A Story To Illustrate How Specific Transactions and Account Balances Affect the Cash Flow Statement

The remainder of our SCF explanation illustrates how specific transactions and account balances affect a company’s cash flow statement (as well as its income statement and balance sheet).

We will use an easy-to-follow story with only one transaction per day to help you better understand the cash flow statement. You will also see how the financial statements are connected.

Matt is a college student who enjoys buying and selling merchandise using the Internet. On January 2, 2023, he decided to turn his hobby into a business called “Good Deal Co.” Each month the Good Deal Co. had one or two transactions. Matt wants to prepare an income statement, balance sheet, and a statement of cash flows for the current month and for the year-to-date period. He asks our help in preparing and understanding the SCF.

Please let us know how we can improve this explanation

No ThanksJanuary Transactions and Financial Statements

On January 2, 2023 Matt invested $2,000 of his personal money into his sole proprietorship, Good Deal Co. On January 20, Good Deal buys 14 graphing calculators at a cost of $50 per calculator (which was about 50% of the selling price Matt has observed at the retail stores). The total cost to Good Deal for all 14 calculators was $700. Good Deal had no other transactions during January.

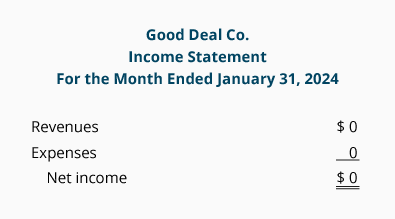

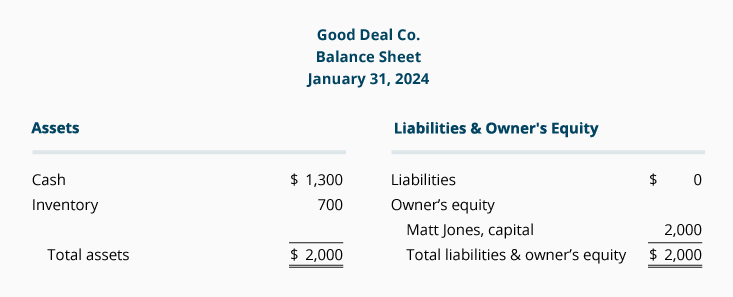

Matt prepared the income statement and balance sheet for his new business as of January 31, 2023 as shown below:

Note that the $50 cost of each calculator is not reported on the income statement as an expense until a sale occurs. (This is part of the accrual basis of accounting and the related matching principle.)

The cost of each unsold calculator will be reported as the asset inventory on the company’s balance sheet. Therefore, the 14 calculators purchased at $50 each will appear as $700 of inventory. The company’s balance sheet will report the remaining cash balance of $1,300 ($2,000 – $700).

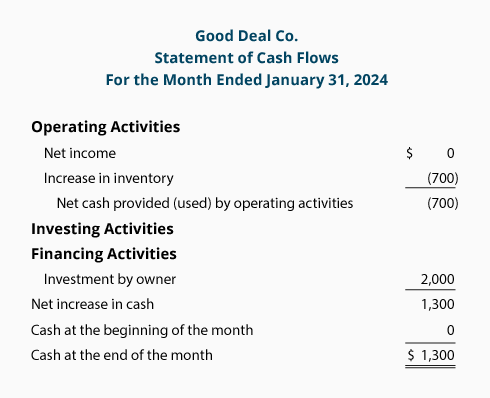

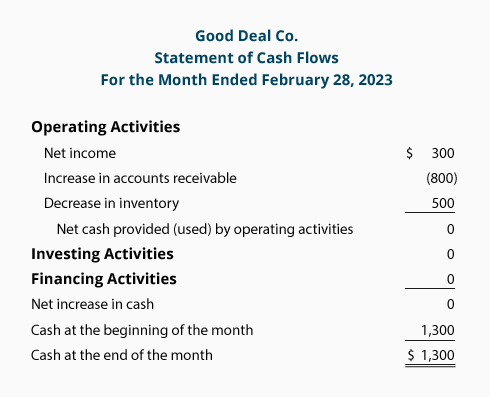

From the information on the company’s income statement and balance sheet, we prepared the statement of cash flows for the month of January:

Under the indirect method, the operating activities section of the statement of cash flows (SCF) begins with the company’s net income. Note that Good Deal Co.’s January net income of $0 appears as the first item in the operating activities section of the SCF. Since the net income was determined through the accrual basis of accounting, we will list the adjustments needed to convert the amount of net income to the net cash provided (used) by operating activities.

Amounts in parentheses indicate a negative effect on the company’s cash balance. An amount in parentheses can also be viewed as a cash outflow or cash used.

Amounts without parentheses indicate a positive effect on the company’s cash balance. An amount without parentheses can also be viewed as a cash inflow or cash provided.

For example, from Good Deal Co.’s balance sheet we know its inventory increased from $0 at January 1 to $700 at January 31. Increasing inventory by $700 during January was not good for the company’s cash balance since the company paid out $700. Therefore, under Operating Activities on Good Deal Co.’s SCF the Increase in inventory appears as (700) since it had an unfavorable or negative effect on the company’s cash balance.

If the inventory had decreased by $700, the adjustment would have been a positive 700. The reason is that by decreasing its inventory the company avoided purchasing $700 of the cost of goods sold that reduced net income. Not having to pay $700 of the cost of goods sold was good/positive for the company’s cash balance.

The financing activities section shows Investment by owner 2,000 which had a positive effect of $2,000 on the company’s cash. This amount could be discovered by examining the change in the owner’s capital account between the two balance sheet dates. Again, you can view the positive $2,000 as cash that flowed in or was good for the company’s cash balance.

The combination of the $700 cash outflow from operating activities and the $2,000 cash inflow from financing activities is shown as Net increase in cash. The net increase of $1,300 agrees with the change in the cash balances reported on the balance sheet: At January 1, the cash balance was $0; and at January 31, the cash balance was $1,300.

Here’s a Tip

For a change in assets (other than cash), the change in Cash is in the opposite direction. Recall that when Inventory increased by $700, Cash decreased by $700.

For a change in liabilities and owner’s equity, the change in Cash is in the same direction. Recall that when the owner invested cash in the company, Owner’s Equity increased and Cash increased.

Please let us know how we can improve this explanation

No ThanksFebruary Transactions and Financial Statements

On February 28, 2023, Good Deal sold 10 calculators to a nearby high school for $80 each. Matt delivered the calculators on February 28 and gave the school an $800 invoice due by March 10. Matt received $800 from the school on March 8.

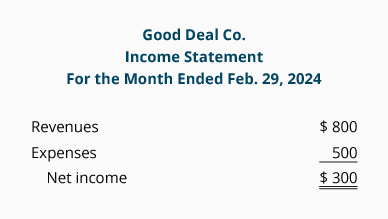

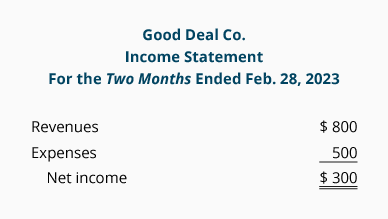

Matt prepared the following income statement for the month of February:

Under the accrual basis of accounting, revenues (such as sales of products) are reported on the income statement in the period in which a sale occurs. Typically, the sale occurs when the products or goods are shipped or delivered to the buyer (or services are provided). As the February 28 transaction shows, revenues can occur before cash is received. Since Good Deal Co. delivered 10 calculators at a selling price of $80 each to a reputable buyer, it had earned revenues of $800 on February 28.

Under the accrual basis of accounting, expenses should be matched with revenues when there is a cause and effect relationship. This means that a retailer should match its sales with the related cost of goods sold. In the case of Good Deal Co., it needs to match the cost of the 10 calculators sold with the revenues from selling 10 calculators. Therefore, its February income statement shows expenses of $500 (10 X $50) being subtracted from its revenues of $800.

Other expenses such as selling, general, administrative, and interest expenses must also be reported on the income statement when 1) they can be matched with the revenues, or 2) when a cost has expired, has been used up, or has no future value. If Good Deal Co. was renting a storage space for $50 per month, each month’s income statement would also list rent expense of $50.

In summary, Good Deal Co. correctly reported $800 of revenues, $500 of expenses, and $300 of net income even though no cash flowed in or out during February.

The statement of cash flows (SCF) for the month of February begins with the accrual accounting net income of $300, which must be converted/adjusted to the net cash from operating activities. Recall that the income statement reported revenues of $800, and the balance sheets from January 31 and February 28 will indicate that accounts receivable increased from $0 to $800. This increase in accounts receivable of $800 indicates that the company did not collect $800 of the revenues that were reported on February’s income statement. Allowing accounts receivable to increase is not good for the company’s cash balance. When something is not good for the company’s cash balance, the amount is shown in parentheses. Again, the (800) indicates the negative effect on the company’s cash caused by the company not yet collecting the cash from its credit sales, reported on its income statement.

When a company’s inventory decreases, it is good/positive for a company’s cash. The reason is the company is not paying out cash for the items it is removing from inventory. While Good Deal Co.’s income statement for the month of February reported “Expenses 500” for the cost of its goods sold, the company did not pay out the $500 during February. Therefore, the company shows a positive $500 on its SCF as an adjustment to the net income amount. The $500 adjustment is not reporting what happened to the amount of inventory, it is reporting the necessary adjustment to convert the accrual accounting net income to the cash amount.

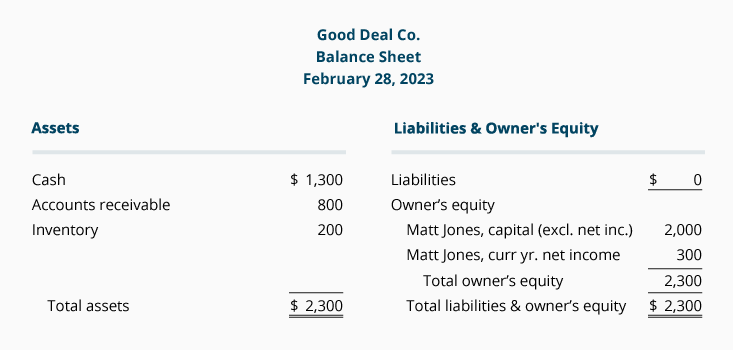

Now let’s look at the year-to-date financial statements covering the two-month period of January 1 through February 28:

The year-to-date net income of $300 increases the owner’s equity on the balance sheet. Note the connection between the bottom line of the year-to-date income statement and the change in Matt Jones, Capital on the balance sheet. Matt Jones, Capital has increased from $2,000 to $2,300.

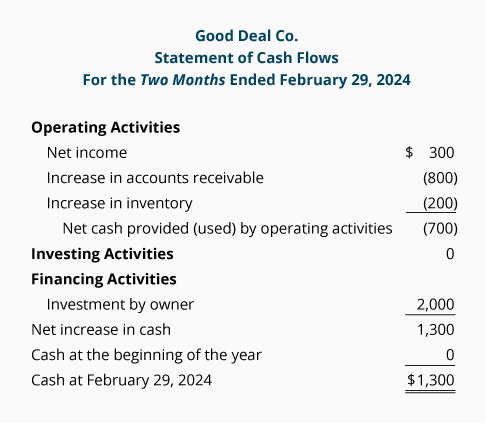

The SCF for the two months of January 1 through February 28, begins with the accrual accounting net income of $300. Since this is not the amount of cash from operating activities, the net income must be adjusted to the net amount of cash from operating activities.

During this two-month time period, the company’s accounts receivable increased from $0 to $800. An increase in accounts receivable means that the customers purchasing on credit did not yet pay for all the credit sales the company reported on the income statement. Therefore, we subtract the increase in accounts receivable from the company’s net income. Not having collected the total amount of past credit sales was not good for the company’s cash balance. For these reasons, the amount of the company’s accrual net income must be adjusted downward. Again, the reported (800) is the adjustment to the net income amount because of the increase in accounts receivable.

During the two-month time period, the company’s inventory changed from $0 on January 1 to $200 at February 28. (Recall that the company had purchased 14 calculators at a cost of $50 each and then sold 10 calculators. That left 4 calculators in inventory at a cost of $50 each.) The increase in inventory from $0 to $200 during this two-month time period required the company to spend (have a cash outflow of) $200. The use of cash for adding goods to inventory is also viewed as not good for the company’s cash balance and is therefore reported on the SCF as (200).

Given these adjustments, the net cash flow from operating activities is a net cash outflow of (700). (The calculation is $300 cash inflow – $800 cash outflow – $200 cash outflow.) The net cash outflow is presented as a negative amount and is described as net cash used in operating activities.

The cash flow statement also shows $2,000 of financing by the owner. When this is combined with the negative $700 from operating activities, the net change in cash for the first two months is a positive $1,300. This agrees to the change in cash on the balance sheet—none on January 1, but $1,300 on February 28.

Please let us know how we can improve this explanation

No Thanks