Introduction

Standard costing is an important subtopic of cost accounting. Historically, standard costs have been associated with a manufacturing company’s costs of direct materials, direct labor, and manufacturing overhead.

Rather than assigning the actual costs of direct materials, direct labor, and manufacturing overhead to a product, some manufacturers assign the expected or standard costs. This means that a manufacturer’s inventories and cost of goods sold will begin with amounts that reflect the standard costs, not the actual costs, of a product. Since a manufacturer must pay its suppliers and employees the actual costs, there are almost always differences between the actual costs and the standard costs, and the differences are noted as variances.

NOTE:

Standard costs can also be thought of as:

- Planned costs

- Expected costs

- Budgeted costs

- “Should be” costs

- Benchmark costs

Standard costing (and the related variances) is a valuable management tool. If a variance arises, it tells management that the actual manufacturing costs are different from the standard costs. Management can then direct its attention to the cause of the differences from the planned amounts.

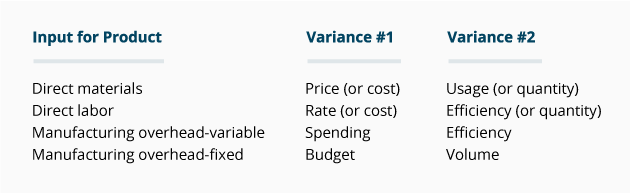

If we assume that a company uses the perpetual inventory system and that it carries all of its inventory accounts at standard cost (including Direct Materials Inventory or Stores), then the standard cost of a finished product is the sum of the standard costs of these inputs:

- Direct materials

- Direct labor

- Manufacturing overhead

- Variable manufacturing overhead

- Fixed manufacturing overhead

Usually there will be two variances computed for each input:

Since the calculation of variances can be difficult, we developed several business forms (for PRO members) to help you get started and to understand what the variances tell us. Learn more about AccountingCoach PRO.

Since the calculation of variances can be difficult, we developed several business forms to help you get started and to understand what the variances tell us.

Note: Our Guide to Managerial & Cost Accounting is designed to deepen your understanding of topics such as product costing, overhead cost allocations, estimating cost behavior, costs for decision making, and more. It is only available when you join AccountingCoach PRO.

WATCH NOW

Advance Your Career with Our PRO Training

Sample Standards Table

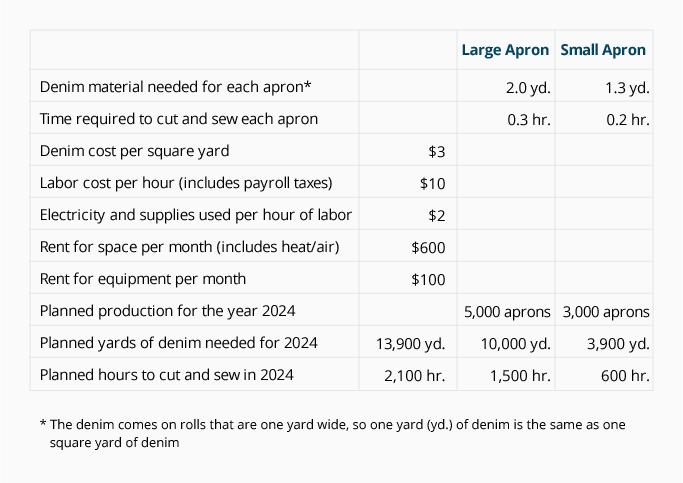

Let’s assume that your Uncle Pete runs a retail outlet that sells denim aprons in two sizes. Pete suggests that you get into the manufacturing side of the business, so on January 1, 2025, you start up an apron production company called DenimWorks. Using the best information at hand, the two of you compile the following information to establish the standard costs for 2025:

Standards Table for DenimWorks

The aprons are easy to produce, and no apron is ever left unfinished at the end of any given day. This means that DenimWorks will never have work-in-process inventory at the end of an accounting period.

When we make the journal entries for completed aprons, we’ll use an account called Inventory-FG which means Finished Goods Inventory. We’ll also be using the account Direct Materials Inventory or Raw Materials Inventory or Stores. Most manufacturers will also have an account entitled Work-in-Process Inventory, which is commonly referred to as WIP Inventory.

Direct Materials Purchased: Standard Cost and Price Variance

Direct materials are the raw materials that are directly traceable to a product. In your apron business the main direct material is the denim. (In a food manufacturer’s business the direct materials are the ingredients such as flour and sugar; in an automobile assembly plant, the direct materials are the cars’ component parts).

DenimWorks purchases its denim from a local supplier with terms of net 30 days, FOB destination. This means that title to the denim passes from the supplier to DenimWorks when DenimWorks receives the material. When the denim arrives, DenimWorks will record the denim received in its Direct Materials Inventory at the standard cost of $3 per yard (see the standards table above) and will record a liability for the actual cost of the material received. Any difference between the standard cost of the material and the actual cost of the material received is recorded as a purchase price variance.

Examples of Standard Cost of Materials and Price Variance

Let’s assume that on January 2, 2025, DenimWorks ordered 1,000 yards of denim at $2.90 per yard. On January 8, DenimWorks receives the 1,000 yards of denim and the supplier’s invoice for the actual cost of $2,900. On January 8, DenimWorks becomes the owner of the material and has a liability to its supplier. On January 8, DenimWorks’ Direct Materials Inventory is increased by the standard cost of $3,000 (1,000 yards of denim at the standard cost of $3 per yard), Accounts Payable is credited for $2,900 (the actual amount owed to the supplier), and the difference of $100 is credited to Direct Materials Price Variance. Putting this information in a general journal entry looks like this:

The $100 credit to the Direct Materials Price Variance account indicates that the company is experiencing actual costs that are more favorable than the planned, standard costs.

In February, DenimWorks orders 3,000 yards of denim at $3.05 per yard. On March 1, DenimWorks receives the 3,000 yards of denim and the supplier’s invoice for $9,150 due in 30 days. On March 1, the Direct Materials Inventory account is increased by the standard cost of $9,000 (3,000 yards at the standard cost of $3 per yard), Accounts Payable is credited for $9,150 (the actual cost of the denim), and the difference of $150 is debited to Direct Materials Price Variance as an unfavorable price variance:

After the March 1 transaction is posted, the Direct Materials Price Variance account shows a debit balance of $50 (the $100 credit on January 8 combined with the $150 debit on March 1). A debit balance in any variance account means it is unfavorable. It means that the actual costs are higher than the standard costs and the company’s profit will be $50 less than planned unless some action is taken.

On June 1 your company receives an additional 3,000 yards of denim at an actual cost of $2.92 per yard for a total of $8,760 due in 30 days. The entry is:

Direct Materials Inventory is debited for the standard cost of $9,000 (3,000 yards at $3 per yard), Accounts Payable is credited for the actual amount owed, and the difference of $240 is credited to Direct Materials Price Variance. The $240 variance is favorable since the company paid $0.08 per yard less than the standard cost per yard x the 3,000 yards of denim.

NOTE:

A debit to a variance account indicates unfavorable.

A credit to a variance account indicates favorable.

After this transaction is recorded, the Direct Materials Price Variance account shows a credit balance of $190. A credit balance in a variance account is always favorable. In other words, your company’s profit will be $190 greater than planned due to the lower than expected cost of direct materials.

Note that the entire price variance pertaining to all of the direct materials received was recorded immediately (as opposed to waiting until the materials were used).

We will discuss later how to handle the balances in the variance accounts under the heading What To Do With Variance Amounts.

Direct Materials Usage Variance

In a standard costing system, the costs of production, inventories, and the cost of goods sold are initially recorded using the standard costs. In the case of direct materials, it means the standard quantity of direct materials that should have been used to make the good output. If the manufacturer uses more direct materials than the standard quantity of materials for the products actually manufactured, the company will have an unfavorable direct materials usage variance.

If the quantity of direct materials actually used is less than the standard quantity for the products produced, the company will have a favorable usage variance. The amount of a favorable and unfavorable variance is recorded in a general ledger account Direct Materials Usage Variance. (Alternative account titles include Direct Materials Quantity Variance or Direct Materials Efficiency Variance.) We will demonstrate this variance with the following information.

January 2025

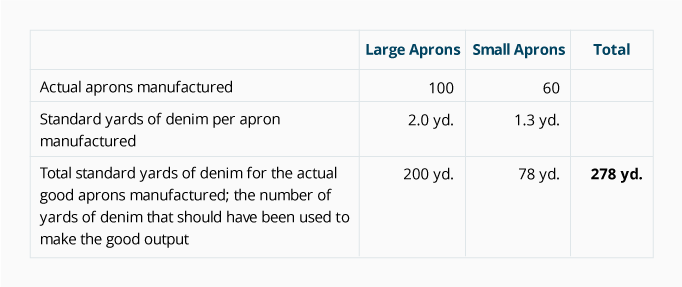

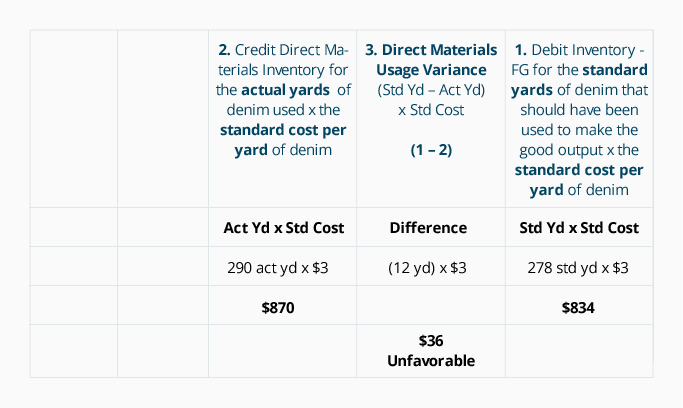

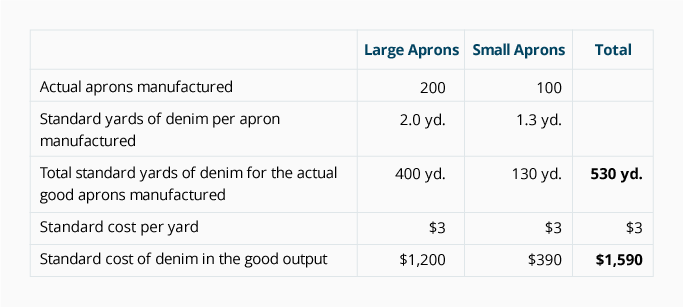

In order to calculate the direct materials usage (or quantity) variance, we start with the number of acceptable units of products that have been manufactured—also known as the good output. At DenimWorks this is the number of good aprons physically produced. If DenimWorks produces 100 large aprons and 60 small aprons during January, the production and the finished goods inventory will begin with the cost of the direct materials that should have been used to make those aprons. Any difference will be a variance.

Note:We are not determining the quantity of aprons that DenimWorks should have made. Rather, we are determining whether the 100 large aprons and 60 small aprons that were actually manufactured were produced efficiently. In the case of direct materials, we want to determine whether or not the company used the proper amount of denim to make the 160 aprons that were actually produced. (For the purposes of calculating the direct materials usage variance, it doesn’t matter whether DenimWorks had a goal to produce 100 aprons, 200 aprons, or 250 aprons. The direct materials usage variance is computed for the actual number of aprons produced.)

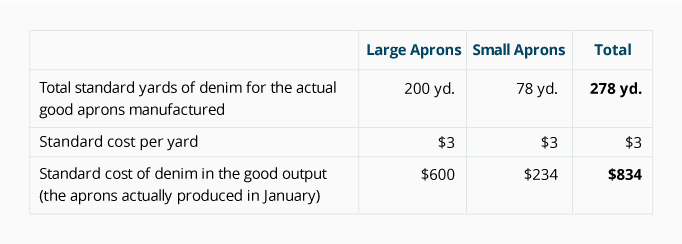

Standard costs are sometimes referred to as the “should be costs.” DenimWorks should be using 278 yards of denim to make 100 large aprons and 60 small aprons as shown in the following table.

We determine the total standard cost of the denim that should have been used to make the 160 aprons by multiplying the standard quantity of denim (278 yards) by the standard cost of a yard of denim ($3 per yard):

An inventory account (such as F.G. Inventory or Work-in-Process) is debited for $834; this is the standard cost of the direct materials component in the aprons manufactured in January 2025.

The Direct Materials Inventory account is reduced by the standard cost of the denim that was removed from the direct materials inventory. Let’s assume that the actual quantity of denim removed from the direct materials inventory and used to make the aprons in January was 290 yards. Because Direct Materials Inventory reports the standard cost of the actual materials on hand, we reduce the account balance by $870 (the 290 yards actually used x the standard cost of $3 per yard). After removing 290 yards of materials, the balance in the Direct Materials Inventory account as of January 31 is $2,130 (710 yards x the standard cost of $3 per yard).

The Direct Materials Usage Variance is: [the standard quantity of material that should have been used to make the good output minus the actual quantity of material used] X the standard cost per yard.

In our example, DenimWorks should have used 278 yards of material to make 100 large aprons and 60 small aprons. Because the company actually used 290 yards of denim, we say that DenimWorks did not operate efficiently. When we multiply the additional 12 yards times the standard cost of $3 per yard, the result is an unfavorable direct materials usage variance of $36.

For the remainder of our explanation, we will use a common format for calculating variances. The amounts for each column are computed in the order indicated in the headings.

Direct Materials Usage/Quantity/Efficiency Variance Analysis

The journal entry for the direct materials used for the January production is:

February 2025

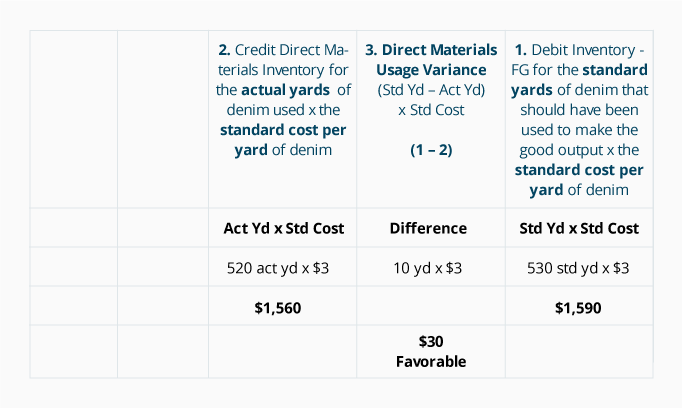

Let’s assume that in February 2025 DenimWorks produces 200 large aprons and 100 small aprons and that 520 yards of denim are actually used. From this information we can compute the following:

Let’s put the February 2025 information into our format:

Direct Materials Usage (or Quantity) Variance Analysis

The journal entry for the direct materials used for the February production is:

Direct Labor: Standard Cost, Rate Variance, Efficiency Variance

Direct labor refers to the work done by employees who work directly on the goods being produced. (Indirect labor refers to the employees who work in the production area, but do not work directly on the products. An example of indirect labor is the employees who set up or maintain the equipment.)

Unlike direct materials (which are obtained prior to being used) direct labor is obtained and used at the same time. This means that for the given good output, we can compute the following at the same time (when goods are produced):

- Standard direct labor cost

- Direct labor rate variance

- Direct labor efficiency variance

January 2025

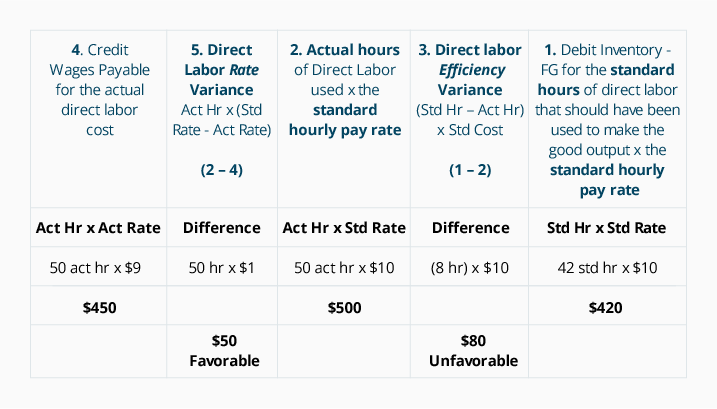

Let’s begin by determining the standard cost of direct labor for the good output produced in January 2025:

Assuming that the actual direct labor in January adds up to 50 hours and the actual hourly rate of pay (including payroll taxes) is $9 per hour, our analysis will look like this:

Direct Labor Variance Analysis for January 2025:

In January, the direct labor efficiency variance (item #3 in the above image/analysis) is unfavorable because the company actually used 50 hours of direct labor, which is 8 hours more than the standard quantity of 42 hours allowed for the good output. The additional 8 hours multiplied by the standard rate of $10 results in an unfavorable direct labor efficiency variance of $80. (The direct labor efficiency variance could also be referred to as the direct labor quantity variance or usage variance.)

Note that DenimWorks paid $9 per hour for labor when the standard rate is $10 per hour. This $1 difference is multiplied by the 50 actual hours, resulting in a $50 favorable direct labor rate variance. (The direct labor rate variance could be referred to as the direct labor price variance.)

The journal entry for the direct labor used in the January production is:

February 2025

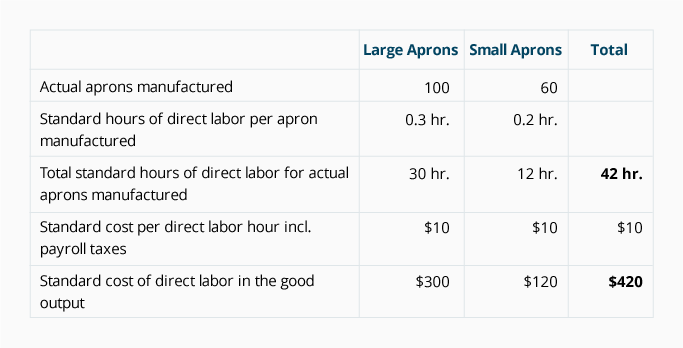

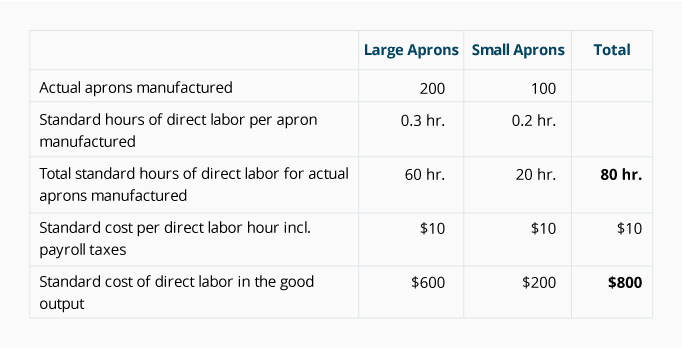

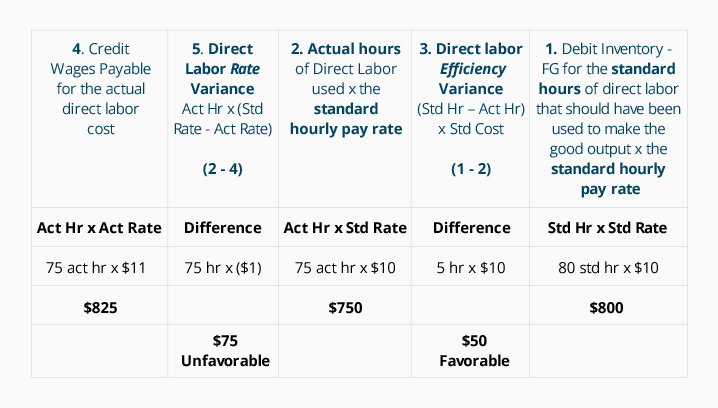

In February DenimWorks manufactured 200 large aprons and 100 small aprons. The standard cost of direct labor and the variances for the February 2025 output is computed next.

If we assume that the actual labor hours in February add up to 75 and the hourly rate of pay (including payroll taxes) is $11 per hour, the total equals $825. The analysis for February 2025 looks like this:

Direct Labor Variance Analysis for February 2025:

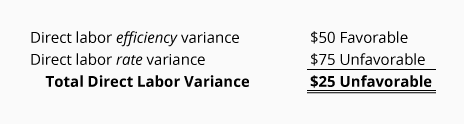

Notice that for February’s good output, the total actual labor costs amounted to $825 and the total standard cost of direct labor amounted to $800. This unfavorable difference of $25 agrees to the sum of the two labor variances:

The journal entry for the direct labor used in the February production is:

Later we will discuss what to do with the balances in the direct labor variance accounts under the heading What To Do With Variance Amounts.

Variable Manufacturing Overhead: Standard Cost, Spending Variance, Efficiency Variance

Manufacturing overhead costs refer to the costs within a manufacturing facility other than direct materials and direct labor. Manufacturing overhead includes items such as indirect labor, indirect materials, utilities, quality control, material handling, and depreciation on the manufacturing equipment and facilities, and more.

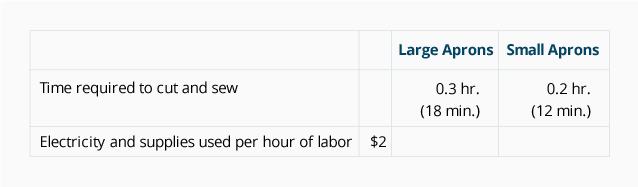

Variable manufacturing overhead costs will increase in total as output increases. An example is the cost of the electricity needed to operate the machines that cut and sew the denim. Another example is the cost of the manufacturing supplies (such as needles and thread) that increase when production increases. We will assume that these variable manufacturing overhead costs fluctuate in response to the number of direct labor hours. Recall the following information in our Standards Table in Section 2.

January 2025

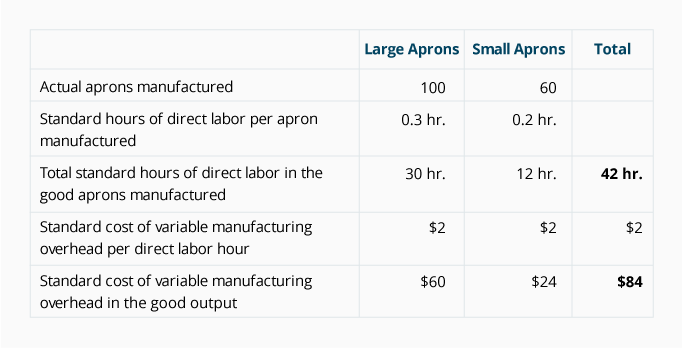

Let’s begin by determining the standard cost of variable manufacturing overhead for DenimWorks’ good output in January 2025:

Recall that there were 50 actual direct labor hours in January. Now let’s assume that the actual cost for the variable manufacturing overhead (electricity and manufacturing supplies) during January was $90.

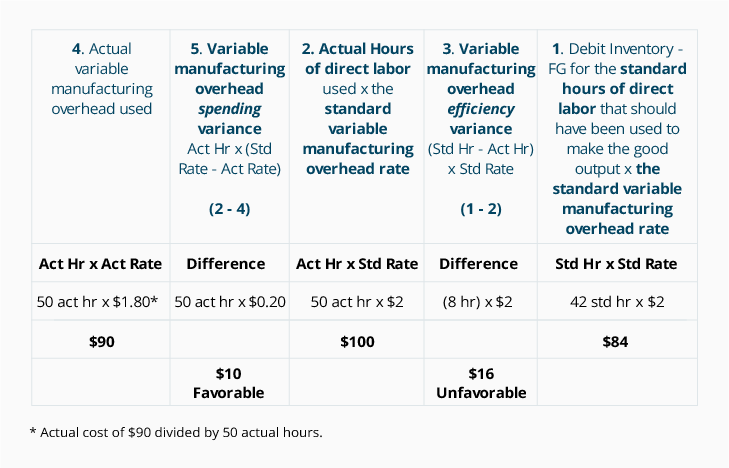

Based on the above information, our analysis will look like this:

Variable Manufacturing Overhead Analysis for January 2025:

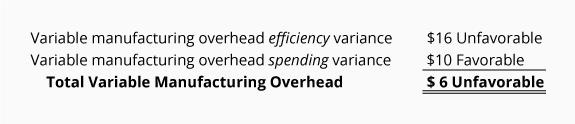

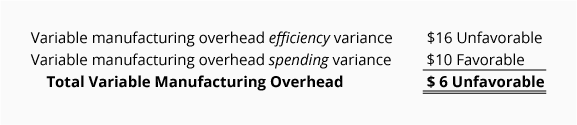

Notice that for the good output produced in January, the actual cost of variable manufacturing overhead was $90 and the total standard cost of variable manufacturing overhead for the good output was $84. This unfavorable difference of $6 agrees to the sum of the two variances:

Variable Manufacturing Overhead Efficiency Variance

As our analysis shows, DenimWorks did not produce the good output efficiently since it used 50 actual direct labor hours instead of the 42 standard direct labor hours.

It is assumed that the additional 8 hours caused the company to use additional electricity and supplies. Measured at the originally estimated rate of $2 per direct labor hour, this amounts to $16 (8 hours x $2). As a result, this is an unfavorable variable manufacturing overhead efficiency variance.

Variable Manufacturing Overhead Spending Variance

In our previous analysis, item 2 shows that based on the 50 direct labor hours actually used, electricity and supplies could cost $100 (50 hours x $2 per hour) instead of the standard cost of $84. However, the actual cost of the electricity and supplies was $90, not $100. This $10 favorable variance indicates that the company did not spend the planned $2 per direct labor hour. (Perhaps electricity rates were lower than the rates anticipated when the standard costs were established.)

Actual variable manufacturing overhead costs are debited to overhead cost accounts. The credits are made to accounts such as Accounts Payable. For example:

Another entry records how the overhead costs were assigned to the product based on the standard costs:

Our analysis and the journal entries illustrate that DenimWorks had actual variable manufacturing overhead of $90, but only $84 (the standard amount) was applied to the products. The $6 difference is “explained” by the two variances:

February 2025

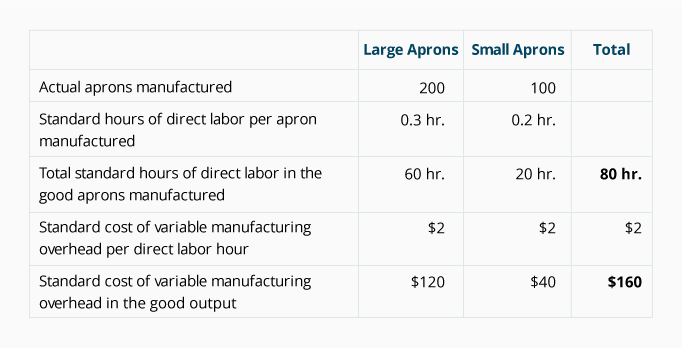

Recall that in February 2025 the company produced 200 large aprons and 100 small aprons. With that information we can compute the standard cost of variable manufacturing overhead for February 2025:

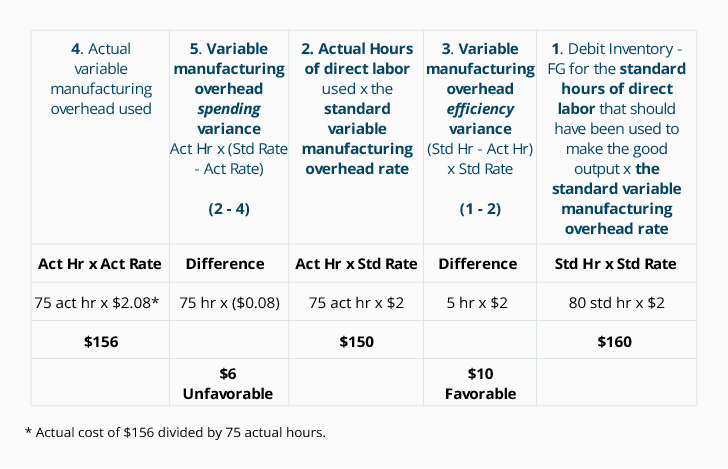

Given that there were 75 actual direct labor hours in February and assuming that the actual cost for the variable manufacturing overhead in February was $156, our analysis is:

Variable Manufacturing Overhead Analysis for February 2025:

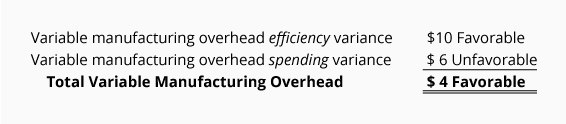

The favorable difference between the actual cost of $156 and the standard cost of $160 agrees with the sum of the following two variances:

Actual variable manufacturing overhead costs are debited to overhead cost accounts. The credits are made to accounts such as Accounts Payable. For example:

Another entry records how these overheads were assigned to the product:

As our analysis notes above and as these entries illustrate, even though DenimWorks had actual variable manufacturing overhead of $156, the standard amount of $160 was applied to the products. Accountants might say that for the month of February 2025, the company overapplied variable manufacturing overhead.

We will discuss how to report the balances in the variance accounts under the heading What To Do With Variance Amounts.

Fixed Manufacturing Overhead: Standard Cost, Budget Variance, Volume Variance

Fixed manufacturing overhead costs remain the same in total even though the production volume increases by a modest amount. For example, the property tax on a large manufacturing facility might be $50,000 per year and it arrives as one tax bill in December. The amount of the property tax bill does not depend on the number of units produced or the number of machine hours that the plant operated. A few of the many examples of fixed manufacturing overhead costs include the depreciation or rent on production facilities; salaries of production managers and maintenance supervisors; and professional memberships and training for managers in the manufacturing area. Although the fixed manufacturing overhead costs present themselves as large monthly or annual expenses, they are part of each product’s cost.

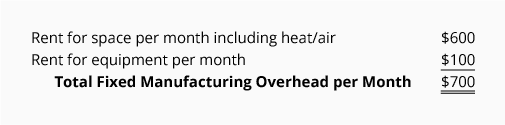

DenimWorks has two fixed manufacturing overhead costs:

A portion of these fixed manufacturing overhead costs must be allocated to each apron produced. This is known as absorption costing and it explains why some accountants say that each product must “absorb” a portion of the fixed manufacturing overhead costs.

A simple way to assign or allocate the fixed costs is to base it on things such as direct labor hours, machine hours, or pounds of direct material. Accountants realize that this is simplistic; they know that overhead costs are caused by many different factors. Nonetheless, we will assign the fixed manufacturing overhead costs to the aprons by using the direct labor hours.

Establishing a Predetermined Rate

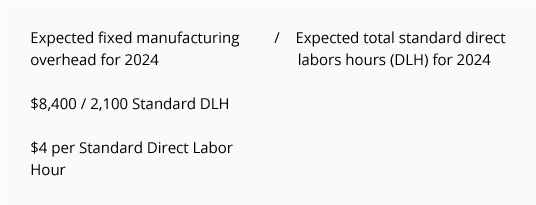

Companies typically establish a standard fixed manufacturing overhead rate prior to the start of the year and then use that rate for the entire year. Let’s assume it is December 2024 and DenimWorks is developing the standard fixed manufacturing overhead rate for use in 2025. As mentioned above, we will assign the fixed manufacturing overhead on the basis of direct labor hours.

Step 1. Estimate the fixed manufacturing overhead costs for the year 2025.

We indicated above that the fixed manufacturing overhead costs are the rents of $700 per month, or $8,400 for the year 2025.

Step 2. Estimate the total number of standard direct labor hours that are needed to manufacture your products during 2025.

We can estimate the direct labor hours from the information given earlier (and repeated here):

Step 3. Compute the standard fixed manufacturing rate to be used in 2025.

The standard fixed manufacturing overhead rate calculation is:

Note:One reason a company develops a predetermined annual rate is to have a uniform rate for all months. If the company used monthly rates, the rate would be high in the months when few units are produced (monthly fixed costs of $700 ÷ 100 units produced = $7 per unit) and low when many units are produced (monthly fixed costs of $700 ÷ 350 units = $2 per unit).

Fixed Manufacturing Overhead Budget Variance

The difference between the actual amount of fixed manufacturing overhead and the estimated amount (the amount budgeted when setting the overhead rate prior to the start of the year) is known as the fixed manufacturing overhead budget variance.

In our example, we budgeted the annual fixed manufacturing overhead at $8,400 (monthly rents of $700 x 12 months). If DenimWorks pays more than $8,400 for the year, there is an unfavorable budget variance; if the company pays less than $8,400 for the year, there is a favorable budget variance.

Fixed Manufacturing Overhead Volume Variance

Recall that the fixed manufacturing overhead costs (such as the large amount of rent paid at the start of every month) must be assigned to the aprons produced. In other words, each apron must absorb a small portion of the fixed manufacturing overhead costs. At DenimWorks, the fixed manufacturing overhead is assigned to the good output by multiplying the standard rate by the standard hours of direct labor in each apron. Hopefully, by the end of the year there will be enough good aprons produced to absorb all of the fixed manufacturing overhead costs.

The fixed manufacturing overhead volume variance is the difference between the amount of fixed manufacturing overhead budgeted and the amount that was applied to (or absorbed by) the good output. If the amount applied is less than the amount budgeted, there is an unfavorable volume variance. This means there was not enough good output to absorb the budgeted amount of fixed manufacturing overhead. If the amount applied to the good output is greater than the budgeted amount of fixed manufacturing overhead, the fixed manufacturing overhead volume variance is favorable.

Illustration of Fixed Manufacturing Overhead Variances for 2025

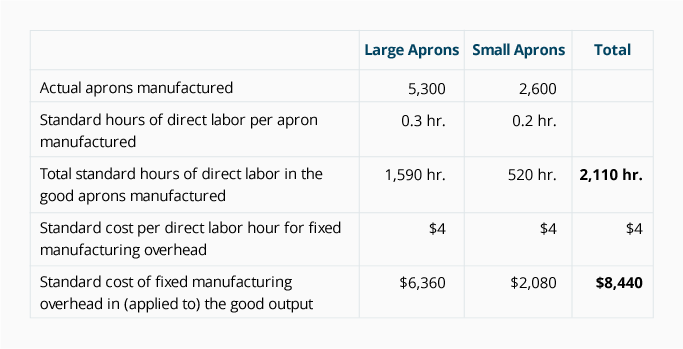

Let’s assume that in 2025 DenimWorks manufactures (has actual good output of) 5,300 large aprons and 2,600 small aprons. Let’s also assume that the actual fixed manufacturing overhead costs for the year are $8,700. As we calculated earlier, the standard fixed manufacturing overhead rate is $4 per standard direct labor hour.

We begin by determining the fixed manufacturing overhead applied to (or absorbed by) the good output produced in the year 2025. Recall that we apply the overhead costs to the aprons by using the standard amount of direct labor hours.

Our analysis looks like this:

Fixed Manufacturing Overhead Analysis for the Year 2025:

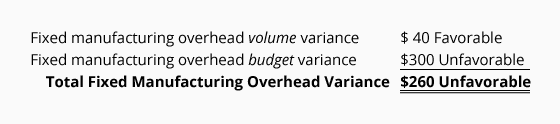

This analysis shows that the actual fixed manufacturing overhead costs are $8,700 and the fixed manufacturing overhead costs applied to the good output are $8,440. This unfavorable difference of $260 agrees to the sum of the two variances:

The actual fixed manufacturing overhead costs are debited to overhead cost accounts. The credits are made to accounts such as Accounts Payable or Cash. For example:

Another entry records how these overheads are assigned to the product:

We will discuss how to report the balances in the variance accounts under the heading What To Do With Variance Amounts.

Relationship Between Variances

If the direct labor is not efficient when producing the good output, there will be an unfavorable labor efficiency variance. That inefficiency will likely cause additional variable manufacturing overhead which will result in an unfavorable variable manufacturing overhead efficiency variance. If the inefficiencies are significant, the company might not be able to produce enough good output to absorb the planned fixed manufacturing overhead costs. This in turn can also cause an unfavorable fixed manufacturing overhead volume variance.

We will pursue the interdependence of variances in the following examples.

Example 1

Assume your company’s standard cost for denim is $3 per yard, but you buy some denim at a bargain price of $2.50 per yard. For each yard of denim purchased, DenimWorks reports a favorable direct materials price variance of $0.50.

Let’s also assume that the quality of the low-cost denim ends up being slightly lower than the quality to which your company is accustomed. This lesser quality denim causes the production to be a bit slower as workers spend additional time working around flaws in the material. In addition to this decline in productivity, you also find that some of the denim is of such poor quality that it has to be discarded. Further, some of the finished aprons don’t pass the final inspection due to occasional defects not detected as the aprons were made.

You get the picture. If the favorable $0.50 per yard price variance correlates with lower quality, that denim was no bargain. The $0.50 per yard favorable variance may be more than offset by the following unfavorable quantity variances:

- Direct material usage variance

- Direct labor efficiency variance

- Variable manufacturing overhead efficiency variance

Keep in mind that the standard cost is the cost allowed on the good output. Putting material, labor, and manufacturing overhead costs into products that will not end up as good output will likely result in unfavorable variances.

Example 2

Let’s assume that you decide to hire an unskilled worker for $9 per hour instead of a skilled worker for the standard cost of $15 per hour. Although the unskilled worker will create a favorable direct labor rate variance of $6 per hour, you may see significant unfavorable variances such as a direct material usage variance, a direct labor efficiency variance, a variable manufacturing overhead efficiency variance, and possibly a fixed manufacturing overhead volume variance.

These two examples highlight what experienced managers know: you need to look at more than price. A low cost for an inferior input is no bargain if it results in costly inefficiencies.

What To Do With Variance Amounts

Throughout our explanation of standard costing we showed you how to calculate the variances. In the case of direct materials and direct labor, the variances were recorded in specific general ledger accounts. The manufacturing overhead variances were the differences between the accounts containing the actual costs and the accounts containing the applied costs. Now we’ll discuss what we do with those variance amounts.

Direct Materials Price Variance

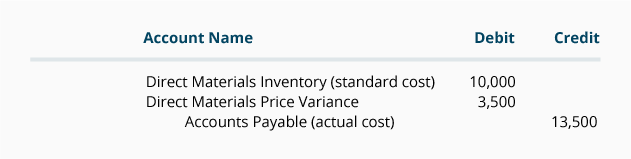

Let’s begin by assuming that the account Direct Materials Price Variance has a debit balance of $3,500 at the end of the accounting year resulting from one purchase:

Because of the cost principle, the financial statements for DenimWorks report the company’s actual cost. If none of the direct materials purchased in this journal entry was used in production (all of the direct materials remain in the direct materials inventory), the company’s balance sheet must report the direct materials inventory at $13,500. In other words, the balance sheet will report the standard cost of $10,000 plus the price variance of $3,500.

If all of the materials were used in making products, and all of the products have been sold, the $3,500 price variance is added to the company’s standard cost of goods sold.

If 20% of the materials remain in the direct materials inventory and 80% of the materials are in the finished goods that have been sold, then $700 of the price variance (20% of $3,500) is added to the standard cost of the direct materials inventory, $2,800 (80% of $3,500) is added to the standard cost of goods sold.

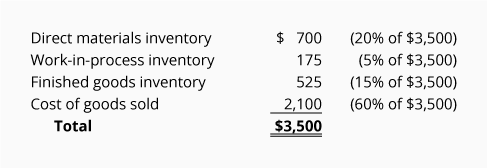

Now let’s assume the direct materials are in various stages of use:

- 20% have not been used yet

- 5% are in work-in-process

- 15% are in finished goods on hand

- 60% are in finished goods that have been sold

We need to assign or allocate the unfavorable $3,500 direct materials price variance to the four places where the direct materials are now located. Since the $3,500 is an unfavorable amount, the following amounts are added to the standard costs:

Accounting professionals have a materiality guideline which allows a company to make an exception to an accounting principle if the amount in question is insignificant. (For example, a large company may report amounts to the nearest $1,000 on its financial statements, or an inexpensive item like a wastebasket can be expensed immediately instead of being depreciated over its useful life.) This means that if the total variance of $3,500 shown above is a very, very small amount relative to the company’s net income, the company can assign the entire $3,500 to the cost of goods sold instead of allocating some of the amount to the inventories.

If the balance in the Direct Materials Price Variance account is a credit balance of $3,500 (instead of a debit balance) the procedure and discussion would be the same, except that the standard costs would be reduced instead of increased.

Direct Materials Usage Variance

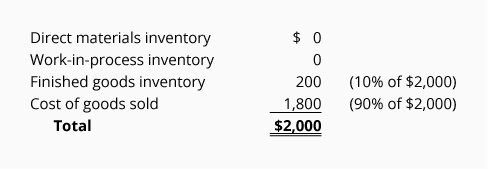

Let’s assume that the Direct Materials Usage Variance account has a debit balance of $2,000 at the end of the accounting year. A debit balance is an unfavorable balance resulting from more direct materials being used than the standard amount allowed for the good output.

The first question to ask is “Why do we have this unfavorable variance of $2,000?” If it was caused by errors and/or inefficiencies, it cannot be assigned to the inventory. Errors and inefficiencies are never considered to be assets; therefore, the entire amount must be expensed immediately.

On the other hand, if the unfavorable $2,000 variance is the result of an unrealistic standard for the quantity of direct materials needed, then we should allocate the $2,000 variance to wherever the standard costs of direct materials are now located. If 90% of the related direct materials have been sold and 10% are in the finished goods inventory, then the $2,000 should be allocated and added to the standard direct material costs as follows:

If $2,000 is an insignificant amount relative to a company’s net income, the entire $2,000 unfavorable variance can be added to the cost of goods sold. This is permissible because of the materiality guideline.

If the $2,000 balance is a credit balance, the variance is favorable. This means that the actual direct materials used were less than the standard quantity of materials called for by the good output. We should allocate this $2,000 to wherever those direct materials are physically located. However, if $2,000 is an insignificant amount, the materiality guideline allows for the entire $2,000 to be deducted from the cost of goods sold on the income statement.

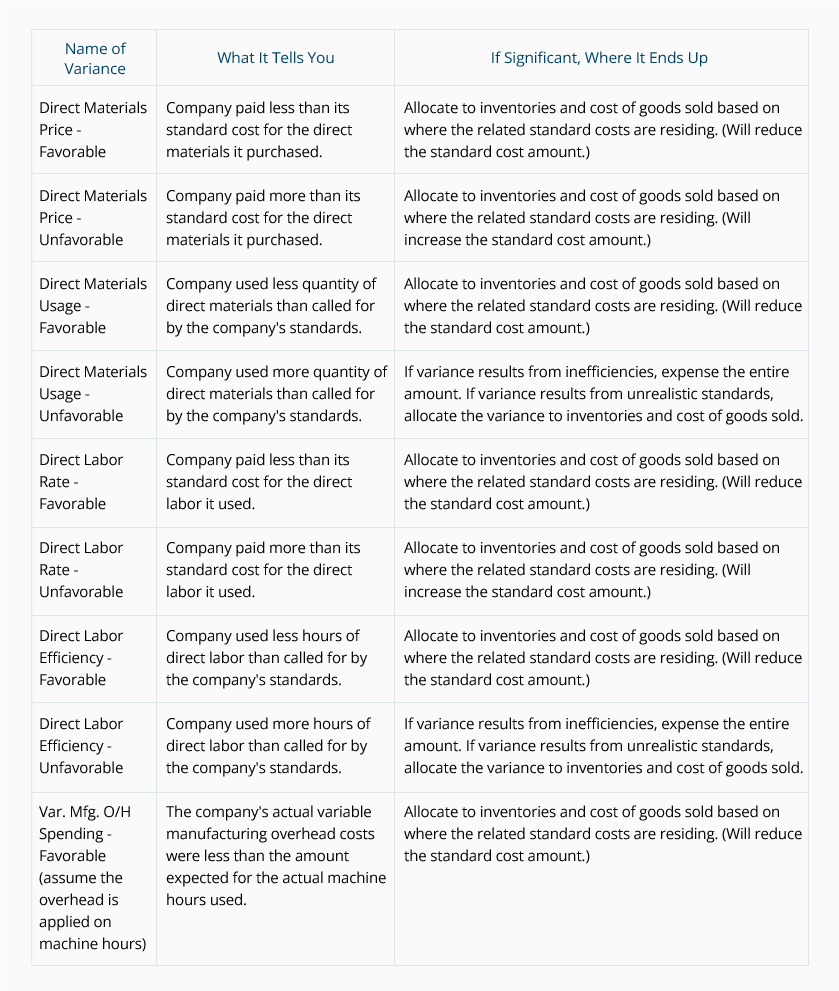

Other Variances

The examples above follow these guidelines:

- If the variance amount is very small (insignificant relative to the company’s net income), simply put the entire amount on the income statement. If the insignificant variance amount is unfavorable, increase the cost of goods sold—thereby reducing net income. If the insignificant variance amount is favorable, decrease the cost of goods sold—thereby increasing net income.

- If the variance is unfavorable, significant in amount, and results from mistakes or inefficiencies, the variance amount can never be added to any inventory or asset account. These unfavorable variance amounts go directly to the income statement and reduce the company’s net income.

- If the variance is unfavorable, significant in amount, and results from the standard costs not being realistic, allocate the variance to the company’s inventory accounts and cost of goods sold. The allocation should be based on the location of the inputs from which the variances arose.

- If the variance amount is favorable and significant in amount, allocate the variance to the company’s inventories and its cost of goods sold.

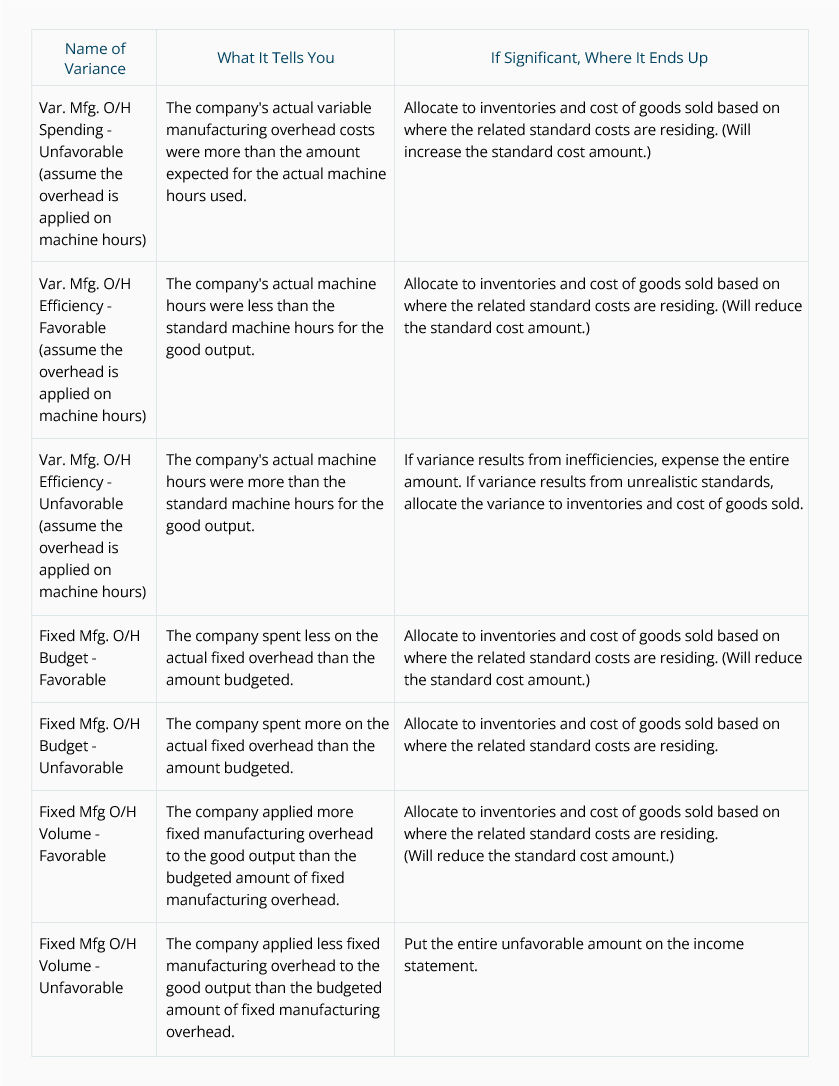

The following table will serve as a guide for reporting variances that are significant in amount:

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Standard Costing materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.