DEFINITION

Current liabilities are a company’s 1) obligations arising from past transactions, and 2) the amounts must be paid (or satisfied) within one year.

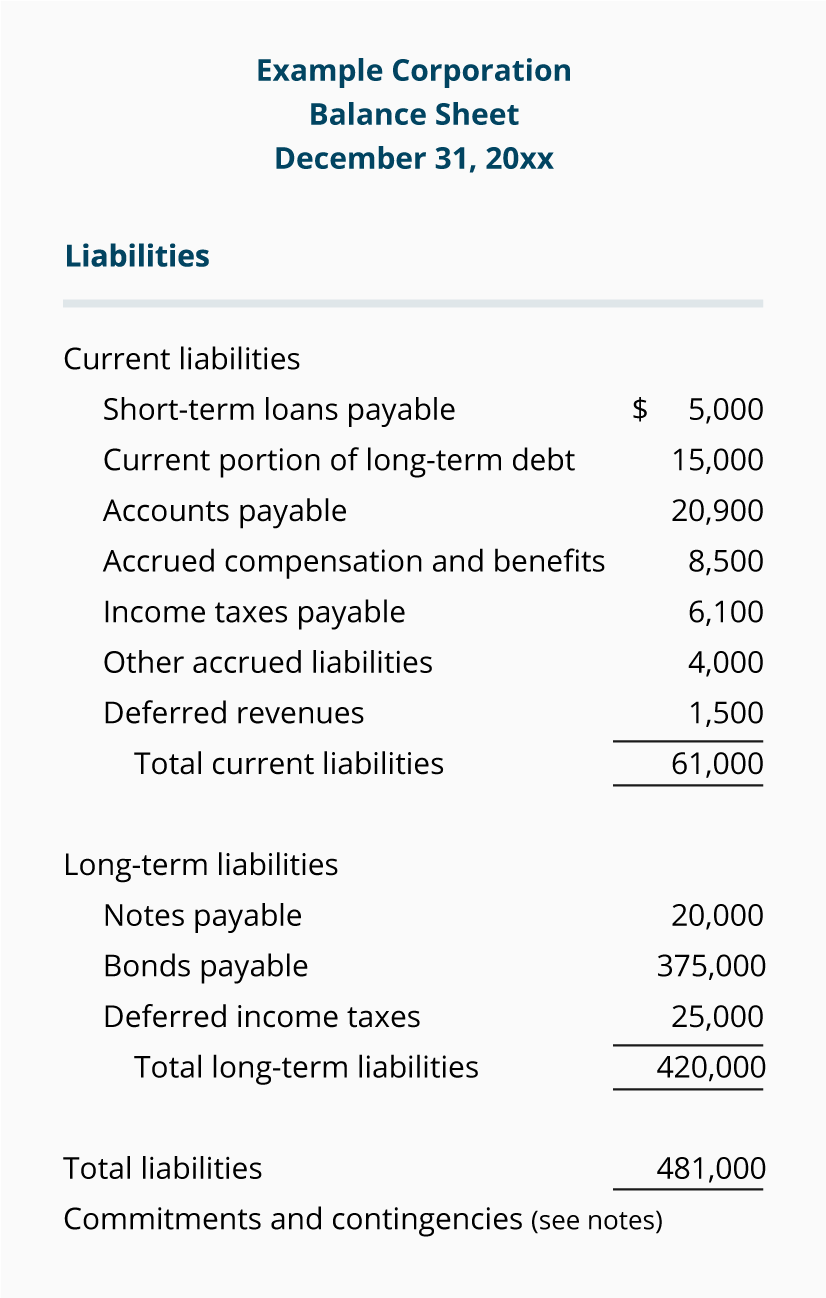

The amounts owed are recorded in the company’s general ledger accounts known as current liability accounts. These account balances will be summarized into perhaps 5 lines which are reported on the company’s balance sheet under the heading current liabilities.

Reporting the amount of current liabilities is necessary so management, lenders, and others can determine whether the company’s current assets are sufficient to pay the current liabilities when they are due.

In the accounting for current liabilities, the current liability accounts are increased with a credit entry. (Each entry will also include a debit entry to a different account such as an expense or asset account.) The credit balances in the current liability accounts are reduced with a debit entry. (For instance, when a company pays a current liability, the account balance is reduced with a debit entry and the Cash account is credited.)

Therefore, it is normal for current liability accounts to have credit balances. A debit balance in a current liability account likely indicates an error occurred somewhere in the account.

Formula for Calculating the Amount of Current Liabilities

The formula for calculating the total amount of current liabilities = the sum of the amounts that the company has incurred and must pay within one year.

Many of these amounts are already recorded in the company’s general ledger accounts such as Accounts Payable, Short-term Notes Payable, and Other Current Liabilities. However, there are usually additional obligations (that will be due within a year) that are not yet recorded in the general ledger accounts.

The unrecorded obligations the company incurred must also be included in the calculation of current liabilities. Accountants refer to these as accrued expenses and accrued liabilities which require adjusting entries prior to issuing the company’s balance sheets.

Current Liabilities are a Key Component of Other Formulas

A company’s current liabilities are a key component in the formulas for calculating three “liquidity” financial ratios. These ratios (or metrics) are used to judge whether a company will be able to pay its current liabilities when they are due. The three financial ratios and their formulas are:

- Working capital = current assets – current liabilities

- Current ratio = current assets / current liabilities

- Quick ratio = liquid assets / current liabilities

Sample calculations are shown later.

Current Liabilities vs. Noncurrent or Long-term Liabilities

The formula for calculating the amount of current liabilities = sum of the amounts a company has incurred and must be paid within one year.

The formula for calculating the amount of noncurrent liabilities = sum of the amounts the company has incurred, but the amounts are not due until after one year.

Generally, a company will have most of its transactions with its suppliers of goods and services who allow the company to pay in 10 to 60 days. Since the due dates are sooner than one year, the amounts are recorded with a credit entry in a current liability account such as Accounts Payable.

Less frequently, the company will have transactions where the amounts are to be paid after one year. These transactions are recorded with a credit entry in a noncurrent or long-term liability account. The balances in the noncurrent liability accounts will be reported on the balance sheet immediately after the total amount of current liabilities.

Some transactions may affect both a current liability account and a noncurrent liability account.

For example, a corporation’s bonds payable will involve:

- The principal or maturity amount (assume $2 million) that must be repaid at the end of 5 years, and

- Interest amounts (assume $120,000 semiannually) that must be paid at the end of each of the 10 six-month periods.

When the bonds are issued, the principal amount of $2 million is recorded as a long-term liability. The corporation will also be incurring interest expense and a current liability of $20,000 per month ($120,000 semiannually divided by 6 months). Therefore, each month the corporation will record a debit of $20,000 to Interest Expense and a credit of $20,000 to the current liability account Accrued Interest Payable.

The balance in Accrued Interest Payable will increase by $20,000 each month. At the end of each 6-month period, the credit balance will be $120,000 before recording the $120,000 interest payment to the bondholders. The interest payment will debit Accrued Interest Payable and credit Cash. As a result, the balance in Accrued Interest Payable is reduced to $0 for that moment.

Examples of Current Liabilities

You should expect a company to have many current liability accounts for its many obligations. However, when the current liabilities are reported on the external balance sheet, the company will summarize these account balances into perhaps 5 or 6 amounts.

The order in which the current liabilities appear on the balance sheet will vary by company. We will discuss some common current liability categories in the following order:

- Accounts payable

- Accrued expenses

- Short-term borrowings

- Current portion of long-term debt

- Deferred revenue

- Other current liabilities

Accounts payable

Accounts payable (or trade payables) are the amounts a company owes to its vendors or suppliers for goods or services it obtained on credit. Typically, the amounts are recorded in the general ledger account Accounts Payable when the goods or services have been received and the vendors’ invoices are reviewed and approved for payment.

Assume a company had a plumbing repair and the plumber’s invoice is approved for payment. The invoice will be the source document for a credit entry in the general ledger account Accounts Payable and a debit to the general ledger account Plumbing Repairs Expense.

Accrued expenses

Accrued expenses (or accrued payables) refer to expenses that occurred in the accounting period, but the vendor’s invoice was not recorded in the accounts as of the end of the accounting period.

A typical example is the electricity used by a retailer each month. Let’s assume a retailer began operating on December 1 and it is required to pay for the electricity used. The bill for the electricity used in December is calculated after the electricity meters are read in early January. Therefore, as of December 31 the retailer’s general ledger accounts have no expense and no liability for the electricity used during December. However, the retailer has agreed to provide its investors and lenders with the December financials by January 4.

For the December financial statements to report realistic amounts, the retailer must report an estimated cost for December’s electricity. If $1,000 is a realistic estimate, the retailer will record an accrual-type adjusting entry dated December 31 that debits Electricity Expense for $1,000 and credits the current liability Accrued Expenses or Accrued Electricity Expense.

Reporting a realistic, estimated amount is better than reporting no expense and no liability.

Other examples of accrued expenses/liabilities include interest incurred on debt (but not yet paid) and wages earned by employees (but not yet paid).

Short-term borrowings

Short-term borrowings (or short-term debt) is the amount of principal owed to lenders must be repaid within one year.

When the loan proceeds are received from the lender and the amount must be repaid within one year, the company will credit the current liability account Short-term Borrowings (and debit the current asset account Cash). When the company repays the loan, the account Short-term Borrowings will be debited, and the account Cash will be credited.

The interest associated with the loan is recorded after it is incurred. This is done with a credit to a separate current liability account such as Interest Payable (and a debit to Interest Expense).

Current portion of long-term debt

The current liability “current portion of long-term debt” reports the principal amount of long-term loans that must be repaid within one year of the balance sheet’s date.

(Note interest expense that has occurred, but has not yet been paid, is recorded as a credit in a separate current liability account such as Accrued Interest Expense.)

To illustrate, assume that a company obtained a 3-year, 8% loan of $72,000 on January 2 to purchase a new delivery truck. The loan required 36 monthly payments of $2,193.55 each that will be withdrawn from the company’s checking account on the last day of each month.

By using a loan amortization schedule the company can determine amounts of 1) principal that will be repaid in the first 12 monthly payments, and 2) interest that will be paid. Assumeg the totals for the years are: $21,499.52 for principal repayment and $4,823.03 for interest. The company will record the loan on January 2 as follows:

- Debit Cash for $72,000

- Credit the current liability account Current Portion of Long-term Debt for $21,499.52

- Credit the noncurrent or long-term liability account Truck Loan Payable for $48,550.48 ($72,000 – $21,499.52)

On January 31, the company will use the loan amortization schedule to record the following:

- Debit Interest Expense for $466.67

- Debit Truck Loan Payable for $1,726.88

- Credit Cash for $2,193.55

(Occasionally, the principal amounts that are due within one year and due after one year are reviewed and adjusted to agree with the loan amortization schedule.)

Deferred revenue

The current liability deferred revenue (or unearned revenue) is the amount of money a company has received from its customers but has not yet been earned. It could represent customer deposits, down payments, or advance payments.

Until the money is earned, it cannot be reported as revenue on the income statement. Therefore, any unearned amounts are deferred to the balance sheet and recorded in the current liability account Deferred Revenue.

When the company earns the money by delivering the customers’ goods or services, the amounts earned will be debited to Deferred Revenue and credited to an income statement account such as Revenue Earned.

Other current liabilities

Small balances in the current liability accounts that don’t fit into the main categories will be reported on the balance sheet as “other current liabilities”.

The Importance of Reporting Current Liabilities

The current liabilities section of the balance sheet is of interest to many users of the company’s financial statements including:

- Management

- Owners

- Bankers and other lenders

- Financial analysts

- Vendors/suppliers

- Customers

A significant concern involves the company’s ability to pay its bills and meet other obligations on time. When a company fails to meet its payments and other obligations on time, it signals there is a financial problem. In response, its banker and other lenders become cautious about extending loans or granting additional loans.

Not paying suppliers on time can lead to a reduction in the amount they provide on credit. Even customers want assurance that their suppliers have the financial ability to produce and supply their orders of goods even with slowdowns in the economy.

To satisfy their concerns and fears, the various parties will ask for a company’s financial statements so it can determine if the company’s financial position is sufficient. An early step will be comparing the company’s current liabilities to the company’s current assets.

Calculation of Financial Ratios Using the Current Liabilities

To illustrate the formulas for three financial ratios (or metrics), which are categorized as liquidity ratios, let’s assume a company has $120,000 of current assets (which include inventory having a cost of $70,000) and current liabilities of $100,000.

- Working capital = current assets of $120,000 – current liabilities of $100,000 = $20,000

- Current ratio = current assets of $120,000 / current liabilities of $100,000 = 1.2

- Quick ratio = quick assets* of $50,000 / current liabilities of $100,000 = 0.5.

*Quick assets are current assets except that inventory and prepaid expenses are excluded. In other words, the quick ratio assumes that only the company’s cash, temporary investments, and accounts receivable can be turned to cash quickly.

The calculated ratios should be compared to other companies in the same industry or to the averages for the company’s industry.

You can learn more by visiting our In-Depth Explanation of Working Capital and Liquidity.

What if the Current Liabilities Are Understated?

Keep in mind that a company’s financial statements are interconnected with the double-entry accounting system and the accounting equation. Therefore, if the amount of current liabilities is incorrect there will be at least one other item on the income statement or balance sheet that is incorrect not to mention the resulting subtotals, totals, ratios, etc.

For instance, if the company fails to record an emergency repair, the current liabilities on the balance sheet will be incorrect and so will the amount of expenses on the income statement. This means the net income is incorrect as well as the owner’s equity, financial ratios, and more.

Month-end Closing Procedures

To be certain that a company’s monthly financial statements include all current liabilities at the end of each month (and only the expenses, losses, revenues, and gains that belong in the month), it is wise to have procedures for the “month-end close” or “monthly closing”. The standard procedures include:

- A proper cutoff of revenue and expense transactions

- Accrual adjusting entries to record all the liabilities and expenses (not simply the transactions that were routinely recorded in the general ledger accounts)

- Deferral adjusting entries to record or adjust the account balances of deferred revenues and prepaid expenses.

- Recording other adjusting entries such as the allowance for doubtful accounts (and bad debts expense), accumulated depreciation (and depreciation expense), etc.

- Reconciling (reviewing, documenting) the balances in other balance sheet accounts.

The final month of the accounting year is especially important since these financial statements are likely distributed outside of the company. As a result, this “year-end close” will be more intense, thorough, and needs to be more accurate.