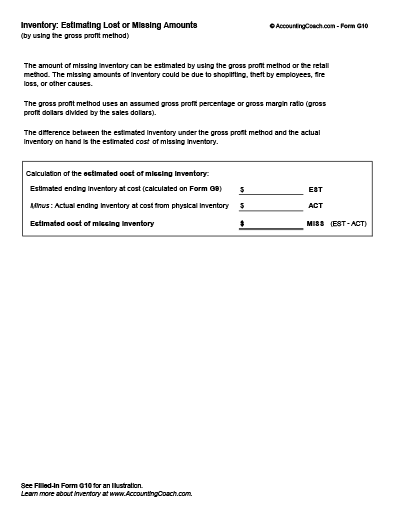

Form Description

This form, along with the form Inventory: Estimating Using the Gross Profit Method, helps you determine the approximate cost of inventory that is missing. This is done by comparing two amounts: 1) the estimated cost of inventory that is expected to be on hand, compared to 2) the cost of the actual inventory that is on hand.