaid Insurance or Prepaid Expenses of $6,000.

In each of the months January through June, the company must reduce the asset account by recording the following adjusting entry:

5. Depreciation expense

Depreciation is associated with fixed assets (or plant assets) that are used in the business. Examples of fixed assets are buildings, machinery, equipment, vehicles, furniture, and other constructed assets used in a business and having a useful life of more than one year. (However, land is not depreciated.)

Depreciation allocates the asset’s cost (minus any expected salvage value) to expense in the accounting periods in which the asset is used. Hence, office equipment with a useful life of 5 years and no salvage value will mean monthly depreciation expense of 1/60 of the equipment’s cost. A building with a useful life of 25 years and no salvage value will result in a monthly depreciation expense of 1/300 of the building’s cost.

Note: To learn more about adjusting entries, visit our Explanation and Quiz for this topic.

Reversing Entries

The first two categories of adjusting entries that we had discussed above were:

- Accrued revenues

- Accrued expenses

These categories are also referred to as accrual-type adjusting entries or simply accruals. Accrual-type adjusting entries are needed because some transactions had occurred but the company had not entered them into the accounts as of the end of the accounting period. In order for a company’s financial statements to include these transactions, accrual-type adjusting entries are needed.

In all likelihood, an actual transaction (that required an accrual-type adjusting entry) will get routinely processed and recorded in the next accounting period. This presents a potential problem in that the transaction could get entered into the accounting records twice: once through the adjusting entry and also when it is routinely processed in the subsequent accounting period. The purpose of reversing entries is to remove the accrual-type adjusting entries once the financial statements are distributed.

Therefore, reversing entries will be dated as of the first day of the accounting period immediately following the period of the accrual-type adjusting entries. In other words, for a company with accounting periods which are calendar months, an accrual-type adjusting entry dated December 31 will be reversed on January 1.

To illustrate, let’s assume that the company had accrued repairs expenses using the following adjusting entry on December 31:

This accrual-type adjusting entry was needed so that the December repairs would be reported as 1) part of the expenses on the December income statement, and 2) a liability on the December 31 balance sheet.

In a manual accounting system, after the financial statements for December are issued, closing entries dated December 31 will transfer the balances from the income statement accounts (such as Repairs Expense) to a balance sheet capital account. (If the business is a regular corporation, the capital account is Retained Earnings. If the business is a sole proprietorship, the account is the owner’s capital account.)

On January 1, the following reversing entry is recorded in order to remove the accrual-type adjusting entry of December 31:

The reversing entry removes the liability established on December 31 and creates a credit balance in the Repairs Expense account on January 1. When the vendor’s invoice is processed in January, it can be debited to Repairs Expenses (as would normally happen). If the vendor’s invoice is $6,000 the balance in the account Repairs Expenses will show a $0 balance after the invoice is entered. (The $6,000 credit from the reversing entry on January 1, plus the $6,000 debit from the vendor’s invoice equals $0.) Zero is the correct amount because the expense of $6,000 belonged in December and was reported in December as the result of the December 31 adjusting entry.

Some accounting software will allow you to indicate the adjusting entries you would like to have reversed automatically in the next accounting period.

Balance Sheet

The balance sheet is one of the five main financial statements of a business:

The balance sheet reports a company’s assets, liabilities, and stockholders’ equity as of a moment in time. (The other three financial statements report amounts for a period of time such as a year, quarter, month, etc.) The balance sheet is also known as the statement of financial position and it reflects the accounting equation:

Assets = Liabilities + Stockholders’ Equity.

Bankers will look at the balance sheet to determine the amount of a company’s working capital, which is the amount of current assets minus the amount of current liabilities. They will also review the assets and the liabilities and compare these amounts to the amount of stockholders’ equity.

When a balance sheet reports at least one additional column of amounts from an earlier balance sheet date, it is referred to as a comparative balance sheet.

Balance Sheet Classifications

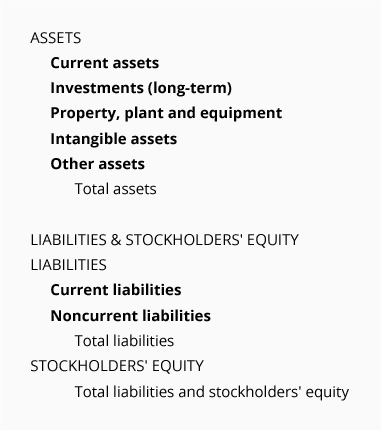

Typically, companies issue a classified balance sheet. This means that the amounts are presented according to the following classifications:

Descriptions of the balance sheet classifications

The following are brief descriptions of the classifications usually found on a company’s balance sheet.

Current assets

Generally, current assets include cash and other assets that are expected to turn to cash within one year of the date of the balance sheet. Examples of current assets are cash and cash equivalents, short-term investments, accounts receivable, inventory and prepaid expenses.

Investments

This classification is the first of the noncurrent or long-term assets. Included are long-term investments in other companies, the cash surrender value of life insurance, bond sinking funds, real estate held for sale, and cash that is restricted for construction of plant and equipment.

Property, plant and equipment

This category of noncurrent assets includes the cost of land, buildings, machinery, equipment, furniture, fixtures, and vehicles used in the operations of a business. Except for land, these assets will be depreciated over their useful lives.

Intangible assets

Intangible assets include goodwill, trademarks, patents, copyrights and other non-physical assets that were acquired at a cost. The amount reported is their cost to acquire minus any amortization or write-down due to impairment. Valuable trademarks and logos that were developed by a company through years of advertising are not reported because they were not purchased from another person or company.

Other assets

This category often includes costs that have been paid but are being expensed over a period greater than one year. Examples include bond issue costs and certain deferred income taxes.

Current liabilities

Current liabilities are obligations of a company that are payable within one year of the date of the balance sheet (and will require the use of a current asset or will be replaced with another current liability).

Current liabilities include loans payable that will be due within one year of the balance sheet date, the current portion of long-term debt, accounts payable, income taxes payable and liabilities for accrued expenses.

Noncurrent liabilities

These are also referred to as long-term liabilities. In other words, these obligations will not be due within one year of the balance sheet date. Examples include portions of automobile loans, portions of mortgage loans, bonds payable, and deferred income taxes.

Stockholders’ equity

This section of the balance sheet consists of the following major sections:

- Paid-in capital (the amounts paid by investors when the original shares of a corporation were issued)

- Retained earnings (the earnings of the corporation since it began minus the amounts that were distributed in the form of dividends to the stockholders)

- Treasury stock (a subtraction that represents the amount paid to repurchase the corporation’s own stock)

Note: To learn more about the balance sheet, visit our Explanation and Quiz for this topic.

Income Statement

The income statement is also known as the statement of operations, the profit and loss statement, or P&L. It presents a company’s revenues, expenses, gains, losses and net income for a specified period of time such as a year, quarter, month, 13 weeks, etc.

Income Statement Formats

There are two formats for presenting a company’s income statement:

- Multiple-step

- Single-step

The difference in formats has to do with the number of subtractions and subtotals that appear on the income statement before getting to the company’s bottom line net income.

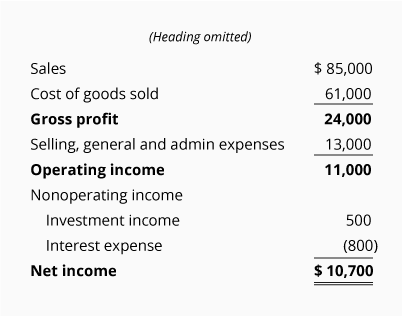

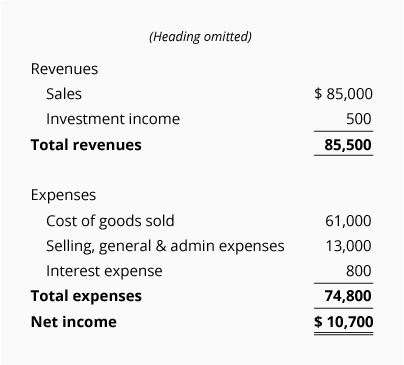

Multiple-step income statement

Note that in the following multi-step income statement, there are three subtractions:

- The first subtraction results in the subtotal gross profit.

- The second subtraction results in the subtotal operating income.

- The third subtraction provides the bottom line net income.

Single-step income statement

In the single-step format, the income statement will have only one subtraction—all of the expenses (both operating and non-operating) are subtracted from all of the revenues (both operating and non-operating). In this format, there is no subtotal for gross profit or operating income. The bottom line, net income, results from a single subtraction (a single step) as shown here:

Balance Sheet and Income Statement are Linked

As we had discussed earlier, revenues cause stockholders’ equity to increase while expenses cause stockholders’ equity to decrease. Therefore, a positive net income reported on the income statement (which is the result of revenues being greater than expenses) will cause stockholders’ equity to increase. A negative net income will cause stockholders’ equity to decrease.

The income statement accounts are temporary accounts because their balances will be closed at the end of each accounting year to the stockholders’ equity account Retained Earnings. (The balances in a sole proprietorship’s income statement accounts will be closed to the owner’s capital account.)

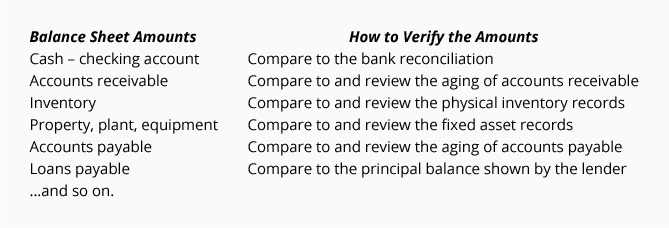

The link between the balance sheet and income statement is helpful for bookkeepers and accountants who want some assurance that the amount of net income appearing on the income statement is correct. If you verify the ending balances in the relatively few balance sheet accounts, you can have confidence that the income statement has the proper net income. Hence, you are wise to establish a routine to verify all of the balance sheet amounts.

Note: This technique does not guarantee that the details within the income statement are perfect.

Here is our suggestion for reviewing the balance sheet amounts.

Additional review

Another review that should be done routinely is to compare each item on the income statement to the same item on an earlier income statement. For example, the amounts for the 5-month period of the current year should be compared to the 5-month period of the previous year. If budgets are prepared, also compare this year’s actual amounts for the 5-month period to the budgeted amounts for this year’s 5-month period.

The same holds for the balance sheet: compare the recent amounts to the amounts on the balance sheet from a year earlier and from a month earlier.

Cash Flow Statement

While the balance sheet and the income statement are the most frequently referenced financial statements, the statement of cash flows or cash flow statement is a very important financial statement.

The cash flow statement is important because the income statement and balance sheet are normally prepared using the accrual method of accounting. Hence the revenues reported on the income statement were earned but the company may not have received the money from its customers. (Many times companies allow customers to pay in 30 days or 60 days and often customers pay later than the agreed upon terms.) Similarly the expenses that are reported on the income statement have occurred, but the company may not have paid for the expense in the same period. In order to understand how cash has changed, and because many believe that “cash is king” the cash flow statement should be distributed and read at the same time as the income statement and balance sheet.

Format of the Cash Flow Statement

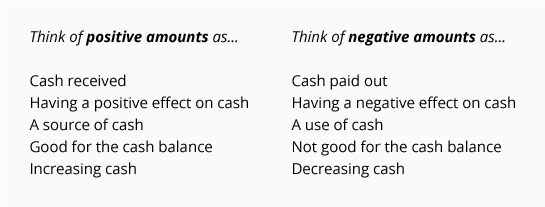

Within the cash flow statement, the cash receipts or cash inflows are reported as positive amounts. The cash paid out or cash outflows are reported as negative amounts.

The following table provides various ways for you to think of the positive and negative amounts that are shown on the cash flow statement:

The net total of all of the positive and negative amounts reported on the cash flow statement should equal the change in the amount of the company’s cash and cash equivalents. (The company’s cash and cash equivalents are reported on its balance sheets.)

The cash inflows and cash outflows which explain the change in a company’s cash and cash equivalents are reported in three main sections of the cash flow statement:

- Operating activities

- Investing activities

- Financing activities

In addition to the three main sections, the cash flow statement requires the following disclosures:

- the amount of interest paid

- the amount of income taxes paid

- exchanges of major items that did not involve cash (such as exchanging land for common stock, converting bonds into common stock, etc.).

1. Operating activities

The cash flows reported in the operating activities section of the cash flow statement can be presented using one of two methods:

- Direct method

- Indirect method

The direct method is recommended by the FASB. However, a survey of 500 annual reports of large U.S. corporations revealed that only about 1% had used the recommended direct method. Nearly all of the U.S. corporations in the survey used the indirect method. Hence, we will limit our discussion to the indirect method.

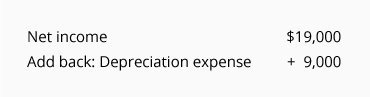

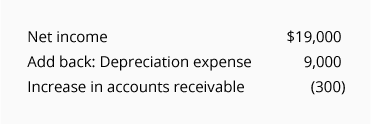

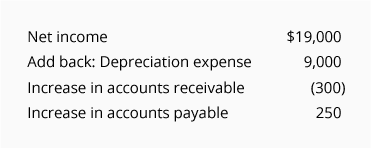

When the indirect method is used, the first section of the cash flow statement, Cash Flows from Operating Activities, begins with the company’s net income (which is the bottom line of the income statement). Since the net income was computed using the accrual method of accounting, it needs to be adjusted in order to reflect the cash received and paid.

The very first adjustment involves depreciation. The amount of Depreciation Expense reported on the income statement had reduced the company’s net income, but the depreciation entry did not involve cash. (The journal entry for the current period’s depreciation was a debit to Depreciation Expense and a credit to Accumulated Depreciation. Cash was not used.) Since the depreciation expense reduced net income, but did not use any cash, the amount of depreciation expense is added back to the net income amount.

So far, the Cash Flows from Operating Activities is $28,000

Any amortization or depletion expense is also added back.

Next, the operating activities will adjust the net income to reflect the changes in the amounts of current assets and current liabilities during the accounting period. For example, if accounts receivable increased from $9,500 to $9,800 during the period, we conclude that the company did not collect cash for all of the sales revenues shown on the income statement. Not collecting all of the sales amounts (or seeing accounts receivable increase) is viewed as negative for the company’s cash. Hence the $300 increase in accounts receivable is shown as a negative adjustment of $300:

So far, the Cash Flows from Operating Activities is $27,700

If accounts payable increased from $3,100 to $3,350 during the period, that indicates that the company did not pay all of its expenses. Not paying the bills is good for the company’s cash. Hence, the $250 increase in accounts payable will be shown as a positive amount:

So far, the Cash Flows from Operating Activities is $27,950

The changes in the current asset and the current liability accounts are reported as adjustments to the company’s net income in the operating activities section—except that the change in short-term notes payable will be reported in the financing activities section.

2. Investing activities

The purchasing and selling of long-term assets are reported in the second section of the cash flow statement, investing activities.

The cash flows that involve long-term assets include:

- The cash received from selling long-term assets. These are reported as positive amounts.

- The cash used to purchase long-term assets. These are reported as negative amounts.

3. Financing activities

The changes in the noncurrent liabilities, stockholders’ (or owner’s) equity, and short-term loans are reported in the financing activities section of the cash flow statement.

The positive amounts in the financing activities section could indicate that cash was received from:

- Issuing bonds payable

- Borrowing through other long-term loans

- Issuing shares of stock

- Borrowing through short-term loans

The negative amounts indicate that cash was used for:

- Retiring (paying off) long-term debt

- Purchasing shares of the company’s stock (treasury stock)

- Paying dividends to stockholders

- Repaying short-term loans

Other

At the bottom of the cash flow statement, the net totals of the three sections are reconciled with the change in the cash and cash equivalents that are reported on the company’s balance sheet.

The reporting requirements for the cash flow statement also include disclosing the amounts paid for interest and income taxes and significant noncash investing and financing activities. (Two examples of noncash investing and financing activities are converting bonds to common stock and exchanging bonds payable for land.)

Statement of Stockholders’ Equity

The fourth financial statement is the statement of stockholders’ equity. This statement lists the changes to the stockholders’ equity section of the balance sheet during the current accounting period.

A common format of the statement of stockholders’ equity is shown here:

To see additional examples of the statement of stockholders’ equity we recommend that you identify a few U.S. corporations with stock that is publicly traded. On each corporation’s website, select Investor Relations and then select each corporation’s Form 10-K (the annual report to the Securities and Exchange Commission). Go to the section of the 10-K which presents the corporation’s financial statements and view the statement of stockholders’ equity.

Closing Cut-Off

At a minimum of once per year, companies must prepare financial statements. In addition, companies often prepare quarterly and monthly financial statements which are referred to as interim financial statements.

For any of the financial statements to be accurate it is necessary to have a proper cut-off. This means including all of a company’s business transactions in the proper accounting period. For example, the electricity bill arriving on January 10 might be the cost of the electricity that was actually used in December. (The time lag resulted from the utility company reading the electric meters and preparing and mailing the bill.) Hence under the accrual method of accounting, the bill received on January 10 needs to be included in December’s expenses and must also be reported by the company as a liability as of December 31.

Similarly, the hourly payroll processed during the first few days in January and paid on January 6 is likely to include the cost of employees working during the last few days in December. The cost of the hours worked through December 31 must be included in the company’s December expenses and in the liabilities as of December 31.

As you read the previous paragraph, you may have been reminded of our discussion of adjusting entries. That’s because the adjusting entries are part of each period’s closing process. The adjusting entries are prepared in order to report a company’s revenues and expenses in the proper accounting period.

The closing process

To achieve a proper cut-off and to distribute the financial statements in a timely manner, it is helpful to have a timeline (or PERT chart) that indicates the necessary steps in the closing process. The timeline will indicate what needs to be done and the sequence in which things need to occur. It will also reveal what is preventing the financial statements from being distributed sooner.

In addition, a checklist of the closing tasks should be prepared and distributed to the appropriate employees as to what is required, who is responsible, and the day it is due.

If some journal entries must be written every month, it is helpful to assign journal entry numbers to these standard journal entries or recurring journal entries. For example, a company may designate JE33 (Journal Entry #33) to be the recurring accrual of expenses that have occurred but have not yet been recorded in Accounts Payable as of the end of a month. Perhaps the timeline/checklist will indicate that JE33 must be submitted by the accounts payable clerk six days after each month ends. The company may also have its computer automatically prepare JE34 which is the entry that automatically reverses the previous month’s accrual entry JE33.

Some recurring journal entries will have the same amount each month. For example, a company’s JE10 might be $10,800 every month of the year for the company’s depreciation expense. (Some companies will refer to the entries that have the same amounts and accounts every month as standard entries.)

Another recurring entry may involve the same accounts each month, but the amounts will vary from month to month. For example, a company’s JE03 might be the recurring monthly entry for bad debts expense. The company has determined in advance that the amount of JE03 will be 0.002 of the company’s monthly credit sales. Since the amount of sales is different every month, the amounts on JE03 will be different each month.

Having entry numbers and standard entries should help to make the monthly closings more routine and efficient.

Importance of Controls

The use of accounting software has eliminated some of the tedious tasks previously associated with bookkeeping. This could result in fewer people involved in the bookkeeping, accounting and administrative tasks. A side effect of fewer people handling more tasks is the potential for concealing some dishonest activity. For example, if the person who processes the cash receipts is also the person that records the amounts in customers’ accounts, stealing some cash will be easier than if the tasks were separated. Having a third person mailing statements to customers with instructions to report any discrepancies to a fourth person will further safeguard the company’s assets.

Accountants refer to the practices and policies for safeguarding assets as internal controls. Very large corporations may have a staff of internal auditors that ensure there are controls in place (including the separation of duties) so that fraud and misappropriation will not occur. Small companies or organizations with a small staff are therefore at a disadvantage. Nonetheless owners and managers of even the smallest companies and organizations must be aware of the need for internal controls. Here is a partial list of some internal controls that smaller organizations can implement:

- Separate the handling of cash from the person processing accounts receivable.

- Have the bank statement reconciled by someone who does not process the receipts or record the amounts in the general ledger cash account.

- Have the owner of a small company approve all purchase orders.

- Have the owner of a small company review all payments and sign all checks.

- Have all credit memos to customers be approved by the owner.

We are not experts in internal controls, but we realize their importance. We strongly recommend that you seek assistance from your professional accountant regarding internal controls that are appropriate for your business or organization.

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Bookkeeping materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.