For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.

A person starting a new business often asks, “At what level of sales will my company make a profit?” Established companies that have suffered through some rough years might have a similar question. Others ask, “At what point will I be able to draw a fair salary from my company?” Our discussion of break-even point and break-even analysis will provide a thought process that may help to answer those questions and to provide some insight as to how profits change as sales increase or decrease.

Frankly, predicting a precise amount of sales or profits is nearly impossible due to a company’s many products (with varying degrees of profitability), the company’s many customers (with varying demands for service), and the interaction between price, promotion and the number of units sold. These and other factors will complicate the break-even analysis.

In spite of these real-world complexities, we will present a simple model or technique referred to by various names, including:

break-even point

break-even analysis

break-even formula

break-even model

cost-volume-profit (CVP) analysis

expense-volume-profit (EVP) analysis

The latter two names are appealing because the break-even technique can be adapted to determine the sales needed to attain a specified amount of profits. However, we will use the terms break-even point and break-even analysis.

To assist with our explanations, we will use a fictional company Oil Change Co. (a company that provides oil changes for automobiles). The amounts and assumptions used in Oil Change Co. are also fictional.

WATCH NOWDiscover Our PRO TrainingChoose your personalized video for...

Please let us know how we can improve this explanation

No Thanks

Close

Expense Behavior

At the heart of break-even point or break-even analysis is the relationship between expenses and revenues. It is critical to know how expenses will change as sales increase or decrease. Some expenses will increase as sales increase, whereas some expenses will not change as sales increase or decrease.

Variable Expenses

Variable expenses increase when sales increase. They also decrease when sales decrease.

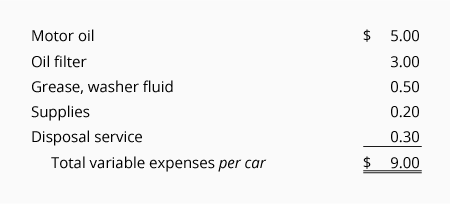

At Oil Change Co. the following items have been identified as variable expenses. Next to each item is the variable expense per car (per oil change):

The other expenses at Oil Change Co. (rent, heat, etc.) will not increase when an additional car is serviced.

For the reasons shown in the above list, Oil Change Co.’s variable expenses will be $9 if it services one car, $18 if it services two cars, $90 if it services 10 cars, $900 if it services 100 cars, etc.

Fixed Expenses

Fixed expenses do not increase when sales increase. Fixed expenses do not decrease when sales decrease. In other words, fixed expenses such as rent will not change when sales increase or decrease.

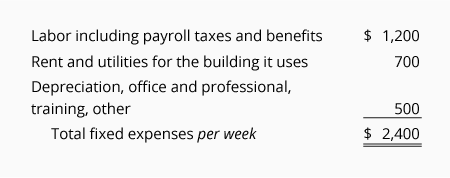

At Oil Change Co. the following items have been identified as fixed expenses. The amount shown is the fixed expense per week:

Mixed Expenses

Some expenses are part variable and part fixed. These are often referred to as mixed expenses or semi-variable expenses. An example would be a salesperson’s compensation that is composed of a salary portion (fixed expense) and a commission portion (variable expense). Mixed expenses could be split into two parts. The variable portion can be listed with other variable expenses and the fixed portion can be included with the other fixed expenses.

Please let us know how we can improve this explanation

No Thanks

Close

Revenues or Sales

Revenues (or sales) at Oil Change Co. are the amounts earned from servicing cars. Oil Change Co. charges one flat fee of $24 for performing the oil change service. For $24 the company changes the oil and filter, adds needed fluids, adds air to the tires, and inspects engine belts.

At the present time no other service is provided and the $24 fee is the same for all automobiles regardless of engine size.

As the result of its pricing, if Oil Change Co. services 10 cars its revenues (or sales) are $240. If it services 100 cars, its revenues will be $2,400.

Please let us know how we can improve this explanation

No Thanks

Close

Contribution Margin

An important term used with break-even point or break-even analysis is contribution margin. In equation format it is defined as follows:

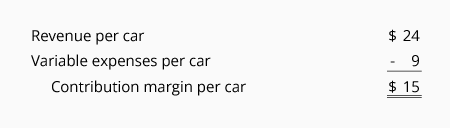

The contribution margin for one unit of product or one unit of service is defined as:

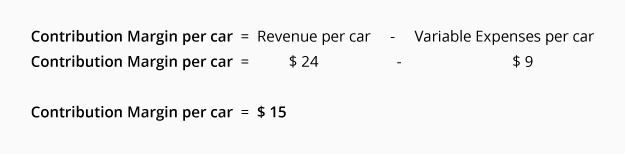

At Oil Change Co. the contribution margin per car (or per oil change) is computed as follows:

The contribution margin per car lets you know that after the variable expenses are covered, each car serviced will provide or contribute $15 toward the Oil Change Co.’s fixed expenses of $2,400 per week. After the $2,400 of weekly fixed expenses has been covered the company’s profit will increase by $15 per car serviced.

Please let us know how we can improve this explanation

No Thanks

Close

Break-even Point In Units

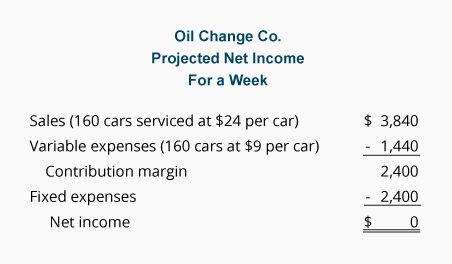

The break-even point in units for Oil Change Co. is the number of cars it needs to service in order to cover the company’s fixed and variable expenses. The break-even point formula is to divide the total amount of fixed costs by the contribution margin per car:

It’s always a good idea to check your calculations. The following schedule confirms that the break-even point is 160 cars per week:

Please let us know how we can improve this explanation

No Thanks

Close

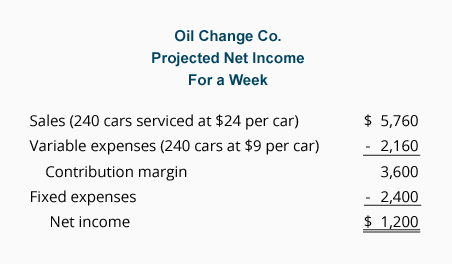

Desired Profit In Units

Let’s say that the owner of Oil Change Co. needs to earn a profit of $1,200 per week rather than merely breaking even. You can consider the owner’s required profit of $1,200 per week as another fixed expense. In other words, the fixed expenses will now be $3,600 per week (the $2,400 listed earlier plus the required $1,200 for the owner). The new point needed to earn $1,200 per week is shown by the following break-even formula:

Always check your calculations:

The above schedule confirms that servicing 240 cars during a week will result in the required $1,200 profit for the week.

Please let us know how we can improve this explanation

No Thanks

Close

Break-even Point In Sales Dollars

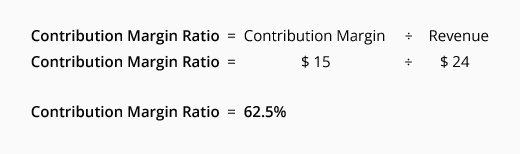

One can determine the break-even point in sales dollars (instead of units) by dividing the company’s total fixed expenses by the contribution margin ratio.

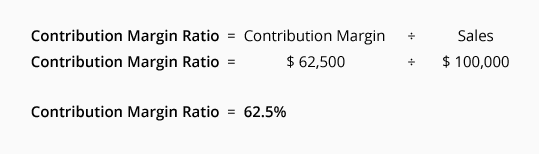

The contribution margin ratio is the contribution margin divided by sales (revenues). The ratio can be calculated using company totals or per unit amounts. We will compute the contribution margin ratio for the Oil Change Co. by using its per unit amounts:

The break-even point in sales dollars for Oil Change Co. is:

The break-even point of $3,840 of sales per week can be verified by referring back to the break-even point in units. Recall there were 160 units necessary to break-even. With revenues of $24 per unit, the necessary sales in dollars would be $3,840 (160 units x $24).

Please let us know how we can improve this explanation

No Thanks

Close

Desired Profit In Sales Dollars

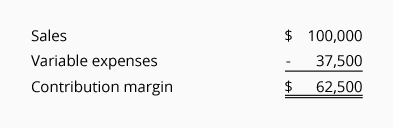

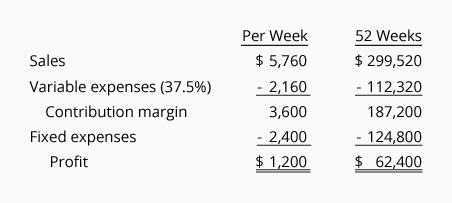

Let’s assume a company needs to cover $2,400 of fixed expenses each week plus earn $1,200 of profit each week. In essence the company needs to cover the equivalent of $3,600 of fixed expenses each week.

Presently the company has annual sales of $100,000 and its variable expenses amount to $37,500 per year. These two facts result in a contribution margin ratio of 62.5%:

The amount of sales necessary to give the owner a profit of $1,200 per week is determined by this break-even point formula:

To verify that this answer is reasonable, we prepared the following schedule:

As you can see, for the owner to have a profit of $1,200 per week or $62,400 per year, the company’s annual sales must triple. Presently the annual sales are $100,000 but the sales need to be $299,520 per year in order for the annual profit to be $62,400.

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Break-even Point materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.

Please let us know how we can improve this explanation

No Thanks

Close

A revenue account that reports the sales of merchandise. Sales are reported in the accounting period in which title to the merchandise was transferred from the seller to the buyer.

Fees earned from providing services and the amounts of merchandise sold. Under the accrual basis of accounting, revenues are recorded at the time of delivering the service or the merchandise, even if cash is not received at the time of delivery. Often the term income is used instead of revenues.

Examples of revenue accounts include: Sales, Service Revenues, Fees Earned, Interest Revenue, Interest Income. Revenue accounts are credited when services are performed/billed and therefore will usually have credit balances. At the time that a revenue account is credited, the account debited might be Cash, Accounts Receivable, or Unearned Revenue depending if cash was received at the time of the service, if the customer was billed at the time of the service and will pay later, or if the customer had paid in advance of the service being performed.

If the revenues earned are a main activity of the business, they are considered to be operating revenues. If the revenues come from a secondary activity, they are considered to be nonoperating revenues. For example, interest earned by a manufacturer on its investments is a nonoperating revenue. Interest earned by a bank is considered to be part of operating revenues.

An expense is variable when its total amount changes in proportion to the change in sales, production, or some other activity. In other words, a variable expense increases when an activity increases, and it decreases when the activity decreases.

Fixed expenses do not change in total when there are normal changes in sales or other activity.

Contribution margin is the amount remaining after all variable expenses are subtracted from revenues. It indicates the amount available from sales to cover the fixed expenses and profit.

Fixed costs are costs and expenses which do not change in response to reasonable changes in sales or another activity.

This ratio indicates the percentage of each sales dollar that is available to cover a company’s fixed expenses and profit. The ratio is calculated by dividing the contribution margin (sales minus all variable expenses) by sales.

For the past 52 years, Harold Averkamp (CPA, MBA) has

worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.