For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.

Before you begin: If you enjoy this free In-Depth Explanation, we recommend trying our PRO materials (used by 80,000+ professionals). You'll receive lifetime access to our certificates of achievement, video training, flashcards, visual tutorials, quick tests, cheat sheets, guides, business forms, printable PDF files, and more. Earn badges, points, and medals as you track your progress and display your achievements on your public profile page.

Introduction

Inventory is a key current asset for retailers, distributors, and manufacturers. Inventory consists of goods (products, merchandise) awaiting to be sold to customers as well as a manufacturer’s raw materials and work-in-process that will become finished goods. Inventory is recorded and reported on a company’s balance sheet at its cost.

When an inventory item is sold, the item’s cost is removed from inventory and the cost is reported on the company’s income statement as the cost of goods sold. Cost of goods sold is likely the largest expense reported on the income statement. When the cost of goods sold is subtracted from sales, the remainder is the company’s gross profit.

It is critical that the items in inventory get sold relatively quickly at a price larger than its cost. Without sales the company’s cash remains in inventory and unavailable to pay the company’s expenses such as wages, salaries, rent, advertising, etc.

It is common for a company to experience rising costs for the goods it purchases. As a result, the company’s costs may be different for the same products purchased during its accounting year. When this occurs, the company must decide which costs should be matched with its sales and which costs should remain in inventory. In the U.S., three of the cost flow methods for removing costs from inventory and reporting them as the cost of goods sold include:

FIFO or first in, first out. This cost flow removes the oldest inventory costs and reports them as the cost of goods sold on the income statement, while the most recent costs remain in inventory.

LIFO or last in, first out. This cost flow removes the most recent inventory costs and reports them as the cost of goods sold on the income statement, and the oldest costs remain in inventory.

Weighted average. This method calculates an average per unit cost and applies it to both the units in inventory and to the units sold.

In addition to selecting a cost flow method, the company selects one of the following inventory systems for recording amounts in its general ledger Inventory account(s):

The periodic system indicates that the Inventory account will be updated periodically, such as on the last day of the accounting year. Throughout the year, the goods purchased will be recorded in temporary general ledger accounts entitled Purchases. At the end of the year, the cost of the ending inventory will be calculated. The Inventory account balance will be adjusted to this amount. At this time, the cost of goods sold is also calculated.

The perpetual system indicates that the Inventory account will be continuously or perpetually updated. In other words, the balance in the Inventory account will be increased by the costs of the goods purchased, and will be decreased by the cost of the goods sold. Hence, the balance in the Inventory account should reflect the cost of the inventory items currently on hand. However, companies should count the actual goods on hand (take a physical inventory) at least once a year and adjust the perpetual records if necessary.

It is time consuming and costly for companies to physically count the items in inventory, determine their unit costs, and calculate the total cost in inventory. There may also be times when it is necessary to determine the cost of inventory that was destroyed by fire or stolen. To solve these problems, accountants often use the gross profit method for estimating the cost of a company’s ending inventory.

We will illustrate the FIFO, LIFO, and weighted-average cost flows along with the periodic and perpetual inventory systems. This will be done with simple, easy-to-understand, instructive examples involving a hypothetical retailer Corner Bookstore.

WATCH NOWAdvance Your Career with Our PRO Training

Please let us know how we can improve this explanation

No Thanks

Close

Inventory Is Reported at Cost

Inventory items are recorded at their cost. Cost is defined as all costs necessary to get the goods in place and ready for sale. For instance, if a bookstore purchases a college textbook from a publisher for $80 and pays $5 to get the book delivered to its store, the bookstore will record the cost of $85 in its Inventory account. The recorded cost will not be increased even if the publisher announces that additional copies will cost $100.

When the textbook is sold, the bookstore removes the cost of $85 from its inventory and reports the $85 as the cost of goods sold on the income statement that reports the sale of the textbook.

The recorded cost for the goods remaining in inventory at the end of the accounting year are reported as a current asset on the company’s balance sheet.

Please let us know how we can improve this explanation

No Thanks

Close

Periodic vs Perpetual Inventory Systems

Each cost flow assumptions can be used in either of the following inventory systems:

Periodic

Perpetual

Under the periodic inventory system:

The amount appearing in the general ledger Inventory account is not updated when purchases of merchandise are made from suppliers or when goods are sold.

The Inventory account is normally adjusted only at the end of the year. During the year the Inventory account will show only the cost of inventory as of the end of the previous year.

Purchases of merchandise are recorded in one or more Purchases accounts.

At the end of the year the Purchases account(s) are closed and the Inventory account is adjusted to the cost of the merchandise actually on hand at the end of the current year.

There is no Cost of Goods Sold account to be updated when a sale of merchandise occurs.

There is no way to tell from the general ledger accounts the cost of the current inventory or the cost of goods sold.

Under the perpetual inventory system:

The Inventory account is continuously updated.

It is increased with the cost of merchandise purchased from suppliers.

It is reduced by the cost of merchandise that has been sold to customers.

The Purchases account(s) are not used in the perpetual inventory system.

There is a general ledger account Cost of Goods Sold that is debited at the time of each sale for the cost of the merchandise that was sold.

A sale of goods will result in a journal entry to record the amount of the sale and the cash received or the recording of accounts receivable.

A second journal entry reduces the account Inventory and increases the account Cost of Goods Sold.

Please let us know how we can improve this explanation

No Thanks

Close

When a Company Purchases Identical Items at Increasing Costs

We will use a hypothetical business Corner Bookstore to demonstrate how to flow the costs out of inventory and into the cost of goods sold on the company’s income statement. Often this is done by using either the periodic inventory system or the perpetual system.

Before we begin, keep in mind that there can be a difference between the following:

How the units of product are physically removed from inventory

How the costs are removed from inventory

Generally, the units are physically removed from inventory by selling the oldest units first. Therefore, the physical units of product are flowing first in, first out. Companies want to get the oldest items out of inventory and keep the most recent (freshest) ones in inventory. Businesses will refer to this as rotating the goods on hand or rotating the stock.

However, the costs of the goods in inventory do not have to flow the way the goods flowed. This means the bookstore can sell the oldest copy of its three copies from inventory but remove the cost of its most recently purchased copy. In other words, the goods can flow using first in, first out while the costs flow using last in, first out. This is why accountants refer to the cost flows as cost flow assumptions.

Please let us know how we can improve this explanation

No Thanks

Close

Demonstrating Cost Flow Assumptions

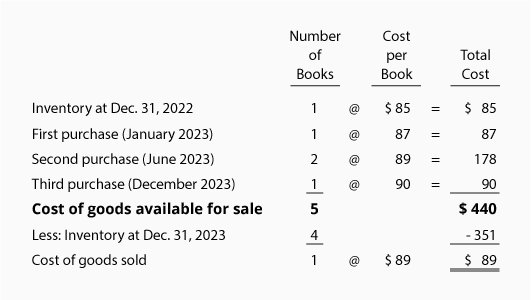

Let’s assume the Corner Bookstore had one book in inventory at the start of the year 2024 and at different times during 2024 it purchased four additional copies of the same book. During the year 2024, the publisher increased the price of the books due to a paper shortage. The following chart shows Corner Bookstore’s total cost of the five books was $440. It also assumes that none of the books has been sold as of December 31, 2024.

If the Corner Bookstore sells only one of the five books, which cost should Corner Shelf report as the cost of goods sold? Should it select $85, $87, $89, $89, $90, or the average cost of the five amounts? Which cost should Corner Bookstore report as inventory on its balance sheet for the four unsold books?

In the U.S., three of the most common ways to flow costs out of inventory and into the cost of goods sold are:

First in, first out (FIFO)

Last in, first out (LIFO)

Weighted average

Note that these are cost flow assumptions. Recall that the order in which costs are removed from inventory (and reported on the income statement as the cost of goods sold) can be different from the order in which the goods are physically removed from inventory. In other words, if Corner Bookstore sells one book that was on hand at the beginning of the year it can remove from inventory the $90 cost of the most recently purchased book in December 2024 (if it had elected the periodic LIFO cost flow assumption).

Please let us know how we can improve this explanation

No Thanks

Close

Inventory Systems with Cost Flow Assumptions

The combination of the three cost flow assumptions and the two inventory systems means six options for calculating the cost of inventory and the cost of goods sold:

Please let us know how we can improve this explanation

No Thanks

Close

Periodic FIFO

Periodic means that the Inventory account is not routinely updated during the accounting period. Instead, the cost of merchandise purchased from suppliers is debited to the general ledger account Purchases. At the end of the accounting year the Inventory account is adjusted to equal the cost of the merchandise that has not been sold.

The cost of goods sold (which is reported on the income statement) is computed by taking the cost of the goods available for sale and subtracting the cost of the ending inventory.

FIFO is an acronym for first in, first out. Under the FIFO cost flow assumption, the first (oldest) costs are the first costs to leave inventory and be reported as the cost of goods sold on the income statement. The last (or recent) costs will remain in inventory and be reported as inventory on the balance sheet.

Remember that the costs can flow differently than the physical flow of the goods. For example, if the Corner Bookstore uses the FIFO cost flow assumption, the owner may sell any copy of the book but report the cost of goods at the first/oldest cost as shown in the exhibit that follows.

Let’s demonstrate periodic FIFO with the following information from the Corner Bookstore:

As before, we need to account for the cost of goods available for sale (5 books having a total cost of $440). With FIFO we assign the first cost of $85 to be the cost of goods sold. The remaining $355 ($440 – $85) will be the cost of the ending inventory. The $355 of inventory costs consists of $87 + $89 + $89 + $90. The $85 cost that was assigned to the book sold is permanently gone from inventory.

If Corner Bookstore sells the textbook for $110, its gross profit using periodic FIFO will be $25 ($110 – $85). If the costs of textbooks continue to increase, FIFO will always result in more gross profit than other cost flows, because the first cost will always be lower.

Please let us know how we can improve this explanation

No Thanks

Close

Periodic LIFO

Periodic means that the Inventory account is not updated during the accounting period. Instead, the cost of merchandise purchased from suppliers is debited to the general ledger account Purchases. At the end of the accounting year the Inventory account is adjusted to the cost of the merchandise that is unsold. The remainder of the cost of goods available is reported on the income statement as the cost of goods sold.

LIFO is an acronym for last in, first out. With the LIFO cost flow assumption, the latest (or most recent) costs are the first ones to leave inventory and become the cost of goods sold on the income statement. The first/oldest costs will remain in inventory and will be reported as the cost of the ending inventory on the balance sheet.

Remember that the costs can flow differently than the physical flow of the goods. In other words, if Corner Bookstore uses periodic LIFO, the owner may sell the oldest (first) copy of the book to a customer, and report the cost of goods sold of $90 (the cost of the most recently purchased book).

It’s important to note that under periodic LIFO (not perpetual LIFO) you wait until the entire year is over before assigning the costs. Then you flow out of inventory the year’s most recent costs first, even if those goods arrived after the last sale of the year. For example, assume the last sale of the year at the Corner Bookstore occurred on December 27. Also assume that the store’s last purchase of the year arrived on December 31. Under periodic LIFO, the cost of the book purchased on December 31 is removed from inventory and sent to the cost of goods sold first, even though it was physically impossible for that book to be the one sold on December 27. (This reinforces our earlier statements that the flow of costs does not have to correspond with the physical flow of units.)

Let’s illustrate periodic LIFO by using the data for the Corner Shelf Bookstore:

As before, we need to account for the cost of goods available for sale: 5 books having a total cost of $440. Under periodic LIFO we assign the last cost of $90 to the book that was sold. (If two books were sold, $90 would be assigned to the first book and $89 to the second book.) The remaining $350 ($440 – $90) is reported as the cost of the ending inventory. The $350 of inventory cost consists of $85 + $87 + $89 + $89. The $90 assigned to the book that was sold is permanently gone from inventory.

If the bookstore sold the textbook for $110, its gross profit using periodic LIFO will be $20 ($110 – $90). If the costs of textbooks continue to increase, periodic LIFO will always result in the least amount of profit. The reason is that the last costs will always be higher than the first costs. Higher costs result in less profits and often lower income taxes.

Please let us know how we can improve this explanation

No Thanks

Close

Periodic Average

When the periodic inventory system is used, the Inventory account is not updated when goods are purchased. Instead, purchases of merchandise are recorded in the general ledger account Purchases.

With the average or weighted average cost flow assumption an average cost is calculated using the cost of goods available for sale (cost from the beginning inventory plus the costs of all the purchases made during the year). This means that the periodic average cost is calculated after the year is over—after all the purchases for the year have occurred. This average cost is then applied to the units sold during the year and to the units in inventory at the end of the year.

We will assume the same facts. There were 5 books available for sale for the year 2024 and the cost of the goods available was $440. The weighted average cost of the books is $88 ($440 of cost of goods available ÷ 5 books). The average cost of $88 is used to compute both the cost of goods sold and the cost of the ending inventory.

Since the bookstore sold only one book, the cost of goods sold is $88 (1 x $88). The ending inventory of four unsold books is reported at the cost of $352 (4 x $88) . The total of the cost of goods sold plus the cost of the inventory should equal the cost of goods available ($88 + $352 = $440).

If Corner Bookstore sells the textbook for $110, its gross profit using the periodic average method will be $22 ($110 – $88). This gross profit of $22 lies between the $25 computed using the periodic FIFO and the $20 computed using the periodic LIFO.

Please let us know how we can improve this explanation

No Thanks

Close

Perpetual FIFO

When using the perpetual inventory system, the general ledger account Inventory is constantly (or perpetually) changing. For example, when a retailer purchases merchandise, the retailer debits its Inventory account for the cost. (Under the periodic system, the account Purchases was debited.) When the retailer sells the merchandise, the Inventory account is credited and the Cost of Goods Sold account is debited for the cost of the goods sold. Rather than the Inventory account staying dormant as it did with the periodic system, the Inventory account balance is updated for every purchase and sale.

Under the perpetual system, two entries are recorded when merchandise is sold: (1) the amount of the sale is debited to Accounts Receivable or Cash and is credited to Sales, and (2) the cost of the merchandise sold is debited to the account Cost of Goods Sold and is credited to Inventory. (Note: Under the periodic system the second entry is not made.)

With perpetual FIFO, the first (or oldest) costs are the first costs removed from the Inventory account and debited to the Cost of Goods Sold account. Therefore, the perpetual FIFO cost flows and the periodic FIFO cost flows will result in the same cost of goods sold and the same cost of the ending inventory.

Please let us know how we can improve this explanation

No Thanks

Close

Perpetual LIFO

When using the perpetual system, the Inventory account is constantly (or perpetually) changing. The Inventory account is updated for every purchase and every sale.

Under the perpetual system, two transactions are recorded at the time that the merchandise is sold: (1) the amount of the sale is debited to Accounts Receivable or Cash and is credited to Sales, and (2) the cost of the merchandise sold is debited to the account Cost of Goods Sold and is credited to Inventory. (Note: Under the periodic system the second entry is not made.)

With perpetual LIFO, the last costs available at the time of the sale are the first to be removed from the Inventory account and debited to the Cost of Goods Sold account. Since this is the perpetual system we cannot wait until the end of the year to determine the last cost (as is done with periodic LIFO). An entry is needed at the time of the sale in order to reduce the balance in the Inventory account and to increase the balance in the Cost of Goods Sold account.

If the costs of the goods purchased rise throughout the entire year, perpetual LIFO will result in a lower cost of goods sold and a higher net income than periodic LIFO. Generally this means that periodic LIFO will result in less income taxes than perpetual LIFO. (If you wish to minimize the amount paid in income taxes during periods of inflation, you should discuss LIFO with your tax adviser.)

We will demonstrate perpetual LIFO by using the same Corner Bookstore information:

Let’s assume that after Corner Bookstore makes its second purchase in June 2024, Corner Bookstore sells one book. This means the latest cost at the time of the sale was $89. Under perpetual LIFO the following entry must be made at the time of the sale: $89 will be credited to Inventory and $89 will be debited to Cost of Goods Sold. If that was the only book sold during the year, at the end of the year the Cost of Goods Sold account will have a balance of $89 and the cost in the Inventory account will be $351 ($85 + $87 + $89 + $90).

If the bookstore sells the textbook for $110, its gross profit under perpetual LIFO will be $21 ($110 – $89). Note that this $21 is different than the gross profit of $20 under periodic LIFO.

Please let us know how we can improve this explanation

No Thanks

Close

Perpetual Average

When using the perpetual inventory system, the Inventory account is constantly (or perpetually) changing. The inventory account is updated for every purchase and every sale.

With the perpetual system, two sets of entries are made whenever merchandise is sold: (1) the amount of the sale is debited to Accounts Receivable or Cash and is credited to Sales, and (2) the cost of the merchandise sold is debited to the account Cost of Goods Sold and is credited to the account Inventory. (Note: Under the periodic system the second entry is not made.)

In the perpetual system, “average” means the average cost of the items in inventory as of the date of the sale. This requires calculating a new average cost per unit after every purchase. The new average cost is multiplied by the number of units sold and is credited to the Inventory account and debited to the Cost of Goods Sold account. (We use the average as of the time of the sale because this is a perpetual system. Under the periodic system we wait until the year is over before computing the average cost.)

Let’s demonstrate the perpetual average system using the Corner Bookstore information:

Let’s assume that on July 1 Corner Bookstore sells one book. This means the average cost at the time of the sale was $87.50 ([$85 + $87 + $89 + $89] ÷ 4). Because this is a perpetual average, a journal entry must be made at the time of the sale for $87.50. The $87.50 (the average cost at the time of the sale) is credited to Inventory and is debited to Cost of Goods Sold. After the sale on July 1, three copies remain in inventory. The balance in the Inventory account will be $262.50 (3 books at an average cost of $87.50).

After Corner Bookstore makes its third purchase of the year 2024, the average cost per unit will change to $88.125 ([$262.50 + $90] ÷ 4). As you can see, the average cost moved from $87.50 to $88.125—this is why the perpetual average method is sometimes referred to as the moving average method. The Inventory balance is $352.50 (4 books with an average cost of $88.125 each).

Please let us know how we can improve this explanation

No Thanks

Close

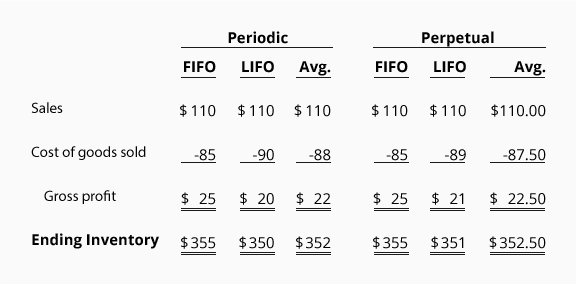

Comparison of Cost Flow Assumptions

Below is a recap of the varying amounts for the cost of goods sold, gross profit, and ending inventory that were calculated above.

The examples assumed that costs were continually increasing. The results would be different if costs were decreasing or increasing at a slower rate. Consult with your tax adviser concerning the election of a cost flow assumption.

In past periods of inflation, many U.S. companies switched from FIFO to LIFO. However, once the switch is made, a company cannot change back to FIFO.

Please let us know how we can improve this explanation

No Thanks

Close

Specific Identification

In addition to the six cost flow options discussed earlier, businesses have another option: expense to the cost of goods sold the specific cost of the specific item it decided to sell. For example, Gold Dealer, Inc. has an inventory of gold and each gold bar has an identification number with the cost of the gold bar. When Gold Dealer sells a gold bar, it can expense to the cost of goods sold the exact cost of the specific gold bar sold. The cost of the other gold bars will remain in inventory. (Alternatively, Gold Dealer could use one of the other six cost flow options described earlier.)

Please let us know how we can improve this explanation

No Thanks

Close

LIFO Benefits Without Tracking Units

Earlier we demonstrated that during periods of increasing costs, LIFO resulted in less profits. In the U.S. this can mean less income taxes paid by a corporation. Most corporations view lower taxes as a significant benefit. However, the process of tracking costs and then assigning those costs to the units sold and the units on hand could be too troublesome for the amount of income tax savings. To gain the benefit of LIFO without tracking costs, there is a method known as dollar value LIFO. This topic is discussed in intermediate accounting textbooks. The Internal Revenue Service also allows companies to use dollar value LIFO by applying price indexes. (You should seek the advice of an accounting and/or tax professional to assess the cost and benefit of LIFO techniques.)

Please let us know how we can improve this explanation

No Thanks

Close

Inventory Management

Over the past decades sophisticated companies have made great strides in reducing their levels of inventory. Rather than carry large inventories, they ask their suppliers to deliver goods “just in time.” Suppliers and merchandisers have learned to coordinate their purchases and sales so that orders and shipments occur automatically.

A company will realize significant benefits if it can keep its inventory levels down without losing sales or production (if the company is a manufacturer). In its early days, Dell Computers greatly reduced its inventory in relationship to its sales. Since the cost of computer components had been dropping as new technologies emerged, it benefited Dell to keep a small inventory of components on hand. It would be a financial hardship if Dell had a large quantity of components that became obsolete or decreased in value.

Please let us know how we can improve this explanation

No Thanks

Close

Financial Ratios

Keeping track of inventory is important. There are two common financial ratios for monitoring inventory levels: (1) Inventory Turnover Ratio, and (2) Days’ Sales in Inventory. These are discussed and illustrated in our Financial Ratios Explanation.

Please let us know how we can improve this explanation

No Thanks

Close

Verifying Ending Inventory

It is very time-consuming for a company to physically count the units of goods in its inventory. In fact, some companies shut down their operations near the end of their accounting year just to perform inventory counts. Often a company assigns one team of employees to count and tag the items and another team to verify the counts. If a company has outside auditors, they will be in attendance to observe the process. (Even if the company’s computers keep track of inventory, the computer quantities must be verified by physically counting the goods at least once per year.)

If a company uses the periodic inventory system and physically counts its inventory only once per year, it must estimate the cost of its inventory at the end of each interim accounting period for its interim financial statements. In fact, a company may need to estimate its inventory for other reasons as well. For example, if a company suffers a loss due to a disaster such as a tornado or a fire, it will need to file a claim for the estimated cost of the inventory that was lost. (An insurance adjuster will also compute the amount independently so that the company is not paid too much or too little for its loss.)

Please let us know how we can improve this explanation

No Thanks

Close

Estimating Inventory: Gross Profit Method

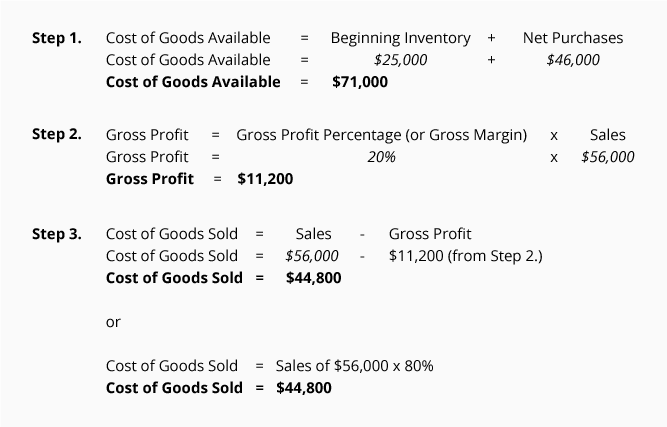

The gross profit method for estimating the cost of the ending inventory uses information from a previously issued income statement. To illustrate the gross profit method we will assume that ABC Company needs to estimate the cost of its ending inventory on June 30, 2024.

ABC’s most recent income statement (which is representative of current conditions) contained the following information:

From ABC’s 2023 information we see that the company’s gross profit was 20% of sales, and therefore its cost of goods sold was 80% of sales. If those percentages are reasonable for the current year, we can use them to estimate the cost of the inventory on hand as of June 30, 2024.

While an algebraic equation could be used, we prefer to simply use the income statement format. We will prepare a partial income statement for the period beginning after the date when inventory was last physically counted, and ending with the date for which we need the estimated inventory cost. In this case, the income statement we prepare will cover the period of January 1, 2024 through June 30, 2024.

Some of the amounts needed can be obtained from sales records, customers, suppliers, earlier financial statements, etc. For example, sales for the first half of the year 2024 are taken from the company’s records. The beginning inventory amount is the ending inventory reported on the December 31, 2023 balance sheet. The purchases information for the first half of 2024 is available from the company’s records or from its suppliers. The amounts that were available are shown in italics in the following partial income statement:

We will fill in the rest of the statement with the answers from the following calculations. The calculation amounts in italics come from the income statement above. The calculation amounts in bold will be used to complete the above section of the income statement:

Inserting this information into the income statement yields the following:

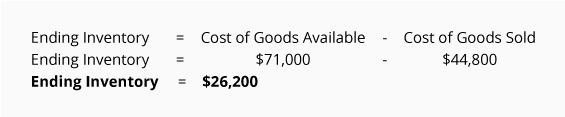

Next, we need to compute the ending inventory amount. This is done by subtracting the cost of goods sold from the cost of goods available as shown here:

Below is the completed partial income statement with the estimated amount of ending inventory at $26,200. (Note: Always recheck the math on the income statement to be certain you computed the amounts correctly.)

Please let us know how we can improve this explanation

No Thanks

Close

Estimating Inventory: Retail Method

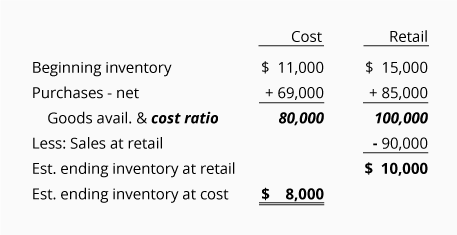

Another method for estimating inventory is the retail method. This method can be used by retailers who have their merchandise records in both cost and retail selling prices. A very simple illustration of using the retail method for estimating the cost of ending inventory (using hypothetical amounts unrelated to earlier examples) is shown here:

Notice that the cost amounts are presented in one column and the retail amounts are listed in a separate column. The Goods Available amounts are used to compute the cost-to-retail ratio. In this case the cost of goods available of $80,000 is divided by the retail amount of goods available of $100,000. Therefore, the cost-to-retail ratio, or cost ratio, is 80%. The estimated ending inventory at cost is the estimated ending inventory at retail of $10,000 times the cost ratio of 80% equals $8,000.

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Inventory and Cost of Goods Sold materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.

Please let us know how we can improve this explanation

No Thanks

Close

That part of a manufacturer’s inventory that is in the production process but not yet completed. This account contains the cost of the direct material, direct labor, and factory overhead in the products so far. A manufacturer must disclose in its financial statements the cost of its work-in-process as well as the cost of finished goods and materials on hand.

One of the main financial statements. The balance sheet reports the assets, liabilities, and owner’s (stockholders’) equity at a specific point in time, such as December 31. The balance sheet is also referred to as the Statement of Financial Position.

One of the main financial statements (along with the statement of comprehensive income, balance sheet, statement of cash flows, and statement of stockholders’ equity). The income statement is also referred to as the profit and loss statement, P&L, statement of income, and the statement of operations. The income statement reports the revenues, gains, expenses, losses, net income and other totals for the period of time shown in the heading of the statement. If a company’s stock is publicly traded, earnings per share must appear on the face of the income statement.

Cost of goods sold is usually the largest expense on the income statement of a company selling products or goods. Cost of Goods Sold is a general ledger account under the perpetual inventory system.

Under the periodic inventory system there will not be an account entitled Cost of Goods Sold. Instead, the cost of goods sold is computed as follows: cost of beginning inventory + cost of goods purchased (net of any returns or allowances) + freight-in – cost of ending inventory.

This account balance or this calculated amount will be matched with the sales amount on the income statement.

A revenue account that reports the sales of merchandise. Sales are reported in the accounting period in which title to the merchandise was transferred from the seller to the buyer.

Gross profit is net sales revenues minus the cost of goods sold.

Costs that are matched with revenues on the income statement. For example, Cost of Goods Sold is an expense caused by Sales. Insurance Expense, Wages Expense, Advertising Expense, Interest Expense are expenses matched with the period of time in the heading of the income statement. Under the accrual basis of accounting, the matching is NOT based on the date that the expenses are paid.

Expenses associated with the main activity of the business are referred to as operating expenses. Expenses associated with a peripheral activity are nonoperating expenses or other expenses. For example, a retailer’s interest expense is a nonoperating expense. A bank’s interest expense is an operating expense.

Generally, expenses are debited to a specific expense account and the normal balance of an expense account is a debit balance. When an expense account is debited, the account credited might be Cash (if cash was paid at the time of the expense), Accounts Payable (if cash will be paid after the expense is recorded), or Prepaid Expense (if cash was paid before the expense was recorded.)

A cost flow assumption where the first (oldest) costs are assumed to flow out first. This means the latest (recent) costs remain on hand.

A cost flow assumption where the last (recent) costs are assumed to flow out of the asset account first. This means the first (oldest) costs remain on hand.

An assumption that determines the order in which costs should flow out of a balance sheet account (e.g. Inventory, Investments, Treasury Stock) when the item is sold.

An account in the general ledger, such as Cash, Accounts Payable, Sales, Advertising Expense, etc.

The entry made in a journal. It will contain the date, the account name and amount to be debited, and the account name and amount to be credited. Each journal entry must have the dollars of debits equal to the dollars of credits.

A current asset resulting from selling goods or services on credit (on account). Invoice terms such as (a) net 30 days or (b) 2/10, n/30 signify that a sale was made on account and was not a cash sale.

This is the sum of the beginning inventory of merchandise plus the net cost of the merchandise purchased including freight-in.

This ratio relates the costs in inventory to the cost of the goods sold.

Usually financial statements refer to the balance sheet, income statement, statement of comprehensive income, statement of cash flows, and statement of stockholders’ equity.

The balance sheet reports information as of a date (a point in time). The income statement, statement of cash flows, statement of comprehensive income, and the statement of stockholders’ equity report information for a period of time (or time interval) such as a year, quarter, or month.

For the past 52 years, Harold Averkamp (CPA, MBA) has

worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.