March Transactions and Financial Statements

On March 8 Good Deal receives $800 for the calculators sold to the school on February 28. No other transactions occurred in March. (Note that this $800 is a March receipt but is not revenue in March. The revenue was earned and was reported on February’s income statement.)

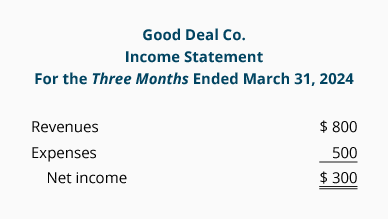

The income statement for the one month ending on March 31 is shown here:

The income statement for the three months of January 1 through March 31 is:

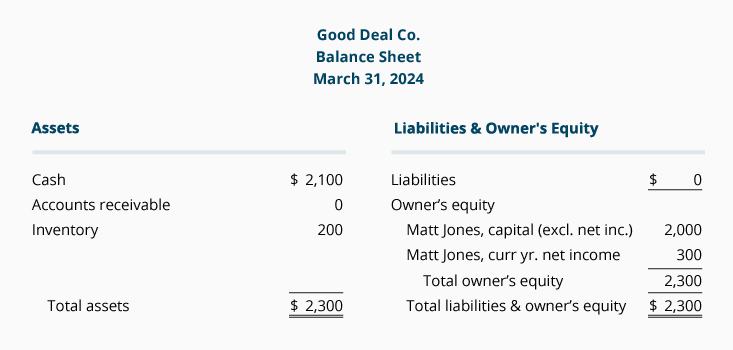

Note that the 3-month year-to-date net income of $300 causes the amount in the owner’s capital account (on the following balance sheet) to increase from $2,000 to $2,300. The receipt of $800 caused the cash to increase from $1,300 to $2,100 and accounts receivable to decrease to zero.

The SCF for the period of January 1 through March 31 is shown here:

The statement of cash flows (SCF) for the first three months of the business (January 1 through March 31) begins with the company’s accrual accounting net income of $300. This amount must be adjusted to show the net cash from operating activities (which are the company’s activities pertaining to the purchasing/producing of goods and selling of goods and/or providing services).

For the 3-month period of the SCF the company’s inventory increased from $0 to $200 at March 31. Therefore, we know that $200 of the company’s cash was used to increase its inventory. Recall that the use of cash, cash outflows, and money spent have a negative effect on the company’s cash balance and are reported as a negative amount on the SCF. Therefore, the $200 increase in inventory must be shown as (200). [If the inventory had decreased, the amount would have been a positive 200, since selling items from inventory is positive/good for the company’s cash balance.]

Since the amount of the company’s accounts receivable was $0 at January 1, and $0 at March 31, there is no adjustment and this line could have been omitted.

The combination of the positive net income of $300 and the adjustment for the cash used to increase inventory (200) results in the net cash provided by operating activities of a positive $100.

The owner’s $2,000 investment in January was a source of cash (hence it was a cash inflow, was good for the company’s cash balance, etc.) and is listed as a positive 2,000 in the section described as financing activities.

Finally, the combination of the amounts from the three sections of the SCF is $2,100. This agrees with the change in the amount of cash on the company’s balance sheets: $0 on January 1, and $2,100 on March 31.

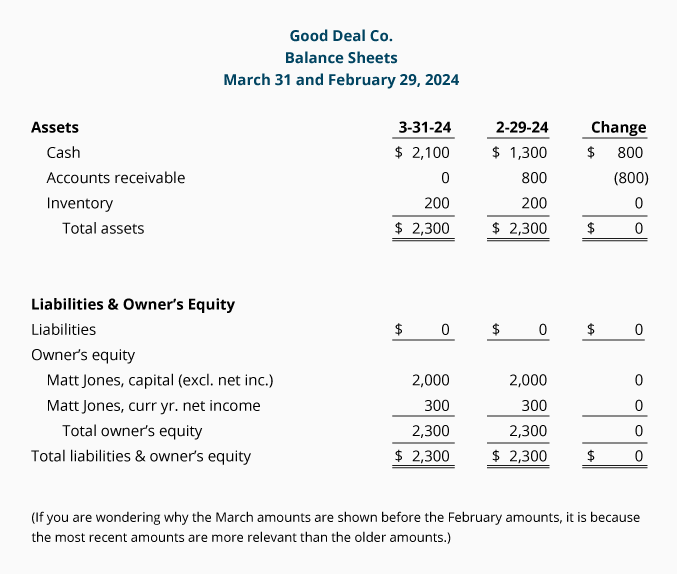

Next, we will prepare a SCF for the month of March. To do this we will compare the company’s balance sheet of March 31 with its balance sheet of February 28:

Look at the “Change” column above. The first amount, a positive $800 change in the Cash account, will serve as a “check figure” for the line Net increase in cash on the cash flow statement for the month of March. In other words, the cash flow statement for March must end up explaining the $800 increase in the Cash reported on the balance sheet. The other balance sheet amounts that changed will be used on the statement of cash flows to identify the reasons for the $800 increase in cash.

Since there were no revenues and no expenses in March, the income statement for the one month of March (shown earlier) reported no net income. This $0 of net income will be shown as the first amount reported on the statement of cash flows. The changes in the balance sheet accounts from February 28 to March 31 provided the other information needed for the following SCF for the month of March:

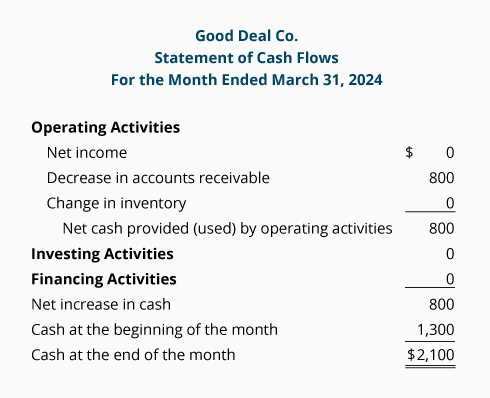

Let’s review the cash flow statement for the month of March 2023:

-

Net income for March is $0, since there were no revenues, gains, expenses, or losses.

-

Cash increased by $800 because $800 of accounts receivable were collected during March.

-

Inventory did not change, so Cash was not affected. (We could omit this line since it had no effect on cash.)

-

There were no changes in long-term assets during March, so nothing is reported in the investing activities section.

-

There were no changes in short-term loans payable, long-term liabilities, or owner’s equity. Therefore, nothing is reported in the financing activities section.

-

The sum of the amounts on the statement of cash flows is a positive $800. This amount agrees to the increase in the cash balance from $1,300 on February 28 to $2,100 on March 31.

Please let us know how we can improve this explanation

No Thanks