Introduction

What are debits and credits?

Debits and credits are terms used by bookkeepers and accountants when recording transactions in the accounting records. The amount in every transaction must be entered in one account as a debit (left side of the account) and in another account as a credit (right side of the account). This double-entry system provides accuracy in the accounting records and financial statements.

The initial challenge is understanding which account will have the debit entry and which account will have the credit entry. Before we explain and illustrate the debits and credits in accounting and bookkeeping, we will discuss the accounts in which the debits and credits will be entered or posted.

WATCH NOW

Advance Your Career with Our PRO Training

What Is An Account?

To keep a company’s financial data organized, accountants developed a system that sorts transactions into records called accounts. When a company’s accounting system is set up, the accounts most likely to be affected by the company’s transactions are identified and listed out. This list is referred to as the company’s chart of accounts. Depending on the size of a company and the complexity of its business operations, the chart of accounts may list as few as thirty accounts or as many as thousands. A company has the flexibility of tailoring its chart of accounts to best meet its needs.

Within the chart of accounts the balance sheet accounts are listed first, followed by the income statement accounts. In other words, the accounts are organized in the chart of accounts as follows:

Click here to see a sample chart of accounts.

Double-Entry Accounting

Because every business transaction affects at least two accounts, our accounting system is known as a double-entry system. (You can refer to the company’s chart of accounts to select the proper accounts. Accounts may be added to the chart of accounts when an appropriate account cannot be found.)

For example, when a company borrows $1,000 from a bank, the transaction will affect the company’s Cash account and the company’s Notes Payable account. When the company repays the bank loan, the Cash account and the Notes Payable account are also involved.

If a company buys supplies for cash, its Supplies account and its Cash account will be affected. If the company buys supplies on credit, the accounts involved are Supplies and Accounts Payable.

If a company pays the rent for the current month, Rent Expense and Cash are the two accounts involved. If a company provides a service and gives the client 30 days in which to pay, the company’s Service Revenues account and Accounts Receivable are affected.

Although the system is referred to as double-entry, a transaction may involve more than two accounts. An example of a transaction that involves three accounts is a company’s loan payment to its bank of $300. This transaction will involve the following accounts: Cash, Notes Payable, and Interest Expense.

(If you use accounting software you may not actually see that two or more accounts are being affected due to the user-friendly nature of the software. For example, let’s say that you write a company check by means of your accounting software. Your software automatically reduces your Cash account and prompts you only for the other accounts affected.)

Debits and Credits

After you have identified the two or more accounts involved in a business transaction, you must debit at least one account and credit at least one account.

To debit an account means to enter an amount on the left side of the account. To credit an account means to enter an amount on the right side of an account.

Here’s a Tip

Debit means left

Credit means right

Generally these types of accounts are increased with a debit:

Dividends (Draws)

Expenses

Assets

Losses

You might think of D – E – A – L when recalling the accounts that are increased with a debit.

Generally the following types of accounts are increased with a credit:

Gains

Income

Revenues

Liabilities

Stockholders’ (Owner’s) Equity

You might think of G – I – R – L – S when recalling the accounts that are increased with a credit.

To decrease an account you do the opposite of what was done to increase the account. For example, an asset account is increased with a debit. Therefore it is decreased with a credit.

The abbreviation for debit is dr. and the abbreviation for credit is cr.

T-accounts

Accountants and bookkeepers often use T-accounts as a visual aid to see the effect of a transaction or journal entry on the two (or more) accounts involved.

To learn more about the role of bookkeepers and accountants, visit our Accounting Careers page.

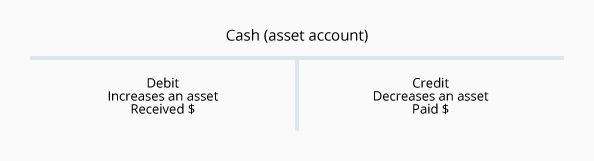

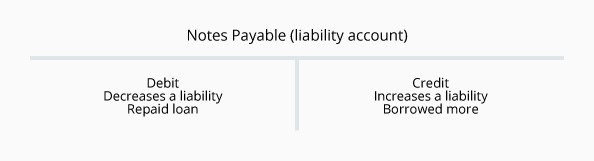

We will begin with two T-accounts: Cash and Notes Payable.

Let’s demonstrate the use of these T-accounts with two transactions:

- On June 1, 2025 a company borrows $5,000 from its bank. As a result, the company’s asset Cash must be increased by $5,000 and its liability Notes Payable must be increased by $5,000. To increase the asset Cash the account needs to be debited. To increase the company’s liability Notes Payable this account needs to be credited. After entering the debits and credits the T-accounts look like this:

- On June 2, 2025 the company repays $2,000 of the bank loan. As a result, the company’s asset Cash must be decreased by $2,000 and its liability Notes Payable must be decreased by $2,000. To reduce the asset Cash the account will need to be credited for $2,000. To decrease the liability Notes Payable that account will need to be debited for $2,000. The T-accounts now look like this:

Journal Entries

Another way to visualize business transactions is to write a general journal entry. Each general journal entry lists the date, the account title(s) to be debited and the corresponding amount(s) followed by the account title(s) to be credited and the corresponding amount(s). The accounts to be credited are indented. Let’s illustrate the general journal entries for the two transactions that were shown in the T-accounts above.

When Cash Is Debited and Credited

Because cash is involved in many transactions, it is helpful to memorize the following:

- Whenever cash is received, debit Cash.

- Whenever cash is paid out, credit Cash.

With the knowledge of what happens to the Cash account, the journal entry to record the debits and credits is easier. Let’s assume that a company receives $500 on June 3, 2025 from a customer who was given 30 days in which to pay. (In May the company had recorded the sale and an accounts receivable.) On June 3 the company will debit Cash, because cash was received. The amount of the debit and the credit is $500. Entering this information in the general journal format, we have:

All that remains to be entered is the name of the account to be credited. Since this was the collection of an account receivable, the credit should be Accounts Receivable. (Because the sale was already recorded in May, you cannot enter Sales again on June 3.)

On June 4 the company paid $300 to a supplier for merchandise the company received in May. (In May the company recorded the purchase and the accounts payable.) On June 4 the company will credit Cash, because cash was paid. The amount of the debit and credit is $300. Entering them in the general journal format, we have:

All that remains to be entered is the name of the account to be debited. Since this was the payment on an account payable, the debit should be Accounts Payable. (Because the purchase was already recorded in May, you cannot enter Purchases or Inventory again on June 4.)

To help you become comfortable with the debits and credits in accounting, memorize the following tip:

Here’s a Tip

Whenever cash is received, the Cash account is debited (and another account is credited).

Whenever cash is paid out, the Cash account is credited (and another account is debited).

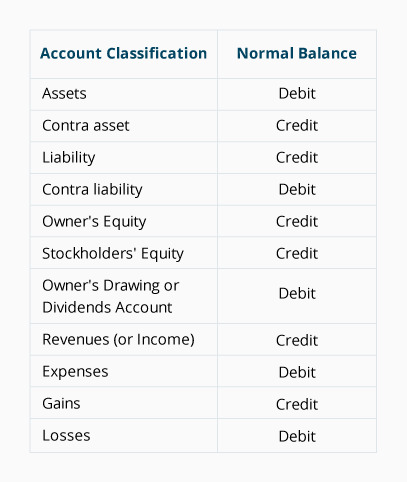

Normal Balances

When looking at an account in the general ledger, the following is the debit or credit balance you would normally find in the account:

Revenues and Gains Are Usually Credited

Revenues and gains are recorded in accounts such as Sales, Service Revenues, Interest Revenues (or Interest Income), and Gain on Sale of Assets. These accounts normally have credit balances that are increased with a credit entry. In a T-account, their balances will be on the right side.

The exceptions to this rule are the accounts Sales Returns, Sales Allowances, and Sales Discounts – these accounts have debit balances because they are reductions to sales. Accounts with balances that are the opposite of the normal balance are called contra accounts hence contra revenue accounts will have debit balances.

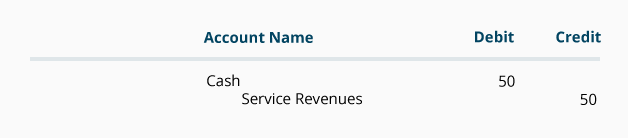

Let’s illustrate revenue accounts by assuming your company performed a service and was immediately paid the full amount of $50 for the service. The debits and credits are presented in the following general journal format:

Whenever cash is received, the asset account Cash is debited and another account will need to be credited. Since the service was performed at the same time as the cash was received, the revenue account Service Revenues is credited, thus increasing its account balance.

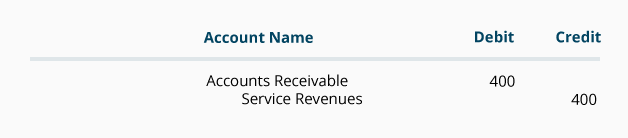

Let’s illustrate how revenues are recorded when a company performs a service on credit (i.e., the company allows the client to pay for the service at a later date, such as 30 days from the date of the invoice). At the time the service is performed the revenues are considered to have been earned and they are recorded in the revenue account Service Revenues with a credit. The other account involved, however, cannot be the asset Cash since cash was not received. The account to be debited is the asset account Accounts Receivable. Assuming the amount of the service performed is $400, the entry in general journal form is:

Accounts Receivable is an asset account and is increased with a debit; Service Revenues is increased with a credit.

Expenses and Losses are Usually Debited

Expenses normally have debit balances that are increased with a debit entry. Since expenses are usually increasing, think “debit” when expenses are incurred. (We credit expenses only to reduce them, adjust them, or to close the expense accounts.) Examples of expense accounts include Salaries Expense, Wages Expense, Rent Expense, Supplies Expense, and Interest Expense. In a T-account, their balances will be on the left side.

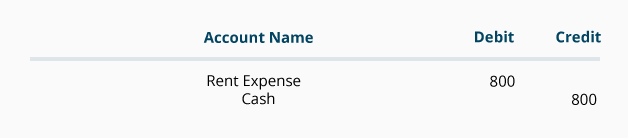

To illustrate an expense let’s assume that on June 1 your company paid $800 to the landlord for the June rent. The debits and credits are shown in the following journal entry:

Since cash was paid out, the asset account Cash is credited and another account needs to be debited. Because the rent payment will be used up in the current period (the month of June) it is considered to be an expense, and Rent Expense is debited. If the payment was made on June 1 for a future month (for example, July) the debit would go to the asset account Prepaid Rent.

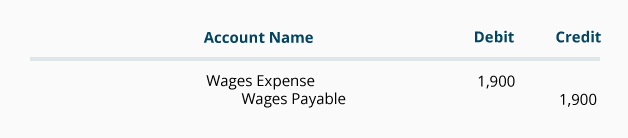

As a second example of an expense, let’s assume that your hourly paid employees work the last week in the year but will not be paid until the first week of the next year. At the end of the year, the company makes an entry to record the amount the employees earned but have not been paid. Assuming the employees earned $1,900 during the last week of the year, the entry in general journal form is:

As noted earlier, expenses are almost always debited, so we debit Wages Expense, increasing its account balance. Since your company did not yet pay its employees, the Cash account is not credited, instead, the credit is recorded in the liability account Wages Payable. A credit to a liability account increases its credit balance.

To help you get more comfortable with debits and credits in accounting and bookkeeping, memorize the following tip:

Here’s a Tip

To increase an expense account, debit the account.

Permanent and Temporary Accounts

Asset, liability, and most owner/stockholder equity accounts are referred to as permanent accounts (or real accounts). Permanent accounts are not closed at the end of the accounting year; their balances are automatically carried forward to the next accounting year.

Temporary accounts (or nominal accounts) include all of the revenue accounts, expense accounts, the owner’s drawing account, and the income summary account. Generally speaking, the balances in temporary accounts increase throughout the accounting year. At the end of the accounting year the balances will be transferred to the owner’s capital account or to a corporation’s retained earnings account.

Because the balances in the temporary accounts are transferred out of their respective accounts at the end of the accounting year, each temporary account will have a zero balance when the next accounting year begins. This means that the new accounting year starts with no revenue amounts, no expense amounts, and no amount in the drawing account.

By having many revenue accounts and a huge number of expense accounts, a company will be able to report detailed information on revenues and expenses throughout the year.

Bank’s Debits and Credits

When you hear your banker say, “I’ll credit your checking account,” it means the transaction will increase your checking account balance. Conversely, if your bank debits your account (e.g., takes a monthly service charge from your account) your checking account balance decreases.

If you are new to the study of debits and credits in accounting, this may seem puzzling. After all, you learned that debiting the Cash account in the general ledger increases its balance, yet your bank says it is crediting your checking account to increase its balance. Similarly, you learned that crediting the Cash account in the general ledger reduces its balance, yet your bank says it is debiting your checking account to reduce its balance.

Although the above may seem contradictory, we will illustrate below that a bank’s treatment of debits and credits is indeed consistent with the basic accounting procedure that you learned. Let’s look at three transactions and consider the related journal entries from both the bank’s perspective and the company’s perspective.

Transaction #1

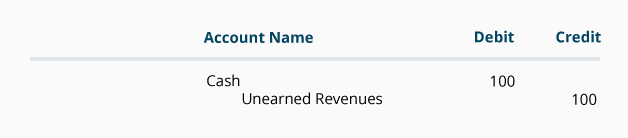

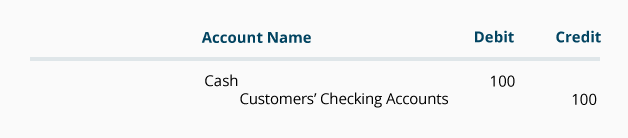

Let’s say that your company, Debris Disposal, receives $100 of currency from a customer as a down payment for a future site cleanup service. When the money is received your company makes the following entry:

(Debris Disposal’s journal entry)

Because it has received cash, Debris Disposal increases its Cash account with a debit of $100. The rules of double-entry accounting require Debris Disposal to also enter a credit of $100 into another of its general ledger accounts. Since the company has not yet earned the $100, it cannot credit a revenue account. Instead, the liability account Unearned Revenues is credited because Debris Disposal has a liability to do the work or to return the $100. (An alternate title for the Unearned Revenues account is Customer Deposits.)

Now let’s say you take that $100 to Trustworthy Bank and deposit it into Debris Disposal’s checking account. Since Trustworthy Bank is receiving cash of $100, the bank debits its general ledger Cash account for $100, thereby increasing the bank’s assets. The rules of double-entry accounting require the bank to also enter a credit of $100 into another of the bank’s general ledger accounts. Because the bank has not earned the $100, it cannot credit a revenue account. Instead, the bank credits a liability account such as Customers’ Checking Accounts to reflect the bank’s obligation/liability to return the $100 to Debris Disposal on demand. In general journal format the bank’s entry is:

(Trustworthy Bank’s journal entry)

As the entry shows, the bank’s assets increase by the debit of $100 and the bank’s liabilities increase by the credit of $100. The bank’s detailed records show that Debris Disposal’s checking account is the specific liability that increased.

Transaction #2

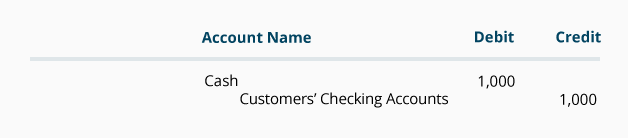

Let’s say Trustworthy Bank receives a $1,000 wire transfer on your company’s behalf from a person who owes money to Debris Disposal. Two things happen at the bank: (1) The bank receives $1,000, and (2) the bank records its obligation to give the money to Debris Disposal on demand. These two facts are entered into the bank’s general ledger as follows:

(Trustworthy Bank’s journal entry)

The debit increases the bank’s assets by $1,000 and the credit increases the bank’s liabilities by $1,000. The bank’s detailed records show that Debris Disposal’s checking account is the specific liability that increased.

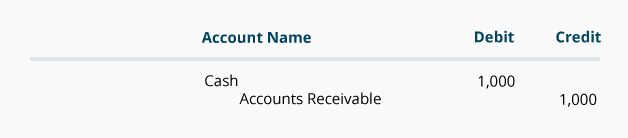

At the same time the $1,000 wire transfer is received at the bank, Debris Disposal makes the following entry into its general ledger:

(Debris Disposal’s journal entry)

As a result of collecting $1,000 from one of its customers, Debris Disposal’s Cash balance increases and its Accounts Receivable balance decreases.

Transaction #3

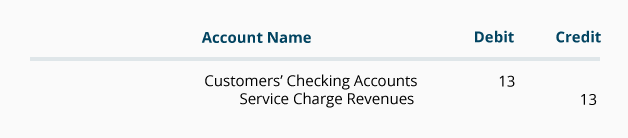

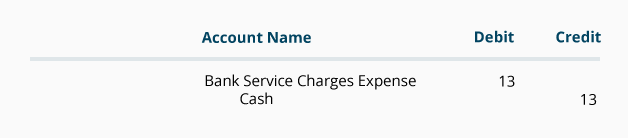

Many banks charge a monthly fee on checking accounts. If Trustworthy Bank decreases Debris Disposal’s checking account balance by $13.00 to pay for the bank’s monthly service charge, this might be itemized on Debris Disposal’s bank statement as a “debit memo.” The entry in the bank’s records will show the bank’s liability being reduced (because the bank owes Debris Disposal $13 less). It also shows that the bank earned revenues of $13 by servicing the checking account.

(Trustworthy Bank’s general ledger)

On your company’s records, the entry will look like this:

(Debris Disposal’s general ledger)

Debris Disposal’s cash is reduced with a credit of $13 and expenses are increased with a debit of $13. (If the amount of the bank’s service charges is not significant a company may debit the charge to Miscellaneous Expense.)

Bank’s Balance Sheet

Accounts such as Cash, Investment Securities, and Loans Receivable are reported as assets on the bank’s balance sheet. Customers’ bank accounts are reported as liabilities and include the balances in its customers’ checking and savings accounts as well as certificates of deposit. In effect, your bank statement is just one of thousands of subsidiary records that account for millions of dollars that a bank owes to its depositors.

Recap

Here are some of the highlights from this explanation:

- Debit means left.

- Credit means right.

- Every transaction affects two accounts or more.

- At least one account will be debited and at least one account will be credited.

- The total of the amount(s) entered as debits must equal the total of the amount(s) entered as credits.

- When cash is received, debit Cash.

- When cash is paid out, credit Cash.

- To increase an asset, debit the asset account.

- To increase a liability, credit the liability account.

- To increase owner’s equity, credit an owner’s equity account.

- To increase revenues, credit the revenues account

- A credit to a revenue account also causes an increase in owner’s equity

- To increase expenses, debit the expense account

- A debit to an expense account also causes a decrease in owner’s equity

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Debits and Credits materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.

Earn Our Certificate

for This Topic

When you join PRO, you will receive instant access to 16 different Certificates of Achievement plus our Bookkeeping Certificate of Excellence.

View PRO Features