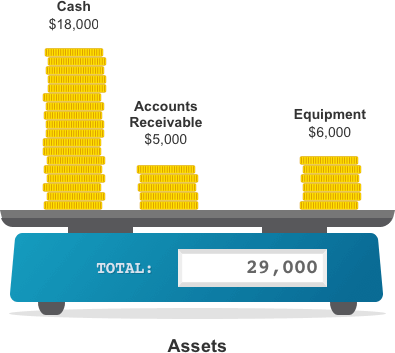

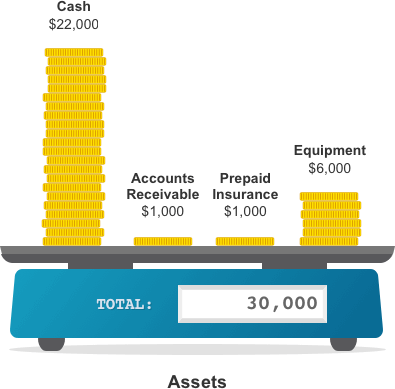

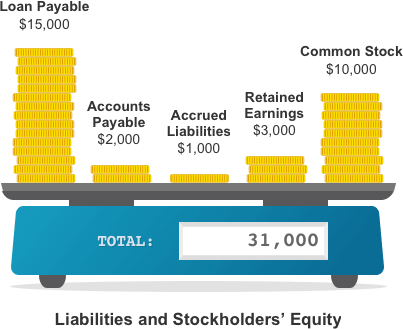

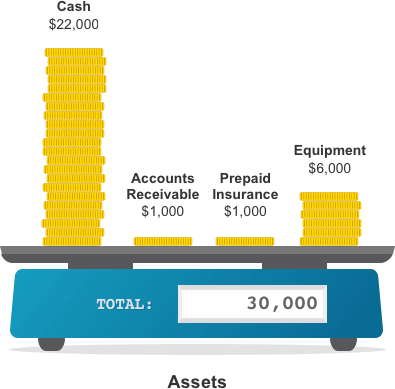

We will illustrate the effect of transactions on the accounting equation and on the balance sheet by using two digital scales. The scale on the left is used to report the total amount of assets. The scale on the right will report the total amount of the liabilities and stockholders’ equity. In U.S. organizations, the totals are reported in U.S. dollars.

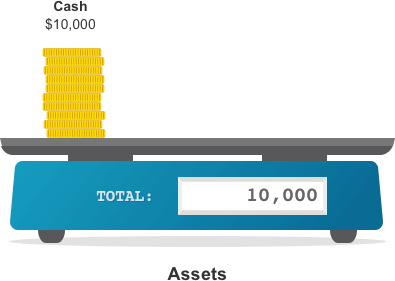

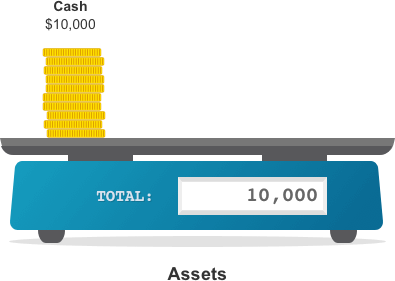

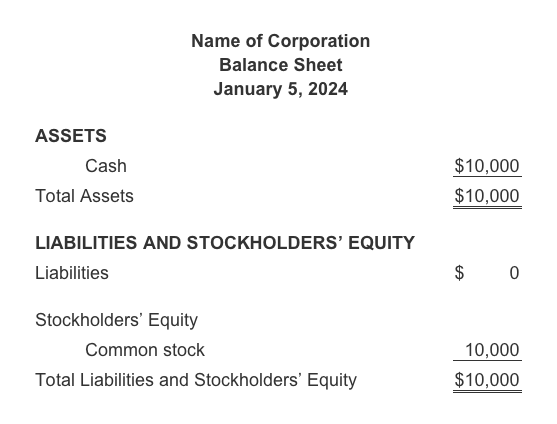

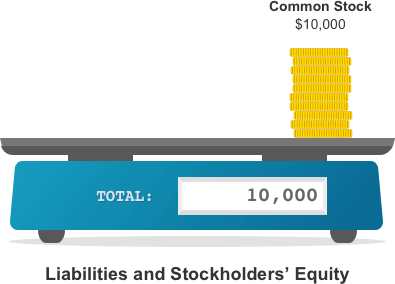

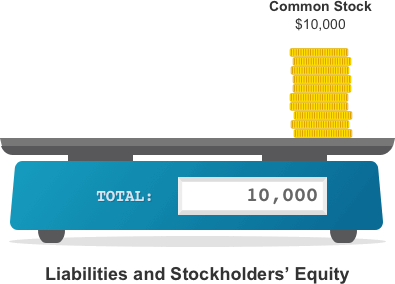

Step 1: The corporation’s asset Cash will increase by $10,000.

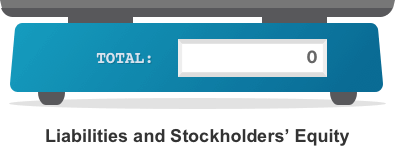

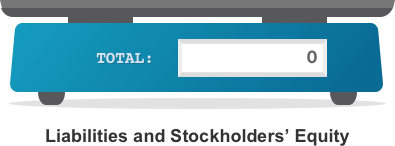

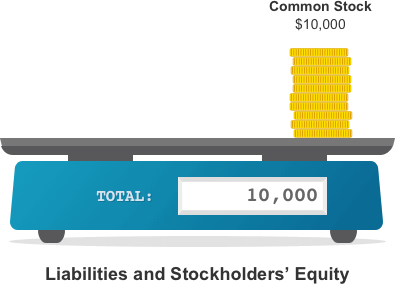

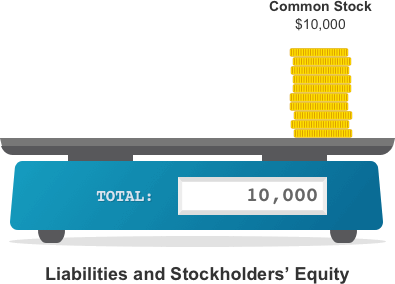

Step 2: The stockholders’ equity account Common Stock will also increase by $10,000.

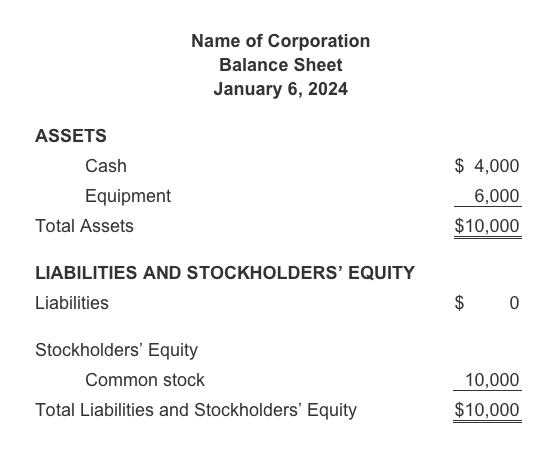

If a balance sheet were issued at this point, it would look like this:

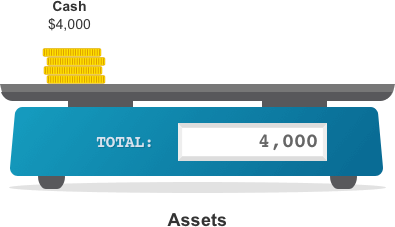

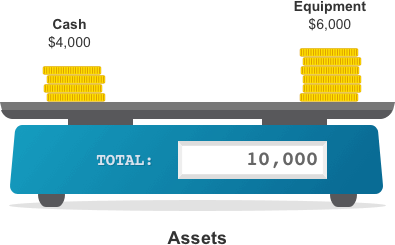

Step 1: The asset Cash will decrease by $6,000.

Step 2: The asset Equipment increases by $6,000.

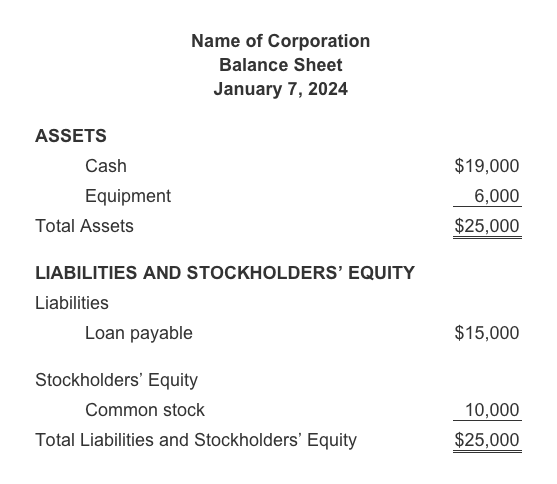

If a balance sheet were issued at this point, it would look like this:

Step 1: The corporation’s asset Cash (checking account) will increase by $15,000.

Step 2: The corporation’s liability Note Payable or Loan Payable increases by $15,000.

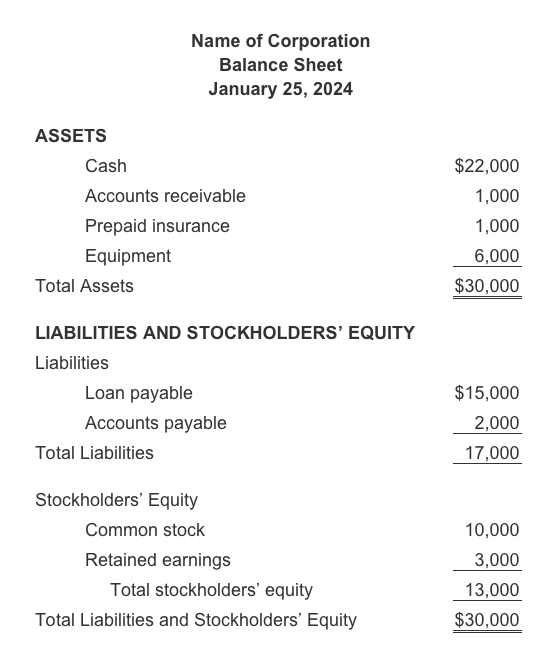

If a balance sheet were issued at this point, it would look like this:

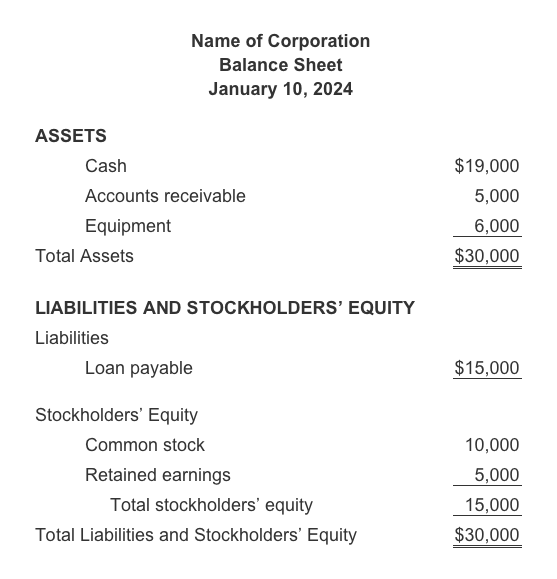

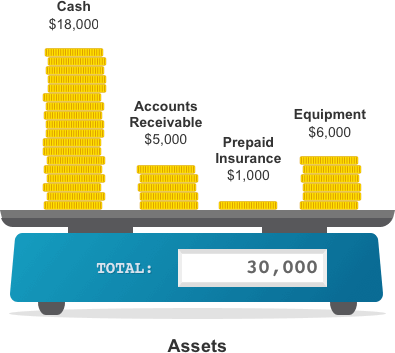

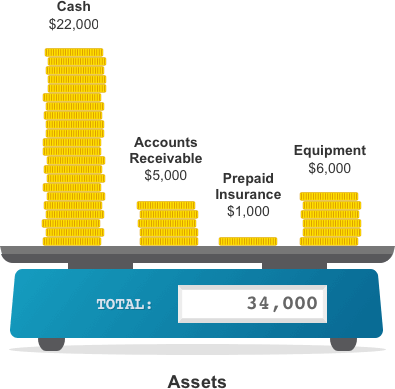

Step 1: The corporation’s asset Accounts Receivable will increase by $5,000.

Step 2: The corporation’s retained earnings will also increase by $5,000.

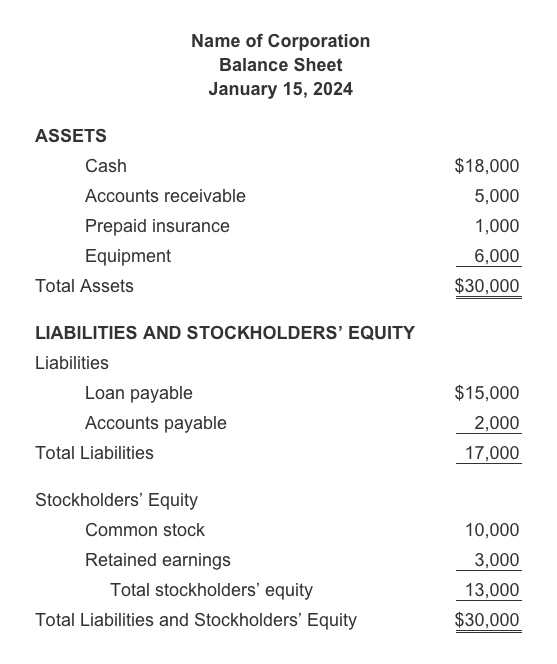

If a balance sheet were issued at this point, it would look like this:

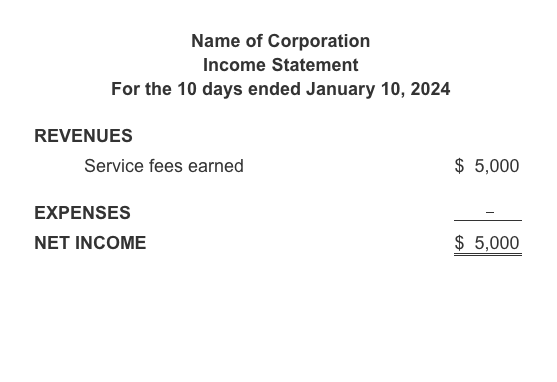

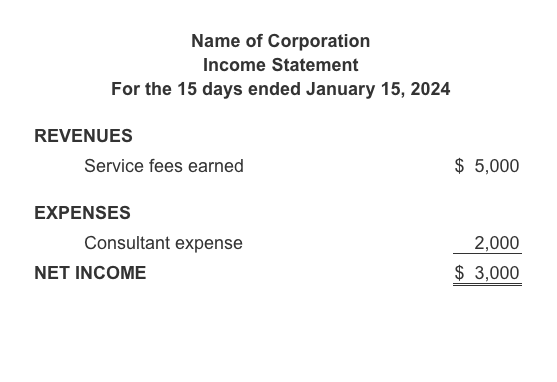

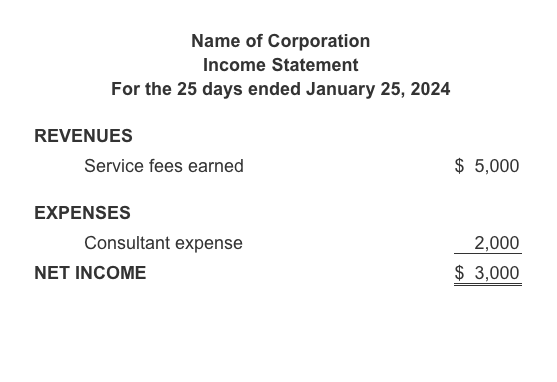

If an income statement were issued at this point, it would look like this:

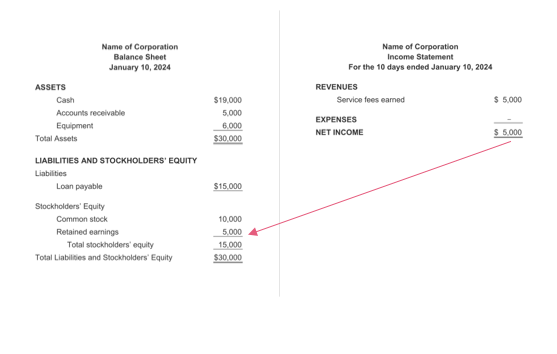

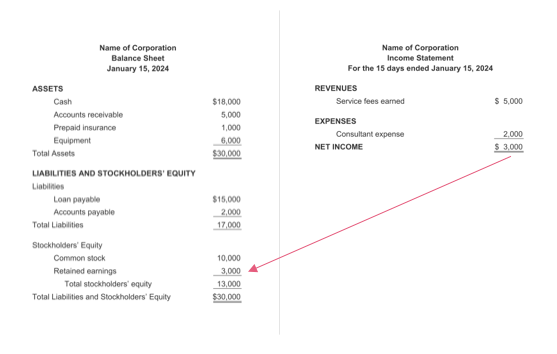

The balance sheet and income statement together would look like this:

Step 1: The corporation’s Accounts Payable (a liability) will increase by $2,000.

Step 2: The corporation’s Retained Earnings will decrease by $2,000. (The decrease in Retained Earnings is caused by the Consulting Expense of $2,000 reported on the income statement.)

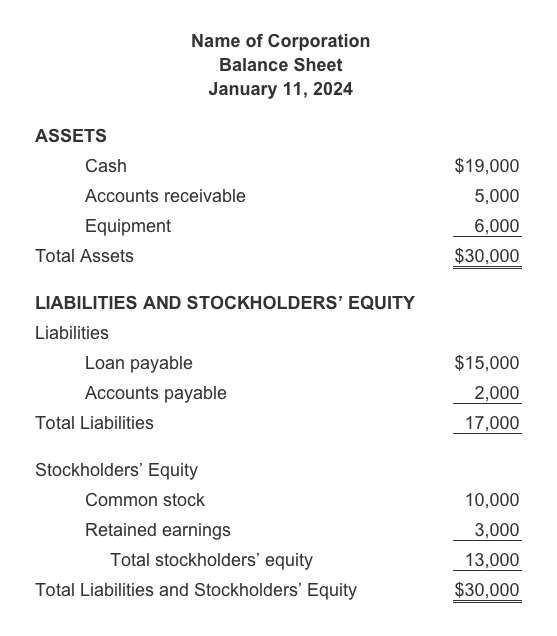

If a balance sheet were issued at this point, it would look like this:

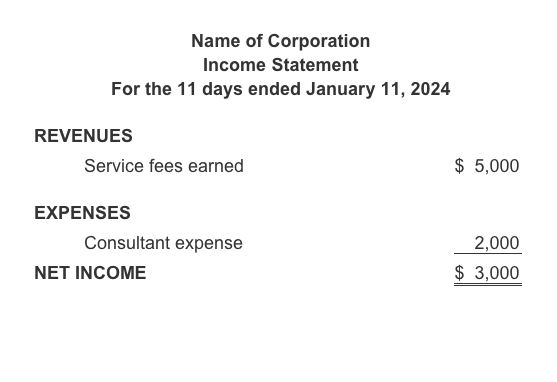

If an income statement were issued at this point, it would look like this:

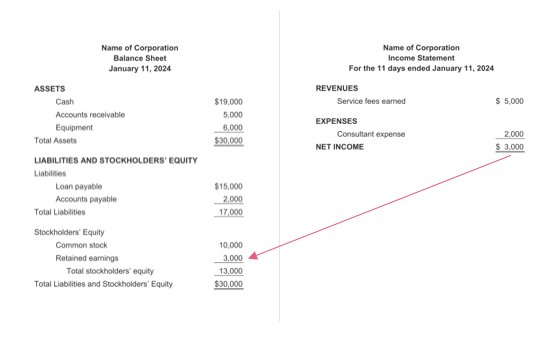

The balance sheet and income statement together would look like this:

Step 1: The corporation’s Cash will decrease by $1,000.

Step 2: The corporation’s asset Prepaid Insurance will increase by $1,000. (There is not an expense or decrease in Retained Earnings until February.)

If a balance sheet were issued at this point, it would look like this:

If an income statement were issued at this point, it would look like this:

The balance sheet and income statement together would look like this:

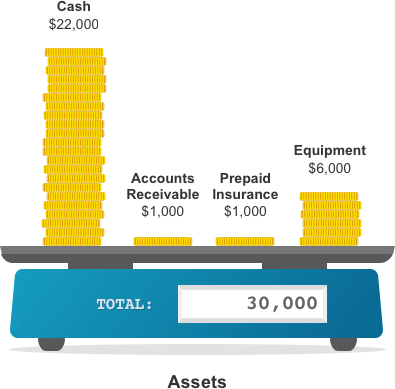

Step 1: The corporation’s Cash will increase by $4,000.

Step 2: The corporation’s Accounts Receivable will decrease by $4,000.

If a balance sheet were issued at this point, it would look like this:

If an income statement were issued at this point, it would look like this:

The balance sheet and income statement together would look like this:

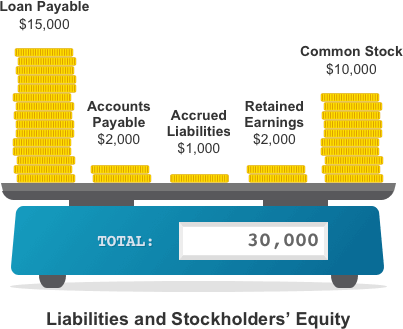

Step 1: The corporation’s Accrued Liabilities will increase by $1,000 for the accrued expenses.

Step 2: The corporation’s Retained Earnings will decrease because of the $1,000 of accrued utilities and interest expenses being reported on the income statement.

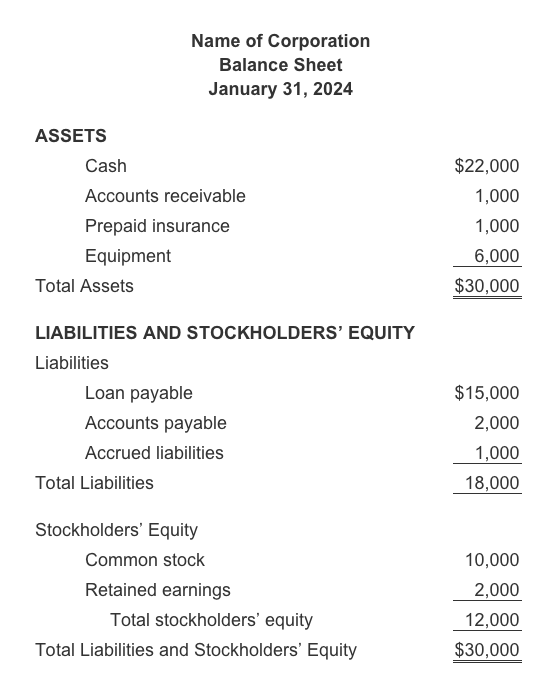

If a balance sheet were issued at this point, it would look like this:

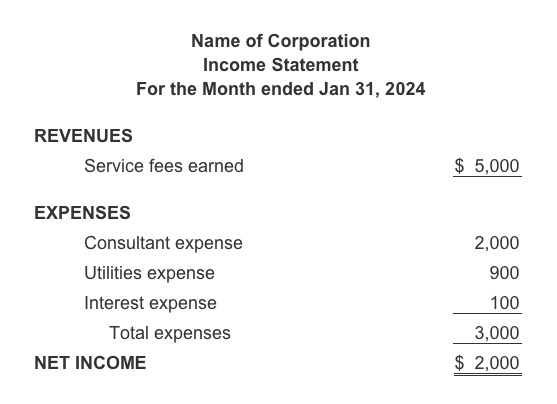

If an income statement were issued at this point, it would look like this:

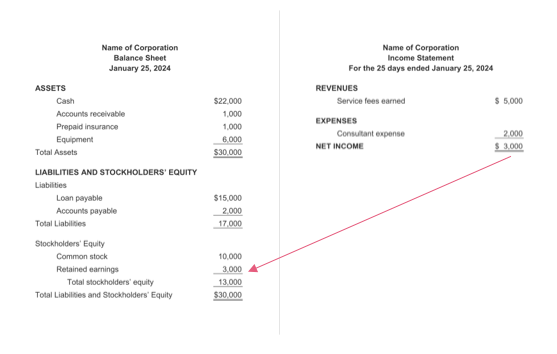

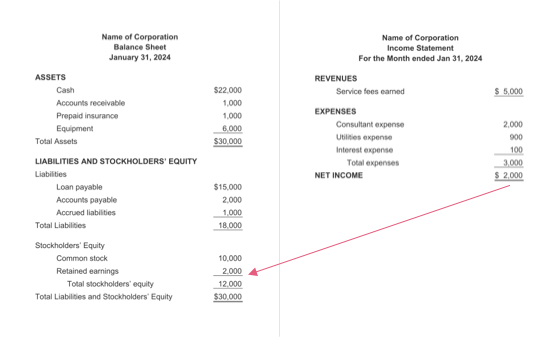

The balance sheet and income statement together would look like this:

Turn on study mode to focus

Accounting Equation Outline

Learn How to Advance Your Accounting and Bookkeeping Career

- Perform better at your current job

- Refresh your skills to re-enter the workforce

- Pass your accounting class

- Understand your small business finances

Featured Review

"I am currently employed at a food distributor as an account specialist. I have been using your website for about a year now. When I started here, I didn't know very much about accrual accounting, as I had always used the cash accounting method. In my position, I am responsible for entering the company’s JE. I was hired as an account specialist, with the opportunity for a promotion to Staff Accountant. For that promotion to be fulfilled, I needed to learn more about accounting procedures. My manager set goals for me to fulfill and went online to find some online accounting courses. That's when he found your website. At the time, we didn't know how useful the site would be, so we chose not to purchase the PRO Plus option. After using it for some time now, I found the site to be extremely useful. It is very user friendly and has a lot of valuable information. I have learned a great deal from your site. The biggest thing I learned was how the accounting equation works. I've been able to learn more about accruals, deferrals, adjusting journal entries, and more. I also understand more about how the JEs I enter affect our financial statements here. This has proven to be invaluable to me because it has helped me move closer to the promotion of Staff Accountant, which includes a pay raise. I know I have a lot more to learn." - Kim B.