Business Stories #5 — #8

Story #5: The Daily Grind—An Innovative Sales Channel

We continue with Bob’s situation from Story #4:

Instead of focusing on adding sales to the top line of the income statement, Bob’s accountant convinced him to focus on improving the bottom line. She said that Bob should put his energy into looking for modest amounts of profitable sales rather than large amounts of unprofitable sales. Bob did this by:

- reviewing his existing expenses by using a standard or benchmark (discussed in Story #6 below), and

- only adding sales when the related expenses are smaller than the sales.

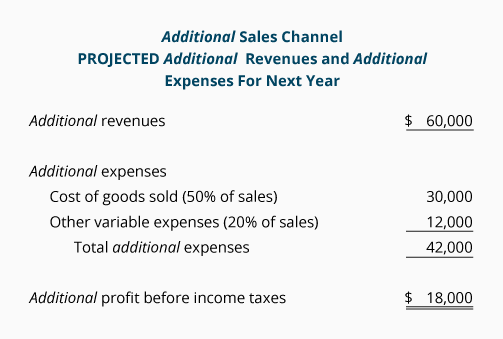

Bob identifies a way to sell his coffee and sandwiches using direct delivery rather than retail space. This new system will not involve additional rent since the products will be delivered from one of Bob’s existing locations. In fact, the only additional expenses for these sales will be the cost of the products (50% of sales value) and the expense of obtaining and delivering the orders (estimated to be 20% of sales). Bob believes he could also add a delivery fee to offset some of the delivery expense and to discourage small orders. Excluding the delivery fee revenues, Bob estimates that $60,000 of sales could be generated from this new sales channel.

With the help of his accountant, Bob prepares the following analysis focusing on additional revenues and expenses:

Bob was amazed to see that just a modest increase in sales could improve profits by $18,000. This is significantly different than the loss projected from opening an additional retail space discussed in Story #4. This profit improvement occurs because Bob did not have to add any fixed expenses. In short, this modest sales increase meant more profit, less stress, and less risk than adding another retail cafe.

Story #6: Nelson Manufacturing—Comparing Hours to the Industry Standard

Nelson Manufacturing is a small company staffed by two salaried employees and two hourly-paid employees. Sales fluctuate seasonally—the company is profitable during spring, summer, and early autumn, but the company suffers losses in late autumn and winter when sales drop off sharply and production declines. The company’s products are such that they cannot be stored for future sales.

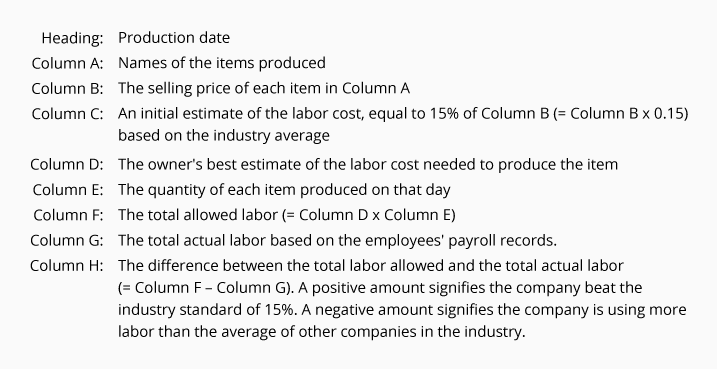

Susan Nelson, the owner, recently reviewed statistics from companies within the same industry as Nelson Manufacturing. The statistics show that on average the labor needed for producing an item equals 15% of its sales value. Susan is curious to compare her company’s labor cost as a percentage of sales to the industry standard. There is no time or money for an elaborate cost accounting study, so Susan’s accountant prepares a simple electronic worksheet to be filled in after each day’s actual production. The worksheet lists the following:

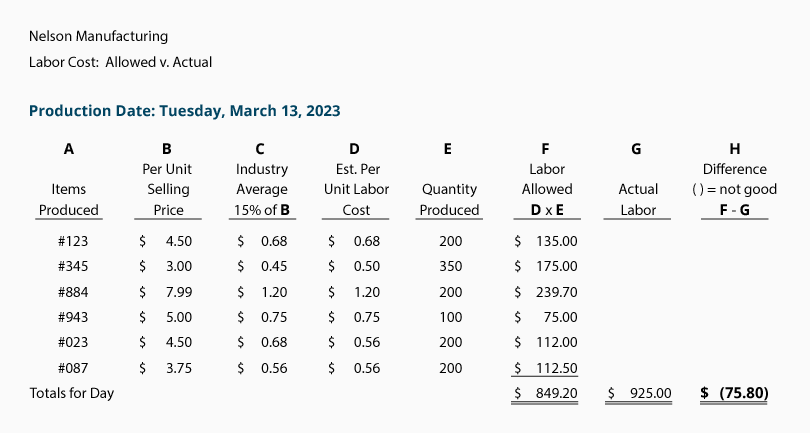

The worksheet for Nelson Manufacturing’s production of March 13 is shown here:

Each day a worksheet is prepared for the previous day’s production. Upon analysis, Susan realizes that her company is using more hours than the industry average to fill production orders. The company is paying workers for hours it does not need—hours that should be eliminated when production volume decreases. In effect, losses due to paying unnecessary wages in the slower months were eating up profits made in the busier months. In order to be competitive with the industry and avoid a net loss on the fall and winter income statements, Susan must immediately reduce worker hours whenever production volume declines.

The accountant explained to Susan that managing the relationship between payroll costs and output is not restricted to manufacturers—many retailers and service companies use part-time employees to work during the busiest hours of the day (or busiest seasons of the year) and then send them home from work when sales or customer counts are down. This is especially true for national companies whose stock is publicly traded—they want to meet earnings-per-share targets, and that will only happen if expenses are reduced when sales decline.

Story #7: Eastland Manufacturing—The Value of a Database

Eastland Manufacturing Company produces component parts for other manufacturers and employs forty people in its production department. Some employees are more productive than other employees, and some parts require more time to produce than other parts.

Eastland is asked to submit a bid (quote a price) for producing a new part similar to a component Eastland already produces (Part #3456). The preparation of the bid is greatly facilitated by Eastland’s computerized database which allows a manager to look up production records specific to Part #3456. Under the part number are entries for each time the part was produced, and each entry shows the number of parts produced, the hours spent producing the parts, the average number of parts produced per hour, and the employee that produced the parts. An average can be retrieved for any time period desired.

While this information is obviously valuable when preparing a bid for a new part, a database can also be useful in monitoring productivity. For example, a manager can use a database to more objectively review an employee’s productivity record—information that is helpful when determining productivity bonuses or deciding whether or not a recent hire should become a permanent employee.

Story #8: Strategies Other Than Cost Control

Improving profits is not limited to controlling costs—sometimes strategies such as better training for employees can reap significant rewards.

For example, one national retail chain electronically monitors the number of people entering each of its stores. Because its cash registers record the time of each sale, the retailer can determine—for any given time period—the percentage of people entering the store who actually make a purchase (the “conversion rate”). If a store has a low conversion rate, the employees are coached on better methods of engaging their customers, thereby increasing sales. This company realizes that a small increase in the conversion rate will result in a significant increase in sales. Since most of the store’s expenses are fixed for that short time period, the cost of the goods sold may be the only increase in expenses associated with the additional sales. The result will be a dramatic increase in profits.

Please let us know how we can improve this explanation

No Thanks