Introduction

The cash flow statement is the name commonly used by practicing accountants for the statement of cash flows or SCF. We will use these names interchangeably throughout our explanation, practice quiz, and other materials.

The cash flow statement is required for a complete set of financial statements.

The SCF reports the cash inflows and cash outflows that occurred during the same time interval as the income statement. The time interval (period of time) covered in the SCF is shown in its heading. Two examples include “Year ended December 31, 2025” and “Three months ended September 30, 2025”.

The amounts on the SCF provide the reasons for the change in a company’s cash and cash equivalents during the period covered. For simplicity, we will assume that the company does not have cash equivalents. Therefore, our SCF will explain the change in the company’s cash from the beginning of the year to the end of the year (or the beginning of the quarter to the end of the quarter, etc.). Given our assumption that the company does not have cash equivalents, the following is a skeleton of the SCF’s format:

The cash flows from operating activities section provides information on the cash flows from the company’s operations (buying and selling of goods, providing services, etc.). With the most likely used indirect method, the starting point of this section is the company’s net income. It is followed with adjustments to convert the amount of net income from the accrual method to the cash amount.

The cash flows from investing activities lists the cash flows associated with the purchase and sale of noncurrent (long-term) assets such as investments and property, plant and equipment.

The cash flows from financing activities section reports the cash flows associated with the issuance and repurchase of a corporation’s bonds and capital stock, the payment of dividends, and the borrowing and repayment of short-term and long-term loans.

At the bottom of the SCF (and other financial statements) is a reference to inform the readers that the notes to the financial statements should be considered as part of the financial statements. The notes provide additional information such as disclosures of significant exchanges of items that did not involve cash, the amount paid for income taxes, and the amount paid for interest.

We begin with reasons why the statement of cash flows (SCF, cash flow statement) is a required financial statement.

WATCH NOW

Advance Your Career with Our PRO Training

Why the Cash Flow Statement is Required

The accounting profession realizes that reading only one or two financial statements is not sufficient for understanding a company’s finances and operations. Accordingly, the generally accepted accounting principles (GAAP, US GAAP) require that the statement of cash flows be part of a set of financial statements distributed outside of a company. A complete set of financial statements consists of five financial statements and the notes to the financial statements:

While the income statement amounts make the news, the amounts are based on the accrual basis of accounting. This method of accounting best measures a company’s sales, expenses, and earnings during a short time interval. However, the income statement does not measure and report the amounts of cash that flowed in and out of the company. For example, the income statement does not report the following:

- Cash collected from sales. (The cash might be collected from customers 45 days after the sale.)

- Cash paid for goods sold. (Payment may have been made many months prior to their sale.)

- Cash paid for buildings and equipment that will be expensed over the next 5 to 30 years.

- Cash received from the sale of long-term assets

- Cash received from bank loans

- Cash payments to reduce a loan’s principal balance

- Cash withdrawn by owners or cash dividends paid to stockholders

A company’s understanding of its cash inflows and outflows is critical for meeting its short-term and long-term obligations to its suppliers, employees, and lenders. Current and potential lenders and investors are also interested in the company’s cash flows.

Financial analysts will review closely the first section of the cash flow statement, cash flows from operating activities. Part of the review consists of comparing this section’s total (described as net cash provided by operating activities) to the company’s net income. This is done to see whether the revenues, expenses, and net income reported on the income statement are consistent with the change in the company’s cash balance.

If they are not consistent, they will seek to uncover the root causes for the differences. Perhaps the company’s inventory is no longer in demand or is being returned by customers. Perhaps receivables are not being collected, and so on. (In short, the analyst believes that “Cash is king”. While there can be some leeway in applying accounting principles, there is no leeway when it comes to reporting the amount of cash.)

Lastly, the SCF provides the cash amounts needed in some financial models.

Example of a Cash Flow Statement

The following is an example of the statement of cash flows, which is commonly referred to as the cash flow statement or SCF. (The company and the amounts shown are hypothetical.)

The heading for Example Corporation’s statement of cash flows indicates that the amounts occurred during the year January 1 through December 31, 2025.

In bold font you see subheadings for the three sections of the SCF. Many corporations omit “Cash flows from” and simply show the following as the subheadings:

- Operating activities

- Investing activities

- Financing activities

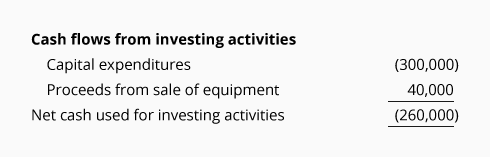

Some amounts are shown in parentheses, while other amounts are not. We will cover these in detail later, but let’s introduce the technique by looking at the amounts shown for investing activities:

-

The amount (300,000) communicates that cash of $300,000 was paid out, was a cash outflow, or that it reduced the company’s cash balance. Parentheses can also be thought of as having a negative or unfavorable effect on the company’s cash balance.

-

The amount 40,000 indicates that cash of $40,000 was received, was a cash inflow, or that it increased the company’s cash balance. Amounts without parentheses can also be thought of as having a positive or favorable effect on the company’s cash balance.

-

The (260,000) is described as the net cash used for investing activities. “Net” means the combination of the cash outflow of (300,000) and the cash inflow of 40,000.

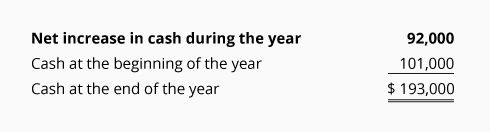

The amount 92,000 shown on the line Net increase in cash during the year is the combination of each section’s sum: 262,000 + (260,000) + 90,000. Since this net amount or grand total is a positive amount, it is shown without parentheses and is described as net increase in cash during the year.

Note that the net increase (or net decrease) in cash during the year is combined with the cash at the beginning of the year to show the cash at the end of the year. In our example, it is 92,000 + 101,000 = $193,000. The end of the year balance of $193,000 should agree with the cash balance on the company’s balance sheet for December 31, 2025.

Lastly, at the bottom of all financial statements is a sentence that informs the reader to read the notes to the financial statements. The reason is that not all business transactions can be adequately expressed as amounts on the face of the financial statements.

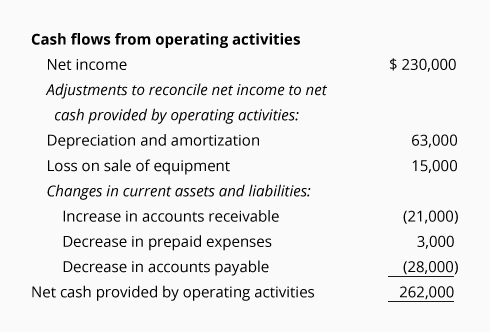

Cash Flows from Operating Activities

The first section of the statement of cash flows is described as cash flows from operating activities or shortened to operating activities. Operating activities are also referred to as company operations.

Operating activities are the business activities other than the investing and financial activities.

Here is the operating activities section of Example Corporation’s SCF which we will be referring to in our discussion:

Note that the combination of the positive and negative amounts in this section add up to a positive 262,000. Hence, it is described as “Net cash provided by operating activities”. If the amounts had added up to a negative amount, the description would be “Net cash used by operating activities”.

Indirect Method for Preparing the Cash Flow Statement

Companies may choose to use either the direct method or the indirect method when preparing the SCF section cash flows from operating activities. However, the indirect method is the dominant method used and the one we will explain.

Under the indirect method, the SCF section cash flows from operating activities begins with the amount of net income, which is taken from the company’s income statement. Since the net income was based on the accrual method of accounting, the amount of net income must be adjusted to the cash amount.

If an adjustment to the amount of net income is in parentheses, it is subtracted from net income. It indicates that the cash amount was less than the related amount on the income statement. Adjustments in parentheses can also be interpreted to be unfavorable for the company’s cash balance.

An adjustment to net income that is not in parentheses is a positive amount, which indicates the cash amount was more than the related amount on the income statement. A positive adjustment can also be interpreted to be favorable for the company’s cash balance.

Adjustments to Convert the Net Income Amount to the Cash Amount

In the case of Example Corporation, the section cash flows from operating income begins with the company’s net income for the year: $230,000.

A large corporation often has 10 or more adjustments to convert the amount of net income to the amount of cash. However, we will limit our discussion to some of the more common adjustments shown on Example Corporation’s statement of cash flows:

-

Depreciation and amortization 63,000. Since this adjustment amount appears without parentheses, it indicates that the cash amount will be $63,000 more than the amount of net income. The reason is depreciation and amortization expense reduced the company’s net income, but it did not reduce the company’s cash balance. In other words, without this noncash expense of $63,000, the company would have seen its cash increase by $230,000 + $63,000.

-

Loss on sale of equipment 15,000. This amount appears without parentheses and therefore the company’s cash amount will be more than the net income. The reason is that Example Corporation’s net income had been reduced by this loss of $15,000. However, the company did not pay out the $15,000. Therefore, it is added to the amount of net income, causing the cash from operations to be greater by $15,000. (If cash is received from the sale of this noncurrent asset, the amount received is reported as a positive amount on the SCF in the section cash flows from investing activities.)

-

If there was a gain on the sale of a noncurrent asset, the amount of the gain would have increased net income. However, since the entire amount of cash received from the sale of a noncurrent asset is reported under cash flows from investing activities, the gain is subtracted from the amount of net income.

-

Increase in accounts receivable (21,000). Since this amount is in parentheses, it communicates that the company collected less cash than the amount of sales reported on the income statement. This is determined by examining how the balance in accounts receivable changed during the year. If the company’s receivables increased, it indicates that not all sales on the income statement were collected. This is viewed as unfavorable for the company’s cash balance. Therefore, the amount of the increase in accounts receivable is deducted from the amount of net income.

-

If the balance in the company’s accounts receivable had decreased, it indicates that the company collected more than the amount of sales reported on the income statement. Therefore, the amount of the decrease in receivables would be added to the amount of net income. The decrease in receivables is positive, favorable, and good for the company’s cash balance.

-

Decrease in prepaid expenses 3,000. If the balance in the current asset prepaid expenses had decreased, it meant that $3,000 of the amount of expenses on the income statement did not require using $3,000 of cash. Therefore, we add $3,000 to the amount of net income. In other words, using part of the prepaid amount instead of paying cash was favorable/positive for the company’s cash balance.

-

If the balance in prepaid expenses had increased during the year, it means the company had paid out more cash than the amount reported as expense on the income statement. Therefore, the increase in this current asset is subtracted from the amount of net income. In other words, increasing the balance in prepaid expense was not good for the company’s cash balance.

-

Decrease in accounts payable (28,000). If the balance in the current liability accounts payable had decreased, it indicates that the company paid its suppliers more than the amount of expenses reported on the income statement. As a result, the decrease in payables is shown in parentheses. Paying the suppliers more than the related expenses reported on the income statement had a negative or unfavorable effect on the company’s cash balance.

-

-

If the balance in accounts payable had increased, it would indicate the company paid its suppliers less than the expenses reported on the income statement. Paying out less cash is good/favorable for the company’s cash balance. Therefore, an increase in payables is added to the amount of net income.

Quick Guide to Changes in Current Asset Balances

When adjusting a company’s net income for changes in the balances of the current assets, the following may be a helpful guide:

-

If a current asset’s balance (other than cash) had increased, the amount of the increase is subtracted from the amount of net income. The increase in a current asset (other than cash) had a negative/unfavorable effect on the company’s cash balance.

-

If a current asset’s balance (other than cash) had decreased, the amount of the decrease is added to the amount of net income. The decrease in a current asset (other than cash) had a positive/favorable effect on the company’s cash balance.

Quick Guide to Changes in Current Liability Balances

When adjusting a company’s net income for changes in the balances of the current liabilities, the following may be a helpful guide:

-

If a current liability’s balance (other than loans payable) had increased, the amount of the increase is added to the amount of net income. The increase in a current liability had a positive/favorable effect on the company’s cash balance.

-

If a current liability’s balance (other than loans payable) had decreased, the amount of the decrease is subtracted from the amount of net income. The decrease in a current liability had a negative/unfavorable effect on the company’s cash balance.

The adjustments reported in the operating activities section will be demonstrated in detail in A Story To Illustrate How Specific Transactions and Account Balances Affect the Cash Flow Statement.

Next, we will discuss the cash flows involving a company’s investing activities.

Cash Flows from Investing Activities

The investing activities section of the SCF reports the cash inflows and cash outflows related to the changes that occurred in the noncurrent (long-term) assets section of the balance sheet.

Examples of investing activities include the following:

- Capital expenditures (additions to property, plant and equipment)

- Proceeds from the sale of property, plant and equipment

- Purchase of long-term investments

- Proceeds from the sale of long-term investments

Our discussion uses Example Corporation’s cash flows from investing activities:

Capital expenditures are the amounts spent for acquiring, adding, and/or improving noncurrent assets used in a business. (Large amounts spent for repairing an existing asset are reported as expenses on the current period’s income statement.)

Since the amount spent by Example Corporation for capital expenditures required an outflow of cash, the amount appears in parentheses: (300,000). You can also think of the amount spent as unfavorable for the company’s cash balance and/or cash used.

Proceeds from sale of equipment 40,000 is a positive amount since this is the amount of cash that was received. In other words, the $40,000 was an inflow of cash and therefore favorable for Example Corporation’s cash balance.

(Also see our discussion of Cash Flows from Operating Activities for the reporting of the gains and losses on the sale of noncurrent assets.)

Amounts spent to acquire long-term investments are reported in parentheses, since it required an outflow or use of cash.

The proceeds (cash received) from the sale of long-term investments are reported as positive amounts since the proceeds are favorable for the company’s cash balance.

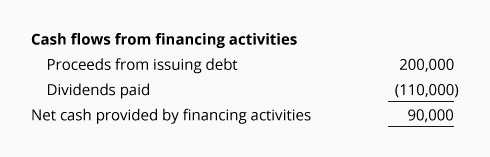

Cash Flows from Financing Activities

The cash inflows and outflows from financing activities are related to the changes in the following balance sheet sections:

- Noncurrent (long-term) liabilities

- Stockholders’ equity (or owner’s equity)

- Loans and similar debt reported under current liabilities

Examples of the descriptions and amounts typically reported under cash flows from financing activities include the following:

- Proceeds from long-term debt

- Repayment of long-term debt

- Proceeds from issuing capital stock

- Payment of dividends

- Purchase of treasury stock

- Change in short-term debt

Our discussion of financing activities will use the following section of Example Corporation’s SCF:

Assume that Example Corporation issued a long-term note/loan payable that will come due in three years and received $200,000. As a result, the amount of the company’s long-term liabilities increased, as did its cash balance. Therefore, this inflow of $200,000 is reported as a positive amount in the financing activities section of the SCF.

Next, assume that Example Corporation distributed $110,000 of cash dividends to its stockholders. The $110,000 cash outflow has an unfavorable or negative effect on the company’s cash balance. As a result, the amount will be shown in the financing section of the SCF as (110,000).

When Example Corporation repays its loan, the amount of the principal repayment will appear in parentheses (since it will be an outflow of cash).

If Example Corporation issues additional shares of its common stock, the amount received will be reported as a positive amount.

Reconciling the Increase in Cash from the SCF with the Change in Cash Reported on the Balance Sheet

The three net cash amounts from the operating, investing, and financing activities are combined into the amount often described as net increase (or decrease) in cash during the year.

In Example Corporation the net increase in cash during the year is $92,000 which is the sum of $262,000 + $(260,000) + $90,000.

As was shown in the Example Corporation’s SCF the net increase for the year was added to the beginning cash balance to arrive at the ending cash balance.

The ending cash balance should agree with the amount reported as cash on the company’s December 31, 2025 balance sheet.

Supplemental Information

Since all transactions cannot be adequately communicated through the relatively few amounts reported on the financial statements, companies are required to have notes to the financial statements.

Some required information for the SCF that will be disclosed in the notes includes significant exchanges that did not involve cash, the amount of interest paid, and the amount of income taxes paid.

A Story To Illustrate How Specific Transactions and Account Balances Affect the Cash Flow Statement

The remainder of our SCF explanation illustrates how specific transactions and account balances affect a company’s cash flow statement (as well as its income statement and balance sheet).

We will use an easy-to-follow story with only one transaction per day to help you better understand the cash flow statement. You will also see how the financial statements are connected.

Matt is a college student who enjoys buying and selling merchandise using the Internet. On January 2, 2025, he decided to turn his hobby into a business called “Good Deal Co.” Each month the Good Deal Co. had one or two transactions. Matt wants to prepare an income statement, balance sheet, and a statement of cash flows for the current month and for the year-to-date period. He asks our help in preparing and understanding the SCF.

January Transactions and Financial Statements

On January 2, 2025 Matt invested $2,000 of his personal money into his sole proprietorship, Good Deal Co. On January 20, Good Deal buys 14 graphing calculators at a cost of $50 per calculator (which was about 50% of the selling price Matt has observed at the retail stores). The total cost to Good Deal for all 14 calculators was $700. Good Deal had no other transactions during January.

Matt prepared the income statement and balance sheet for his new business as of January 31, 2025 as shown below:

Note that the $50 cost of each calculator is not reported on the income statement as an expense until a sale occurs. (This is part of the accrual basis of accounting and the related matching principle.)

The cost of each unsold calculator will be reported as the asset inventory on the company’s balance sheet. Therefore, the 14 calculators purchased at $50 each will appear as $700 of inventory. The company’s balance sheet will report the remaining cash balance of $1,300 ($2,000 – $700).

From the information on the company’s income statement and balance sheet, we prepared the statement of cash flows for the month of January:

Under the indirect method, the operating activities section of the statement of cash flows (SCF) begins with the company’s net income. Note that Good Deal Co.’s January net income of $0 appears as the first item in the operating activities section of the SCF. Since the net income was determined through the accrual basis of accounting, we will list the adjustments needed to convert the amount of net income to the net cash provided (used) by operating activities.

Amounts in parentheses indicate a negative effect on the company’s cash balance. An amount in parentheses can also be viewed as a cash outflow or cash used.

Amounts without parentheses indicate a positive effect on the company’s cash balance. An amount without parentheses can also be viewed as a cash inflow or cash provided.

For example, from Good Deal Co.’s balance sheet we know its inventory increased from $0 at January 1 to $700 at January 31. Increasing inventory by $700 during January was not good for the company’s cash balance since the company paid out $700. Therefore, under Operating Activities on Good Deal Co.’s SCF the Increase in inventory appears as (700) since it had an unfavorable or negative effect on the company’s cash balance.

If the inventory had decreased by $700, the adjustment would have been a positive 700. The reason is that by decreasing its inventory the company avoided purchasing $700 of the cost of goods sold that reduced net income. Not having to pay $700 of the cost of goods sold was good/positive for the company’s cash balance.

The financing activities section shows Investment by owner 2,000 which had a positive effect of $2,000 on the company’s cash. This amount could be discovered by examining the change in the owner’s capital account between the two balance sheet dates. Again, you can view the positive $2,000 as cash that flowed in or was good for the company’s cash balance.

The combination of the $700 cash outflow from operating activities and the $2,000 cash inflow from financing activities is shown as Net increase in cash. The net increase of $1,300 agrees with the change in the cash balances reported on the balance sheet: At January 1, the cash balance was $0; and at January 31, the cash balance was $1,300.

Here’s a Tip

For a change in assets (other than cash), the change in Cash is in the opposite direction. Recall that when Inventory increased by $700, Cash decreased by $700.

For a change in liabilities and owner’s equity, the change in Cash is in the same direction. Recall that when the owner invested cash in the company, Owner’s Equity increased and Cash increased.

February Transactions and Financial Statements

On February 28, 2025, Good Deal sold 10 calculators to a nearby high school for $80 each. Matt delivered the calculators on February 28 and gave the school an $800 invoice due by March 10. Matt received $800 from the school on March 8.

Matt prepared the following income statement for the month of February:

Under the accrual basis of accounting, revenues (such as sales of products) are reported on the income statement in the period in which a sale occurs. Typically, the sale occurs when the products or goods are shipped or delivered to the buyer (or services are provided). As the February 28 transaction shows, revenues can occur before cash is received. Since Good Deal Co. delivered 10 calculators at a selling price of $80 each to a reputable buyer, it had earned revenues of $800 on February 28.

Under the accrual basis of accounting, expenses should be matched with revenues when there is a cause and effect relationship. This means that a retailer should match its sales with the related cost of goods sold. In the case of Good Deal Co., it needs to match the cost of the 10 calculators sold with the revenues from selling 10 calculators. Therefore, its February income statement shows expenses of $500 (10 X $50) being subtracted from its revenues of $800.

Other expenses such as selling, general, administrative, and interest expenses must also be reported on the income statement when 1) they can be matched with the revenues, or 2) when a cost has expired, has been used up, or has no future value. If Good Deal Co. was renting a storage space for $50 per month, each month’s income statement would also list rent expense of $50.

In summary, Good Deal Co. correctly reported $800 of revenues, $500 of expenses, and $300 of net income even though no cash flowed in or out during February.

The statement of cash flows (SCF) for the month of February begins with the accrual accounting net income of $300, which must be converted/adjusted to the net cash from operating activities. Recall that the income statement reported revenues of $800, and the balance sheets from January 31 and February 28 will indicate that accounts receivable increased from $0 to $800. This increase in accounts receivable of $800 indicates that the company did not collect $800 of the revenues that were reported on February’s income statement. Allowing accounts receivable to increase is not good for the company’s cash balance. When something is not good for the company’s cash balance, the amount is shown in parentheses. Again, the (800) indicates the negative effect on the company’s cash caused by the company not yet collecting the cash from its credit sales, reported on its income statement.

When a company’s inventory decreases, it is good/positive for a company’s cash. The reason is the company is not paying out cash for the items it is removing from inventory. While Good Deal Co.’s income statement for the month of February reported “Expenses 500” for the cost of its goods sold, the company did not pay out the $500 during February. Therefore, the company shows a positive $500 on its SCF as an adjustment to the net income amount. The $500 adjustment is not reporting what happened to the amount of inventory, it is reporting the necessary adjustment to convert the accrual accounting net income to the cash amount.

Now let’s look at the year-to-date financial statements covering the two-month period of January 1 through February 28:

The year-to-date net income of $300 increases the owner’s equity on the balance sheet. Note the connection between the bottom line of the year-to-date income statement and the change in Matt Jones, Capital on the balance sheet. Matt Jones, Capital has increased from $2,000 to $2,300.

The SCF for the two months of January 1 through February 28, begins with the accrual accounting net income of $300. Since this is not the amount of cash from operating activities, the net income must be adjusted to the net amount of cash from operating activities.

During this two-month time period, the company’s accounts receivable increased from $0 to $800. An increase in accounts receivable means that the customers purchasing on credit did not yet pay for all the credit sales the company reported on the income statement. Therefore, we subtract the increase in accounts receivable from the company’s net income. Not having collected the total amount of past credit sales was not good for the company’s cash balance. For these reasons, the amount of the company’s accrual net income must be adjusted downward. Again, the reported (800) is the adjustment to the net income amount because of the increase in accounts receivable.

During the two-month time period, the company’s inventory changed from $0 on January 1 to $200 at February 28. (Recall that the company had purchased 14 calculators at a cost of $50 each and then sold 10 calculators. That left 4 calculators in inventory at a cost of $50 each.) The increase in inventory from $0 to $200 during this two-month time period required the company to spend (have a cash outflow of) $200. The use of cash for adding goods to inventory is also viewed as not good for the company’s cash balance and is therefore reported on the SCF as (200).

Given these adjustments, the net cash flow from operating activities is a net cash outflow of (700). (The calculation is $300 cash inflow – $800 cash outflow – $200 cash outflow.) The net cash outflow is presented as a negative amount and is described as net cash used in operating activities.

The cash flow statement also shows $2,000 of financing by the owner. When this is combined with the negative $700 from operating activities, the net change in cash for the first two months is a positive $1,300. This agrees to the change in cash on the balance sheet—none on January 1, but $1,300 on February 28.

March Transactions and Financial Statements

On March 8 Good Deal receives $800 for the calculators sold to the school on February 28. No other transactions occurred in March. (Note that this $800 is a March receipt but is not revenue in March. The revenue was earned and was reported on February’s income statement.)

The income statement for the one month ending on March 31 is shown here:

The income statement for the three months of January 1 through March 31 is:

Note that the 3-month year-to-date net income of $300 causes the amount in the owner’s capital account (on the following balance sheet) to increase from $2,000 to $2,300. The receipt of $800 caused the cash to increase from $1,300 to $2,100 and accounts receivable to decrease to zero.

The SCF for the period of January 1 through March 31 is shown here:

The statement of cash flows (SCF) for the first three months of the business (January 1 through March 31) begins with the company’s accrual accounting net income of $300. This amount must be adjusted to show the net cash from operating activities (which are the company’s activities pertaining to the purchasing/producing of goods and selling of goods and/or providing services).

For the 3-month period of the SCF the company’s inventory increased from $0 to $200 at March 31. Therefore, we know that $200 of the company’s cash was used to increase its inventory. Recall that the use of cash, cash outflows, and money spent have a negative effect on the company’s cash balance and are reported as a negative amount on the SCF. Therefore, the $200 increase in inventory must be shown as (200). [If the inventory had decreased, the amount would have been a positive 200, since selling items from inventory is positive/good for the company’s cash balance.]

Since the amount of the company’s accounts receivable was $0 at January 1, and $0 at March 31, there is no adjustment and this line could have been omitted.

The combination of the positive net income of $300 and the adjustment for the cash used to increase inventory (200) results in the net cash provided by operating activities of a positive $100.

The owner’s $2,000 investment in January was a source of cash (hence it was a cash inflow, was good for the company’s cash balance, etc.) and is listed as a positive 2,000 in the section described as financing activities.

Finally, the combination of the amounts from the three sections of the SCF is $2,100. This agrees with the change in the amount of cash on the company’s balance sheets: $0 on January 1, and $2,100 on March 31.

Next, we will prepare a SCF for the month of March. To do this we will compare the company’s balance sheet of March 31 with its balance sheet of February 28:

Look at the “Change” column above. The first amount, a positive $800 change in the Cash account, will serve as a “check figure” for the line Net increase in cash on the cash flow statement for the month of March. In other words, the cash flow statement for March must end up explaining the $800 increase in the Cash reported on the balance sheet. The other balance sheet amounts that changed will be used on the statement of cash flows to identify the reasons for the $800 increase in cash.

Since there were no revenues and no expenses in March, the income statement for the one month of March (shown earlier) reported no net income. This $0 of net income will be shown as the first amount reported on the statement of cash flows. The changes in the balance sheet accounts from February 28 to March 31 provided the other information needed for the following SCF for the month of March:

Let’s review the cash flow statement for the month of March 2025:

-

Net income for March is $0, since there were no revenues, gains, expenses, or losses.

-

Cash increased by $800 because $800 of accounts receivable were collected during March.

-

Inventory did not change, so Cash was not affected. (We could omit this line since it had no effect on cash.)

-

There were no changes in long-term assets during March, so nothing is reported in the investing activities section.

-

There were no changes in short-term loans payable, long-term liabilities, or owner’s equity. Therefore, nothing is reported in the financing activities section.

-

The sum of the amounts on the statement of cash flows is a positive $800. This amount agrees to the increase in the cash balance from $1,300 on February 28 to $2,100 on March 31.

April Transactions and Financial Statements

On April 28 Good Deal ordered $150 of supplies on account. The supplies arrived on April 30 along with an invoice showing that the entire $150 is due by May 30. None of the supplies were used in April. This was the only transaction during April.

Matt prepared the following financial statements for Good Deal Co. as of April 30:

Since no supplies were used in April, there is no Supplies Expense. The $150 will be reported on the balance sheet in the asset account Supplies.

The balance sheet now includes $150 for the asset supplies and $150 for the liability accounts payable.

A balance sheet comparing April 30 amounts to March 31 amounts and the resulting differences or changes is shown here:

The changes that occurred during the month of April will be used to prepare the SCF for the month of April.

The cash flow statement for the month of April reports that there was no change in the Cash account from March 31 through April 30. The operating activities section reports the increase in Supplies and the resulting negative adjustment to the amount of net income. It also reports the increase in Accounts Payable and the resulting positive adjustment to the amount of net income.

Here’s a Tip

On the statement of cash flows, think of the positive amounts (the numbers not in parentheses) as good for the company’s cash balance. For example, if the company doesn’t pay its bills, that’s good for the company’s cash balance (but bad for the liability Accounts Payable which increases).

Think of the negative amounts (the numbers within parentheses) as not good for cash. For example, if a company pays a bill, that’s not good for its cash balance.

The following comparative balance sheet shows the changes between December 31, 2024 and April 30, 2025:

The changes will be used to prepare the SCF for the four months ended April 30.

The SCF for the period of January 1 through April 30 is:

Let’s review the statement of cash flows for the four months ended April 30:

-

The operating activities section of the SCF starts with the net income of $300 that was earned during the four-month period. The increase in inventory was not good for cash, as shown by the negative adjustment of $200. Similarly, increasing the amount of supplies on hand was not good for cash and it is reported as a negative $150. The increase in accounts payable was good for the cash balance (since some bills were not paid); therefore, the increase in accounts payable appears as a positive $150. Combining the amounts, the net change in cash that is explained by operating activities is a positive $100.

-

There were no changes in long-term assets. As a result, no amount is shown for investing activities.

-

There were no changes in short-term loans payable or long-term liabilities. However, there was a change in owner’s equity since December 31. As a result, the financing activities section reports the owner’s $2,000 investment in Good Deal Co. as a positive amount.

-

Combining the amounts in operating, investing, and financing activities, the cash flow statement reports an increase in cash of $2,100. This agrees with the change in the balance sheet’s Cash from $0 on December 31, 2024 to $2,100 on April 30, 2025.

May Transactions and Financial Statements

On May 30 Good Deal pays its accounts payable of $150. On May 31 Good Deal purchases office equipment (a new computer and printer) that will be used exclusively in the business. The cost of the office equipment is $1,100 and is paid in cash. There were no other transactions in May.

A balance sheet comparing May 31 amounts to April 30 amounts and the resulting differences or changes is shown here:

The following comparative balance sheet shows the changes between December 31, 2024 and May 31, 2025:

The SCF for the period of January 1 through May 31 is:

Let’s review the cash flow statement for the five months ended May 31:

-

The operating activities section starts with the net income of $300 for the five-month period. The increase in Inventory was not good for cash, as shown by the negative adjustment of $200. Similarly, the increase in Supplies was not good for cash and it is reported as a negative adjustment of $150. Combining the amounts, the net change in cash that is explained by operating activities is a negative $50.

-

The investing activities section reports the increase in long-term assets as (1,100) since it was a cash outflow of $1,100. The additions to property, plant and equipment are frequently described as capital expenditures.

-

There were no changes in short-term loans payable or long-term liabilities. However, there was a change in owner’s equity since December 31. As a result, the financing activities section of the SCF reports the owner’s investment of $2,000, which increased Good Deal’s cash balance.

-

Combining the amounts from the operating, investing, and financing activities, the SCF reports an increase in cash of $850. This agrees with the change in the Cash amounts reported on the balance sheets dated December 31, 2024 and May 31, 2025.

Depreciation Expense

Depreciation moves the cost of an asset from the balance sheet to Depreciation Expense on the income statement in a systematic manner during an asset’s useful life. The accounts involved in recording depreciation are Depreciation Expense and Accumulated Depreciation. As you see, cash is not involved. In other words, depreciation reduces net income on the income statement, but it does not reduce the company’s cash that is reported on the balance sheet.

Since we begin the statement of cash flows with the net income figure taken from the income statement, we need to adjust the amount of net income by adding back the amount of the Depreciation Expense.

Depletion Expense and Amortization Expense are accounts similar to Depreciation Expense. They involve allocating the cost of a long-term asset to an expense over the useful life of the asset, but no cash is involved.

Here’s a Tip

In the operating activities section of the cash flow statement, add back expenses that did not require the use of cash. Examples are depreciation, depletion, and amortization expense.

Next, we examine how depreciation expense is reported on the Good Deal Co.’s financial statement.

June Transactions and Financial Statements

The only transaction recorded by Good Deal during June was the depreciation of its office equipment. Recall that on May 31 Good Deal purchased the office equipment (a new computer and printer) for $1,100 and it was put into service on the next day. Let’s assume that depreciation expense of $20 per month is recorded by Good Deal. As a result, Good Deal’s financial statements at June 30 will be as follows:

A balance sheet comparing June 30 amounts to May 31 amounts and the resulting differences or changes is shown here:

The cash flow statement for the month of June illustrates why depreciation expense needs to be added back to net income. Good Deal did not spend any cash in June, however, the entry in the Depreciation Expense account resulted in a net loss on the income statement. On the SCF, we convert the bottom line of the income statement for the month of June (a loss of $20) to the net amount of cash provided or used by operating activities, which was $0. This is done with a positive adjustment which adds back the $20 of depreciation expense.

The following comparative balance sheet shows the changes between December 31, 2024 and June 30, 2025:

The SCF for the period of January 1 through June 30 is:

Let’s review the cash flow statement for the six months ended June 30:

-

The operating activities section began with the net income of $280 for the six-month period. Depreciation expense is added back to net income because it was a noncash transaction (net income was reduced, but there was no cash outflow for depreciation). The increase in the Inventory account was not good for cash, as shown by the negative $200. Similarly, the increase in Supplies was not good for cash and it is reported as a negative $150. Combining the amounts, the net change in cash that is explained by operating activities is a negative $50.

-

The investing activities section reports the cash outflow of $1,100 for the purchase of office equipment.

-

There were no changes in short-term loans payable or long-term liabilities. However, there was the owner’s $2,000 investment in the Good Deal Co. Therefore, the financing activities section reports a positive 2,000.

-

Combining the amounts from the operating, investing, and financing activities, the SCF reports an increase in cash of $850. This agrees with the change in the Cash amounts reported on the balance sheets dated December 31, 2024 and June 30, 2025.

Disposal of Assets

If a company disposes of (sells) a long-term asset for an amount different from the amount in the company’s accounting records (the asset’s book value), an adjustment must be made to the amount of net income appearing as the first item on the SCF.

To illustrate, assume a company sells one of its delivery trucks for $3,000. The truck is in the accounting records at its original cost of $20,000. Its accumulated depreciation is $18,000. Combining the $20,000 and the $18,000 results in a book value (or carrying value) of $2,000.

Because the cash received/proceeds from the sale of the truck was $3,000 and the book value was $2,000 the difference of $1,000 is reported as a gain on the income statement. As a result, the company’s net income will increase by $1,000. (If the truck had sold for $1,500 there would be a $500 loss, which would reduce the company’s net income.)

One of the rules in preparing the SCF is that the entire proceeds received from the sale of a long-term asset must be reported in the section of the SCF entitled investing activities. This presents a problem because any gain or loss on the sale of an asset is included in the amount of net income shown in the SCF section operating activities. To overcome this problem, each gain is deducted from the net income and each loss is added to the net income in the operating activities section of the SCF.

We will demonstrate the loss on the disposal of an asset in Good Deal’s next transaction.

July Transactions and Financial Statements

On July 1, Matt decides that his company no longer needs its office equipment. Good Deal used the equipment for one month (June 1 through June 30) and had recorded one month’s depreciation of $20. This means the book value of the equipment is $1,080 (the original cost of $1,100 less the $20 of accumulated depreciation). On July 1, Good Deal sells the equipment for $900 in cash and reports the resulting $180 loss on sale of equipment on its income statement. There were no other transactions in July.

The income statement for the month of July will show how the disposal of the equipment is reported:

The income statement for the period of January 1 through July 31 is:

The following comparative balance sheet shows the changes that occurred during July:

The SCF for the one month of July is:

Let’s review the cash flow statement for the month of July 2025:

-

Net income for July was a net loss of $180. There were no revenues, expenses, or gains, but there was a loss of $180 on the sale of equipment. However, the loss did not cause the company’s cash to decrease. The $900 of cash that was received is shown under investing activities.

-

There was no depreciation expense in July because the asset was sold on July 1. (We could have omitted the line “Depreciation Expense”.) Also, the current assets and current liabilities did not change in July.

-

The net amount of cash provided or used by operating activities during the month of July was $0.

-

The investing activities section reports the $900 received from the sale of its office equipment.

-

There was no change in short-term loans payable, long-term liabilities, or owner’s equity during July (other than the $180 loss on sale of equipment).

-

The sum of the amounts on the SCF for the month of July was a positive cash inflow of $900. This amount agrees to the increase in the company’s cash balance from June 30 to July 31.

-

The following comparative balance sheet shows the changes between December 31, 2024 and July 31, 2025:

The SCF for the period of January 1 through July 31 is:

Let’s review the cash flow statement for the seven months of January through July 2025:

-

Net income for the seven months was $100. This includes the company’s revenues, gains, expenses, and losses.

-

Included in the net income for the seven months is $20 of depreciation expense. This expense reduced net income but did not reduce the Cash account. Therefore, the $20 of depreciation expense is a positive adjustment to the $100 of net income.

-

Also included in the net income was the $180 loss on sale of equipment. This loss was reported on the income statement thereby reducing net income. However, cash was not reduced. Actually, cash of $900 was received from the sale of the equipment and it is reported in its entirety in the investing activities section of the SCF.

-

Inventory on July 31 is $200 (4 calculators at a cost of $50 each). Since the company began with no inventory, this increase in the Inventory account means that $200 of cash was used to increase inventory. Hence, the adjustment is shown in parentheses.

-

Supplies increased from none to $150. The increase in the Supplies account is assumed to have had a negative effect of $150 on the company’s cash.

-

Combining the amounts so far, we see that the net amount of cash from operating activities is a negative $50. In other words, rather than providing cash, the operating activities used a net $50 of cash.

-

There is cash outflow (or payment) of $1,100 to purchase the office equipment on May 31. On July 1, there was also a $900 cash inflow (or receipt) from the sale of the office equipment. Combining these two amounts results in the net outflow of $200 in the investing activities section as a source of cash.

-

The owner’s investment of $2,000 made on January 2 is reported in the financing activities section.

Net increase in cash during the seven months was a positive $1,750 (the combination of the totals of the three sections—operating, investing, and financing activities). This $1,750 agrees to the check figure—the increase in the cash from the beginning of January to July 31.

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Cash Flow Statement materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.

Earn Our Certificate

for This Topic

When you join PRO, you will receive instant access to 16 different Certificates of Achievement plus our Bookkeeping Certificate of Excellence.

View PRO Features