Variable Manufacturing Overhead: Standard Cost, Spending Variance, Efficiency Variance

Manufacturing overhead costs refer to the costs within a manufacturing facility other than direct materials and direct labor. Manufacturing overhead includes items such as indirect labor, indirect materials, utilities, quality control, material handling, and depreciation on the manufacturing equipment and facilities, and more.

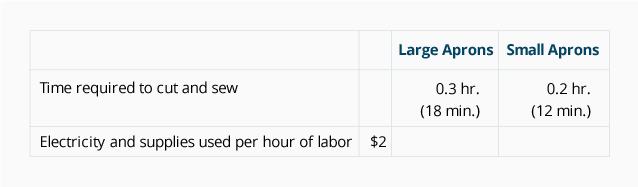

Variable manufacturing overhead costs will increase in total as output increases. An example is the cost of the electricity needed to operate the machines that cut and sew the denim. Another example is the cost of the manufacturing supplies (such as needles and thread) that increase when production increases. We will assume that these variable manufacturing overhead costs fluctuate in response to the number of direct labor hours. Recall the following information in our Standards Table in Part 1.

January 2023

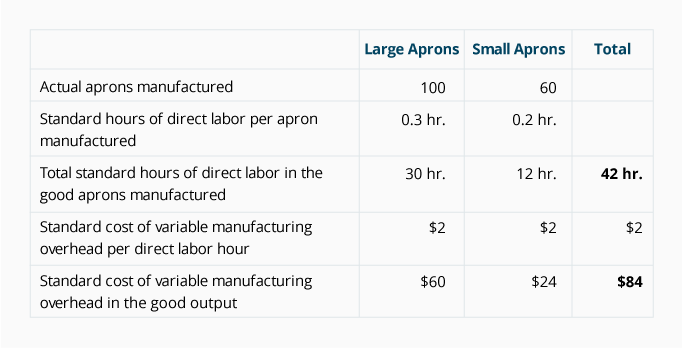

Let’s begin by determining the standard cost of variable manufacturing overhead for DenimWorks’ good output in January 2023:

Recall that there were 50 actual direct labor hours in January. Now let’s assume that the actual cost for the variable manufacturing overhead (electricity and manufacturing supplies) during January was $90.

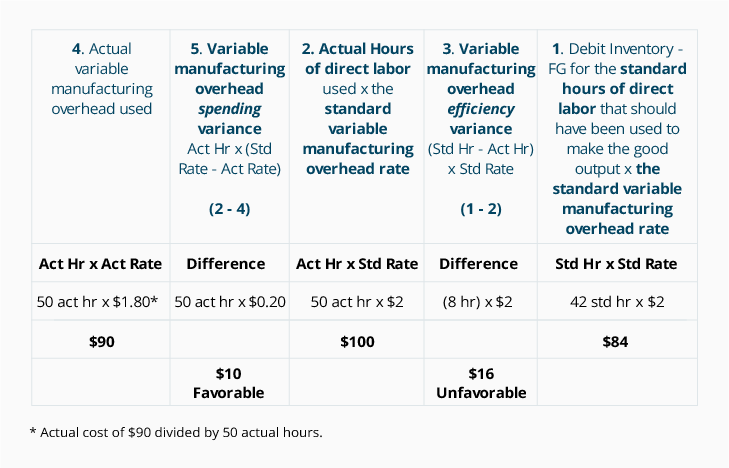

Based on the above information, our analysis will look like this:

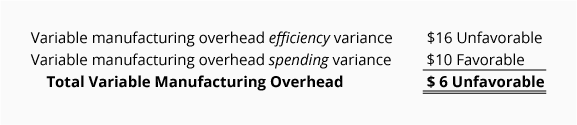

Variable Manufacturing Overhead Analysis for January 2023:

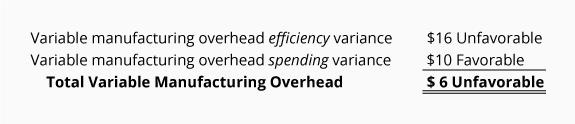

Notice that for the good output produced in January, the actual cost of variable manufacturing overhead was $90 and the total standard cost of variable manufacturing overhead cost for the good output was $84. This unfavorable difference of $6 agrees to the sum of the two variances:

Variable Manufacturing Overhead Efficiency Variance

As our analysis shows, DenimWorks did not produce the good output efficiently since it used 50 actual direct labor hours instead of the 42 standard direct labor hours.

It is assumed that the additional 8 hours caused the company to use additional electricity and supplies. Measured at the originally estimated rate of $2 per direct labor hour, this amounts to $16 (8 hours x $2). As a result, this is an unfavorable variable manufacturing overhead efficiency variance.

Variable Manufacturing Overhead Spending Variance

In our previous analysis, item 2 shows that based on the 50 direct labor hours actually used, electricity and supplies could cost $100 (50 hours x $2 per hour) instead of the standard cost of $84. However, the actual cost of the electricity and supplies was $90, not $100. This $10 favorable variance indicates that the company did not spend the planned $2 per direct labor hour. (Perhaps electricity rates were lower than the rates anticipated when the standard costs were established.)

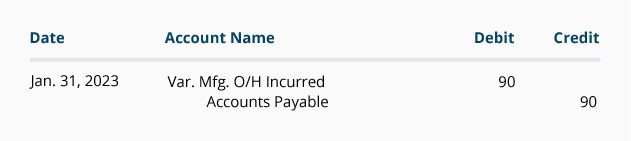

Actual variable manufacturing overhead costs are debited to overhead cost accounts. The credits are made to accounts such as Accounts Payable. For example:

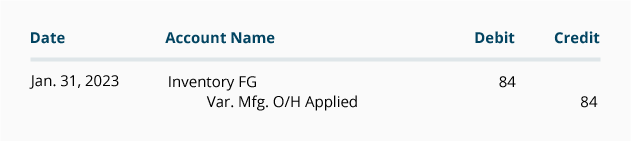

Another entry records how the overhead costs were assigned to the product based on the standard costs:

Our analysis and the journal entries illustrate that DenimWorks had actual variable manufacturing overhead of $90, but only $84 (the standard amount) was applied to the products. The $6 difference is “explained” by the two variances:

February 2023

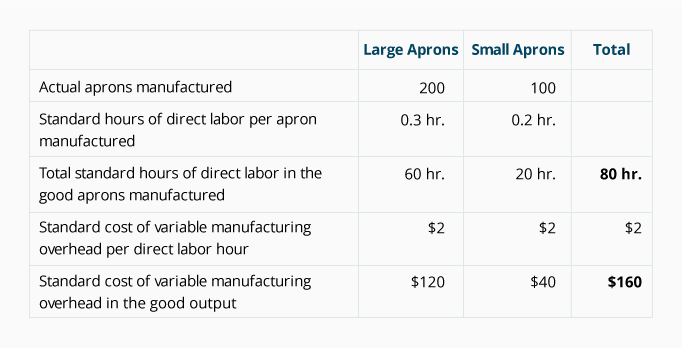

Recall that in February 2023 the company produced 200 large aprons and 100 small aprons. With that information we can compute the standard cost of variable manufacturing overhead for February 2023:

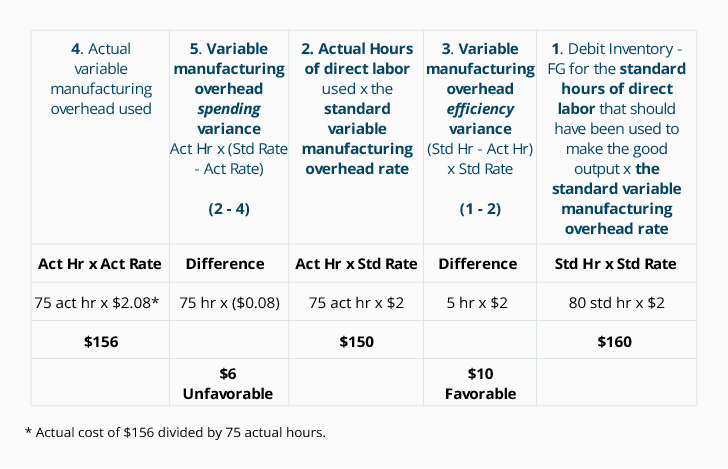

Given that there were 75 actual direct labor hours in February and assuming that the actual cost for the variable manufacturing overhead in February was $156, our analysis is:

Variable Manufacturing Overhead Analysis for February 2023:

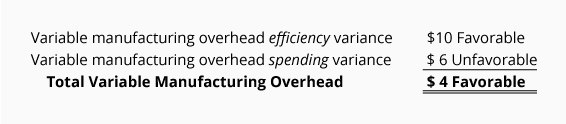

The favorable difference between the actual cost of $156 and the standard cost of $160 agrees with the sum of the following two variances:

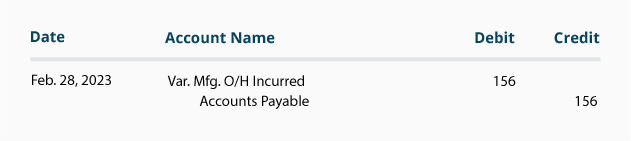

Actual variable manufacturing overhead costs are debited to overhead cost accounts. The credits are made to accounts such as Accounts Payable. For example:

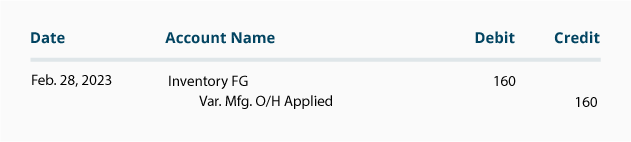

Another entry records how these overheads were assigned to the product:

As our analysis notes above and as these entries illustrate, even though DenimWorks had actual variable manufacturing overhead of $156, the standard amount of $160 was applied to the products. Accountants might say that for the month of February 2023, the company overapplied variable manufacturing overhead.

We will discuss how to report the balances in the variance accounts under the heading What To Do With Variance Amounts.

Please let us know how we can improve this explanation

No Thanks