For multiple-choice and true/false questions, simply press or click on what you think is the correct answer. For fill-in-the-blank questions, press or click on the blank space provided.

If you have difficulty answering the following questions, learn more about this topic by reading our Inventory and Cost of Goods Sold (Explanation).

FIFO

LIFO

Average

FIFO

LIFO

Average

FIFO

LIFO

Average

Cost

Sales Value

Periodic

Perpetual

FIFO

LIFO

Average

FIFO

LIFO

Average

LIFO Periodic

LIFO Perpetual

Neither

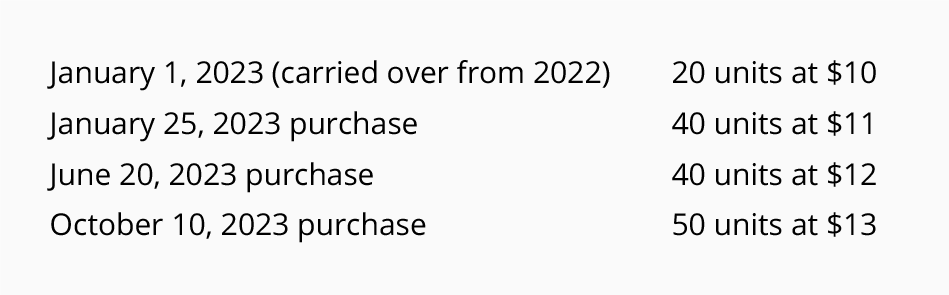

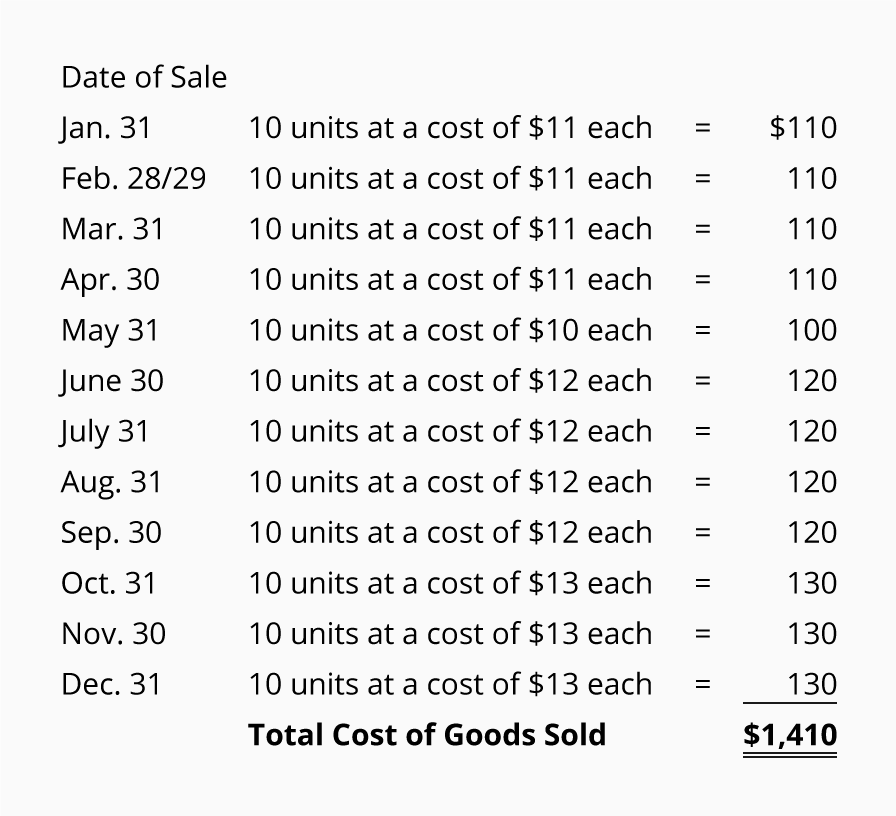

Use the following information for questions 9 – 14:

A company purchased merchandise at increasing costs during the year 2023. The purchases were made at the following costs…

The company sold 10 items at the end of each month.

$1,380

$1,386

$1,400

$1,460

$1,380

$1,386

$1,410

$1,460

$1,386

$1,410

$1,416

$1,460

$1,386

$1,410

$1,416

$1,460

$1,386

$1,410

$1,416

$1,460

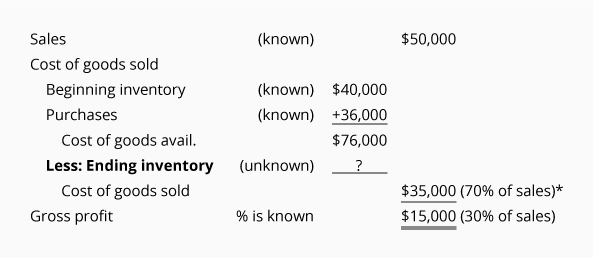

$26,000

$35,000

$41,000

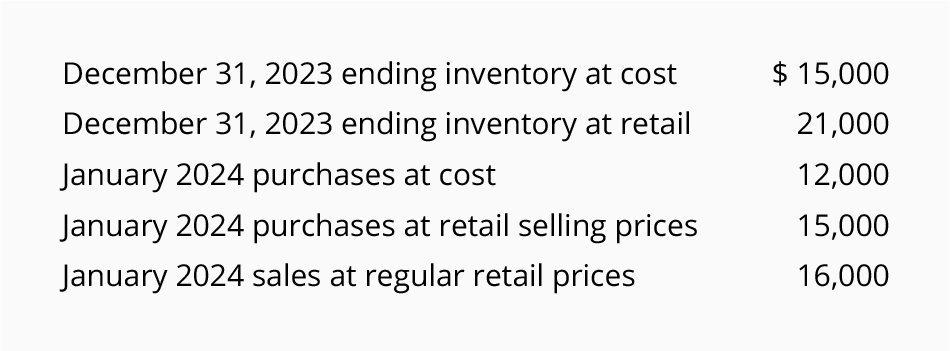

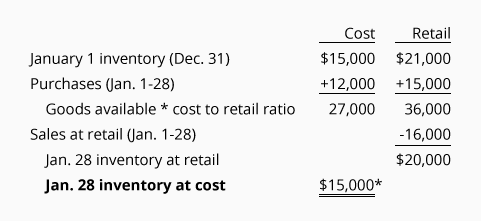

A retailer has the following information:

The estimated cost of inventory to be shown on the retailer's January 31, 2024 balance sheet is

$15,000

$16,000

$20,000

Too High

Too Low

Not Affected

True

False

Want more practice questions?

Receive instant access to our graded Quick

Tests (more than 1,800 unique test questions) when you join

AccountingCoach PRO.

Featured Review

"I am a staff accountant at a small CPA firm in southern California. I previously worked as the accountant for a county probate department for a number of years, and also worked briefly for an oil & gas company. I finished my accounting degree in 2016, but it wasn't long into my career that I realized I didn't know many of the things I should have learned in college. I would often have to google things I should have already learned, and found that I was often directed to AccountingCoach, which answered nearly all my questions. That was when I decided to become a PRO user, and AccountingCoach became my primary tool for supplemental learning. There are tons of topics available and the concepts are taught in an easy-to-understand manner. I especially like the quizzes and the ease of use of the entire program. AccountingCoach has helped me learn many of the things I should have learned in college, and I believe it has directly influenced my professional growth." - Vincent M.

Join PRO or PRO Plus and Get Lifetime Access to Our Premium Materials

Read all 2,645 reviews

For the past 52 years, Harold Averkamp (CPA, MBA) has

worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.

We now offer 10 Certificates of Achievement for Introductory Accounting and Bookkeeping: