Introduction

It’s a fact of business—if a company has employees, it has to account for payroll and fringe benefits.

In this explanation of payroll accounting we will discuss the following payroll-related items:

Sample journal entries will be shown for several pay periods for hourly-paid employees and for salaried employees.

Many of the items discussed are subject to federal and state government regulations as well as labor contracts and company policies.

NOTE: When a company’s financial statements are prepared using the accrual basis of accounting, all wages (including salaries, commissions, bonuses, etc.) that have been earned by the company’s employees must be reported. This usually requires an accrual adjusting entry so that the company’s balance sheet reports a current liability for the wages that have been earned by the employees but have not been paid as of the final moment of the accounting period.

On the other hand, the company must report to the Internal Revenue Service (IRS) the amounts it has paid to its employees. (The reason is that employees’ personal income tax returns are prepared using the cash basis of accounting.) For instance, the IRS Form W-2, Wage and Tax Statement, that is given to employees in January reports the amounts paid to employees in the year that ended on December 31.

In this explanation of payroll accounting we will highlight some of the federal and state payroll-related regulations and provide links to some of the government agencies and publications. We conclude with sample accounting entries that a company will record so that its financial statements reflect the accrual basis of accounting.

Accrual Basis of Accounting and Matching Principle

Since the company’s financial statements must reflect the accrual basis of accounting, a company’s expenses should be reported as follows:

- Match expenses to the related revenues when a cause-and-effect relationship exists. For example, a retailer’s income statement should match the cost of goods sold (which may have been purchased and paid for in an earlier accounting period) in the accounting period in which the sales revenues are earned.

- If there is no cause-and-effect relationship but there is a future value that can be measured, the cost should be reported as an expense on the income statement in the period in which the cost is used up or expired.

- If a cost has no future value, it should be reported as an expense in the period in which it was incurred.

This means that on a retailer’s financial statements, the wages, salaries, commission, bonuses, etc. of its employees should be reported as follows:

- The amounts that were earned by the employees (and therefore incurred by the retailer) during the current accounting period should be reported as expenses on the retailer’s current period’s income statement (even if some of the amounts will be paid in a later accounting period or had been paid in an earlier accounting period).

- The amounts that were earned by the employees (and therefore incurred by the retailer) but have not been paid as of the final moment of the accounting period, must be reported as a current liability on the retailer’s balance sheet.

Let’s illustrate these concepts with four payroll examples:

- A company employs a student to work a total of five days—from December 26 through December 30, 2025. The company issues the student’s payroll check on the next scheduled payday, January 5, 2026.Even though the check is dated January 5, 2026, the matching principle requires that the company report the expense and the liability on the December 2025 financial statements when the work was performed (and the company incurred the liability). Because the student was only employed for the last five days of December, the company will not have any wage or fringe benefits expense for the student during January. The paycheck issued on January 5 merely reduces the company’s liabilities and cash.

- Let’s assume that a company gives its sales manager an annual bonus of 1% of sales, to be paid on January 15, 2026. The bonus amount is calculated by multiplying the sales from January 1 through December 31, 2025 times 1%.The accrual basis of accounting and the related matching principle require that the company report 1% of sales as a Bonus Expense on its income statement (and a liability for the total amount owed on its balance sheet) in every accounting period in which sales occurred in 2025. If the company violates the matching principle by ignoring the bonus expense throughout the year 2025 (when sales actually occurred) and reports the entire bonus amount as an expense for just one day (January 15, 2026), every income statement pertinent to 2025 will report too much net income and the income statement that includes January 15, 2026 will report too little net income. The matching principle requires that the bonus expense pertinent to the 2025 sales be matched with the 2025 sales on the 2025 income statement.If the entries are recorded properly, the balance sheet dated December 31, 2025 will report a current liability for the total bonus amount owed to the sales manager. On January 15, 2026 (when the company pays the bonus) the company will not have an expense; rather, the payment will reduce the company’s cash and reduce the current liability that was established when the bonus was recorded as an expense in 2025.

- A company has a vacation plan that will provide two weeks of vacation in the year 2026 if the employee worked the entire year of 2025. In the year 2025 (when the employee is working) the company reports the vacation expense on its 2025 income statement. The company’s December 31, 2025 balance sheet will report a current liability for the two weeks of vacation pay that was earned by each employee but not yet taken. In 2026 (when employees take the vacations that were earned and expensed in 2025), the company will reduce its cash and its vacation liability.

- A manufacturer begins operations in December and produces 1,000 units of product in December. The direct labor cost of $2,000 is assigned to the products. If all the units produced are sold in January, the $2,000 of direct labor cost will be part of the manufacturer’s inventory cost as of December 31. When the units are sold in January, the $2,000 of labor will be part of January’s cost of goods sold which is an expense on the January’s income statement.

As you learn about accounting for payroll and fringe benefits, keep the matching principle in mind. As the above examples show, the date on which a company pays wages or fringe benefits is not necessarily the date on which the company reports the expense on its financial statements.

WATCH NOW

Advance Your Career with Our PRO Training

Employees vs. Non-Employees

Payroll accounting pertains to a company’s employees. However, there are some non-employees that also carry out some of the company’s tasks. Here are a few examples:

- Many routine accounting tasks are performed by accountants who are employees, but some tasks are performed by accountants who are non-employees.

- Some of the computerized systems work is done by employees, but some computer tasks are performed by people who are non-employees.

- Office cleaning, grounds maintenance, and other tasks might be done by employees and some may be done by non-employees.

It is critical that employers properly classify each person performing tasks. A general rule is that the person is an employee (as opposed to an independent contractor, sole proprietor or business partner) if the employer:

- Has the right to control which tasks will be done, and

- Can control how the tasks will be done

To guide you further, the Internal Revenue Service (IRS) provides detailed information and examples in its Publication 15-A, Employer’s Supplemental Tax Guide (PDF).

Employees

When a company has employees, it will involve the following:

- Having an Employer Identification Number (EIN) obtained from the Internal Revenue Service (IRS)

- Completing the U.S. Citizenship and Immigration Services (USCIS) Form I-9, Employment Eligibility Verification for each individual hired in the U.S.

- Having employees complete the IRS Form W-4, Employee’s Withholding Certificates on which employees indicate if their federal income tax withholdings will be taxed as Single or Married and their number of allowances

- Recording each employee’s hours worked and amounts earned

- Withholding Social Security taxes, Medicare taxes, income taxes, and voluntary deductions

- Remitting the payroll withholdings and the employer-paid payroll taxes

- Remitting the voluntary deductions

- Issuing the employees’ paychecks or processing the direct deposits

- Providing employees with IRS Form W-2, Wage and Tax Statement by January 31

- Filing W-2 forms and IRS Form W-3, Transmittal of Wage and Tax Statements with the Social Security Administration (SSA) by January 31

- Filing IRS Form 941, Employer’s Quarterly Federal Tax Return

- Filing IRS Form 940, Employer’s Annual Federal Unemployment (FUTA) Tax Return

For more complete requirements including the critical dates and procedures for depositing payroll taxes, filing payroll forms, and distributing forms to employees see the following:

- IRS Publication 15, (Circular E), Employer’s Tax Guide

- IRS Publication 15-A, Employer’s Supplemental Tax Guide (Supplement to Pub. 15)

- IRS Publication 15-B, Employer’s Tax Guide to Fringe Benefits

- Your state’s agencies/departments’ rules and regulations

Independent Contractors

Independent contractors are often referred to as non-employees. Hence, an independent contractor is not an employee, sole proprietor of the business, or business partner. Independent contractors are paid through the company’s accounts payable system. As a result, an independent contractor submits an invoice for the services provided and the company issues a non-payroll check.

If the amount paid to an independent contractor (nonemployee compensation) during a calendar year is $600 or greater, the company must issue IRS Form 1099-NEC. However, if the provider of services is a corporation, Form 1099-NEC is not required.

Proprietors and Partners

A sole proprietor is the owner of a business organized as a sole proprietorship and is not considered to be either an employee or an independent contractor. Similarly, partners of a business partnership are neither employees of the business nor independent contractors.

Salaries and Wages

In this section of payroll accounting we focus on the gross amounts earned by the employees of a company.

Salaries

Salaries are usually associated with “white-collar” workers such as office employees, managers, professionals, and executives. Salaried employees are often paid semimonthly (e.g., on the 15th and last day of the month) or biweekly (e.g., every other Friday) and their salaries are often stated as a gross annual amount, such as “$48,000 per year.” The “gross” amount refers to the pay an employee has earned before withholdings are made for such things as taxes, donations to United Way, savings plans, etc.

Since salaried employees earn a specified annual amount, it is likely that their gross pay for each pay period is the same recurring amount. For example, if a manager’s salary is $48,000 per year and salaries are paid semimonthly, the manager’s gross pay will be $2,000 for each of the 24 pay periods. (If the manager is paid biweekly, the gross pay would be $1,846.15 for each of the 26 pay periods.) A salaried employee’s work period usually ends on payday; for example, a paycheck on January 31 usually covers the work period of January 16–31. This is convenient for accounting purposes if the company prepares financial statements for each calendar month.

NOTE: Occasionally, a salaried employee who is paid biweekly feels they are being “cheated” because their paycheck amounts are less than the paycheck amounts received by a salaried employee who is paid semimonthly. To illustrate, let’s assume that the person paid biweekly has a gross salary of $2,000 on each paycheck. The person’s friend who is paid semimonthly receives a gross salary of $2,166.67 on each paycheck. The biweekly-paid person thinks that the employer is paying its employees biweekly in order to save $116.67 each payday for every employee. This person doesn’t consider that being paid biweekly means there will be 26 paychecks during the year, while the person being paid semimonthly will have only 24 paychecks during the year. The following shows that both are receiving the same gross salary for the year:

Biweekly-paid employee = 26 paychecks X $2,000 = $52,000 for the year.

Semimonthly-paid employee = 24 paychecks X $2,166.67 = $52,000 for the year.

Here are two additional points that may explain the misconception:

- If you divide the 52 weeks in a year by the 12 months in a year, there are on average 4.333 weeks in a month (not 4 weeks in a month)

- The 52 weeks in a year times 40 hours in a workweek = 2,080 work hours in a year. The 2,080 work hours divided by 12 months in a year = approximately 173 work hours in a month (not 160 work hours in a month)

Understanding these points will be helpful in calculating a salaried employee’s hourly rate of pay and overtime pay earned by salaried employees.

Wages

Wages are often associated with production employees (sometimes referred to as “blue-collar” workers), non-managers, and other employees whose pay is dependent on hours worked. The pay for these employees is generally stated as a gross, hourly rate, such as “$13.52 per hour.” Again, the “gross” amount refers to the pay an employee earns before withholdings are made for such things as taxes, contributions, and savings plans.

Hourly-paid employees receiving wages are often paid weekly or biweekly. To determine the gross wages earned during a work period, the employer multiplies each employee’s hourly rate times the number of work hours recorded for the employee during the work period. Due to the extra time needed to make calculations for each employee, hourly-paid employees typically receive their paychecks approximately five days after the work period has ended.

When the hourly-paid employees have work periods that are weekly or biweekly, but the company’s financial statements cover calendar months, the company will need to prepare an accrual-type adjusting entry at the end of the month. If hourly wages are a significant portion of a company’s expenses, it is critical that the company report the correct amount of wages expense that pertains to the 30 or 31 days in the month, not the 28 days in a four-week work period. The company’s balance sheet must also report a liability for the amount owed to the employees as of the end of the month.

Other Uses of the Term “Wages”

While many use the term “wages” to indicate the compensation earned by hourly-paid employees, the Internal Revenue Service (IRS) often uses the term to mean the wages, salary, bonuses, etc. paid to an employee. For example the annual maximum amount subject to the Social Security tax is referred to as the “annual wage limit”. Similarly, the IRS Form W-2 is entitled Wage and Tax Statement.

Throughout our explanation, bonuses paid to employees and sales commissions paid to employees will be considered to be part of salaries or wages.

Minimum Wage and Overtime Pay

The Wage and Hour Division (WHD) of the U.S. Department of Labor is charged with administering the Fair Labor Standards Act (FLSA), which requires that employees be paid:

- A minimum wage for all hours worked, and

- Overtime at time and one-half of the regular or straight-time rate of pay for hours worked that are in excess of 40 hours in the workweek.

Some companies and some employees may be exempt from the FLSA rules due to the company’s size or other criteria. However, an employer must also review its state’s regulations and is required to follow the state regulation if it is more beneficial for the employee than the federal regulation. For example, some states require a minimum wage that is much larger than the federal minimum wage. There are also a few states that require overtime be paid for any hours worked in excess of 8 on any workday.

The U.S. Department of Labor, Wage and Hour Division, has Fact Sheet #17A which summarizes the federal exemptions. It is available at https://www.dol.gov/agencies/whd/fact-sheets/17a-overtime. At the end of the fact sheet is a link to the official federal regulations.

Minimum Wage

The federal minimum wage and each state’s minimum wage can be found through:

https://www.dol.gov/general/topic/wages/minimumwage

Overtime Pay

Overtime refers to time worked in excess of 40 hours per workweek. Whether or not employees are paid for overtime depends on each employee’s job responsibilities and rate of pay not the employee’s job title. As a result some employees are exempt from overtime pay and some are not. For example, highly-paid executives are considered to be “exempt”; and therefore their employers are not required to pay them for their overtime hours because (1) their compensation is high, and (2) they can control their work hours. Highly-paid executives do not need state or federal wage and hour laws to protect them from employer abuse.

On the other hand, office clerks earning an annual salary of $18,000 per year are probably not in control of their work hours. If the clerks work for an executive who decides to work 60 hours per week, the clerks need to be protected from having to work 60 hours per week for no more pay than they would receive for 40 hours of work. These employees are considered to be “nonexempt” from the overtime rules and therefore must be paid overtime compensation. Some companies have been known to classify “hourly wage” employees as “salaried” in hopes of making them exempt from overtime pay. Federal and state laws exist to prevent such unfair treatment of employees.

When processing payroll, don’t assume that it’s only the hourly-paid employees who receive overtime pay. State and federal laws require overtime payments to lower-paid salaried employees. It is also possible that some generous employers will give overtime pay to employees who are not required by law to receive it.

For information on the current minimum amount that a salaried employee must earn in order to be considered exempt from being paid overtime, see the U.S. Department of Labor, Wage and House Division website.

Overtime Premium

An overtime premium refers to the “half” portion of “time-and-a-half” or “time-and-one-half” overtime pay. For example, assume an employee in the production department is expected to work 40 hours per week at $10 per hour. If the employer requires the employee to work 42 hours in a given workweek, the extra two hours are paid at time-and-a-half and the employee will earn gross wages of $430 for the week (40 hours x $10 per hour, plus 2 overtime hours x $15 per hour). The gross wages can also be computed as 42 hours at the straight-time rate of $10 per hour plus 2 hours times the overtime premium of $5 per hour.

Calculating Overtime Pay for a Salaried Person

Let’s assume that an office clerk receives an annual salary of $18,000 per year and is expected to work 40 hours per week. However, during a recent workweek the clerk was required to work an additional 4 hours. This person’s salary and responsibilities require the employer to pay overtime at the rate of time-and-a-half for the additional 4 hours. The overtime pay calculation is as follows:

- The straight-time hourly rate for the annual salary of $18,000 is: $18,000 divided by 2,080 hours (40 hours in workweek X 52 weeks) = $8.65 per hour

- The overtime premium (which is half of the straight-time hourly rate) is: $8.65 times 50% = $4.33 per hour

- The time-and-a-half rate is: $8.65 + $4.33 = $12.98 for each overtime hour

Assuming the clerk is paid semimonthly, the clerk’s next paycheck will consist of the following:

- Regular salary amount of $750.00 ($18,000 divided by 24 semimonthly pay periods per year)

- Overtime pay is: 4 overtime hours X $12.98 (from above) = $51.92

- Office clerk’s pay for the semimonthly period = regular salary of $750.00 + overtime pay of $51.92 = $801.92

Federal Insurance Contributions Act (FICA)

An important part of U.S. payroll accounting involves the Federal Insurance Contributions Act (FICA), which consists of two federal programs:

- Old age, survivors and disability insurance (OASDI) which is financed by the Social Security tax

- Hospital insurance for people age 65 and older which is financed by the Medicare tax

The Social Security taxes and the Medicare taxes come from the following:

- Employees through payroll deductions/withholdings, and

- Employers who must pay an amount similar to the amount withheld from employees’ gross pay. (The amount owed by the employer will be slightly less when an employee earns more than $200,000 in a calendar year.)

Summary of FICA’s effect on a company’s payroll processing:

Examples using the above table:

- An employee with wages of $100,000 will have FICA payroll withholdings amounting to $7,650 ($6,200 of Social Security tax + $1,450 of Medicare tax). In addition, the employer will have FICA expense of $7,650 ($6,200 of Social Security tax + $1,450 of Medicare tax). As a result, the employer must remit $15,300 to the U.S. Treasury.

- An employee with wages of $190,000 will have Social Security tax withholdings of $11,439.00 ($184,500 x 6.2%) + Medicare tax withholdings of $2,755.00 ($190,000 x 1.45%). The employer must match the amounts and remit $28,388.00 ($11,439.00 + $11,439.00 + $2,755.00 + $2,755.00).

- An employee with wages of $300,000 will have Social Security tax withholdings of $11,439.00 ($184,500 x 6.2%) + Medicare tax withholdings of $4,350 ($300,000 x 1.45%) + Additional Medicare Tax withholdings of $900 ($100,000 x 0.9%). The employer must match the employee’s amounts except for the Additional Medicare Tax and remit $32,478.00 ($11,439.00 + $11,439.00 + $4,350.00 + $4,350.00 + $900).

Payroll Withholdings: Taxes & Benefits Paid By Employees

This section of payroll accounting focuses on the amounts withheld from employees’ gross pay. (Later we will discuss the payroll taxes that are not withheld from employees’ gross pay.)

The U. S. income tax system and many state income tax systems require employers to withhold payroll taxes from their employees’ gross salaries, wages, bonuses, etc. The withholding of taxes and other deductions from employees’ paychecks affects the employer in several ways:

- The amount paid to employees on payday is reduced

- The employer must record a current liability in its accounting records for the amount withheld

- The employer must remit the withheld amounts by the required dates

Failure to remit the payroll taxes by their due dates can result in severe penalties.

The withholdings from an employee’s gross pay include:

- Employee portion of Social Security tax

- Employee portion of Medicare tax

- Federal income tax

- State income tax

- Court-ordered withholdings

- Other withholdings

1. Employee portion of Social Security tax

A key component of payroll accounting is the Social Security tax which along with the Medicare tax make up what is referred to as FICA. Social Security tax is withheld from an employee’s salary or wages and the employer is also required to pay a Social Security tax. In other words, the employer is responsible for remitting to the federal government both the employee and the employer portions of the Social Security tax.

In 2026, the amount of Social Security tax that an employer must withhold from an employee is 6.2% of the first $184,500 of the employee’s annual wages and salary; any amount above $184,500 is not subject to Social Security tax withholdings. The $184,500 is referred to as the Social Security wage base, wage limit, ceiling or maximum taxable earnings. For example:

- If an employee earns $40,000 in wages in 2026, the entire $40,000 is subject to withholdings at 6.2%, for a total annual withholding of $2,480.

- If an employee earns $200,000 in salary in 2026, only the first $184,500 of the salary is subject to the Social Security tax of 6.2%, for a total annual withholding of $11,439.00. (The amount of salary that is greater than $184,500 is not subject to Social Security tax withholdings, although it will be subject to the Medicare tax discussed in the next section.)

The amount withheld—and the employer’s portion—are reported as a current liability until the amounts are remitted to the government by the employer.

NOTE: The employee’s tax rate for Social Security and the amount subject to the tax can be found in the IRS Publication 15, Employer’s Tax Guide (PDF).

2. Employee portion of Medicare tax

Medicare tax is also withheld from an employee’s salary or wages and the employer is also required to pay a Medicare tax. In other words, similar to the Social Security tax the employer is responsible for remitting to the federal government both the employee and the employer portions of the Medicare tax. (The Medicare program helps pay for hospital care, nursing care, and doctor’s fees for people age 65 and older as well as for some individuals receiving Social Security disability benefits.)

(The combination of the Social Security tax and the Medicare tax is referred to as FICA tax, or the Federal Insurance Contribution Act tax.)

An employer must withhold 1.45% of each employee’s annual wages and salary for the Medicare tax. Unlike the Social Security tax, this percentage is applied on every employee’s total wages or salary no matter how large the amount might be. For example, an employee’s salary of $200,000 will require Medicare tax withholdings of $2,900 (the entire $200,000 times 1.45%).

Also, there is a Medicare surtax of 0.9% (which is also known as the Additional Medicare Tax) that is withheld from the employee on wages and salaries that are in excess of $200,000 in a calendar year. However, this Additional Medicare Tax is not matched by the employer. See IRS Publication 15, Employer’s Tax Guide for more information on this additional tax.

The employee’s Medicare tax and Additional Medicare Tax withholdings plus the employer’s Medicare tax are reported as a current liability until the amounts are remitted to the government by the employer.

3. Federal income tax

The amount withheld for federal income tax is based on the employee’s salary or wages as well as personal information (including whether to be taxed at the Single or Married income tax rates) that the employee is required to provide the employer on IRS Form W-4, Employees Withholding Allowance Certificate.

In cases where an employee is paid low wages, it may not be necessary for the employer to withhold any federal income tax. Unlike FICA, there is no employer contribution for federal income tax.

Amounts withheld from employees for federal income taxes are reported on the employer’s balance sheet as a current liability. When the employer remits the amounts to the federal government, the current liability is reduced.

Federal income tax withholding methods and tables are included in IRS Publication 15 and Publication 15-A.

4. State income tax

In most states payroll accounting will involve a state income tax. In those states an employer is required to withhold the state income tax that an employee is expected to owe based on salaries or wages. Like its federal counterpart, the amount withheld is rarely the exact amount of income tax that the employee will owe to the state government. (Some states do not have a personal income tax.)

The amount withheld for state income tax is based on the employee’s salary or wages as well as personal information that the employee is required to provide the employer on a state version of Form W–4.

In cases where an employee is paid low wages and/or has a large number of personal exemptions, it may not be necessary for the employer to withhold any state income tax.

Amounts withheld from employees for state income taxes are also reported on the employer’s balance sheet as a current liability. When the employer remits the amounts to the state government, the current liability is reduced.

5. Court-ordered withholdings

Payroll accounting also involves withholdings for items other than payroll taxes. For example, courts of law may order employers to garnish (withhold money from) an employee’s salary or wages for purposes such as paying child support or repaying debts.

The amounts withheld from employees for court-ordered withholdings are reported on the employer’s balance sheet as a current liability. When the employer remits the amounts to the designated parties, the liability is reduced.

Some court orders may include a small fee to be withheld from the employee in order to reimburse the employer for administrative expenses. For example, the court order might direct the employer to withhold $101 from the employee and to remit $100 to a designated agency. The $1 difference will be a credit to the company’s administrative expenses or to a miscellaneous revenue account.

6. Other withholdings

In addition to the mandatory withholdings that an employer makes for taxes and court orders, payroll accounting often includes amounts that employers may be willing to withhold at the direction of their employees. These voluntary withholdings can include such things as:

- Union dues

- Charitable donations

- Insurance premiums

- 401(k) and 403(b) contributions

- U.S. Savings bonds purchases

- Payments owed to the company for the purchase of company merchandise

If the voluntary withholdings are to be remitted to places outside of the company (a local charity, for example), the amounts withheld are reported on the employer’s balance sheet as a current liability. When the employer remits the withholdings, the current liability is reduced.

If the withholdings are for amounts that are due the company (such as employees’ share of insurance premiums or amounts owed by employees for company merchandise), no remittance is required. Rather, the journal entry reflects a credit that reduces the company’s insurance expense or reduces the company’s receivables from employees. Sample journal entries are provided later in this topic.

NOTE #1: Some payroll deductions/withholdings will reduce the employee’s taxable gross wages thereby reducing the amount of taxes withheld from the employee’s paycheck. These are referred to as pre-tax deductions.

Other payroll deductions/withholdings do not reduce the employee’s taxable wages and therefore will not reduce the amount of taxes withheld from the employee’s paycheck. These are referred to as post-tax deductions.

You should consult with your tax advisor to learn more about pre-tax and post-tax deductions.

NOTE #2: A few states require employees to contribute a minimal amount toward the state unemployment insurance. However, the employers typically contribute the entire amount.

Net Pay

Net pay is the amount that remains after withholdings are deducted from an employee’s gross pay. Net pay is also referred to as “take home pay” or the amount that an employee “clears.” From the company side of the transaction, it is the cash amount that the company will pay directly to the employees on payday. (The cash amount may be in the form of a check, a direct deposit, or other.)

Payroll Taxes, Costs, and Benefits Paid By Employers

In addition to salaries and wages, the employer will incur some or all of the following payroll-related expenses:

- Employer portion of Social Security tax

- Employer portion of Medicare tax

- State unemployment tax

- Federal unemployment tax

- Worker compensation insurance

- Employer portion of insurance (health, dental, vision, life, disability)

- Employer paid holidays, vacations, and sick days

- Employer contributions toward 401(k), savings plans, & profit-sharing plans

- Employer contributions to pension plans

- Post-retirement health insurance

1. Employer portion of Social Security tax

In addition to the amount withheld from its employees for Social Security taxes, the employer must contribute/remit an additional amount, which is an expense for the employer. In the year 2026, the employer’s portion of the Social Security tax is 6.2% of the first $184,500 of an employee’s annual wages and salary. Hence, the employer’s amount is referred to as the matching amount.

For example, if an employee earns $40,000 of wages, the entire $40,000 is subject to the Social Security tax. This means that in addition to the withholding of $2,480, the employer must also pay $2,480. The combined amount to be remitted to the federal government for this one employee is $4,960 ($2,480 of withholding plus the employer’s portion of $2,480).

For an employee with an annual salary of $200,000 in the year 2026, only the first $184,500 is subject to the Social Security tax. This means that in addition to the withholding of $11,439.00, the employer must also pay $11,439.00. The combined amount to be remitted to the federal government for this one employee is $22,878.00 ($11,439.00 + $11,439.00).

The employer’s share of Social Security taxes is recorded as an expense and as an additional current liability until the amounts are remitted.

2. Employer portion of Medicare tax

In addition to the employee’s Medicare tax there is also an employer’s Medicare tax. The employer’s Medicare tax is considered to be an expense for the employer. For the year 2026, the employer’s portion of the Medicare tax is the same rate as the employee’s withholding—1.45% of every dollar of each employee’s annual wages and salary.

Unlike the Social Security tax, the Medicare tax has no cap (ceiling or limit). For example, if an employee earns a salary of $200,000, the employer must pay a Medicare tax of $2,900 ($200,000 x 1.45%) in addition to the $2,900 that was withheld from the employee. The combined amount to be remitted to the federal government for this one employee is $5,800.

The employer’s share of Medicare taxes is recorded as an expense and as an additional current liability until the amounts are remitted.

There is a Medicare surtax known as the Additional Medicare Tax which is withheld from employee’s earnings in excess of $200,000. However, the employer does not match the Additional Medicare Tax.

3. State unemployment tax

State governments administer unemployment services (determine eligibility, remit payments to unemployed workers, etc.) and determine the state unemployment tax rate for each employer.

Generally, states require that the employers pay the entire unemployment tax rate. (Only a few states require employees to make a minimal contribution.)

The state unemployment tax rate is applied to each employee’s wages up to the state unemployment wage base, which could be $7,000 per year in one state and $30,000 in another state.

If a state has an unemployment tax rate of 4% and an unemployment wage base of $14,000, it means that the employer’s maximum payment for each employee will be $560 per year.

To illustrate, let’s assume that a company has three employees. In the year 2026, Employee #1 earns $19,000, Employee #2 earns $40,000, and Employee #3 earns $4,000. If the 2026 state unemployment tax rate is 4%, the employer will pay a tax of $1,280 to the state government:

The contact information for each state’s unemployment office is available at the following U.S. Department of Labor website: https://oui.doleta.gov/unemploy/agencies.asp

4. Federal unemployment tax

The federal government oversees the state unemployment programs and requires employers to pay a federal unemployment tax of 6.0% minus a credit if the employer has paid into a state unemployment fund and the state has met certain conditions. If an employer is allowed the maximum credit of 5.4%, then the federal unemployment tax rate will be 0.6%. This reduced rate is applied to each employee’s first $7,000 of annual salaries and wages.

Using the example of three employees with annual 2026 earnings of $19,000, $40,000, and $4,000; with a federal unemployment tax rate of 0.6%, the employer will pay a tax of $108 to the federal government:

Even though the federal unemployment tax is based on employee salaries and wages, the entire tax is paid by the employer. There is no withholding from an employee’s salary or wages for the federal unemployment tax.

The Federal Unemployment Tax Act (FUTA) requires employers to pay this tax. The employer is also required to file IRS Form 940, Employer’s Annual Federal Unemployment (FUTA) Tax Return.

Additional information on FUTA can be found in IRS Publication 15, Employer’s Tax Guide.

5. Worker compensation insurance

Worker compensation insurance (or workers’ compensation insurance, or workers’ comp) provides coverage for employees who are injured on the job. State law usually requires that employers carry this insurance. The cost of worker compensation insurance is a function of at least three variables: (1) the type of business or industry, (2) the type of job being performed, and (3) the employer’s history of claims.

For example, statistics show that a production worker in a meat packing plant has a greater-than-average chance of suffering job-related cuts or back injuries. Because of this, worker compensation insurance rates for these employees can be as high as 15% of wages. On the other hand, the office staff of the meat packing plant (provided that they do not spend time in the production area) may have a rate that is less than 1% of salaries and wages.

The worker compensation insurance rates are applied to the wages and salaries of the employees to arrive at the worker compensation insurance premiums or costs. Although the insurance premiums are based on employee salaries and wages, generally the entire amount is paid by the employer and is considered an expense for the employer. (Contact your state’s worker compensation office for the specifics in your state.)

If the employer pays the insurance premium in advance, a current asset such as Prepaid Insurance is used. The account balance will be reduced and Worker Compensation Insurance Expense will increase as the employees work.

If the employer does not pay the premiums in advance, the company must accrue the expense with an adjusting entry that increases Worker Compensation Insurance Expense along with increases in a current liability such as Worker Compensation Insurance Liability. In this situation the current liability will be reduced when the employer pays the worker compensation insurance premiums.

In some industries, worker compensation insurance is a significant expense for the employer and therefore we consider it an important part of payroll accounting.

6. Employer portion of insurance (health, dental, vision, life, disability)

In the past, many companies included group health, dental, vision, disability, and life insurance in the benefit package provided to employees. Over the past few decades, however, the costs for these group policies have risen significantly. Today the insurance premium for family coverage can be more than $10,000 per year per employee. As a result of these escalating costs, most companies now require employees to pay a portion of the premium cost; this amount is usually collected by means of employee-directed payroll withholding.

The employers’ net cost (or expense) is simply the total amount of premiums paid to the insurance company minus the portion of the cost the employer collects from its employees.

7. Employer paid holidays, vacations, and sick days

Many companies pay their permanent employees for holidays such as New Year’s Day, Memorial Day, July 4th, Labor Day, Thanksgiving, and Christmas. It is not unusual for employees to be paid for 10 holidays per year. It is also common for employees to earn one week of vacation after one year of service. Many employers give their employees two weeks of vacation after three years of service, with more weeks given after 10 years of service.

Paid sick days are also a common benefit given to employees. If an employee is absent from work due to such things as illness or surgery, the company will pay the employee for the time missed. Employers generally set policies as to how sick days are to be used, and as to whether or not an employee is permitted to carry over unused sick days into subsequent years.

The matching principle requires that the cost of compensated (or paid) absences (holidays, vacations, and sick days) be recognized as an expense during the time the employee is present and working. In other words, the cost is expensed when the benefit is being earned by the employee, not when the benefit is being used by the employee. (However, the Financial Accounting Standards Board generally allows for sick days and holidays not to be accrued.)

To illustrate, assume that an employee works full-time for the entire year 2025 and as a result earns one week of vacation to be taken anytime during the year 2026. In the weeks/months of the year 2025 (when the employee is working), the employer debits Vacation Expense and credits Vacation Liability. In 2026, when the employee takes the vacation earned in the previous year, the employer records the gross amount of the vacation check with a debit to Vacation Liability (instead of Vacation Expense or Wages Expense).

8. Employer contributions toward 401(k), savings plans, and profit-sharing plans

If an employer is required to contribute company money into an employee’s savings program or profit-sharing plan, the contribution should appear as an expense in the period when the employee earned the company contribution. It is also likely that the company will have the expense and the liability before the company actually pays the amount. This situation requires the company to record an adjusting entry in order to match the expense to the proper accounting period.

9. Employer contributions to pension plans

Some companies provide pensions for their employees. This means their employees will receive ongoing monthly payments after they retire from the company. The matching principle requires that the cost of the benefit should be recognized during the years that the employees are working (earning the benefit), and not when the employee is retired.

Note: In effect, pensions (and other benefits) are part of the compensation package given to employees working at a company. While some parts of the compensation package are paid out during the time the employee is working, other benefits are deferred until the employee is retired. The cost of the entire compensation package, however, must be expensed or assigned to products manufactured when the employee is working, so that the cost of the employee’s work is matched with the revenue resulting from the employee’s work.

The concept is that in the years that the employee works, the company will charge Pension Expense and will credit either Pension Payable or Cash. For more specifics on pensions, you are referred to an Intermediate Accounting text or to the Financial Accounting Standards Board’s website.

10. Post-retirement health insurance

Some companies continue to provide health insurance coverage to employees after they have retired. This retiree benefit is considered to be part of the compensation package earned by employees while they are working. Again, accrual accounting and the matching principle require that the cost of this future insurance coverage be expensed (or assigned to manufactured products) during the years the employees are working by debiting an expense and crediting a liability. During the employees’ retirement years, the company’s payment for insurance will reduce the company’s liability and will reduce its cash.

To learn more on the accounting for post-retirement benefits, such as health insurance coverage, you are referred to an Intermediate Accounting text and/or to the Financial Accounting Standards Board’s website.

Depositing Federal Payroll Taxes

The employer is required to deposit the federal payroll taxes (amounts withheld from employees and the employer’s matching amount) to the U.S. Treasury by means of an electronic funds transfer (EFT). Generally, this is done using EFTPS which is a free service of the U.S. Treasury.

The federal payroll taxes must be sent via an electronic funds transfer by the dates described in IRS Publication 15. The dates depend upon the current amount of the federal payroll taxes and also the employer’s amount during a previous one-year period. Here is part of the criteria regarding the current amount of federal payroll taxes:

- If the amount is $100,000 on any day, the money must be transferred within one day.

- If the amount is more than $50,000 but less than $100,000, the money must be transferred semiweekly (twice a week). For example, if the payday is on Wednesday, Thursday, and/or Friday, the payroll taxes must be deposited by the following Wednesday. If the payday is on Saturday, Sunday, Monday, and/or Tuesday the payroll taxes must be deposited by the following Friday.

- If the amount is $50,000 or less, the money must be transferred monthly. However, if the amount is less than $2,500 for the quarter, under certain circumstances you may be able to pay with a timely filed quarterly Form 941. See IRS Publication 15 for more information.

Failure to deposit the amount owed on the required date may result in severe penalties.

IRS Form 941, Employer’s Quarterly Federal Tax Return

IRS Form 941, Employer’s Quarterly Federal Tax Return is filed quarterly by companies who have employees. On Form 941 the employer reports the amounts for the following items:

- Wages, salaries, etc. paid to employees

- Tips the employees reported

- Federal income taxes withheld from employees

- Social Security and Medicare taxes (both employee withholdings and employer’s share)

- Qualified small business payroll tax credit for increasing research

- Adjustments

Small employers could be granted permission to file the annual Form 944 but must have received notification from the IRS.

Form 941 is due by the last day of the month following the calendar quarter. In other words, Form 941 covering the months of January, February, and March must be filed by April 30. The second quarter report must be filed by July 31, and so on. There are significant penalties for not filing these required quarterly reports by their due dates.

The federal income taxes withheld from employees plus the employees’ and employer’s Social Security and Medicare taxes must be deposited electronically according to due dates discussed in the previous section entitled “Depositing Federal Payroll Taxes”.

The IRS has Form 941 with instructions (and all other IRS forms) in PDF format available on the IRS website.

Outsourcing Payroll Processing

Many companies choose to outsource the processing of payroll to large payroll processing firms (ADP, Paychex, and others), banks, accounting firms, etc.

The services of payroll processors can vary and the company using the service may be able to select the features it will use. Some of the common features include:

- Preparing the employee paychecks or processing direct deposits based on data (hours worked, etc.) furnished by the company

- Preparing the payroll summaries (by department, total company)

- Preparing and filing tax reports

- Preparing IRS Form W-2 for each employee and transmitting them to government agencies

- Remitting payroll taxes to government agencies

To learn more about outsourcing payroll processing including risks and responsibilities see “Third-Party Payer Arrangements” found in IRS Publication 15, Employer’s Tax Guide.

Examples of Payroll Journal Entries For Wages

NOTE: In the following examples we assume that the employee’s tax rate for Social Security is 6.2% and that the employer’s tax rate is 6.2%.

In this section of payroll accounting we will provide examples of the journal entries for recording the gross amount of wages, payroll withholdings, and employer costs related to payroll.

Let’s assume that a distributor has hourly-paid employees working in two departments: delivery and warehouse. The company’s workweek is Sunday through Saturday and paychecks are dated and distributed on the Thursday following the workweek.

For the workweek of December 18–24, the gross wages are $1,000 for hourly employees in the delivery department and $1,300 for employees in the warehouse. Tax withholdings are hypothetical amounts from federal and state tax withholding tables. Other withholdings are based on agreements with employees and court orders. Paychecks are dated and distributed on December 29.

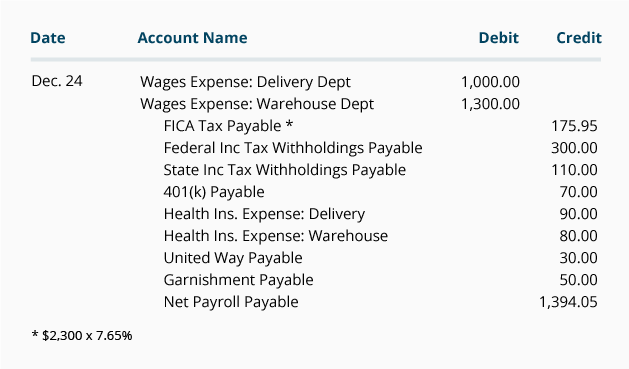

The journal entry to record the hourly payroll’s wages and withholdings for the work period of December 18–24 is illustrated in Hourly Payroll Entry #1. In accordance with accrual accounting and the matching principle, the date used to record the hourly payroll is the last day of the work period.

Hourly Payroll Entry #1: To record hourly-paid employees wages and withholdings for the workweek of December 18–24 that will be paid on December 29.

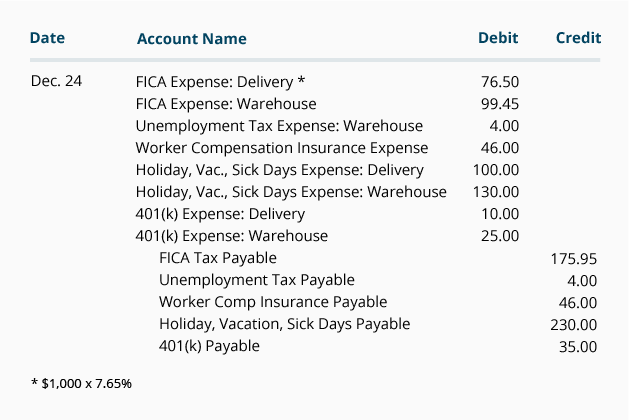

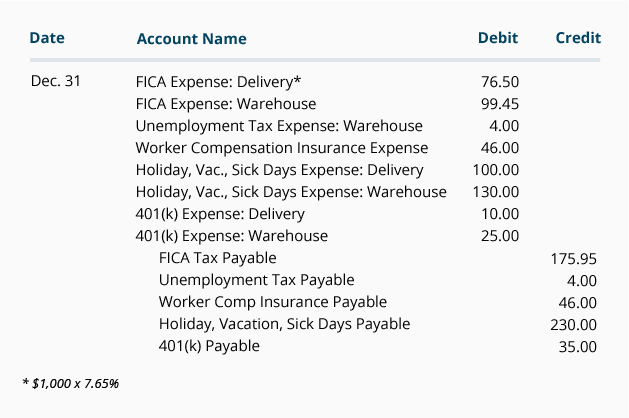

In addition to the wages and withholdings in the above entry, the employer has incurred additional expenses that pertain to the above workweek. These are shown next in Hourly Payroll Entry #2, which is also dated the last day of the work period. The items included are the employer’s share of FICA, the employer’s estimated cost for unemployment tax, worker compensation insurance, compensated absences, and company contributions for the company’s 401(k) plan. The company is recognizing these additional expenses and the related liability in the period in which the employees are working and earning them. Later, when the company pays for them, it will reduce the liability and reduce its cash. (Our journal entry assumes that this company does not provide post-retirement benefits such as pensions or health insurance for its employees.)

Hourly Payroll Entry #2: To record the company’s additional payroll-related expenses for hourly-paid employees for the workweek of December 18–24.

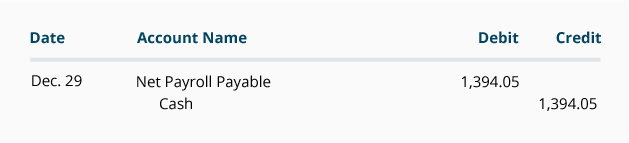

On payday, December 29, the checks will be distributed to the hourly-paid employees. The following entry will record the issuance of those payroll checks.

Hourly Payroll Entry #3: To record the distribution of the hourly-paid employees’ payroll checks on Dec. 29. (These checks reflect the net pay for the wages earned during the workweek of Dec. 18–24).

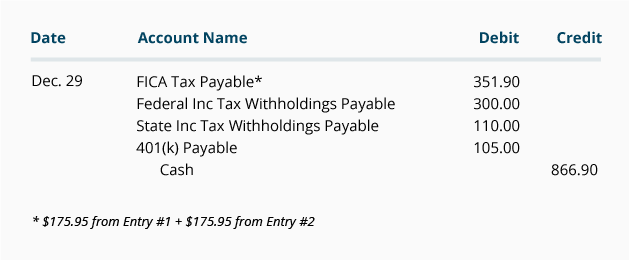

Some withholdings and the employer’s portion of FICA were remitted on payday; others are not due until a later date. Some withholdings, such as health insurance, were recorded as reductions of the company’s expenses in Hourly Payroll Entry #1. We will assume the amounts in the following Hourly Payroll Entry #4 were remitted on payday.

Hourly Payroll Entry #4: To record the remittance of some of the payroll withholdings and company matching that pertain to the hourly-paid workweek of Dec. 18–24.

End of Month and End of Year

Let’s continue with our example of the payroll for the hourly-paid employees. We’ll assume that the distributor’s accounting month and accounting year both end on Saturday, December 31. The matching principle requires the company to report all of its December expenses (not simply its cash payments) on its December financial statements. This means the company must report on its income statement the hourly wages and other payroll expenses that the company incurred (and the employees earned) through December 31.

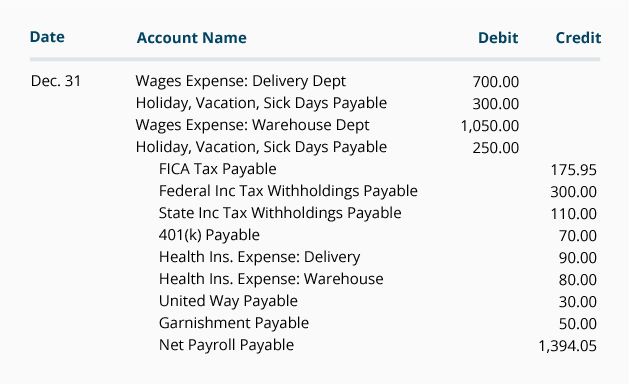

Recall that the paychecks issued on December 29 covered the work done by hourly employees only through December 24. On December 31, the company must record the cost of work done during the week of December 25–31. In addition, the employees’ holiday and vacation days must be recorded.

Let’s assume that during the workweek of December 25–31, some of the hourly-paid employees in the Delivery Department were paid for a holiday and a few vacation days. Let’s assume that this paid time off amounted to $300 and the pay for the hours worked during the workweek was $700. Recall that each workweek’s payroll entries had been anticipating the paid time off with a $100 debit to Holiday, Vacation, Sick Days Expense: Delivery Dept., and a $100 credit to Holiday, Vacation, Sick Days Payable. Now that vacation time off is being taken, the current workweek’s payroll entry will reduce the company’s liability with a debit to Holiday, Vacation, Sick Days Payable for $300. The $700 of pay for the hours worked is debited to Wages Expense: Delivery Dept.

Let’s also assume that the Warehouse Department’s hourly-paid employees had been paid for their time off for the holiday and some vacation time. Let’s assume that the paid time off amounts to $250, and the amount associated with the hours worked was $1,050. Since the paid time off had been accrued each workweek, the current workweek’s entry reduces the company’s liability with a debit to Holiday, Vacation, Sick Days Payable for $250. The $1,050 of pay for the hours worked is debited to Wages Expense: Warehouse Dept.

Hourly Payroll Entry #1: To record hourly-paid employees’ wages and withholdings for the workweek of December 25–31 that will be paid on January 5.

In addition to the wages and withholdings in Hourly Payroll Entry #1, the employer has incurred additional expenses that pertain to the above workweek. These are shown next in Hourly Payroll Entry #2, which is also dated the last day of the work period. The items included are the employer’s share of FICA, the employer’s estimated cost for unemployment tax, worker compensation insurance, compensated absences, and company contributions for the company’s 401(k) plan. The company is recognizing these additional expenses and the related liability in the period in which the employees are working and earning them. Later, when the company pays for them, it will reduce the liability and reduce its cash. (Our journal entry assumes that this company does not provide post-retirement benefits such as pensions or health insurance to its employees.)

Hourly Payroll Entry #2: To record the company’s additional payroll-related expenses for hourly-paid employees for the workweek of December 25–31.

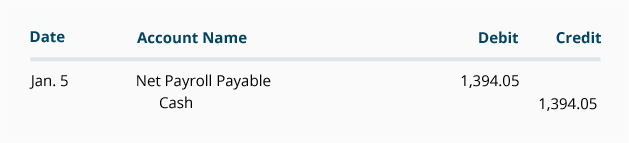

On payday, January 5, the checks will be distributed to the hourly-paid employees. The following entry will record the issuance of those payroll checks.

Hourly Payroll Entry #3: To record the distribution of the hourly-paid employees’ payroll checks on Jan 5. (These checks reflect the hourly-paid employees’ take home pay from their wages earned during the workweek of Dec. 25–31).

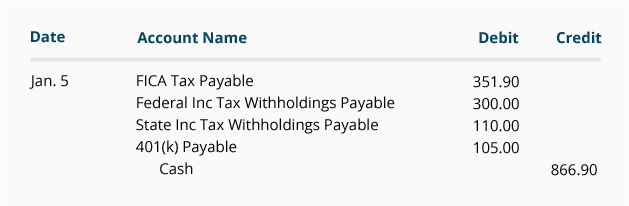

Some withholdings and the employer’s portion of FICA were remitted on payday; others are not due until a later date. Some withholdings, such as health insurance, were recorded as reductions of the company’s expenses in Hourly Payroll Entry #1. We will assume the amounts in the following Payroll Entry #4 were remitted on payday.

Hourly Payroll Entry #4: To record the remittance of some of the payroll withholdings and company matching that pertain to the hourly-paid workweek of Dec. 25–31.

Additional Accrual of Wages

In our example above, the workweek ended on the same day as the calendar month and year (December 31). In other months and in some years, the last full workweek might end on the 28th of the month. In that case, the employer will need to estimate the payroll and payroll-related expenses for the 29th, 30th, and 31st days of the month. Those estimates will be used to record an accrual-type adjusting entry on the 31st. This is required so that all of the expenses actually occurring during the month are matched with the revenues of the month. Recording wages expense in the proper period is critical for accurate financial statements and therefore a very important part of payroll accounting.

Examples of Payroll Journal Entries For Salaries

NOTE: In the following examples we assume that the employee’s tax rate for Social Security is 6.2% and that the employer’s tax rate is 6.2%.

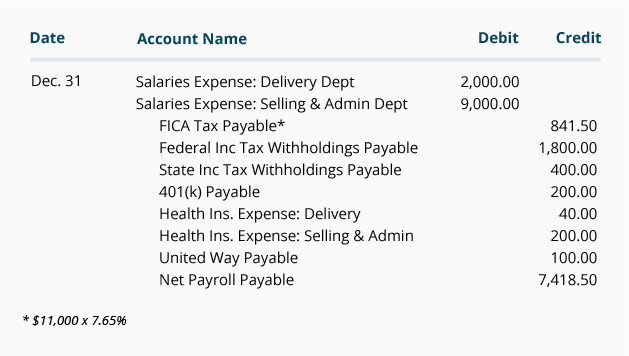

Let’s assume our company also has salaried employees who are paid semimonthly on the 15th and the last day of each month. The pay period for these employees is the half-month that ends on payday. There is one salaried employee in the warehouse department with a gross salary of $48,000 per year, or $2,000 per pay period. There are four salaried employees in the Selling & Administrative Department with combined salaries of $9,000 per pay period.

Because the salaried employees are paid on the last day of the month and their pay period ends on payday, there is no need to accrue for salaries at the end of December (or any other calendar month). The salaried payroll entry for the work period of December 16–31 will be dated December 31 and will look like this:

Salaried Payroll Entry #1: To record the salaries and withholdings for the work period of December 16–31 that will be paid on December 31.

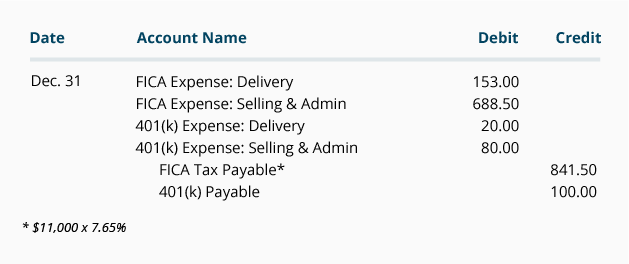

In addition to the salaries recorded above, the company has incurred additional expenses pertaining to the salaried payroll for this semi-monthly period of December 16–31. These expenses must be included in the December financial statements, as shown in the next journal entry:

Salaried Payroll Entry #2: To record additional payroll-related expenses for salaried employees for the work period of December 16–31.

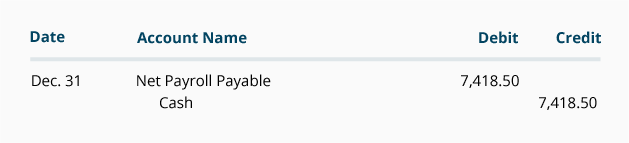

On payday, December 31, the checks will be distributed to the salaried employees. The following entry will record the issuance of those payroll checks.

Salaried Payroll Entry #3: To record the distribution of the salaried employees’ payroll checks on Dec. 31. (These checks reflect the take-home pay for the salaries earned during the work period of Dec. 16–31).

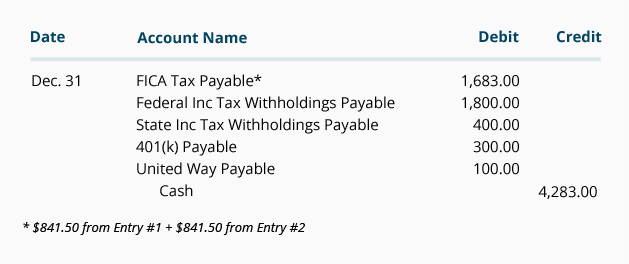

Some withholdings and the employer portion of FICA were remitted on payday; others are not due until a later date. Some withholdings, such as health insurance, were recorded as reductions of the company’s expenses in Salaried Payroll Entry #1. We will assume the amounts in the following Payroll Entry #4 were remitted on payday.

Salaried Payroll Entry #4: To record the remittance of some of the payroll withholdings and company matching that pertain to the salaried employees during the work period of Dec. 15–31.

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Payroll Accounting materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.

Earn Our Certificate

for This Topic

When you join PRO, you will receive instant access to 16 different Certificates of Achievement plus our Bookkeeping Certificate of Excellence.

View PRO Features