Accounting Equation for a Corporation: Transactions C1–C2

The accounting equation (or basic accounting equation) for a corporation is:

Examples

In our examples below, we show how a given transaction affects the accounting equation for a corporation. We also show how the same transaction will be recorded in the company’s general ledger accounts.

In addition, we show the effect of each transaction on the balance sheet and income statement. (Our examples assume that the accrual basis of accounting is being followed.)

In the examples that follow, we will use the following accounts:

- Cash

- Accounts Receivable

- Equipment

- Notes Payable

- Accounts Payable

- Common Stock

- Retained Earnings

- Treasury Stock

- Service Revenues

- Advertising Expense

- Temp Service Expense

(To view a more complete listing of accounts for recording transactions, visit our Explanation of Chart of Accounts.)

We also assume that the corporation is a Subchapter S corporation in order to avoid the income tax accounting that would occur with a “C” corporation. (In a Subchapter S corporation the owners are responsible for the income taxes instead of the corporation.)

Corporation Transaction C1

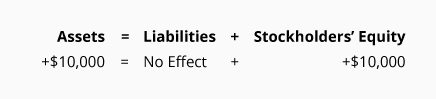

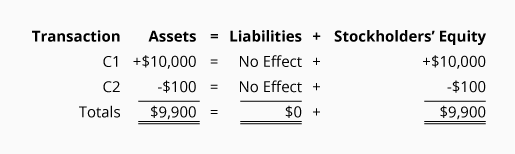

Let’s assume that members of the Ott family form a corporation called Accounting Software, Inc. (ASI). On December 1, 2023, several members of the Ott family invest a total of $10,000 to start ASI. In exchange, the corporation issues a total of 1,000 shares of common stock. (The stock has no par value and no stated value.) The effect on the corporation’s accounting equation is:

Since ASI’s assets increase by $10,000 and stockholders’ equity increases by the same amount the accounting equation is in balance.

The accounting equation tells us that ASI has assets of $10,000 and the source of those assets was the stockholders. Alternatively, the accounting equation tells us that the corporation has assets of $10,000 and the only claim to the assets is from the stockholders (owners).

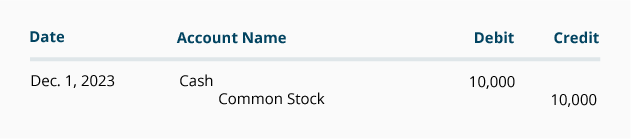

This transaction is recorded in the asset account Cash and in the stockholders’ equity account Common Stock. The general journal entry to record the transaction is:

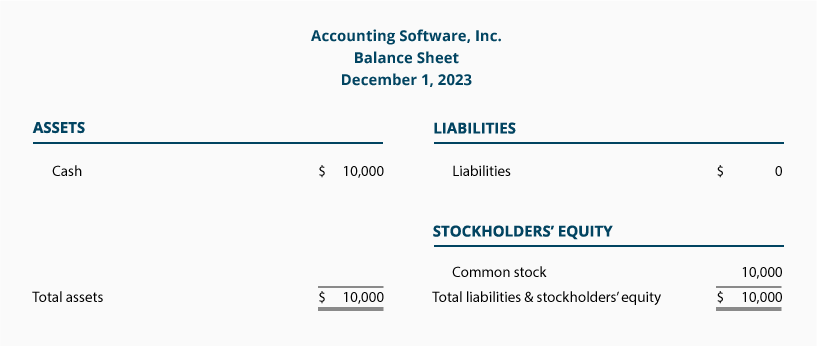

After the journal entry is recorded in the accounts, a balance sheet can be prepared to show ASI’s financial position at the end of December 1, 2023:

The purpose of an income statement is to report revenues and expenses. Since ASI has not yet earned any revenues nor incurred any expenses, there are no amounts to be reported on an income statement.

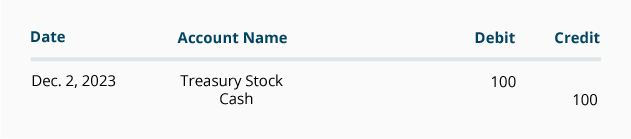

Corporation Transaction C2.

On December 2, 2023, ASI purchases $100 of its stock from one of its stockholders. The stock will be held by the corporation as Treasury Stock. The effect of the accounting equation is:

The purchase of its own stock for cash causes ASI’s assets to decrease by $100 and its stockholders’ equity to decrease by $100.

This transaction is recorded in the asset account Cash and in the stockholders’ equity account Treasury Stock. The accounting entry in general journal form is:

Since the transactions of December 1 and December 2 were in balance, the sum of both transactions should also be in balance:

The totals indicate that ASI has assets of $9,900 and the source of those assets is the stockholders. The accounting equation also shows that the corporation has assets of $9,900 and the only claim against the assets is the stockholders’ claim.

The December 2 balance sheet will communicate the corporation’s financial position as of midnight on December 2:

The purchase of a corporation’s own stock will never result in an amount to be reported on the income statement.

Please let us know how we can improve this explanation

No Thanks