Minimum Wage and Overtime Pay

The Wage and Hour Division (WHD) of the U.S. Department of Labor is charged with administering the Fair Labor Standards Act (FLSA), which requires that employees be paid:

- A minimum wage for all hours worked, and

- Overtime at time and one-half of the regular or straight-time rate of pay for hours worked that are in excess of 40 hours in the workweek.

Some companies and some employees may be exempt from the FLSA rules due to the company’s size or other criteria. However, an employer must also review its state’s regulations and is required to follow the state regulation if it is more beneficial for the employee than the federal regulation. For example, some states require a minimum wage that is much larger than the federal minimum wage. There are also a few states that require overtime be paid for any hours worked in excess of 8 on any workday.

The U.S. Department of Labor, Wage and Hour Division, has Fact Sheet #17A which summarizes the federal exemptions. It is available at https://www.dol.gov/agencies/whd/fact-sheets/17a-overtime. At the end of the fact sheet is a link to the official federal regulations.

Minimum Wage

The federal minimum wage and each state’s minimum wage can be found through:

https://www.dol.gov/general/topic/wages/minimumwage

Overtime Pay

Overtime refers to time worked in excess of 40 hours per workweek. Whether or not employees are paid for overtime depends on each employee’s job responsibilities and rate of pay not the employee’s job title. As a result some employees are exempt from overtime pay and some are not. For example, highly-paid executives are considered to be “exempt”; and therefore their employers are not required to pay them for their overtime hours because (1) their compensation is high, and (2) they can control their work hours. Highly-paid executives do not need state or federal wage and hour laws to protect them from employer abuse.

On the other hand, office clerks earning an annual salary of $18,000 per year are probably not in control of their work hours. If the clerks work for an executive who decides to work 60 hours per week, the clerks need to be protected from having to work 60 hours per week for no more pay than they would receive for 40 hours of work. These employees are considered to be “nonexempt” from the overtime rules and therefore must be paid overtime compensation. Some companies have been known to classify “hourly wage” employees as “salaried” in hopes of making them exempt from overtime pay. Federal and state laws exist to prevent such unfair treatment of employees.

When processing payroll, don’t assume that it’s only the hourly-paid employees who receive overtime pay. State and federal laws require overtime payments to lower-paid salaried employees. It is also possible that some generous employers will give overtime pay to employees who are not required by law to receive it.

For information on the current minimum amount that a salaried employee must earn in order to be considered exempt from being paid overtime, see the U.S. Department of Labor, Wage and House Division website.

Overtime Premium

An overtime premium refers to the “half” portion of “time-and-a-half” or “time-and-one-half” overtime pay. For example, assume an employee in the production department is expected to work 40 hours per week at $10 per hour. If the employer requires the employee to work 42 hours in a given workweek, the extra two hours are paid at time-and-a-half and the employee will earn gross wages of $430 for the week (40 hours x $10 per hour, plus 2 overtime hours x $15 per hour). The gross wages can also be computed as 42 hours at the straight-time rate of $10 per hour plus 2 hours times the overtime premium of $5 per hour.

Calculating Overtime Pay for a Salaried Person

Let’s assume that an office clerk receives an annual salary of $18,000 per year and is expected to work 40 hours per week. However, during a recent workweek the clerk was required to work an additional 4 hours. This person’s salary and responsibilities require the employer to pay overtime at the rate of time-and-a-half for the additional 4 hours. The overtime pay calculation is as follows:

- The straight-time hourly rate for the annual salary of $18,000 is: $18,000 divided by 2,080 hours (40 hours in workweek X 52 weeks) = $8.65 per hour

- The overtime premium (which is half of the straight-time hourly rate) is: $8.65 times 50% = $4.33 per hour

- The time-and-a-half rate is: $8.65 + $4.33 = $12.98 for each overtime hour

Assuming the clerk is paid semimonthly, the clerk’s next paycheck will consist of the following:

- Regular salary amount of $750.00 ($18,000 divided by 24 semimonthly pay periods per year)

- Overtime pay is: 4 overtime hours X $12.98 (from above) = $51.92

- Office clerk’s pay for the semimonthly period = regular salary of $750.00 + overtime pay of $51.92 = $801.92

Please let us know how we can improve this explanation

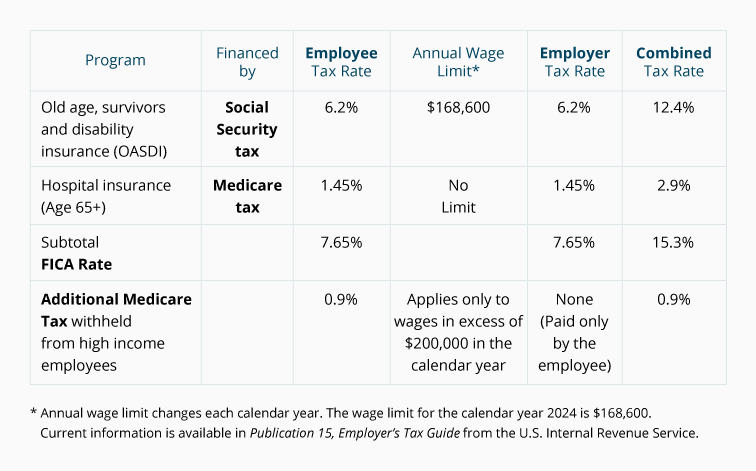

No ThanksFederal Insurance Contributions Act (FICA)

An important part of U.S. payroll accounting involves the Federal Insurance Contributions Act (FICA), which consists of two federal programs:

- Old age, survivors and disability insurance (OASDI) which is financed by the Social Security tax

- Hospital insurance for people age 65 and older which is financed by the Medicare tax

The Social Security taxes and the Medicare taxes come from the following:

- Employees through payroll deductions/withholdings, and

- Employers who must pay an amount similar to the amount withheld from employees’ gross pay. (The amount owed by the employer will be slightly less when an employee earns more than $200,000 in a calendar year.)

Summary of FICA’s effect on a company’s payroll processing:

Examples using the above table:

-

An employee with wages of $100,000 will have FICA payroll withholdings amounting to $7,650 ($6,200 of Social Security tax + $1,450 of Medicare tax). In addition, the employer will have FICA expense of $7,650 ($6,200 of Social Security tax + $1,450 of Medicare tax). As a result, the employer must remit $15,300 to the U.S. Treasury.

-

An employee with wages of $170,000 will have Social Security tax withholdings of $10,453.20 ($168,600 x 6.2%) + Medicare tax withholdings of $2,465.00 ($170,000 x 1.45%). The employer must match the amounts and remit $25,836.40 ($10,453.20 + $10,453.20 + $2,465.00 + $2,465.00).

-

An employee with wages of $300,000 will have Social Security tax withholdings of $10,453.20 ($168,600 x 6.2%) + Medicare tax withholdings of $4,350 ($300,000 x 1.45%) + Additional Medicare Tax withholdings of $900 ($100,000 x 0.9%). The employer must match the employee’s amounts except for the Additional Medicare Tax and remit $30,506.40 ($10,453.20 + $10,453.20 + $4,350.00 + $4,350.00 + $900).

Please let us know how we can improve this explanation

No Thanks