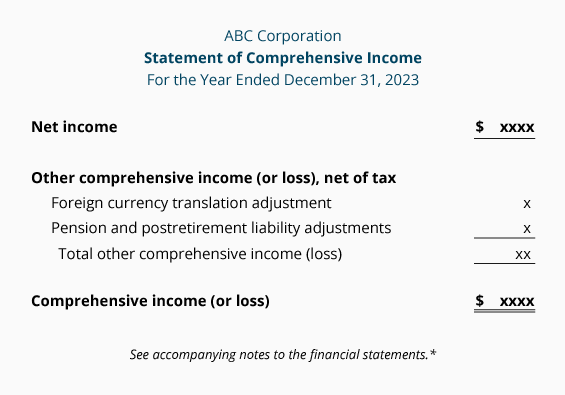

Statement of Comprehensive Income

The statement of comprehensive income should be presented immediately after the income statement. (However, it could be combined with the income statement.)

The term comprehensive income consists of 1) a corporation’s net income (which is detailed on the corporation’s income statement), and 2) a few additional items which make up what is known as other comprehensive income.

The items which make up other comprehensive income include:

- Unrealized gains or losses on derivatives used in hedging

- Unrealized gains or losses on pension and postretirement liabilities

- Foreign currency translation adjustments

The amounts of these other comprehensive income adjustments (positive or negative) are not included in the corporation’s net income, income statement, or retained earnings. Instead the adjustments are reported as other comprehensive income on the statement of comprehensive income and will be included in accumulated other comprehensive income (which is a separate item within stockholders’ equity).

The following shows the format of the statement of comprehensive income:

*Every financial statement should inform the reader that the notes are an integral part of the financial statements and should be read for important information.

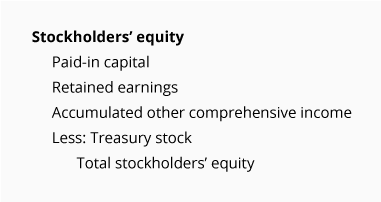

The adjustments for the items defined as other comprehensive income will be included in the amount of accumulated other comprehensive income, which is reported in the stockholders’ equity section of the balance sheet:

You can learn more about other comprehensive income by referring to an intermediate accounting textbook.

Please let us know how we can improve this explanation

No Thanks