Introduction

From churches to youth organizations to the local chambers of commerce, nonprofit organizations make our communities more livable places. Unlike for-profit businesses that exist to generate profits for their owners, nonprofit organizations exist to pursue missions that address the needs of society. Nonprofit organizations serve in a variety of sectors, such as religious, education, health, social services, commerce, amateur sports clubs, and the arts.

Nonprofits do not have commercial owners and must rely on funds from contributions, membership dues, program revenues, fundraising events, public and private grants, and investment income.

Our intent is to merely introduce some of the basic concepts that are unique to nonprofit accounting and reporting that are required by the Financial Accounting Standards Board (FASB).

We will not discuss the accounting which is similar to that used by for-profit businesses. If you are not familiar with accounting for businesses or you need a refresher, you will find explanations, practice quizzes, Q&A, and more by visiting our course outline.

Accountants often refer to businesses as for-profit entities and to nonprofit organizations as not-for-profit entities, or NFPs. We will be using the more common term nonprofit instead of not-for-profit.

Again, this is a very brief introduction to nonprofit accounting. There are many different types of nonprofits, including governmental nonprofits, which we will not address.

Note: We developed seven business forms to assist you in preparing the financial statements of a nonprofit organization. You can find additional information at AccountingCoach PRO.

WATCH NOW

Advance Your Career with Our PRO Training

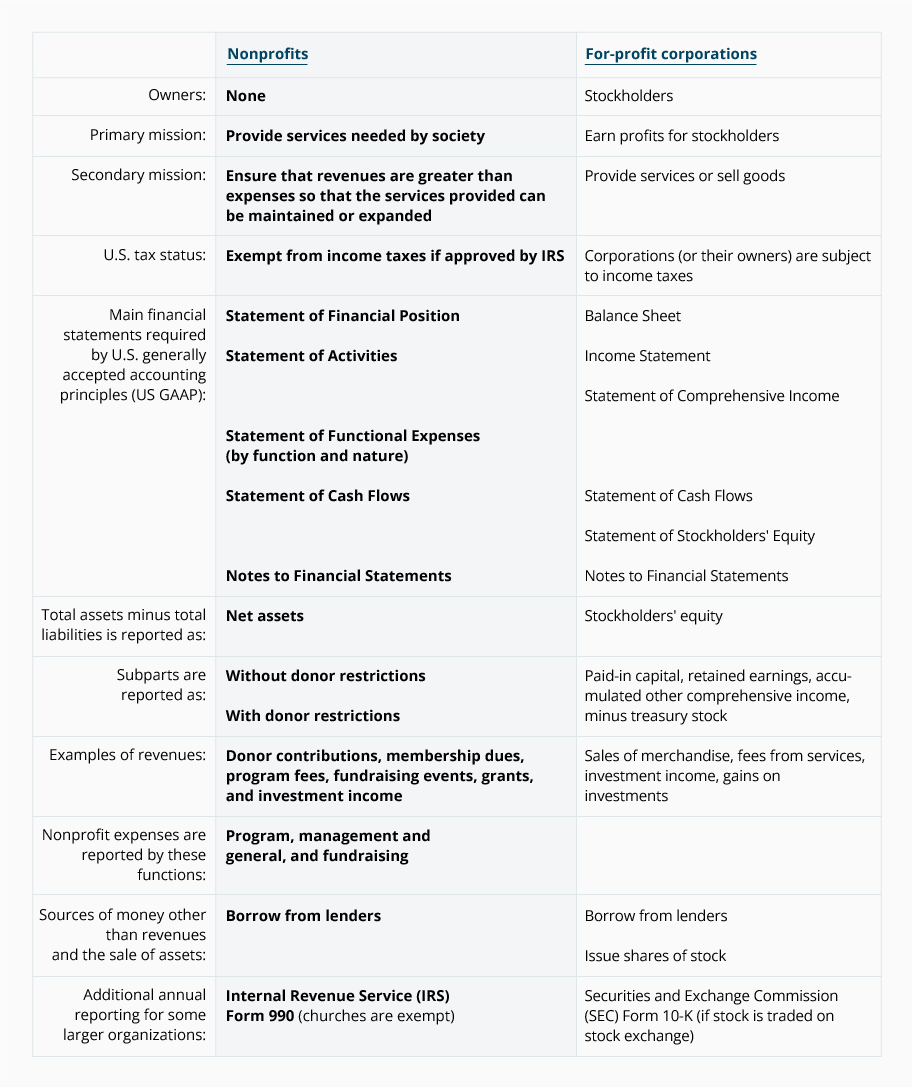

Nonprofits vs. For-Profit Corporations

The following table highlights some of the key differences between nonprofit organizations and for-profit corporations:

Mission and Ownership, Tax-Exempt Status

Mission and Ownership

While businesses are organized to generate profits, nonprofits are organized to address needs in society. As a result, nonprofits will issue a statement of activities instead of the income statement issued by for-profit businesses.

Since nonprofits do not have owners, there is no owner’s equity or stockholders’ equity and there cannot be distributions to owners.

Some people mistakenly assume that if an organization is designated as a nonprofit, it cannot legally earn profits. In fact, having more revenues than expenses is almost a necessity for a nonprofit if it hopes to withstand such things as:

- unexpected expenses

- uneven flows of revenues

- a decrease in revenues

- rising costs due to inflation

- an increase in staffing needs

- an increase in the need for its services

- a purchase or replacement of needed equipment

- other needs since a nonprofit cannot issue shares of stock

Tax-Exempt Status

Nonprofit organizations may apply to the Internal Revenue Service in order to be exempt from federal income taxes.

A second issue is whether a donor’s contribution to a nonprofit organization will qualify as a charitable deduction on the donor’s income tax return. For example, churches, schools, and Red Cross chapters are some of the nonprofits that will qualify as tax-exempt and their donors’ contributions will also qualify as charitable deductions on the donors’ income tax returns.

However, there are nonprofits that qualify as tax-exempt but their donors’ contributions do not qualify as charitable deductions (although they may qualify as business expenses). Examples of these nonprofits include social organizations, chambers of commerce, college fraternities and sororities, amateur sports clubs, employee organizations, and more.

You can learn more about the tax-exempt status for a nonprofit, the deductibility of contributions by donors, and the taxability of activities not directly related to a nonprofit’s exempt purpose in the Internal Revenue Service Publication 557, Tax-Exempt Status for Your Organization, which is available at no cost on IRS.gov.

Even if a nonprofit is exempt from federal income taxes, it is likely that its employees will be subject to employment taxes. Nonprofits may or may not be exempt from sales taxes, real estate taxes, and other taxes depending on which state in the U.S. they are incorporated or operate.

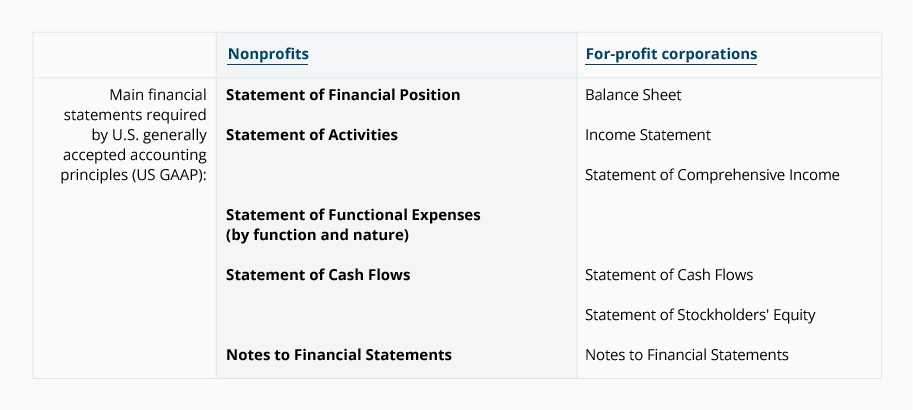

Financial Statements of Nonprofits

The following table compares the main financial statements of a nonprofit organization with those of a for-profit corporation.

Statement of Financial Position

A nonprofit’s statement of financial position (similar to a business’s balance sheet) reports the organization’s assets and liabilities in some order of when the assets will turn to cash and when the liabilities need to be paid. The amounts are as of the date shown in the heading which is usually the end of a month, quarter, or year. (We will present a sample statement of financial position in a later section.)

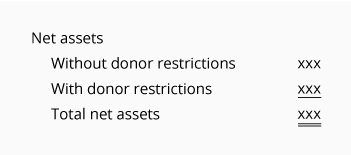

Net Assets

Since a nonprofit organization does not have owners, the third section of the statement of financial position is known as net assets (instead of owner’s equity or stockholders’ equity).

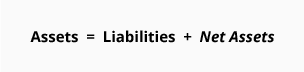

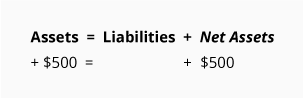

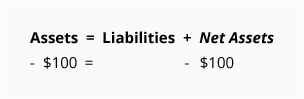

A nonprofit’s statement of financial position is represented by the following accounting equation:

Because of double-entry bookkeeping, the accounting equation and the statement of financial position should remain in balance at all times. For example, if a donor contributes $500, the effect on the nonprofit’s accounting equation and its statement of financial position is:

If the nonprofit pays $100 for supplies that will be used immediately, the effect on its accounting equation and its statement of financial position is:

The items that cause the changes in Net Assets are reported on the nonprofit’s statement of activities (to be discussed later).

The net assets section of a nonprofit’s statement of financial position requires at a minimum the following:

These classifications are based on the restrictions made by the donors at the time of their contributions.

Net assets without donor restrictions

If a donor does not specify a restriction on his or her contribution, the amount received by the nonprofit is recorded as an asset and as part of unrestricted contribution revenues. Unrestricted contribution revenues (reported on the statement of activities) also cause the amount of net assets without donor restrictions to increase. For instance, if a nonprofit receives an unrestricted contribution of $800 of cash, the effect on the statement of financial position is:

If the nonprofit’s board of directors designates some of the nonprofit’s unrestricted assets for a specific purpose, those assets must continue to be reported as net assets without donor restrictions.

Net assets with donor restrictions

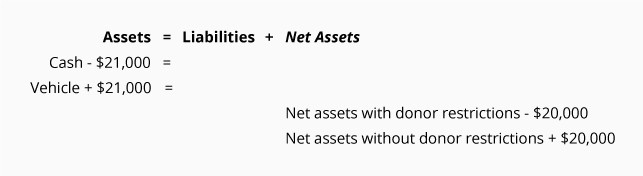

If a nonprofit receives a contribution that has a donor-imposed restriction, the amount is usually recorded as an asset and as donor restricted contribution revenues. Donor-restricted contribution revenues (reported on the statement of activities) also cause the amount of net assets with donor restrictions to increase. For example, James donates $20,000 with the requirement that the nonprofit use it to purchase a vehicle that is urgently needed in one of the nonprofit’s programs. The effect on the nonprofit’s accounting equation at the time the contribution is received is:

When the nonprofit purchases the vehicle at a cost of say $21,000, the purchase and the release of the restriction will cause the following changes:

Statement of Activities

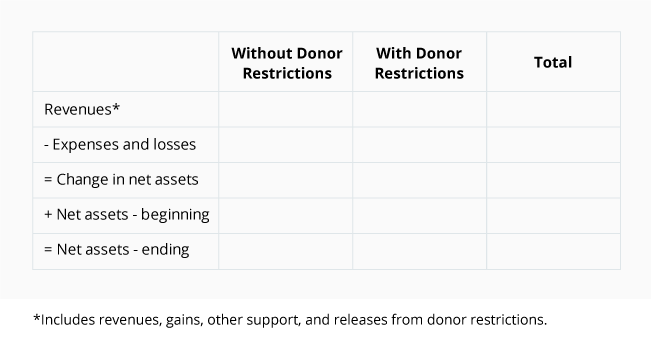

Since a nonprofit’s primary purpose is to provide programs that meet certain societal needs, it issues a statement of activities (instead of the income statement that is issued by a for-profit business).

The statement of activities reports revenue and expense amounts according to the two classifications of net assets discussed above (without donor restrictions, with donor restrictions). The following is the framework of the statement of activities without its heading and amounts:

Before we illustrate a sample statement of activities, let’s take a closer look at its components.

Revenues, gains, other support, and releases from donor restrictions

This heading will be followed by items such as:

- Contributions

- Membership dues

- Program fees

- Fundraising events

- Grants

- Investment income

- Gain on sale of investments

- Reclassifications when net assets are released from restrictions (a negative amount in the With Donor Restrictions column and a positive amount in the Without Donor Restrictions column)

Under the accrual method of accounting, revenues are reported in the accounting period in which they are earned. In other words, revenues might be earned in an accounting period that is different from the period in which the cash is received.

Expenses and losses

Under this caption expenses are reported according to the following functions:

1. Program functions

Program expenses (or program services expenses) are the amounts directly incurred by the nonprofit in carrying out its programs. For instance, if a nonprofit has three main programs, then each of the three programs will be listed along with each program’s expenses.

2. Support functions

Support expenses are reported in two subgroups:

- Management and general

- Fundraising and development

In order to accurately report the amount in each of these subgroups, it may be necessary to allocate some management and general salaries to fundraising based on the time spent by employees performing fundraising activities. For example, a management employee might be spending 30% of her time in fundraising activities but her entire salary has been recorded as management and general expenses.

Under the accrual method of accounting, expenses are to be reported in the accounting period in which they best match the related revenues. If that is not clear, then the expenses should be reported in the period in which they are used up. If there is uncertainty as to when an expense is matched or is used up, the amount spent should be reported as an expense in the current period.

General Ledger Accounts and Chart of Accounts

A nonprofit’s transactions are recorded in accounts in the general ledger. A listing of the titles of the general ledger accounts is known as the chart of accounts.

The accounts in the general ledger and in the chart of accounts are organized as follows:

- Statement of financial position accounts

- Asset accounts

- Liability accounts

- Net asset accounts

- Statement of activities accounts

- Revenues and gains

- Expenses and losses

The number of accounts in a nonprofit’s general ledger could range from 30 to 1,000 or more. The number of accounts depends on the number of programs that the nonprofit has, the types of revenues it earns, and the level of detail required for planning and control of the organization.

For example, a nonprofit is likely to have a separate general ledger account for each of its bank accounts. It may also have 50 general ledger accounts for each of its major programs, plus many accounts under its fundraising and management and general expense categories.

The detail in the general ledger accounts will always be available for management’s use. However, the account balances will be combined into a few amounts that are presented in the financial statements and IRS Form 990.

Nonprofit recordkeeping can get a bit challenging, so it is worth noting that accounting software exists to help nonprofits record transactions efficiently. The accounting software will also allow for reports of revenues and expenses by function (programs, fundraising, management and general), by the nature or type of expense (salaries, electricity, rent, depreciation, etc.), and/or by grant.

Illustration of the Statement of Financial Position and the Statement of Activities

We are now ready to present examples of the statement of financial position and the statement of activities. To do that, we’ll follow the activities of a nonprofit organization called Home4U, a daytime shelter for adults.

Let’s assume that Home4U was incorporated in January 2025 and its accounting years end on each December 31. The following transactions occurred during a three-month period.

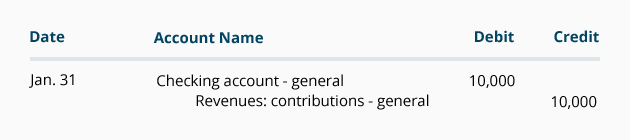

January Transaction

Transaction 1. On January 31, a donor contributes $10,000, without restriction, for the operation of Home4U. This transaction affects the general ledger accounts as follows:

Assuming this is the only transaction in January, the general ledger account balances will result in the following financial statements:

February Transactions

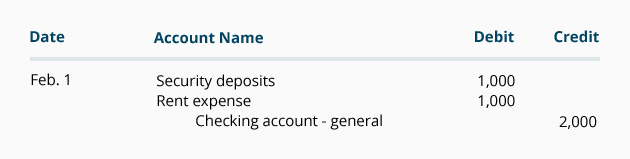

Transaction 2. On February 1, Home4U rents office space. A check is written for $2,000. This covers a one-time security deposit of $1,000 plus the February office rent of $1,000.

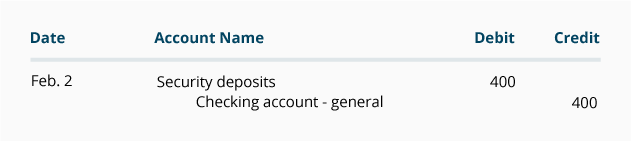

Transaction 3. On February 2, a $400 check is written to the utility as a one-time security deposit for electricity and heat service.

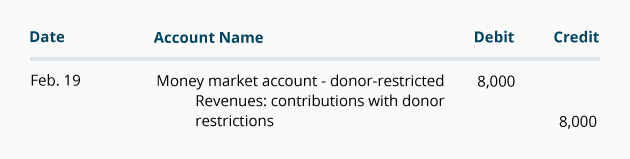

Transaction 4. On February 19, Home4U receives a contribution of $8,000 that the donor specifies must be used for the purchase of furniture. The contribution is deposited into a money market account. This transaction affects the general ledger accounts as follows:

Transaction 5. The electricity and heating bills have not arrived. It is estimated that the amount for February’s usage was $350, so the following accrual adjusting entry is recorded on February 28:

Assuming that Transactions 2 through 5 are the only transactions occurring in February, the general ledger account balances will result in the following financial statements:

March Transactions

During March, Home4U paid the March rent of $1,000. Home4U also paid the February utilities which were equal to the estimated amount of $350. Home4U estimates that March’s utilities will be $300.

On March 31, Home4U paid $8,300 to purchase furniture (using the donor-restricted donation of $8,000). The statement of financial position dated March 31 will report the following amounts:

Statement of Functional Expenses

The statement of functional expenses is described as a matrix since it reports expenses by their function (programs, management and general, fundraising) and by the nature or type of expense (salaries, rent). For instructional purposes we highlighted the column headings to indicate the expenses by function. We also highlighted the words in the first column as they indicate the nature or type of expenses.

The FASB requires every nonprofit to present expenses by function and nature in one place (statement or notes).

Statement of Cash Flows

The statement of cash flows (SCF) for a nonprofit organization is similar to that of a for-profit business. The SCF reports the organization’s change in its cash and cash equivalents during the accounting period.

The statement of cash flows consists of three sections:

- Cash flows from operating activities

- Cash flows from investing activities

- Cash flows from financing activities

The operating activities section of the SCF reports the changes in cash other than those reported in the investing and financing sections.

The investing activities section of the SCF reports the amounts spent to purchase long-term assets such as equipment, vehicles and long-term investments. The investing section also reports the amount received from the sale of long-term assets.

The financing activities section of the SCF reports the amounts received from borrowings and also any repayments.

While the statement of cash flows, or cash flow statement, may be a bit difficult to prepare, it is an important financial statement to be read.

You can learn more about this financial statement by visiting our Cash Flow Statement Explanation.

Notes to the Financial Statements

The notes to the financial statements are an integral part of the statement of financial position, the statement of activities, and the statement of cash flows. The FASB Accounting Standards Codification Topic 958 requires important additional disclosures regarding liquidity, restrictions, etc. for creditors, donors, and others.

Additional Reporting by Nonprofits

The U.S. Internal Revenue Service (IRS) requires some tax-exempt nonprofit organizations to file Form 990 (some can file Form 990-EZ) each year. (However, churches and some other nonprofit organizations are not required to file.) The title of Form 990 is Return of Organization Exempt From Income Tax.

Since the Form 990 filed by the nonprofit becomes public information, you can learn much about a nonprofit by reading the information on Form 990. The website guidestar.org is a resource one can use to obtain financial (and other) information reported on nonprofits’ Form 990.

Budgeting for Nonprofits

Budgeting for nonprofits can become complex when it involves several overlapping categories, such as grants, programs, function, and nature.

Budgeting is also complicated when sources of support are not secured at the time the budget is prepared for the upcoming year. This could lead to the use of an account entitled Resource Development in order to balance the budget.

Since resource development is often ongoing, budgets may require frequent modification. Good accounting software will also allow directors to compare budgeted amounts to actual amounts and make the necessary adjustments.

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Nonprofit Accounting materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.