Difference between Expense and Allowance

The account Bad Debts Expense reports the credit losses that occur during the period of time covered by the income statement. Bad Debts Expense is a temporary account on the income statement, meaning it is closed at the end of each accounting year. (Closed means the account balance is transferred to retained earnings, perhaps through an income summary account.) By closing Bad Debts Expense and resetting its balance to zero, the account is ready to receive and tally the credit losses for the next accounting year.

The Allowance for Doubtful Accounts reports on the balance sheet the estimated amount of uncollectible accounts that are included in Accounts Receivable. Balance sheet accounts are almost always permanent accounts, meaning their balances carry forward to the next accounting period. In other words, they are not closed and their balances are not reset to zero.

Because the Bad Debts Expense account is closed each year, while the Allowance for Doubtful Accounts is not, these two balances will most likely not be equal after the company’s first year of operations.

For example, let’s assume that at the end of its first year of operations a company’s Bad Debts Expense had a debit balance of $14,000 and its Allowance for Doubtful Accounts had a credit balance of $14,000. Because the income statement account balances are closed at the end of the year, the company’s opening balance in Bad Debts Expense for the second year of operations is $0. The credit balance of $14,000 in Allowance for Doubtful Accounts, however, carries forward to the second year. If an adjusting entry of $3,000 is made during year 2, Bad Debts Expense will report a $3,000 debit balance, while Allowance for Doubtful Accounts might report a credit balance of $17,000.

Again, the reasons for the account balance differences are 1) Bad Debts Expense is a temporary account that reports credit losses only for the period shown on the income statement, and 2) Allowance for Doubtful Accounts is a permanent account that reports an estimated amount for all of the uncollectible receivables reported in the asset Accounts Receivable as of the balance sheet date.

Please let us know how we can improve this explanation

No ThanksAging of Accounts Receivable

Download our Aging of Accounts Receivable Form and Template

The general ledger account Accounts Receivable usually contains only summary amounts and is referred to as a control account. The details for the control account—each credit sale for every customer—is found in the subsidiary ledger for Accounts Receivable. The total amount of all the details in the subsidiary ledger must be equal to the total amount reported in the control account.

The detailed information in the accounts receivable subsidiary ledger is used to prepare a report known as the aging of accounts receivable. This report directs management’s attention to accounts that are slow to pay. It is also useful in determining the balance amount needed in the account Allowance for Doubtful Accounts.

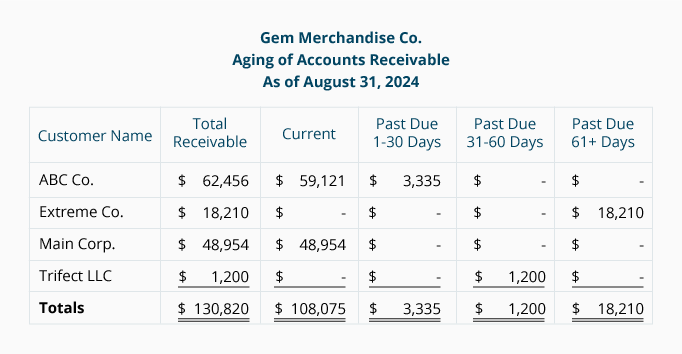

The aging of accounts receivable report is typically generated by sorting unpaid sales invoices in the subsidiary ledger—first by customer and then by the date of the sales invoices. If a company sells merchandise (or provides services) and allows customers to pay 30 days later, this report will indicate how much of its accounts receivable is past due. It also reports how far past due the accounts are.

With the click of a mouse, most accounting software will provide the aging of accounts receivable report. For example, Gem Merchandise Co.’s software looks at each of its customer’s accounts receivable activity and compares the date of each unpaid sales invoice to the date of the report. If we assume the report is dated August 31 and that Gem’s credit terms are net 30 days, any unpaid sales invoices with an August date will be classified as current. Any unpaid invoices with a date in July are classified as 1 – 30 days past due. Any unpaid invoices with a date of June are classified as 31 – 60 days past due, and so on. The sorted information is present in a report that looks similar to the following:

If a customer realizes that one of its suppliers is lax about collecting its account receivable on time, it may take advantage by further postponing payment in order to pay more demanding suppliers on time. This puts the seller at risk since an older, unpaid accounts receivable is more likely to end up as a credit loss. The aging of accounts receivable report helps management monitor and collect the accounts receivable in a more timely manner.

Aging Used in Calculating the Allowance

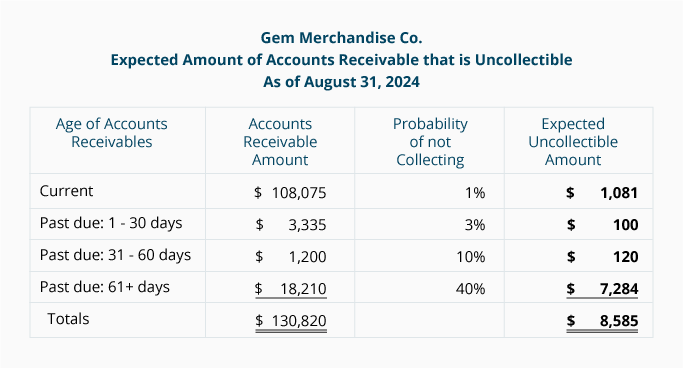

The aging of accounts receivable can also be used to estimate the credit balance needed in a company’s Allowance for Doubtful Accounts. For example, based on past experience, a company might make the assumption that accounts not past due have a 99% probability of being collected in full. Accounts that are 1-30 days past due have a 97% probability of being collected in full, and the accounts 31-60 days past due have a 90% probability. The company estimates that accounts more than 60 days past due have only a 60% chance of being collected. With these probabilities of collection, the probability of not collecting is 1%, 3%, 10%, and 40% respectively.

If we multiply the totals from the aging of accounts receivable report by the probabilities of not collecting, we arrive at the expected amount of uncollectible receivables. This is illustrated below:

This computation estimates the balance needed for Allowance for Doubtful Accounts at August 31 to be a credit balance of $8,585.

Please let us know how we can improve this explanation

No ThanksMailing Statements to Customers

To improve the probability of collection (and avoid bad debts expense) many sellers prepare and mail monthly statements to all customers that have accounts receivable balances. If worded skillfully, the seller can use the statement to say “thank you for your continued business” while at the same time “reminding” the customer that receivables are being monitored and payment is expected. To further prompt customers to pay in a timely manner, the statement may indicate that past due accounts are assessed interest at an annual rate of 18% (1.5% per month). Because transactions are usually itemized on the statement, some customers use the statement as a means to compare its records with those of the seller.

Please let us know how we can improve this explanation

No Thanks