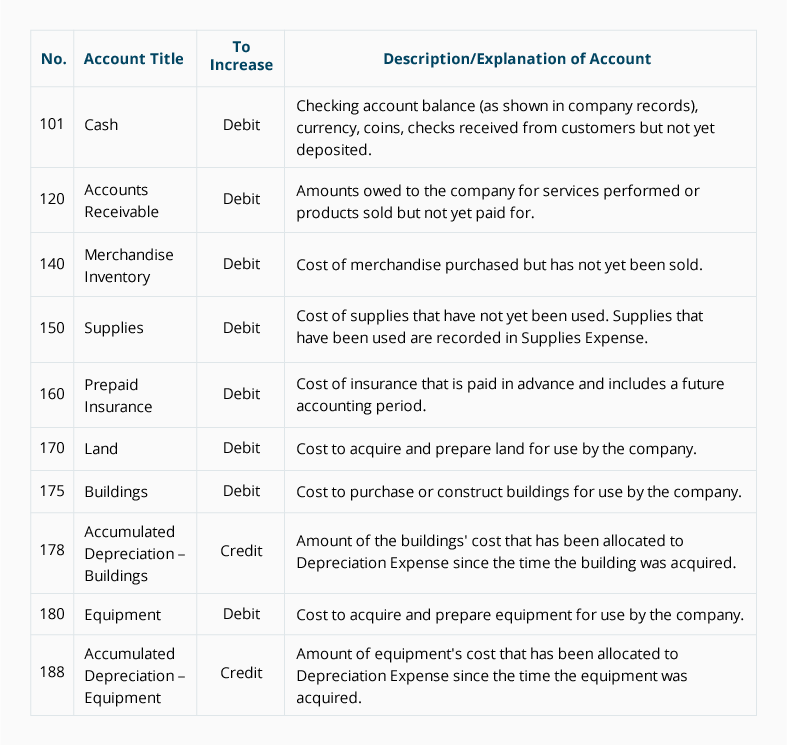

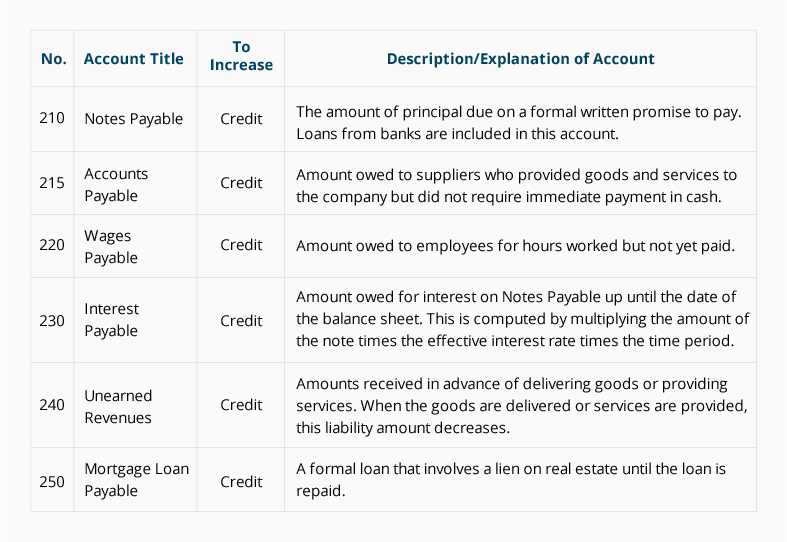

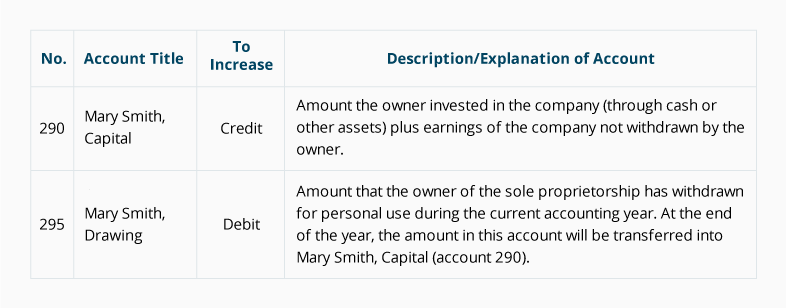

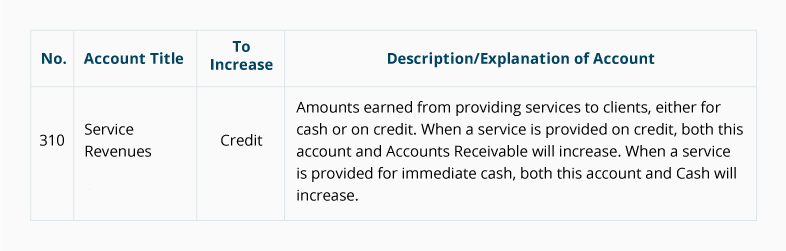

Sample Chart of Accounts for a Small Company

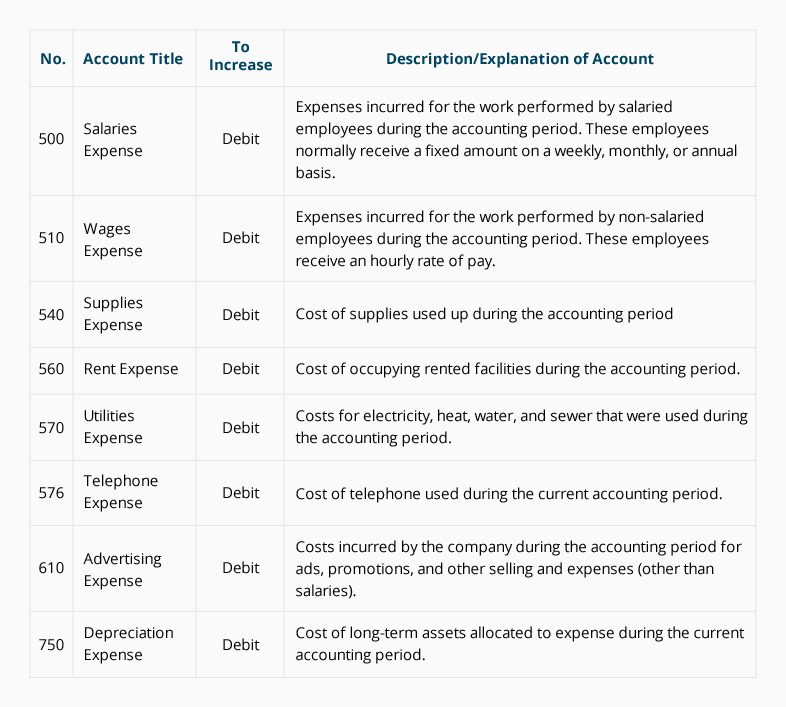

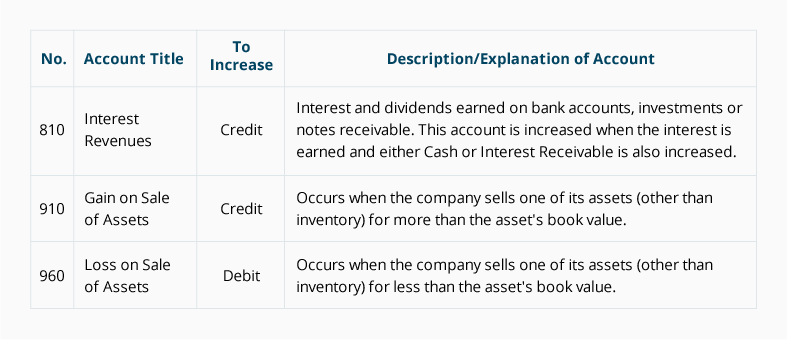

This is a partial listing of another sample chart of accounts. Note that each account is assigned a three-digit number followed by the account name. The first digit of the number signifies if it is an asset, liability, etc. For example, if the first digit is a “1” it is an asset, if the first digit is a “3” it is a revenue account, etc. The company decided to include a column to indicate whether a debit or credit will increase the amount in the account. This sample chart of accounts also includes a column containing a description of each account in order to assist in the selection of the most appropriate account.

Asset Accounts

Liability Accounts

Owner’s Equity Accounts

Operating Revenue Accounts

Operating Expense Accounts

Non-Operating Revenues and Expenses, Gains, and Losses

Accounting software frequently includes sample charts of accounts for various types of businesses. It is expected that a company will expand and/or modify these sample charts of accounts so that the specific needs of the company are met. Once a business is up and running and transactions are routinely being recorded, the company may add more accounts or delete accounts that are never used.

Please let us know how we can improve this explanation

No ThanksAt Least Two Accounts for Every Transaction

The chart of accounts lists the accounts that are available for recording transactions. In keeping with the double-entry system of accounting, a minimum of two accounts is needed for every transaction—at least one account is debited and at least one account is credited.

When a transaction is entered into a company’s accounting software, it is common for the software to prompt for only one account name—this is because the software is programmed to automatically assign one of the accounts. For example, when using accounting software to write a check, the software automatically reduces the asset account Cash and prompts you to designate the other account(s) such as Rent Expense, Advertising Expense, etc.

Some general rules about debiting and crediting the accounts are:

- Expense accounts are debited and have debit balances

- Revenue accounts are credited and have credit balances

- Asset accounts normally have debit balances

- To increase an asset account, debit the account

- To decrease an asset account, credit the account

- Liability accounts normally have credit balances

- To increase a liability account, credit the account

- To decrease a liability account, debit the account

To learn more about debits and credits, visit our Explanation of Debits and Credits and our Practice Quiz for Debits and Credits.

To learn more about the role of bookkeepers and accountants, visit our topic Accounting Careers.

Please let us know how we can improve this explanation

No Thanks