Accounting Equation for a Sole Proprietorship: Transactions 1-2

We present eight transactions to illustrate how a company’s accounting equation stays in balance.

When a company records a business transaction, it is not entered into an accounting equation, per se. Rather, transactions are recorded into specific accounts contained in the company’s general ledger. Each account is designated as an asset, liability, owner’s equity, revenue, expense, gain, or loss account. The amounts in the general ledger accounts are then used to prepare the balance sheets and income statements.

In our transactions, we will use the following accounts:

- Cash

- Accounts Receivable

- Equipment

- Notes Payable

- Accounts Payable

- J. Ott, Capital

- J. Ott, Drawing

- Service Revenues

- Advertising Expense

- Temp Service Expense

(To view a more complete listing of accounts for recording transactions, visit our Explanation of Chart of Accounts.)

Sole Proprietorship Transaction #1.

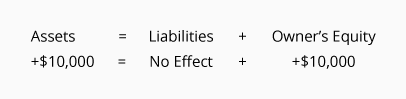

Let’s assume that J. Ott forms a sole proprietorship called Accounting Software Co. (ASC). On December 1, 2023, J. Ott invests personal funds of $10,000 to start ASC. The effect of this transaction on ASC’s accounting equation is:

As you can see, ASC’s assets increase by $10,000 and so does ASC’s owner’s equity. As a result, the accounting equation will be in balance.

You can interpret the amounts in the accounting equation to mean that ASC has assets of $10,000 and the source of those assets was the owner, J. Ott. Alternatively, you can view the accounting equation to mean that ASC has assets of $10,000 and there are no claims by creditors (liabilities) against the assets. As a result, the owner has a claim for the remainder or residual of $10,000.

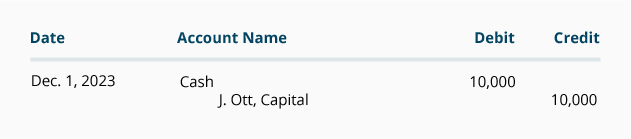

This transaction is recorded in the asset account Cash and the owner’s equity account J. Ott, Capital. The general journal entry to record the transaction in these accounts is:

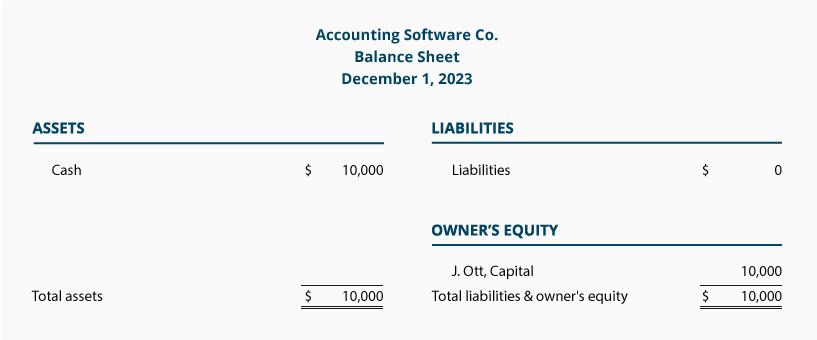

After the journal entry is recorded in the accounts, a balance sheet can be prepared to show ASC’s financial position at the end of December 1, 2023:

The purpose of an income statement is to report revenues and expenses. Since ASC has not yet earned any revenues nor incurred any expenses, there are no amounts to be reported on an income statement.

Sole Proprietorship Transaction #2.

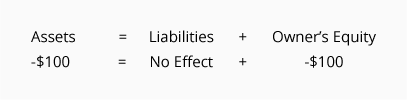

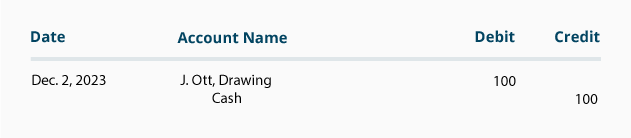

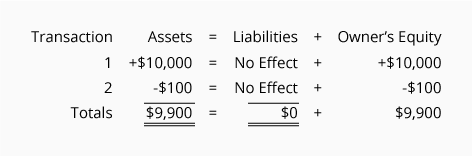

On December 2, 2023, J. Ott withdraws $100 of cash from the business for his personal use. The effect of this transaction on ASC’s accounting equation is:

The accounting equation remains in balance since ASC’s assets have been reduced by $100 and so has the owner’s equity.

This transaction is recorded in the asset account Cash and the owner’s equity account J. Ott, Drawing. The general journal entry to record the transactions in these accounts is:

Since the transactions of December 1 and December 2 were in balance, the sum of both transactions should also be in balance:

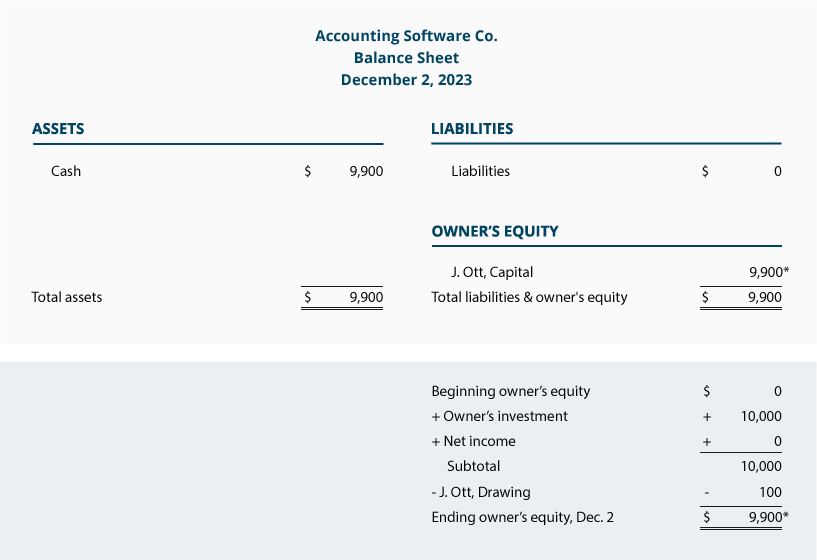

The totals indicate that ASC has assets of $9,900 and the source of those assets is the owner of the company. You can also conclude that the company has assets or resources of $9,900 and the only claim against those resources is the owner’s claim.

The December 2 balance sheet will communicate the company’s financial position as of midnight on December 2:

Withdrawals of company assets by the owner for the owner’s personal use are known as “draws.” Since draws are not expenses, the transaction is not reported on the company’s income statement.

Please let us know how we can improve this explanation

No Thanks