Introduction

In this topic you will learn about the five financial statements that a U.S. corporation should include when it distributes its annual financial statements to anyone outside of the corporation. The five financial statements are:

- Income statement

- Statement of comprehensive income

- Balance sheet

- Statement of stockholders’ equity

- Statement of cash flows

The annual financial statements should also include notes to the financial statements. The notes (which are to be referenced on each financial statement) disclose important information regarding the amounts appearing or not appearing on the financial statements.

The financial statements that are distributed by a U.S. corporation must comply with the common rules known as generally accepted accounting principles or GAAP or US GAAP. If the corporation’s stock is traded on a stock exchange, the corporation is also required to comply with the reporting requirements of the Securities and Exchange Commission (SEC), an agency of the U.S. government.

It is important to understand that most of the amounts contained in the financial statements resulted from recording past transactions. Hence the amounts may not be relevant for future decisions and will not indicate the corporation’s fair market value.

WATCH NOW

Advance Your Career with Our PRO Training

Where the Amounts Come From

Generally, the amounts reported on the financial statements originated from the corporation’s business transactions that were recorded and stored in the general ledger accounts. The accounting records are often referred to as the corporation’s books.

In addition to recording the business transactions, accountants will also record adjusting entries before issuing the financial statements. The following are three examples of why adjusting entries are necessary:

-

Some of the transaction amounts that were recorded pertain to more than one accounting period. (An accounting period could be a year, quarter, month, 13 weeks, etc.) An adjusting entry is necessary so that only the pertinent amounts appear in each period’s financial statements.

To illustrate, let’s assume that a corporation purchased an asset for $60,000 that is expected to be used in the business for 60 months. If the corporation issues monthly financial statements, an adjusting entry will be necessary so that each income statement will report a monthly expense of $1,000 ($60,000 of cost divided by the useful life of 60 months). The adjusting entry will also cause the asset section of the balance sheet to decrease by $1,000 per month.

-

Some expenses may occur so late in an accounting period that they were not processed and recorded in the general ledger accounts. In order for these expenses and related obligations to be included in financial statements, the accountant will record accrual-type adjusting entries. (Similarly, an adjusting entry may be required if revenues were earned, but were not yet recorded.)

- US GAAP will likely require additional adjusting entries. Two examples include:

- an adjustment for uncollectible accounts receivable

- an adjustment for some marketable securities where the fair market value has changed

To learn more about recording adjustments, visit our Adjusting Entries Explanation.

Accrual Method of Accounting

The adjusting entries we mentioned are needed to comply with the accrual method (or basis) of accounting, which is required for most corporations. (Individuals and very small companies may be allowed to use the cash basis of accounting.)

Under the accrual method of accounting the financial statements will report sales and receivables when products or services have been delivered (as opposed to reporting sales when the corporation receives money from its customers). It also means that expenses and liabilities will be reported on the financial statements when they occur (as opposed to reporting expenses when the corporation remits payment).

The accrual method of accounting results in more complete and accurate financial statements than the cash method of accounting for the following reasons:

- All of the revenues that were earned during the accounting period will be included

- All of the expenses that were incurred during the accounting period will be included

- All of the assets as of the end of the accounting period will be included

- All of the liabilities as of the end of the accounting period will be included

When the accrual method of accounting is used, you will see the following balance sheet accounts:

Accounting Periods

A corporation is required to issue annual financial statements, but it is common for a corporation to prepare monthly financial statements for its management. Financial statements issued between the annual financial statements are known as interim financial statements. Interim financial statements could be prepared for periods such as one month, four weeks, three months, 13 weeks, eight months, eleven months, etc.

Many corporations have accounting years that begin on January 1 and end on December 31. This one-year period of time (or time interval) is referred to as a calendar year. A calendar year corporation will have quarterly accounting periods that end on March 31, June 30, September 30, and December 31.

Some U.S. corporations have accounting years that end on a date other than December 31. For example, a corporation could have an accounting year that begins on July 1 and ends on the following June 30. Another corporation might have an accounting year that begins on October 1 and ends on September 30. These are known as fiscal years.

Some U.S. corporations have a fiscal year that is based on weeks instead of months. For example, some large U.S. retailers have fiscal years consisting of the 52 or 53 weeks ending on the Saturday nearest to January 31. Hence, their fiscal year could begin on a Sunday (such as February 3) and end 52 weeks later on a Saturday (such as February 1).

The benefit of having a fiscal year is that it will coincide with the business year. A retailer will have a fiscal year ending four or five weeks after the peak holiday sales of December so that its net sales and net income will reflect the merchandise that was sold in December but was returned in January.

Users of the Financial Statements

The financial statements issued by a U.S. corporation and distributed outside of the corporation could find their way into the hands of the following people and/or organizations:

- current stockholders

- current lenders

- financial analysts

- potential future investors

- potential future lenders

- current and future suppliers of goods or services

- certain customers

- government agencies

- labor unions

- competitors and others

The users often compare a corporation’s financial statements to those of 1) previous accounting periods, and 2) other companies. Therefore, for the financial statements to be useful they must consistently follow common reporting rules. In the U.S. these common rules are referred to as generally accepted accounting principles or GAAP or US GAAP. US GAAP includes basic underlying guidelines such as the historical cost principle, revenue recognition, going concern, full disclosure, industry practices, plus some very detailed reporting requirements for leases, pensions, investment securities, hedging activities, and other complex financial transactions. The task of researching and developing US GAAP is carried out by the non-government organization Financial Accounting Standards Board or FASB (pronounced “faz-bee”).

US GAAP requires that when the annual financial statements are distributed outside of the corporation they must include all five of the following financial statements (including the notes to the financial statements):

- Income statement

- Statement of comprehensive income

- Balance sheet

- Statement of stockholders’ equity

- Statement of cash flows

Income Statement

The income statement reports a corporation’s net income for the period of time indicated in its heading. The income statement is also known as the following:

- Statement of income

- Statement of earnings

- Statement of operations

- Profit and loss statement

- P&L

The following is a condensed version of an income statement for a regular corporation that sells products:

*The period of time could be a year, quarter, month, 13 weeks, eight months, etc.

**The earnings per share must be reported if a corporation’s shares of stock are traded on a stock exchange.

***Every financial statement should inform the reader that the notes are an integral part of the financial statements and should be read for important information.

Amounts on the Income Statement

The historical cost principle means that most of the amounts shown on the income statement reflect a corporation’s vast number of actual transactions that occurred with parties outside of the corporation. Most of the transactions were routinely recorded by the accounting system, but some additional amounts were included through adjusting entries.

Revenues

Revenues are the amounts earned by a corporation through its main activities such as:

- Selling products. These are reported as net sales, net product revenue, revenues from net sales, revenues, etc.

- Providing services. These are likely reported as net service revenues or revenues.

Under the accrual method of accounting, revenues are reported on the income statement in the accounting period in which they are earned (and there is a reasonable assurance that the amounts will be collected). The revenues (and the related assets) are likely captured at the time that the sales invoice is prepared. At the end of the accounting period, accountants will also prepare adjusting entries for revenues that were earned but were not yet fully processed through the accounting system.

(Keep in mind that under the accrual method of accounting the term revenues is different from cash receipts.)

Expenses

Expenses are the historical costs that are associated with a corporation’s main business activities, and are reported on the income statement. Examples of a retailer’s expenses include:

- The cost of the merchandise (or goods) that it had sold

- Sales commissions that its employees and agents earned

- Ads that ran

- Store rent

- Other costs that had occurred or were used up during the accounting period

Under the accrual method of accounting, expenses will be reported on the income statement when they are best matched with 1) the revenues, or 2) the accounting period. The following are four ways in which costs will end up as expenses on the income statement:

-

When they best match revenues. The cost of goods sold and sales commission expense should be reported in the same period as the related sales are reported.

-

When they have expired or were used. The $400,000 cost of a building that is expected to be used for 40 years will often be reported as annual depreciation expense of $10,000.

-

When they have no future value which can be measured. The current year’s $50,000 advertising campaign will be reported as an expense on the current year’s income statement. The reason is that the future value of the current year’s ads cannot be determined.

-

When costs are too small to justify allocating them to future periods. As an example, the entire $300 cost of a paper shredder will be expensed immediately even though it is expected to be used for several years.

Gains and Losses

If a corporation disposes of an asset that is no longer used in its business, the amount received should not be included in its sales revenues. Instead a gain or loss on the disposal is recorded.

For example, if a florist sells its old delivery van, the amount received is not included in its sales revenues. The reason is its main business activities involve buying and selling floral products (not buying and selling delivery vehicles).

Hence, if a florist receives $2,000 for its old delivery van and the accounting records show that the van has a carrying value of $1,500 the income statement will report a gain on sale of assets of $500. If the florist receives only $1,300 the income statement will report a loss on sale of assets of $200.

Gross Profit

An important metric that is available from the income statement of a retailer or manufacturer is the gross profit. Gross profit is defined as net sales minus the cost of goods sold. Therefore, a corporation with net sales of $1,000,000 and cost of goods sold of $800,000 will have a gross profit of $200,000. Its gross margin or gross profit percentage is 20% of net sales ($200,000 divided by $1,000,000).

The gross margin or gross profit percentage is monitored by the readers of the financial statements to determine if the corporation was able to maintain the usual percentage during periods when its product costs had increased. This is important because the corporation’s gross profit amount must be sufficient to cover its selling, general and administrative (SG&A) expenses and to provide a sufficient amount of net income.

Net Income

A corporation’s net income is often referred to as the bottom line of the income statement. In other words, net income is the amount remaining after all of the corporation’s expenses, gains, and losses are considered. Depending on the industry, the net income as a percentage of net sales is often a very small percentage, such as 3% to 5% of net sales.

Net Income’s Impact on Retained Earnings and Comprehensive Income

The positive net income reported on the income statement also causes an increase in the corporation’s retained earnings (a component of stockholders’ equity). A negative net income (a net loss) will cause a decrease in retained earnings. This provides a link between a corporation’s income statement and its balance sheet.

Net income is also one component of a corporation’s comprehensive income. The other component is other comprehensive income, which will be discussed shortly.

Earnings Per Share (EPS)

When a corporation’s shares of stock are publicly traded, the income statement must display the earnings per share of common stock or EPS.

The number of shares of common stock is the weighted-average number of common shares that were outstanding during the accounting period. Therefore, if a corporation repurchases some of its shares of stock, the number of shares outstanding will decrease and the earnings per share will likely increase.

Income Statement Amounts are History

The historical cost principle means that most of the expenses reported on the income statement are the actual costs from past transactions. For instance, the expensing of a building with an actual historical cost of $400,000 and a useful life of 40 years will mean that the annual depreciation expense will average $10,000 per year. It also means that the total of the depreciation expense over the asset’s useful life cannot exceed $400,000. This means that in the 41st year of the building’s life the depreciation expense will be $0. This will be the case even if the building’s market value increased to $2 million or more.

If a competitor constructs a similar building close to the 41st year at a cost of $2,000,000 the competitor’s annual depreciation expense will be $50,000 per year ($2,000,000/40 years). Hence, the depreciation expense for older assets is not indicative of the economic capacity being used. (This is why accountants say “depreciation is an allocation process, not a valuation process”.)

Similarly, the sales revenues reported on the income statement reflect the past selling prices and past quantities. Current and future selling prices could be higher or lower than the past selling prices.

You can learn more by visiting our Income Statement Explanation.

Statement of Comprehensive Income

The statement of comprehensive income should be presented immediately after the income statement. (However, it could be combined with the income statement.)

The term comprehensive income consists of 1) a corporation’s net income (which is detailed on the corporation’s income statement), and 2) a few additional items which make up what is known as other comprehensive income.

The items which make up other comprehensive income include:

- Unrealized gains or losses on derivatives used in hedging

- Unrealized gains or losses on pension and postretirement liabilities

- Foreign currency translation adjustments

The amounts of these other comprehensive income adjustments (positive or negative) are not included in the corporation’s net income, income statement, or retained earnings. Instead the adjustments are reported as other comprehensive income on the statement of comprehensive income and will be included in accumulated other comprehensive income (which is a separate item within stockholders’ equity).

The following shows the format of the statement of comprehensive income:

*Every financial statement should inform the reader that the notes are an integral part of the financial statements and should be read for important information.

The adjustments for the items defined as other comprehensive income will be included in the amount of accumulated other comprehensive income, which is reported in the stockholders’ equity section of the balance sheet:

You can learn more about other comprehensive income by referring to an intermediate accounting textbook.

Balance Sheet

The balance sheet, which is also known as the statement of financial position, reports a corporation’s assets, liabilities, and stockholders’ equity account balances as of a point in time. The point in time is often the final instant or moment of the accounting period. Hence it is common for a balance sheet to report a corporation’s amounts as of the final instant of December 31.

An interesting point concerning the balance sheet accounts is that the account balances at the final instant of an accounting year will carry forward to become the beginning balances of the subsequent year. (The other four financial statements report amounts for a period of time.)

The format of the balance sheet is similar to the accounting equation:

Assets = Liabilities + Stockholders’ Equity

As result of the double-entry system of accounting, the balance sheet and the accounting equation should always be in balance. Here are a few examples:

-

When a corporation borrows money from its bank, 1) the corporation’s assets will increase, and 2) the corporation’s liabilities will increase.

-

When the corporation uses its cash to purchase land for a new warehouse, 1) the asset land increases, and 2) the asset cash decreases.

-

When a corporation earns $5,000 by providing consulting services, 1) the corporation’s assets (such as cash or accounts receivable) will increase, and 2) its stockholders’ equity (specifically retained earnings) will increase. Stockholders’ equity is increasing because revenues will cause an increase in the amount of net income, and the increase in net income causes an increase in retained earnings.

You can gain additional insights by visiting our Accounting Equation Explanation.

Assets

Assets are often described as:

- a corporation’s resources

- things the corporation owns (as a result of a previous transaction)

- costs that have not yet expired

Some of the accounts used to record a corporation’s assets include:

- Cash

- Marketable Securities

- Accounts Receivable

- Other Receivables

- Inventory

- Prepaid Expenses

- Long-term Investments

- Land

- Buildings

- Equipment

- Vehicles

- Patents

- and many others

Normally, the balance sheet will present the asset accounts under one of the following headings:

- Current assets

- Investments (long-term)

- Property, plant and equipment

- Other assets

Liabilities

Liabilities are often described as:

- a corporation’s obligations

- amounts the corporation owes

- customer deposits or customer prepayments which a corporation has not yet earned

- Sources (along with stockholders’ equity) of the corporation’s assets

- Claims against the corporation’s assets

Some of the accounts used to record liabilities include:

Liability accounts are usually presented on the balance sheet under one of the following headings:

Stockholders’ Equity

Stockholders’ equity (which is also known as shareholders’ equity) is defined as a corporation’s assets minus its liabilities. Stockholders’ equity can be viewed as:

- a residual claim on the corporation’s assets (after liabilities)

- a source (along with liabilities) of the corporation’s assets

The major components of stockholders’ equity include:

- Paid-in capital

- Retained earnings

- Accumulated other comprehensive income

- Treasury stock (a deduction)

Since the reported amounts for a corporation’s assets and liabilities reflect US GAAP (including the historical cost principle), the amount of stockholders’ equity does not indicate a corporation’s current market value. For example, valuable trademarks and brand names that a corporation developed internally are not reported as assets and therefore are not included in the amount of stockholders’ equity.

Stockholders’ equity will be discussed further under the Statement of Stockholders’ Equity.

Format of the Balance Sheet

The following shows the headings and classifications found in a classified balance sheet:

*Every financial statement should inform the reader that the notes are an integral part of the financial statements and should be read for additional important information.

Working Capital and Current Ratio

I believe that bankers will immediately calculate a corporation’s working capital when meeting with a loan applicant. Working capital is calculated as follows:

Working capital = current assets minus current liabilities

This means that a corporation with $100,000 of current assets and $100,000 of current liabilities has no working capital. If it has $150,000 of current assets and $100,000 of current liabilities, it has $50,000 of working capital.

Related to working capital, is the current ratio, which is calculated as follows:

Current ratio = current assets divided by current liabilities

Hence a corporation with $100,000 of current assets and $100,000 of current liabilities will have a current ratio of 1:1. If the corporation has $150,000 of current assets and $100,000 of current liabilities, its current ratio is 1.5:1.

The amount of working capital and the current ratio are indicators of a corporation’s ability to pay its obligations when they come due. These and other financial ratios can be found in our Financial Ratios Explanation.

Current assets include cash and the assets that will turn to cash within one year of the balance sheet date (or within the operating cycle, if it is longer than one year). In other words, current assets include:

- Cash

- Cash equivalents

- Temporary investments

- Accounts receivable (net of the allowance for uncollectible accounts)

- Inventory

- Prepaid expenses

Current liabilities are a corporation’s obligations that are due within one year of the balance sheet date (or within the operating cycle, if it is longer than one year) and will require the use of a current asset or will create another current liability. The following are examples of current liabilities:

- Accounts payable

- Wages payable

- Payroll withholdings that need to be remitted

- Bank loans and other borrowings due within a year

- Principal portion of long-term loans (the principal that must be paid within the next 12 months)

- Customer deposits

- Unearned/deferred revenue

- Income taxes payable

For more information and a more complete balance sheet visit our Balance Sheet Explanation.

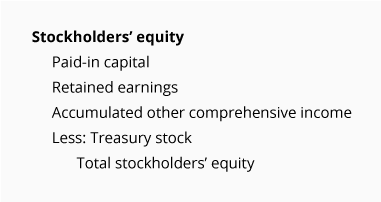

Statement of Stockholders’ Equity

The financial statement that lists the components of stockholders’ equity, their balances, and the changes that occurred during an accounting year is also known by the following titles:

- Statement of stockholders’ equity

- Statement of shareholders’ equity

- Statement of changes in stockholders’ equity

- Statement of changes in shareholders’ equity

The major components and headings in the statement of stockholders’ equity include:

Paid-in capital – common stock

Paid-in capital – excess of par value

Retained earnings (or accumulated deficit when negative)

Accumulated other comprehensive income (or loss)

Treasury stock (an amount that is a subtraction)

A common format of the statement of stockholders’ equity is shown here:

To see a more comprehensive example, we suggest an Internet search for a publicly-traded corporation’s Form 10-K.

Statement of Cash Flows (SCF)

The statement of cash flows (SCF) or cash flow statement reports a corporation’s significant cash inflows and outflows that occurred during an accounting period. This financial statement is needed because many investors and financial analysts believe that “cash is king” and cash amounts are required for various analyses. The SCF is necessary because the income statement is prepared using the accrual method of accounting (as opposed to the cash method).

The statement of cash flows highlights the major reasons for the changes in a corporation’s cash and cash equivalents from one balance sheet date to another. For example, the SCF for the year 2025 reports the major cash inflows and cash outflows that caused the corporation’s cash and cash equivalents to change between December 31, 2024 and December 31, 2025.

The cash inflows are the cash amounts that were received and/or have a favorable effect on a corporation’s cash balance. Hence, they will appear on the SCF as positive amounts.

The cash outflows are the cash amounts that were used and/or have an unfavorable effect on a corporation’s cash balance. Hence, these amounts will appear in parentheses to indicate that they had a negative effect on the cash balance.

The major cash flows occurring during an accounting period are reported under the following headings or sections of the SCF:

- Cash flows provided or used in operating activities

- Cash flows provided or used in investing activities

- Cash flows provided or used in financing activities

In addition, the following supplementary or supplemental information must be disclosed:

- Interest paid

- Income taxes paid

- Significant amounts involving investing and/or financing activities that did not involve cash (such as the exchange of common stock for long-term debt, or the exchange of common stock for land)

Cash Flows from Operating Activities

The first section of a SCF is described as the cash flows from operations or cash flows from operating activities. The following is an example of the cash flows from the operating activities section prepared using the indirect method, which is used by nearly all corporations:

Under the indirect method, the first amount shown is the corporation’s net income (or net earnings) from the income statement. Assuming the net income was $100,000 it is listed first and is followed by many adjustments to convert the net income (computed under the accrual method of accounting) to the approximate amount of cash.

The first adjustment to the net income is the amount of depreciation expense that had reduced net income. Assuming the depreciation expense was $30,000, this amount will be added back to the net income. The reason is that it was an expense that did not use cash. (It was merely an adjusting entry that debited Depreciation Expense and credited Accumulated Depreciation.)

Many of the other adjustments in the operating activities section of the SCF reflect the changes in the balances of the current assets and current liabilities. For example, if accounts receivable decreased by $5,000, the corporation must have collected more than the current period’s credit sales that were included in the income statement. Since the decrease in the balance of accounts receivable is favorable for the corporation’s cash balance, the $5,000 decrease in receivables will be a positive amount on the SCF.

If accounts payable decreased by $9,000 the corporation must have paid more than the amount of expenses that were included in the income statement. Paying more than the amount in the income statement is unfavorable for the corporation’s cash balance. As a result the $9,000 decrease in accounts payable will appear in parentheses on the SCF.

Experienced financial people will review the net cash provided from operating activities. If there are negative amounts, they will ask “Why?” For instance, if inventory increases, the amount of the increase will be shown as a negative amount on the SCF since it assumed to have used the corporation’s cash. The negative amount may lead to the question “Was there a decline in the demand for the corporation’s products?” Perhaps some of the corporation’s items in inventory have become obsolete.

You can gain additional insights regarding the cash flows from operating activities from our Cash Flow Statement Explanation.

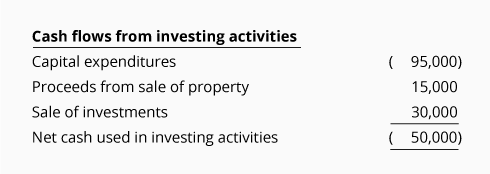

Cash Flows from Investing Activities

The second section of the SCF reports 1) the cash outflows that were used to acquire noncurrent assets, and 2) the cash inflows received from the sale of noncurrent assets.

The cash outflows spent to purchase noncurrent assets are reported as negative amounts since the payments have an unfavorable effect on the corporation’s cash balance. A common outflow is connected to a corporation’s capital expenditures. This is the property, plant and equipment that will be used in the business and was acquired during the accounting period.

The positive amounts in this section of the SCF indicate the cash inflows or proceeds from the sale of property, plant and equipment and/or other long-term assets.

Here is an example of what might be reported in the second section of the statement of cash flows:

Note that the $95,000 appears as a negative amount because the outflow of cash for capital expenditures has an unfavorable or negative effect on the corporation’s cash balance. The $15,000 is a positive amount since the money received has a favorable effect on the corporation’s cash balance. The $30,000 received from selling an investment also had a favorable effect on the corporation’s cash balance.

Cash Flows from Financing Activities

The third section of the statement of cash flows reports the cash received when the corporation borrowed money or issued securities such as stock and/or bonds. Since the cash received is favorable for the corporation’s cash balance, the amounts received will be reported as positive amounts on the SCF.

Cash outflows used to repay debt, to retire shares of stock, and/or to pay dividends to stockholders are unfavorable for the corporation’s cash balance. As a result the amounts paid out will be shown as negative amounts.

Here is an example of what might appear in the third section of the statement of cash flows:

In the above example we see that the payment of cash dividends of $10,000 had an unfavorable effect on the corporation’s cash balance. This is also true of the $20,000 of cash that was used to repay short-term debt and to purchase treasury stock for $2,000. On the other hand, the borrowing of $60,000 had a favorable or positive effect on the corporation’s cash balance. The net result of the four financing activities caused cash and cash equivalents to increase by $28,000.

Format of a Complete SCF

The following shows all three sections of the statement of cash flows:

Note that near the bottom of the SCF there is a reconciliation of the cash and cash equivalents between the beginning and the end of the year.

In addition, the SCF must disclose the following supplementary information: amount of interest paid, amount of income taxes paid, and significant noncash transactions such as the exchange of shares of stock for bonds payable, or common stock for land. Typically, these are disclosed in the notes to the financial statements.

Free Cash Flow

Some financial analysts also calculate what is known as free cash flow. This is defined as the amount of cash from operating activities minus the amount of cash required for capital expenditures. Some people also subtract the corporation’s cash dividends when the dividends are viewed as a necessity.

Using the amounts from above, the ABC Corporation had free cash flow of $31,000 (which is the $126,000 of net cash provided from operating activities minus the capital expenditures of $95,000). If dividends are considered a required cash outflow, the free cash flow would be $21,000.

Notes to Financial Statements

In addition to the amounts that are reported on the face of the financial statements, US GAAP requires that additional information be provided as notes to the financial statements. To alert the readers of these important disclosures, each financial statement is required to make reference to them. The following are some examples of the reference found at the bottom of each financial statement:

- See accompanying notes.

- See accompanying notes to the financial statements.

- The accompanying notes are an integral part of these financial statements.

- The accompanying Notes to the Financial Statements are an integral part of this statement.

- See Notes to Consolidated Financial Statements.

The notes (or footnote disclosures) are required by the full disclosure principle because the amounts and line descriptions on the face of the financial statements cannot provide sufficient information. In fact, there may be some large potential losses that cannot be expressed as a specific amount, but they are critical information for lenders, investors, and others.

The notes usually begin with the corporation’s significant accounting policies. This note describes how revenues were recognized on the income statement, how inventory is accounted for, etc. Our review of the financial statements of 20 publicly-traded corporations showed notes on the following topics:

- Nature of business

- Investments

- Employee benefit plans

- Basis of consolidation

- Accounts receivable

- Pensions and postretirement health plans

- Use of estimates

- Inventories

- Fair value measurement

- Revenue recognition

- Property, plant and equipment

- Long-term debt and available credit

- Fiscal periods

- Goodwill and other intangible assets

- Commitments and contingencies

- Foreign currency translation

- Deferred compensation

- Stock options

- Business segments

- Leases

- Stock repurchase program

- Significant customers

- Impairment of long-lived assets

- Accumulated other comprehensive income

- Cash and cash equivalents

- Accrued liabilities

- Recent accounting pronouncements

Sophisticated investors and lenders will read closely the notes to the financial statements. If the corporation’s shares of stock are publicly traded, they will also read the additional information presented in the corporation’s Annual Report to the Securities and Exchange Commission, Form 10-K.

Other Information Pertaining to Financial Statements

Consolidated Financial Statements

It is common for a large business to consist of several legal corporations. However, those separate legal corporations (called subsidiaries) are owned and controlled by one of the corporations (the parent corporation). The shares of common stock of the parent corporation are often traded on a major stock exchange. Those stockholders are interested in receiving financial statements which report the results and financial position of the entire economic entity, which is all of the subsidiaries and the parent corporation.

The consolidated financial statements report the results of the transactions that occurred between the economic entity and its customers, suppliers, and others outside of the economic entity. For example, the consolidated income statement will report the sales made to customers who are outside of the economic entity. (The sales and the related purchases made between the subsidiaries and between the subsidiaries and the parent corporation are not included.)

Similarly, a consolidated balance sheet reports the amounts owed to lenders outside of the economic entity. (The loans and borrowings between subsidiaries and between the subsidiaries and the parent corporation are not included.)

In the review of 20 corporations whose stock was traded on a major stock exchange, all of the corporations had:

- Consolidated income statements

- Consolidated statements of comprehensive income

- Consolidated balance sheets

- Consolidated statements of stockholders’ equity

- Consolidated statements of cash flows

- Notes to the consolidated financial statements

Comparative Financial Statements

When a financial statement reports the amounts for the current year and for one or two additional years, the financial statement is referred to as a comparative financial statement. For example, the income statement of a large corporation with its shares of stock traded on a stock exchange might have as its heading “Consolidated Statements of Income” and will report the amounts for 2025, 2024, and 2023. This allows the user to compare sales that occurred in 2025 to the sales that occurred in 2024 and in 2023.

The balance sheet of the same corporation will have as its heading “Consolidated Balance Sheets” and will report the amounts as of the final instant as of December 31, 2025 and the final instant as of December 31, 2024.

Audited Financial Statements

Some corporations may be required to have their external financial statements audited. This requires independent certified public accountants to provide assurance that the financial statements present fairly the financial position, results of operations, and cash flows of the corporation according to US GAAP.

If a corporation’s stock is not traded on a stock exchange and no one requires audited financial statements, the financial statements do not have to be audited. (Corporations with its stock trading on a stock exchange must have its financial statements audited by a registered firm of independent CPAs.)

Publicly-Traded Corporations

When a U.S. corporation’s shares of stock are traded on a stock exchange, we say that the shares are publicly traded or publicly held. We also refer to the corporation as a publicly-traded corporation.

In addition to US GAAP the external financial statements of a publicly-traded U.S. corporation must comply with the reporting requirements of the U.S. government agency, Securities and Exchange Commission (SEC). Among the many required reports is the Annual Report to the SEC, Form 10-K. The Form 10-K must include audited, comparative financial statements.

Typically, the large, publicly-held corporations will be issuing consolidated financial statements. Examples of the headings are shown below. (In parentheses we show the number of years for which amounts will appear.)

- Consolidated statements of income (3 years)

- Consolidated statements of comprehensive income (3 years)

- Consolidated balance sheets (end-of-year amounts for 2 years)

- Consolidated statements of stockholders’ equity (3 years)

- Consolidated statements of cash flows (3 years)

- Notes to the consolidated financial statements

Since the corporation’s shares of stock are publicly traded, the consolidated financial statements must be audited by a registered firm of independent certified public accountants.

Other parts of Form 10-K include Management’s Discussion and Analysis of Financial Condition and Results of Operations, as well as a certification by management on the corporation’s internal controls, a statement of management’s responsibility for the financial statements, disclosures of risk, legal proceedings, and more.

In addition to the annual consolidated financial statements, the publicly-held corporation will issue quarterly consolidated financial statements. These are referred to as interim financial statements and will be more condensed (fewer details), reviewed by the registered CPA and will be part of the corporation’s Quarterly Report to the Securities and Exchange Commission (Form 10-Q).

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Financial Statements materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.

Earn Our Certificate

for This Topic

When you join PRO, you will receive instant access to 16 different Certificates of Achievement plus our Bookkeeping Certificate of Excellence.

View PRO Features