Company’s Process for Preparing its Bank Reconciliation

The process for preparing the bank reconciliation of a company’s checking account includes:

-

Identifying and reviewing any difference between every amount on the bank statement (or the online banking information) and every amount in the company’s Cash account.

-

Determining the true/correct/adjusted balance for the company’s Cash. This is done by listing the unadjusted balance from the bank statement, the unadjusted balance from the company’s Cash account, and then listing the adjustments (differences) that were identified.

-

Recording the pertinent adjustments to the company’s Cash account.

We suggest the following five steps for preparing a bank reconciliation:

Step 1. Compare every amount on the bank statement (or in the bank’s online information) with every amount in the company’s general ledger Cash account and note any differences.

-

Compare the amount of every check that was paid by the bank (cleared the bank account) with the amount of every check in the company’s Cash account. Any differences, such as the outstanding checks and errors, must be shown on the bank reconciliation.

-

Compare every deposit processed by the bank with the receipts recorded in the company’s Cash account. Any differences, such as a deposit in transit and/or errors, must be shown on the bank reconciliation.

-

Compare other items on the bank statement with the other items in the company’s Cash account. Any differences, such as bank fees, checks returned because of insufficient funds, collections made by the bank, etc., must be shown on the bank reconciliation.

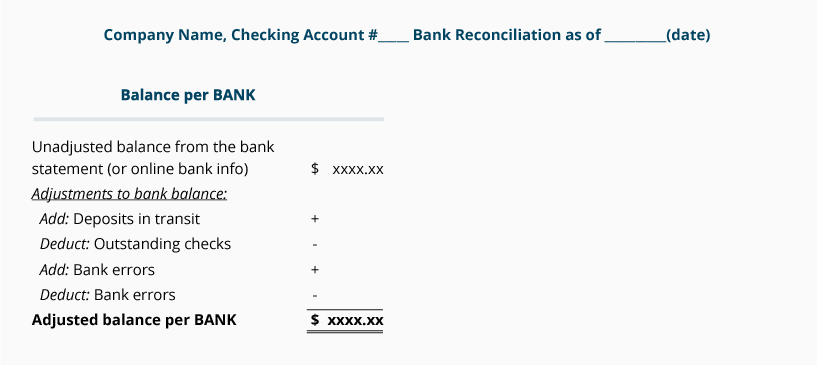

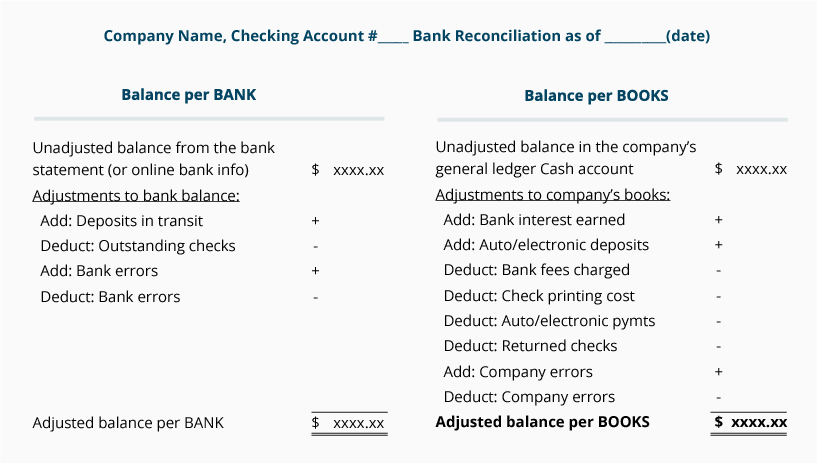

Step 2. Complete the Balance per BANK side of the bank reconciliation format.

The Balance per BANK side of the bank reconciliation requires the following:

-

Enter the unadjusted balance from the bank statement (or online banking information).

-

Add any deposits in transit. These are receipts in the company’s Cash account that have not been processed by the bank as of the date of the bank reconciliation.

-

Subtract any outstanding checks. These are the checks the company had issued and recorded in its Cash account, but they have not been paid by the bank (not cleared the bank account) as of the date of the bank reconciliation.

-

Add/subtract other items with amounts that were incorrectly recorded by the bank.

-

Combine the above amounts and show the total amount on the bottom line, Adjusted balance per BANK.

Here’s a Tip

Put the item where it isn’t.

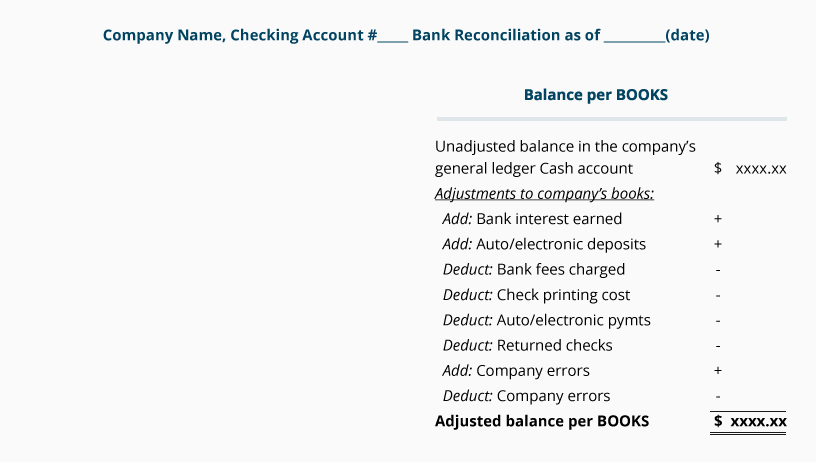

Step 3. Complete the Balance per BOOKS side of the bank reconciliation format.

The Balance per BOOKS side of the bank reconciliation requires the following:

-

Enter the unadjusted balance appearing in the company’s general ledger Cash account.

-

Add any increases (interest earned, bank credit memos) that are shown on the bank statement but were not yet recorded in the company’s Cash account.

-

Subtract any decreases (such as bank services charges, return items, bank debit memos) that are shown on the bank statement but are not yet recorded in the company’s Cash account.

-

Add/subtract other items with amounts that were incorrectly recorded by the company.

-

Combine the amounts on the right side and show the total on the bottom line, Adjusted balance per BOOKS.

Here’s a Tip

Put the item where it isn’t.

Step 4. Be certain that the bank reconciliation shows Adjusted balance per BANK = Adjusted balance per BOOKS.

The bottom line of both sides of the bank reconciliation must be the same amount. In other words, Adjusted balance per BANK must equal Adjusted balance per BOOKS.

Note: Having the Adjusted balance per BANK = Adjusted balance per BOOKS does not guarantee that the company’s cash has been completely accounted for. For instance, if an employee had stolen some of the company’s cash receipts before the money was recorded in the company’s accounts (and obviously not deposited in the company’s bank account) the missing amount will not be detected by the bank reconciliation.

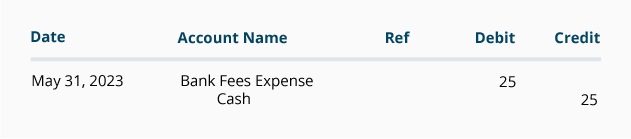

Step 5. Record in the company’s general ledger the adjustments to the balance per BOOKS.

Since the adjustments to the balance per the BOOKS have not been recorded as of the date of the bank reconciliation, the company must record them in its general ledger accounts.

For example, if one of the adjustments to the balance per BOOKS is a $25 service charge (that was on the bank statement on May 31, 2023 but not yet recorded in the company’s general ledger), the company must post the following entry:

Note: After recording/posting the adjustments to the general ledger accounts, it is important to confirm that the company’s general ledger Cash account balance is indeed equal to the Adjusted balance per BOOKS shown on the bottom line of the bank reconciliation.

Next, we will prepare a bank reconciliation for a hypothetical company by using transactions that are commonly encountered.

Please let us know how we can improve this explanation

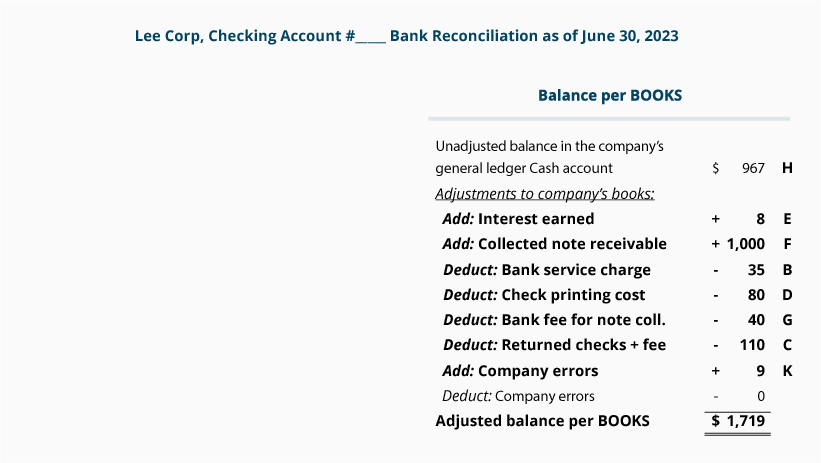

No ThanksSample of a Company’s Bank Reconciliation with Amounts

In this section we will prepare a June 30 bank reconciliation for Lee Corp using the five steps discussed above.

Step 1. Compare every amount on the bank statement (or the bank’s online information) with every amount in the company’s general ledger Cash account and note any differences.

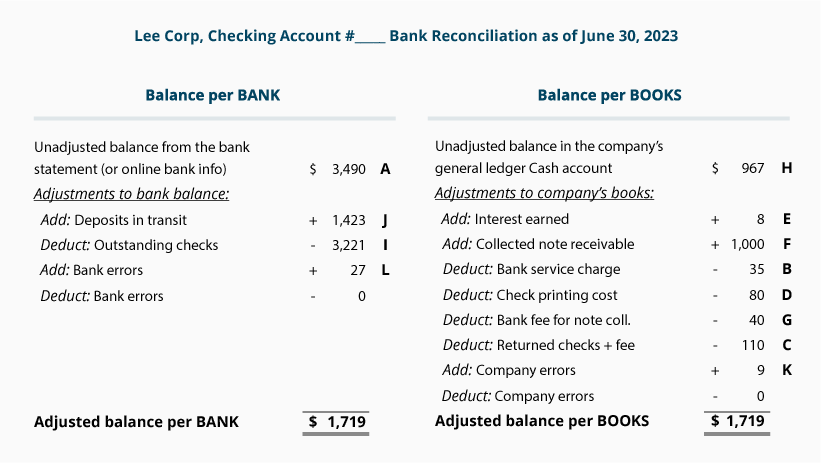

After comparing every item on the bank statement (checks paid, deposits processed, other items) with every item in Lee Corp’s general ledger Cash account (checks written, money received, other items), we listed the differences and other pertinent information in the table that follows.

(The letter in the “Item” column will be shown on the bank reconciliation next to the amount.)

Keep in mind our TIP: Put the item where it isn’t. This means:

-

If an item appears on the bank statement (but isn’t in the company’s general ledger), put the item on the bank reconciliation under Adjustments to BOOKS

-

If an item is already in the company’s general ledger Cash account (but it isn’t on the bank statement), put the item on the bank reconciliation under Adjustments to BANK

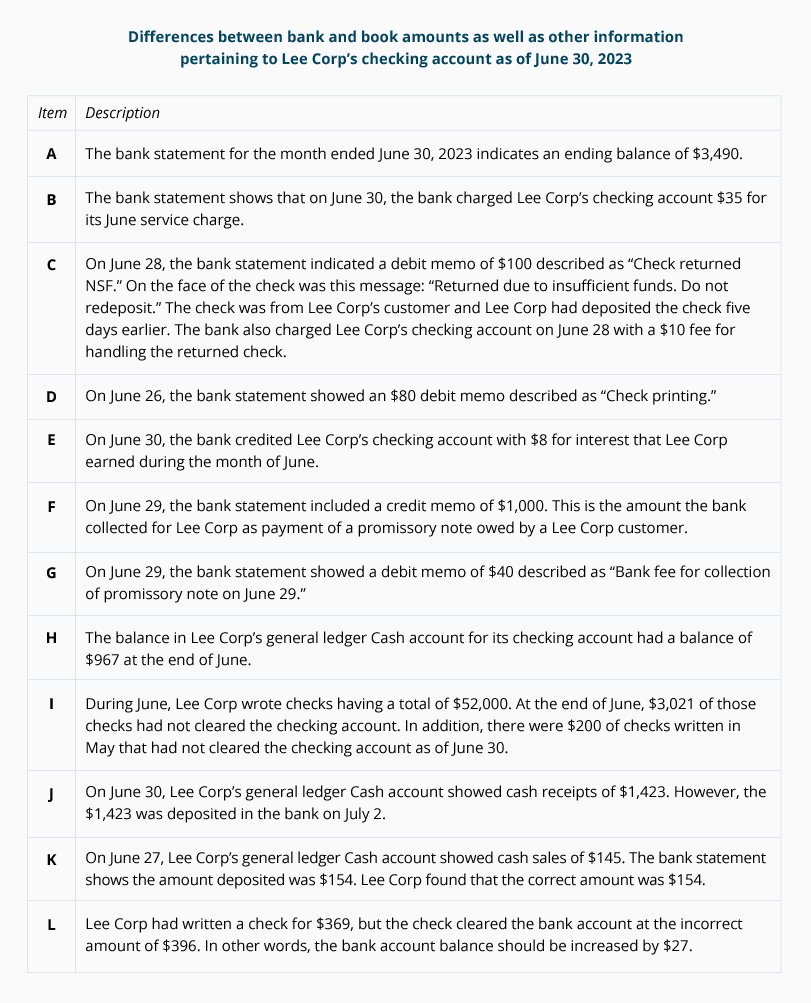

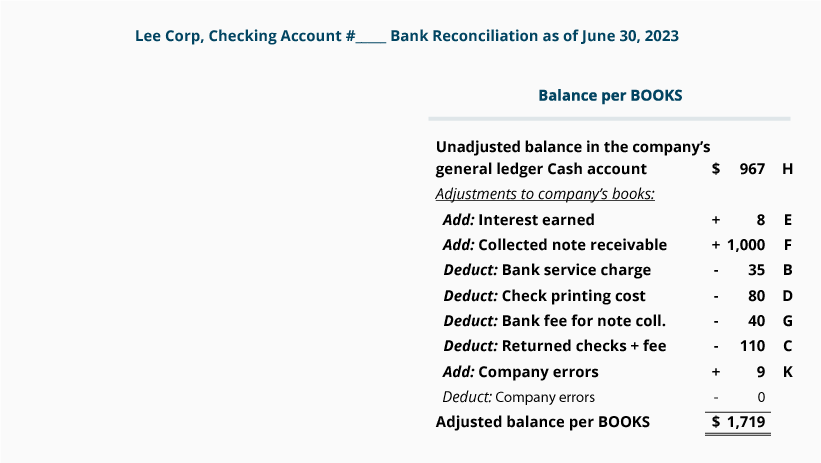

Step 2. Complete the Balance per BANK side of the bank reconciliation format.

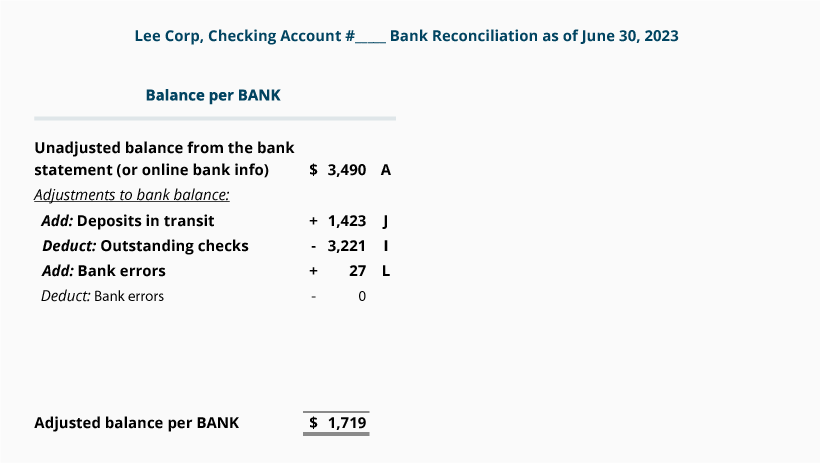

Step 3. Complete the Balance per BOOKS side of the bank reconciliation format.

Step 4. Be Certain the Adjusted Balance per BANK = Adjusted Balance per BOOKS.

Since the Adjusted balance per BANK of $1,719 is equal to Adjusted balance per BOOKS of $1,719, the bank statement of August 31 has been reconciled.

Step 5. Record in the company’s general ledger the adjustments to the balance per BOOKS.

Recall that the adjustments to the balance per BOOKS will require accounting entries for the items to be posted to the company’s general ledger accounts.

For each of the adjustments shown on the Balance per BOOKS side of the bank reconciliation, a journal entry is required. Each journal entry will affect at least two accounts, one of which is the company’s general ledger Cash account.

[Note: The company does not make accounting entries for the adjustments to the bank’s records.]

The following are the necessary entries for the adjustments to the balance per BOOKS. We reference each entry as E, F, B, D, G, C, or K, as indicated on the right side of the bank reconciliation.

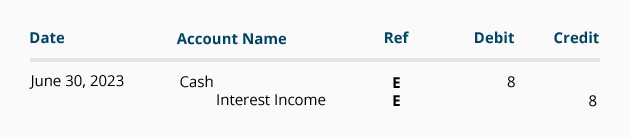

Adjustment E

The bank statement showed that on June 30, the bank added $8 of interest that had been earned by Lee Corp. Assuming that this was not yet recorded in Lee Corp’s general ledger, the following journal entry is required:

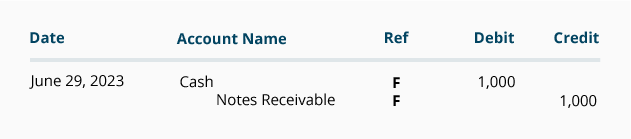

Adjustment F

On June 29, the bank statement showed a bank credit memo of $1,000 which caused the checking account balance to increase. We assume that Lee Corp had not yet recorded the collection of the note in its general ledger accounts. Therefore, Lee Corp must increase its Cash account balance and decrease the balance in its asset account Notes Receivable. This is achieved by the following journal entry:

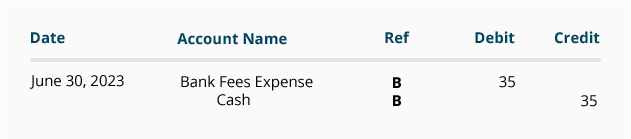

Adjustment B

The bank statement shows a service charge of $35 on June 30. Since this reduced the balance in Lee Corp’s checking account, Lee Corp must credit its Cash account and debit an expense such as Bank Fees Expense. Lee Corp’s entry is:

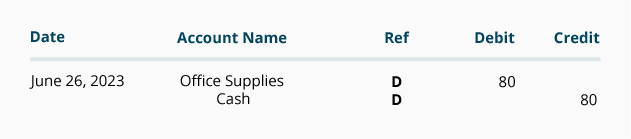

Adjustment D

On June 26, the bank statement showed that the bank processed a debit memo of $80 for the printing of Lee Corp’s checks. While the bank debits its liability account Customers’ Deposits to reduce its credit balance, Lee Corp must credit its asset account Cash to reduce its debit balance. Assuming that Lee Corp has not yet recorded the $80 printing cost, Lee Corp will record this journal entry:

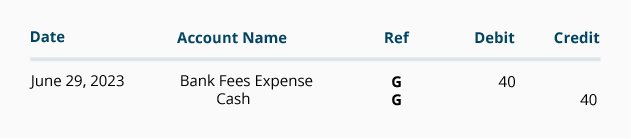

Adjustment G

On June 29, the bank statement showed a debit memo of $40 for the bank’s fee for collecting a note receivable for Lee Corp. Since this reduces Lee Corp’s checking account balance, Lee Corp will need to reduce the balance in its general ledger asset account Cash. Assuming this has not yet been recorded, the following entry is needed:

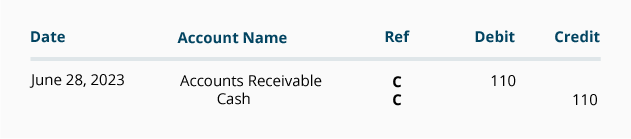

Adjustment C

On June 28, the bank statement showed that Lee Corp’s checking account balance was decreased by $110 for a check that Lee Corp had deposited in its checking account. (The deposited check was not paid by the bank on which it was drawn and was returned.) As a result, Lee Corp must reduce its general ledger Cash account by $110. Assuming this was not yet recorded by Lee Corp, it will record the following entry:

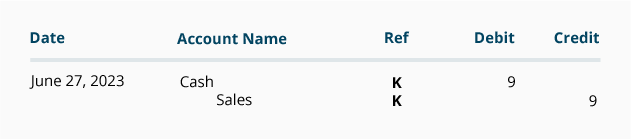

Adjustment K

On June 27 Lee Corp had increased its Cash account and its Sales account by $145. While reconciling its August bank statement, Lee Corp learned that the correct amount was $154. Therefore, Lee Corp must increase its Cash account balance by $9 and increase its Sales by $9. (Instead of removing the $145 and then adding $154, Lee Corp is adding the difference of $9 to the accounts.)

Note: After the above entries are posted to the general ledger accounts, it is important to confirm that the balance in the Cash account is equal to the Adjusted balance per BOOKS shown on the bank reconciliation.

It is also necessary to contact the bank immediately for any bank errors that were discovered in order for the bank account to be corrected.

Please let us know how we can improve this explanation

No ThanksWhen you join PRO Plus, you will receive lifetime access to all of our premium materials, as well as 10 different Certificates of Achievement.

Earn Our Certificate

for This Topic