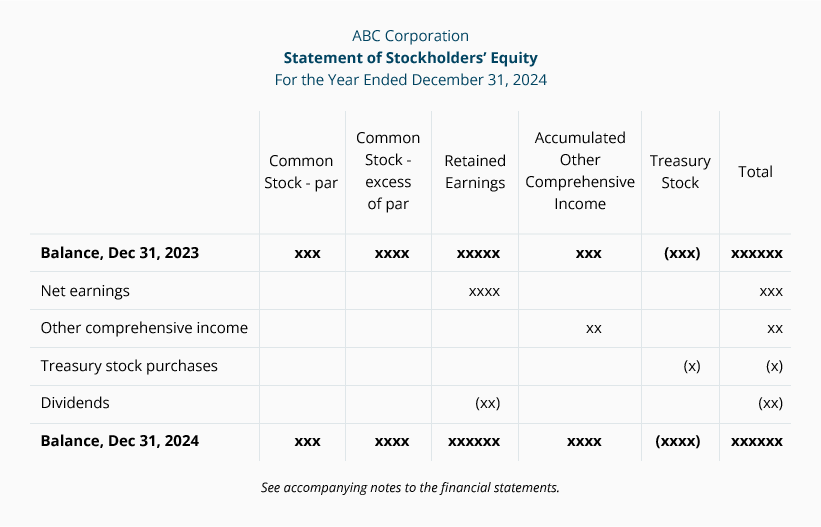

Statement of Stockholders’ Equity

The fourth financial statement is the statement of stockholders’ equity. This statement lists the changes to the stockholders’ equity section of the balance sheet during the current accounting period.

A common format of the statement of stockholders’ equity is shown here:

To see additional examples of the statement of stockholders’ equity we recommend that you identify a few U.S. corporations with stock that is publicly traded. On each corporation’s website, select Investor Relations and then select each corporation’s Form 10-K (the annual report to the Securities and Exchange Commission). Go to the section of the 10-K which presents the corporation’s financial statements and view the statement of stockholders’ equity.

Please let us know how we can improve this explanation

No ThanksClosing Cut-Off

At a minimum of once per year, companies must prepare financial statements. In addition companies often prepare quarterly and monthly financial statements which are referred to as interim financial statements.

For any of the financial statements to be accurate it is necessary to have a proper cut-off. This means including all of a company’s business transactions in the proper accounting period. For example, the electricity bill arriving on January 10 might be the cost of the electricity that was actually used in December. (The time lag resulted from the utility company reading the electric meters and preparing and mailing the bill.) Hence under the accrual method of accounting, the bill received on January 10 needs to be included in December’s expenses and must also be reported by the company as a liability as of December 31.

Similarly, the hourly payroll processed during the first few days in January and paid on January 6 is likely to include the cost of employees working during the last few days in December. The cost of the hours worked through December 31 must be included in the company’s December expenses and in the liabilities as of December 31.

As you read the previous paragraph, you may have been reminded of our discussion of adjusting entries. That’s because the adjusting entries are part of each period’s closing process. The adjusting entries are prepared in order to report a company’s revenues and expenses in the proper accounting period.

The closing process

To achieve a proper cut-off and to distribute the financial statements in a timely manner, it is helpful to have a timeline (or PERT chart) that indicates the necessary steps in the closing process. The timeline will indicate what needs to be done and the sequence in which things need to occur. It will also reveal what is preventing the financial statements from being distributed sooner.

In addition, a checklist of the closing tasks should be prepared and distributed to the appropriate employees as to what is required, who is responsible, and the day it is due.

If some journal entries must be written every month, it is helpful to assign journal entry numbers to these standard journal entries or recurring journal entries. For example, a company may designate JE33 (Journal Entry #33) to be the recurring accrual of expenses that have occurred but have not yet been recorded in Accounts Payable as of the end of a month. Perhaps the timeline/checklist will indicate that JE33 must be submitted by the accounts payable clerk six days after each month ends. The company may also have its computer automatically prepare JE34 which is the entry that automatically reverses the previous month’s accrual entry JE33.

Some recurring journal entries will have the same amount each month. For example, a company’s JE10 might be $10,800 every month of the year for the company’s depreciation expense. (Some companies will refer to the entries that have the same amounts and accounts every month as standard entries.)

Another recurring entry may involve the same accounts each month, but the amounts will vary from month to month. For example, a company’s JE03 might be the recurring monthly entry for bad debts expense. The company has determined in advance that the amount of JE03 will be 0.002 of the company’s monthly credit sales. Since the amount of sales is different every month, the amounts on JE03 will be different each month.

Having entry numbers and standard entries should help to make the monthly closings more routine and efficient.

Please let us know how we can improve this explanation

No ThanksImportance of Controls

The use of accounting software has eliminated some of the tedious tasks previously associated with bookkeeping. This could result in fewer people involved in the bookkeeping, accounting and administrative tasks. A side effect of fewer people handling more tasks is the potential for concealing some dishonest activity. For example, if the person who processes the cash receipts is also the person that records the amounts in customers’ accounts, stealing some cash will be easier than if the tasks were separated. Having a third person mailing statements to customers with instructions to report any discrepancies to a fourth person will further safeguard the company’s assets.

Accountants refer to the practices and policies for safeguarding assets as internal controls. Very large corporations may have a staff of internal auditors that ensure there are controls in place (including the separation of duties) so that fraud and misappropriation will not occur. Small companies or organizations with a small staff are therefore at a disadvantage. Nonetheless owners and managers of even the smallest companies and organizations must be aware of the need for internal controls. Here is a partial list of some internal controls that smaller organizations can implement:

- Separate the handling of cash from the person processing accounts receivable.

- Have the bank statement reconciled by someone who does not process the receipts or record the amounts in the general ledger cash account.

- Have the owner of a small company approve all purchase orders.

- Have the owner of a small company review all payments and sign all checks.

- Have all credit memos to customers be approved by the owner.

We are not experts in internal controls, but we realize their importance. We strongly recommend that you seek assistance from your professional accountant regarding internal controls that are appropriate for your business or organization.

Want More Bookkeeping Materials?

When you join AccountingCoach PRO you will receive lifetime access to our Guide to Bookkeeping Concepts, Bookkeeping Video Training, Bookkeeping Cheat Sheet, Bookkeeping Quick Test, Bookkeeping Tests for Prospective Employees, and Bookkeeping Flashcards.

Please let us know how we can improve this explanation

No Thanks