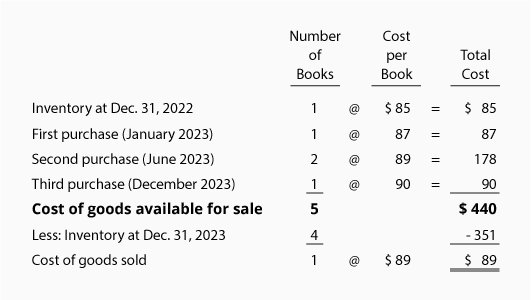

Perpetual FIFO

When using the perpetual inventory system, the general ledger account Inventory is constantly (or perpetually) changing. For example, when a retailer purchases merchandise, the retailer debits its Inventory account for the cost. (Under the periodic system, the account Purchases was debited.) When the retailer sells the merchandise the Inventory account is credited and the Cost of Goods Sold account is debited for the cost of the goods sold. Rather than the Inventory account staying dormant as it did with the periodic method, the Inventory account balance is updated for every purchase and sale.

Under the perpetual system, two entries are recorded when merchandise is sold: (1) the amount of the sale is debited to Accounts Receivable or Cash and is credited to Sales, and (2) the cost of the merchandise sold is debited to the account Cost of Goods Sold and is credited to Inventory.

(Note: Under the periodic system the second entry is not made.)

With perpetual FIFO, the first (or oldest) costs are the first removed from the Inventory account and debited to the Cost of Goods Sold account. Therefore, the perpetual FIFO cost flows and the periodic FIFO cost flows will result in the same cost of goods sold and the same cost of the ending inventory.

Please let us know how we can improve this explanation

No ThanksPerpetual LIFO

When using the perpetual system, the Inventory account is constantly (or perpetually) changing. The Inventory account is updated for every purchase and every sale.

Under the perpetual system, two transactions are recorded at the time that the merchandise is sold: (1) the amount of the sale is debited to Accounts Receivable or Cash and is credited to Sales, and (2) the cost of the merchandise sold is debited to the account Cost of Goods Sold and is credited to Inventory. (Note: Under the periodic system the second entry is not made.)

With perpetual LIFO, the last costs available at the time of the sale are the first to be removed from the Inventory account and debited to the Cost of Goods Sold account. Since this is the perpetual system we cannot wait until the end of the year to determine the last cost (as is done with periodic LIFO). An entry is needed at the time of the sale in order to reduce the balance in the Inventory account and to increase the balance in the Cost of Goods Sold account.

If the costs of the goods purchased rise throughout the entire year, perpetual LIFO will result in a lower cost of goods sold and a higher net income than periodic LIFO. Generally this means that periodic LIFO will result in less income taxes than perpetual LIFO. (If you wish to minimize the amount paid in income taxes during periods of inflation, you should discuss LIFO with your tax adviser.)

We will demonstrate perpetual LIFO by using the same Corner Bookstore information:

Let’s assume that after Corner Bookstore makes its second purchase in June 2023, Corner Bookstore sells one book. This means the latest cost at the time of the sale was $89. Under perpetual LIFO the following entry must be made at the time of the sale: $89 will be credited to Inventory and $89 will be debited to Cost of Goods Sold. If that was the only book sold during the year, at the end of the year the Cost of Goods Sold account will have a balance of $89 and the cost in the Inventory account will be $351 ($85 + $87 + $89 + $90).

If the bookstore sells the textbook for $110, its gross profit under perpetual LIFO will be $21 ($110 – $89). Note that this $21 is different than the gross profit of $20 under periodic LIFO.

Please let us know how we can improve this explanation

No ThanksPerpetual Average

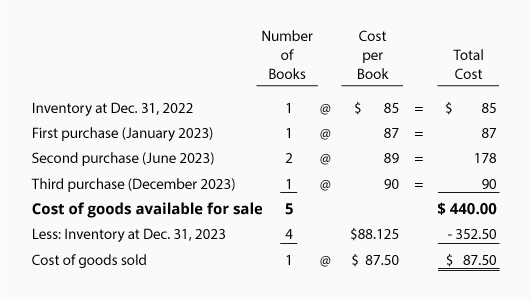

When using the perpetual inventory system, the Inventory account is constantly (or perpetually) changing. The inventory account is updated for every purchase and every sale.

With the perpetual system, two sets of entries are made whenever merchandise is sold: (1) the amount of the sale is debited to Accounts Receivable or Cash and is credited to Sales, and (2) the cost of the merchandise sold is debited to the account Cost of Goods Sold and is credited to the account Inventory. (Note: Under the periodic system the second entry is not made.)

In the perpetual system, “average” means the average cost of the items in inventory as of the date of the sale. This requires calculating a new average cost per unit after every purchase. The new average cost is multiplied by the number of units sold and is credited to the Inventory account and debited to the Cost of Goods Sold account. (We use the average as of the time of the sale because this is a perpetual method. Under the periodic system we wait until the year is over before computing the average cost.)

Let’s demonstrate the perpetual average method using the Corner Bookstore information:

Let’s assume that on July 1 Corner Bookstore sells one book. This means the average cost at the time of the sale was $87.50 ([$85 + $87 + $89 + $89] ÷ 4). Because this is a perpetual average, a journal entry must be made at the time of the sale for $87.50. The $87.50 (the average cost at the time of the sale) is credited to Inventory and is debited to Cost of Goods Sold. After the sale on July 1, three copies remain in inventory. The balance in the Inventory account will be $262.50 (3 books at an average cost of $87.50).

After Corner Bookstore makes its third purchase of the year 2023, the average cost per unit will change to $88.125 ([$262.50 + $90] ÷ 4). As you can see, the average cost moved from $87.50 to $88.125—this is why the perpetual average method is sometimes referred to as the moving average method. The Inventory balance is $352.50 (4 books with an average cost of $88.125 each).

Please let us know how we can improve this explanation

No Thanks