Introduction

The balance sheet (also known as the statement of financial position) reports a corporation’s assets, liabilities, and stockholders’ equity as of the final moment of an accounting period. For example, a balance sheet dated December 31 summarizes the balances in the appropriate general ledger accounts after all transactions up to midnight of December 31 have been accounted for.

The balance sheet is one in a set of five financial statements distributed by a U.S. corporation. To get a complete understanding of the corporation’s financial position, one must study all five of the financial statements including the notes to the financial statements.

The structure of the balance sheet reflects the accounting equation: assets = liabilities + stockholders’ (or owner’s) equity. The use of double-entry accounting keeps the balance sheet in balance.

The amounts reported on the balance sheet are summations of the ending balances in the many asset, liability, and stockholders’ equity accounts. The summarized amounts are presented in the following sections of the balance sheet:

Generally accepted accounting principles (GAAP)

To assist the users of the balance sheet, a U.S. company must prepare its externally distributed financial statements according to common rules known as generally accepted accounting principles (GAAP or US GAAP; pronounced ‘gap’). US GAAP includes basic underlying accounting principles, assumptions, and detailed accounting standards of the Financial Accounting Standards Board (FASB).

Part of US GAAP is to have financial statements prepared by using the accrual method of accounting (as opposed to the cash method). The accrual method means that the balance sheet must report liabilities from the time they are incurred until the time they are paid. It also means the balance sheet will report assets such as accounts receivable and interest receivable when the amounts are earned (as opposed to waiting until the money is received). In short, the accrual method of accounting results in a more complete set of financial statements.

US GAAP will also mean that some of a company’s most valuable things (internally developed brand names, trademarks, patents, creative employees, etc.) will not be included as assets on the company’s balance sheet.

Let’s begin by looking at some balance sheet formats.

WATCH NOW

Advance Your Career with Our PRO Training

Sample Balance Sheets

We will present examples of three balance sheet formats containing the same hypothetical amounts. (The notes to the financial statements are omitted as they will be identical regardless of the format used.)

Example of a balance sheet using the account form

In the account form (shown above) its presentation mirrors the accounting equation. That is, assets are on the left; liabilities and stockholders’ equity are on the right.

With the account form it is easy to compare the totals. It is also convenient to compare the current assets with the current liabilities.

A drawback of the account form is the difficulty in presenting an additional column of amounts on an 8.5″ by 11″ page.

Example of a balance sheet using the report form

As you can see, the report form presents the assets at the top of the balance sheet. Beneath the assets are the liabilities followed by stockholders’ equity.

Example of a comparative balance sheet

The comparative balance sheet presents multiple columns of amounts, and as a result, the heading will be Balance Sheets. The additional column allows the reader to see how the most recent amounts have changed from an earlier date.

It is common to present the recent amounts in the column closest to the descriptions, and the oldest amounts furthest from the descriptions. It is also common for the amounts to be rounded to the nearest dollar or nearest thousand dollars.

As you can see, the report form is more conducive to reporting an additional column(s) of amounts.

Balance Sheet Templates

Did you know? Our Business Forms Package offers 80+ different business forms including the following balance sheet templates in Excel and PDF format:

- Balance Sheet Template: Manufacturer – Corporation

- Balance Sheet Template: Retail/Wholesale – Corporation

- Balance Sheet Template: Retail/Wholesale – Sole Proprietor

- Balance Sheet Template: Services – Corporation

- Balance Sheet Template: Services – Sole Proprietor

In addition to our balance sheet templates, our business forms also offer templates for the income statement, statement of cash flows, and more.

Now that we have seen some sample balance sheets, we will describe each section of the balance sheet in detail.

Balance Sheet Heading

The heading found at the top of the balance sheet contains the following:

- Company name

- Name of the financial statement: Balance Sheet or Statement of Financial Position

- Date

Typically, the balance sheet date is the final day of the accounting period. If a company issues monthly financial statements, the date will be the final day of each month.

The date communicates to the reader that the amounts reported on the balance sheet represent the balances in the company’s asset, liability, and stockholders’ equity accounts after all transactions up to the final moment of the date have been accounted for.

NOTE: Of the five financial statements, only the balance sheet’s heading indicates a point or moment in time, such as December 31, 2025. This date means the amounts shown reflect all transactions up to midnight on December 31, 2025.

The headings on the other four financial statements indicate a span of time (interval of time, period of time) during which the amounts occurred. For instance, the heading of a company’s income statement might indicate “For the year ended December 31, 2025”. This tells the reader that the amounts reported for sales and expenses are the total amounts for the 365 days of the year.

Financial statements issued between the end-of-the-year financial statements are referred to as interim financial statements. Accounting years which end on dates other than December 31 are known as fiscal years.

Balance sheet heading when a corporation owns multiple corporations

Many large corporations own and control several corporations. When the main corporation issues a comparative balance sheet for the entire group of corporations, the balance sheet heading will state “Consolidated Balance Sheets”.

Assets

Assets are a company’s resources (things the company owns). Their amounts appear on the company’s balance sheet if they:

- Were acquired through a purchase or were received through a donation

- Have a future economic value that can be measured and expressed in amounts of currency

- Include prepaid expenses that have not yet expired or been used up

Assets are recorded in the company’s general ledger accounts at their cost when they were acquired. In accounting cost means all costs that were necessary to get the assets in place and ready for use. For example, the cost of new equipment to be used in a business will include the cost of getting the equipment installed and operating properly.

(In a company’s general ledger, the balances in the asset accounts are normally debit balances. We often visualize the debit balances as appearing on the left side of a T-account. This is consistent with the accounting equation where assets appear on the left side of the equal sign. You can learn more by visiting our Debits and Credits Explanation.)

Reporting assets on the balance sheet

Some common examples of general ledger asset accounts include Cash, Accounts Receivable, Inventory, Prepaid Expenses, Buildings, Equipment, Vehicles, and perhaps 50 additional accounts.

The general rule (except for certain marketable securities) is that the cost recorded at the time of an asset’s purchase will not be increased for inflation or to the asset’s current market value.

However, some accounting rules do require some recorded costs to be reduced through a contra asset account. For example, the cost of buildings and equipment used in the business will be depreciated and the amount of the depreciation will be recorded with a credit entry to the contra asset account Accumulated Depreciation. It is also possible that the reported amount of these and other long-term assets will be reduced when their book values (cost minus accumulated depreciation) have been impaired.

The ending balances in the company’s related asset accounts will be combined and presented on perhaps 15 lines on the balance sheet. Those combined amounts will appear as lines under the following balance sheet categories:

- Current assets

- Investments

- Property, plant and equipment

- Intangible assets

- Other assets

Current Assets

A quick definition of current assets is cash and assets that are expected to be converted to cash within one year of the balance sheet’s date.

NOTE: The complete definition of a current asset is cash and assets that are expected to turn to cash within one year of the balance sheet’s date, or within the company’s operating cycle, whichever is longer.

Since most industries have operating cycles of less than a year, our examples will assume that one year is longer than the companies’ operating cycles.

The operating cycle for a distributor of goods is the average time it takes for the distributor’s cash to return to its checking account after purchasing goods for sale. To illustrate, assume that a distributor spends $200,000 to buy goods for its inventory. If it takes 3 months to sell the goods on credit and then another month to collect the receivables, the distributor’s operating cycle is 4 months. Because one year is longer than the 4-month operating cycle, the distributor’s current assets include its cash and assets that are expected to turn to cash within one year.

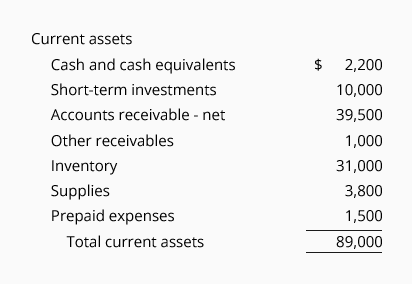

Here is the current asset section from our sample balance sheets:

Within the current asset section of the balance sheet, we usually see amounts for the following:

- Cash and cash equivalents

- Short-term investments

- Accounts receivable – net

- Other receivables

- Inventory

- Supplies

- Prepaid expenses

Cash and cash equivalents

Cash and cash equivalents appear as the first current asset and will be the combined amount of the following:

- Cash which includes the company’s checking account balances, currency, checks received but not yet deposited in the bank account, and petty cash.

- Cash equivalents include investments that will mature within three months of the date they were purchased. In other words, cash equivalents will be investments where their market values are not likely to fluctuate in the near term. Examples of cash equivalents include 90-day U.S. Treasury Bills and money market accounts.

Short-term investments

Short-term investments are temporary investments that do not qualify as cash equivalents but are expected to turn to cash within one year.

Accounts receivable – net

The balance sheet item accounts receivable – net (or trade receivables – net) is the amount in the company’s account Accounts Receivable minus the amount in the contra account Allowance for Doubtful Accounts. This net amount is also known as the net realizable value of the company’s accounts receivable.

Generally, a company’s accounts receivable will turn to cash within a month or two depending on the company’s credit terms.

The balance in the general ledger account Accounts Receivable is the sales invoice amounts for goods sold on credit terms minus the amounts collected from these customers. In other words, the balance in Accounts Receivable is the amount of the open or uncollected sales invoices.

The balance in the general ledger account Allowance for Doubtful Accounts is an estimate of the amount in Accounts Receivable that the company anticipates will not be collected.

You can learn more by visiting our Accounts Receivable and Bad Debts Expense Explanation.

Other receivables

The current asset other receivables is the amount other than accounts receivable that a company has a right to receive. For example, if a company lent an employee $1,000 and the amount is being repaid over a four-month period, the amount owed by the employee as of the balance sheet date will be reported as part of other receivables (or miscellaneous receivables or nontrade receivables).

Another example of other receivables is a corporation’s income tax refund related to its recently filed income tax return.

Inventory

Inventory is likely the largest current asset on a retailer’s or manufacturer’s balance sheet. The reported amount on the retailer’s balance sheet is the cost of merchandise that was purchased, but not yet sold to customers.

In the accounting period when the items in inventory are sold, the cost of the items sold is removed from the asset inventory and is reported on the income statement as cost of goods sold.

In the U.S., a company can elect which costs will be removed first from inventory (oldest, most recent, average, or specific cost). During times of inflation or deflation this decision affects both the cost of the inventory reported on the balance sheet and the cost of goods sold reported on the income statement.

A manufacturer is required to report (on the face of the balance sheet or in the notes to the financial statements) the following ending inventory amounts:

You can learn more about inventory and the related cost flows by visiting our Inventory and Cost of Goods Sold Explanation.

Supplies

Supplies includes the cost of office supplies, packaging supplies, maintenance supplies, etc. that the company has on hand.

Prepaid expenses

The current asset prepaid expenses reports the amount of future expenses that the company had paid in advance and they have not yet expired (have not been used up).

To illustrate, assume that on December 1, a company pays its $1,800 insurance premium for property insurance covering the next six months of December 1 through May 31. This means that during each of the six months, 1/6 of the $1,800 = $300 will be reported on the monthly income statements. The amount not yet used up (still prepaid) as of each balance sheet date is reported as the current asset prepaid expenses.

Given the above information, the company’s December 31 balance sheet will report $1,500 as the current asset prepaid expenses. (This is the original $1,800 payment on December 1 minus $300 that was used up during the month of December. The $1,500 is also calculated as 5 months of unexpired insurance X $300 per month.) On January 31 the current asset prepaid expenses will report $1,200 (4 months still unexpired X $300 per month). On February 28 prepaid expenses will report $900 (3 months of the insurance cost that is unexpired/still prepaid X $300 per month), and so on.

You can learn more about prepaid expenses by visiting our Adjusting Entries Explanation.

Long-Term Assets

Long-term assets are also described as noncurrent assets since they are not expected to turn to cash within one year of the balance sheet date.

The long-term assets are usually presented in the following balance sheet categories:

- Investments

- Property, plant and equipment – net

- Intangible assets

- Other assets

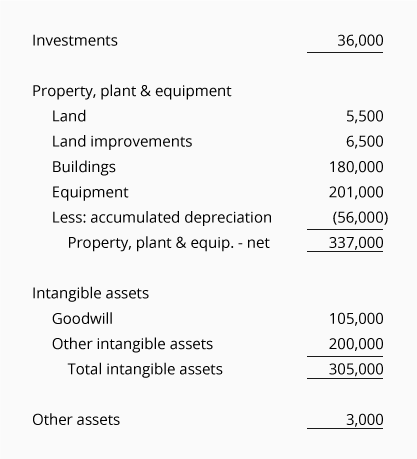

Here is the long-term (or noncurrent) asset section from our sample balance sheets:

Investments

The first long-term asset Investments will include amounts such as the following:

- Long-term investments in investment securities, real estate, or other businesses

- Property that is in the process of being sold

- Cash surrender value of life insurance policies owned by the company

- Bond sinking funds and other assets restricted for a long-term purpose

While long-term investments in marketable securities are initially recorded at their cost, the amount of these investments will be adjusted (increased or decreased) to report their market value as of the date of the balance sheet.

Property, plant and equipment – net

The balance sheet category property, plant and equipment – net includes the cost of the noncurrent, tangible assets that are used in a business minus the related accumulated depreciation. (These assets are sometimes referred to as fixed assets, plant assets, long-lived assets, and capital assets.)

An asset’s cost minus its accumulated depreciation is known as the asset’s book value or carrying value.

NOTE: The depreciation and the accumulated depreciation reported on a company’s financial statements are typically based on the assets’ years of useful life.

These amounts are likely different from the amounts reported on the company’s income tax return.

The following amounts often appear under property, plant and equipment – net or will be disclosed in the notes to the financial statements:

- Land

- Land improvements

- Buildings and improvements

- Machinery and equipment

- Furniture and fixtures

- Construction in progress

- Less: accumulated depreciation

Land

Land refers to the land used in the business, such as the land on which the production facilities, warehouses, and office buildings were (or will be) constructed. The cost of the land is recorded and reported separately from the cost of buildings since the cost of the land is not depreciated.

Land improvements

Land improvements include parking lots, lighting, driveways, etc. These will be depreciated over their useful lives.

Buildings and improvements

The line buildings and improvements reports the cost of the buildings and improvements but not the cost of the land on which they were constructed. For financial statement purposes, the cost of buildings and improvements will be depreciated over their useful lives.

Machinery and equipment

The cost of a company’s production assets is reported on the balance sheet as equipment or as machinery and equipment. Since the machinery and equipment will not last forever, their cost is depreciated on the financial statements over their useful lives.

Furniture and fixtures

Furniture and fixtures reports the cost of these items. Their cost will be depreciated on the financial statements over their useful lives.

Construction in progress

The long-term asset construction in progress accumulates a company’s costs of constructing new buildings, additions, equipment, etc. Each project’s costs are accumulated separately and will be transferred to the appropriate property, plant, or equipment account when the asset is placed into service. At that point, the depreciation of the constructed asset will begin.

Accumulated depreciation

Accumulated depreciation reports the cumulative amount of depreciation that was recorded on the financial statements since the time that the depreciable assets were purchased and put into service. (The cost of land and the costs reported as construction in progress are not depreciated.)

The general ledger account Accumulated Depreciation will have a credit balance that grows larger when the current period’s depreciation is recorded. As the credit balance increases, the book (or carrying) value of these assets decreases.

You can learn more about depreciation expense and accumulated depreciation by visiting our Depreciation Explanation.

Intangible assets

Intangible assets are described as assets without physical substance. The intangible assets that were purchased (as opposed to the result of effective advertising, training, etc.) are reported on two long-term asset lines:

Goodwill

Goodwill is an intangible asset that is recorded when a company buys another business for an amount that is greater than the fair value of the identifiable assets. To illustrate, assume that a corporation pays $5 million to acquire a business that has tangible and identifiable intangible assets having a fair value of $4 million. The $1 million difference is recorded as the intangible asset goodwill.

Goodwill is assumed to have an indefinite useful life. Therefore, the recorded amount of goodwill is not amortized to expense. Instead, each year the recorded cost of the goodwill must be tested to see if the cost must be reduced by what is known as an impairment loss.

Other intangible assets

The line other intangible assets refers to intangible assets other than goodwill that were purchased from another party. Some examples include the following:

- Copyrights

- Mailing lists

- E-mail lists

- Trademarks

- Patents (including the cost of defending existing patents)

Except for trademarks, the amount paid to purchase any of these other intangible assets must be amortized to expense over the shorter of their expected useful life or their legal life.

Other assets

The noncurrent balance sheet item other assets reports the company’s deferred costs which will be charged to expense more than a year after the balance sheet date.

Liabilities

Liabilities are a company’s obligations (amounts owed). Their amounts appear on the company’s balance sheet if they:

- Are owed as the result of a past transaction

- Are owed as of the balance sheet date

- Include money received before it has been earned

Liabilities (and stockholders’ equity) are generally referred to as claims to a corporation’s assets. However, the claims of the liabilities come ahead of the stockholders’ claims.

Sometimes liabilities (and stockholders’ equity) are also thought of as sources of a corporation’s assets. For example, when a corporation borrows money from its bank, the bank loan was a source of the corporation’s assets, and the balance owed on the loan is a claim on the corporation’s assets.

A few examples of general ledger liability accounts include Accounts Payable, Short-term Loans Payable, Accrued Liabilities, Deferred Revenues, Bonds Payable, and many more.

The balance sheet reports two major categories or classifications of liabilities:

- Current liabilities

- Long-term liabilities

Current Liabilities

Current liabilities are a company’s obligations that will come due within one year of the balance sheet’s date and will require the use of a current asset or create another current liability. Current liabilities are sometimes known as short-term liabilities.

(If the company’s operating cycle is longer than one year, the length of the operating cycle determines whether a liability is reported as current or long-term.)

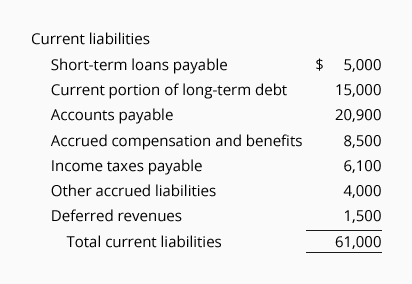

Examples of the descriptions used to report a company’s current liabilities include:

- Short-term loans payable

- Current portion of long-term debt

- Accounts payable

- Accrued compensation and benefits

- Income taxes payable

- Other accrued liabilities

- Deferred revenues

The order in which the current liabilities will appear on the balance sheet can vary. However, it is common to see three (listed in any order) at the top of the list: accounts payable, short-term loans payable, and the current portion of long-term debt.

Here is the current liability section from our sample balance sheets:

Short-term loans payable

A short-term loan payable is an obligation usually in the form of a formal written promise to pay the principal amount within one year of the balance sheet date. Interest is likely to be due monthly. Short-term loans payable could appear as notes payable or short-term debt.

For instance, if a company obtains a 6-month bank loan on December 31, 2025 for $100,000 and agrees to pay interest at the end of each month at the annual interest rate of 10%, the company’s balance sheet as of December 31, 2025 will report a current liability of $100,000. Since no interest is owed as of December 31, 2025, no liability for interest is reported on this balance sheet.

Current portion of long-term debt

The current portion of long-term debt is the amount of principal that must be paid within 12 months of the balance sheet date. (The principal amount that comes due after 12 months is reported as a noncurrent liability.)

To illustrate, assume that a corporation borrows $120,000 on December 31, 2025. The promissory note requires each month’s interest to be paid on the last day of each month. The note also requires the company to make annual principal payments of $40,000 on December 31 of 2026, 2027, and 2028. On the December 31, 2025 balance sheet, the corporation’s $120,000 of debt is reported as follows:

- A current liability (reported as current portion of long-term debt) of $40,000

- A long-term liability (reported as notes payable) of $80,000

Since no interest is payable on December 31, 2025, this balance sheet will not report a liability for interest on this loan.

Accounts payable

Accounts payable represents the amounts owed to vendors or suppliers for goods or services the company had received on credit. The amount is supported by the vendors’ invoices which had been received, approved for payment, and recorded in the company’s general ledger account Accounts Payable.

You can learn more by visiting our Accounts Payable Explanation.

Accrued compensation and benefits

The current liability accrued compensation and benefits reports the wages, salaries, bonuses, employers’ payroll taxes, and benefits that employees have earned as of the balance sheet date, but they have not yet been paid by the company.

Income taxes payable

The current liability described as income taxes payable is the amount of income taxes that a regular U.S. corporation must pay to the federal and state governments within one year of the balance sheet date. (Sole proprietorships, partnerships, and some corporations will not have income taxes payable since the business income is reported by the owners on their personal tax returns.)

Other accrued expenses and liabilities

Other accrued expenses and liabilities is a current liability that reports the amounts that a company has incurred (and therefore owes) other than the amounts already recorded in Accounts Payable.

Examples of accrued expenses include interest owed on loans payable, cost of electricity used (but the electric bill was not yet received), repair expenses that occurred at the end of the accounting period (but the repair bill was not yet processed), etc.

In order to issue a company’s financial statements on a timely basis, it may require using an estimated amount for the accrued expenses.

You can learn more about accrued expenses by visiting our Adjusting Entries Explanation.

Another item that could be included as part of other liabilities is the state and local sales and use taxes. To illustrate, assume a company sold $10,000 of merchandise that was subject to sales taxes of 8%. The retailer records this information in its general ledger accounts as follows:

- Debit Cash for $10,800

- Credit Sales for $10,000

- Credit the current liability Sales Taxes Payable for $800

Note that the sales taxes are not part of the company’s sales revenues. Instead, any sales taxes not yet remitted to the government are a current liability.

Deferred revenues

The current liability deferred revenues reports the amount of money a company received from a customer for future services or future shipments of goods. Until the company delivers the services or goods, the company has an obligation to deliver them or to refund the customer’s money. When they are delivered, the company will reduce this liability and increase its revenues.

Three examples of deferred (or unearned) revenues include:

- Deposits from customers for work to be done in a future accounting period

- Money received in advance by an insurance company for the next six months of insurance coverage

- Money received for gift cards that have not been redeemed as of the balance sheet date.

You can learn more about deferred revenues by visiting our Adjusting Entries Explanation.

Long-Term Liabilities

Long-term liabilities, which are also known as noncurrent liabilities, are obligations that are not due within one year of the balance sheet date.

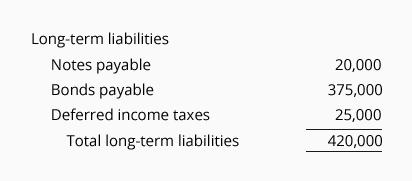

Three examples of long-term liabilities include:

- Notes payable

- Bonds payable

- Deferred income taxes

Here is the long-term liability section from our sample balance sheets:

Notes payable

When notes payable appears as a long-term liability, it is reporting the amount of loan principal that will not be payable within one year of the balance sheet date.

To illustrate, assume that a company signed a promissory note on December 31, 2025 for a loan of $120,000. The loan requires the interest to be paid at the end of every month. The loan’s principal of $120,000 is required to be paid as follows:

- On December 31, 2026, a principal payment of $40,000

- On December 31, 2027, a principal payment of $40,000

- On December 31, 2028, a principal payment of $40,000

The company’s December 31, 2025 balance sheet will report the $120,000 of principal owed as follows:

- The long-term liability notes payable will report $80,000. This is the total of the two principal payments due after December 31, 2026 (the payments due on December 31, 2027 and December 31, 2028).

- The current liability current portion of long-term debt will report $40,000. This is the principal payment due within one year of December 31, 2025 (the payment due on December 31, 2026).

The company’s December 31, 2026 balance sheet will report the remaining $80,000 of principal owed as follows:

- The long-term liability notes payable will report $40,000. This is the principal payment due after December 31, 2027 (the payment due on December 31, 2028).

- The current liability current portion of long-term debt will report $40,000. This is the principal payment due within one year of December 31, 2026 (the payment due on December 31, 2027).

Another example of a long-term liability is a mortgage loan for a company’s office building. (A mortgage loan is a loan secured by a lien on real estate.) Assuming the mortgage loan requires monthly payments of interest and principal, the total of the 12 loan principal payments following the date of the balance sheet will be reported as the current liability current portion of long-term debt. The principal balance remaining after those 12 principal payments is reported as the long-term liability mortgage loan payable. (For an example of this calculation, see our Business Form G-7 Current Portion of Long-term Debt.)

Bonds payable

Bonds payable are long-term debt securities issued by a corporation. Typically, bonds require the issuer to pay interest semi-annually (every six months) and the principal amount is to be repaid on the date that the bonds mature. It is common for bonds to mature (come due) 10-20 years after the bonds were issued.

A corporation that issues bonds will often have some balance sheet general ledger accounts associated with the bonds (Bonds Payable, Bond Issue Costs, Discount on Bonds Payable, Premium on Bonds). The balances in these accounts are likely combined into a single amount.

Any bond interest that has accrued but has not been paid as of the balance sheet date is reported as the current liability other accrued liabilities.

You can learn about bonds by visiting our Bonds Payable Explanation.

Deferred income taxes

Often the amount reported as the long-term liability deferred income taxes pertains to the difference between the amounts of depreciation expense reported on a regular U.S. corporation’s financial statements vs. the amounts of depreciation expense reported on the corporation’s income tax returns. The amount results from the timing of when the depreciation expense is reported.

Commitments and Contingencies

The final liability appearing on a company’s balance sheet is commitments and contingencies along with a reference to the notes to the financial statements. No amount is shown on the balance sheet for this item.

The notes for commitments and contingencies could include the following disclosures:

- A company’s guarantee of another party’s debt. In other words, the company will have a liability only if/when the other party fails to pay the amount owed.

- A lawsuit filed against the company and a loss is reasonably possible but not probable. (If a loss is probable and the amount can be estimated, the amount is to be reported as a liability on the face of the balance sheet.)

Stockholders’ Equity

If a business is organized as a corporation, the balance sheet section stockholders’ equity (or shareholders’ equity) is shown beneath the liabilities. The total amount of the stockholders’ equity section is the difference between the reported amount of assets and the reported amount of liabilities. Similar to liabilities, stockholders’ equity can be thought of as claims to (and sources of) the corporation’s assets.

(If the business is a sole proprietorship, this section appears as owner’s equity. We will discuss owner’s equity later.)

The stockholders’ equity section will report the following items as separate amounts:

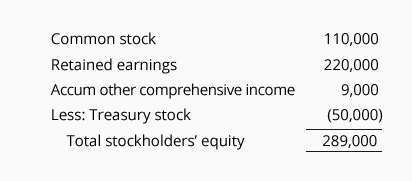

Here is the stockholders’ equity section from our sample balance sheets:

Common stock

Common stock reports the amount a corporation received when the shares of its common stock were first issued.

NOTE: Some of the states in the U.S. require that a corporation’s shares of common stock have a par value. If so, the amount the corporation received when the shares were issued is divided between two lines that are reported within the stockholders’ equity section:

- Common stock – par value

- Common stock – amount in excess of par value

A relatively small percent of corporations will issue preferred stock in addition to their common stock. The amount received from issuing these shares will be reported separately in the stockholders’ equity section.

The amount the corporation received from issuing shares of stock is referred to as paid-in capital and as permanent capital.

Retained earnings

For many successful corporations, the largest amount in the stockholders’ equity section of the balance sheet is retained earnings. Retained earnings is the cumulative amount of 1) its earnings minus 2) the dividends it declared from the time the corporation was formed until the balance sheet date.

It is important to realize that the amount of retained earnings will not be in the corporation’s bank accounts. The reason is that corporations will likely use the cash generated from its earnings to purchase productive assets, reduce debt, purchase shares of its common stock from existing stockholders, etc.

Accumulated other comprehensive income

The stockholders’ equity section may include an amount described as accumulated other comprehensive income. This amount is the cumulative total of the amounts that had been reported over the years as other comprehensive income (or loss).

Three examples of other comprehensive income (or loss) that resulted in the amount reported in the stockholders’ equity section as accumulated other comprehensive income are:

- Foreign currency translation adjustments

- Unrealized gains/losses on hedge/derivative financial instruments

- Unrealized gains/losses on postretirement benefit plans

Treasury stock

Treasury stock is a subtraction within stockholders’ equity for the amount the corporation spent to purchase its own shares of stock (and the shares have not been retired).

When the corporation purchases shares of its stock, the corporation’s cash declines, and the amount of stockholders’ equity declines by the same amount. Hence, the cumulative cost of the treasury stock appears in parentheses.

NOTE: One of the financial statements issued by a corporation is the statement of stockholders’ equity. This financial statement summarizes the changes in the components of stockholders’ equity for each of the most recent three years.

You can learn more about the components of stockholders’ equity by visiting our Stockholders’ Equity Explanation.

Owner’s Equity

Since our sample balance sheets focused on the stockholders’ equity section of a corporation, we want to discuss the comparable section for a business organized as a sole proprietorship.

The balance sheet of a sole proprietorship will report owner’s equity instead of a corporation’s stockholders’ equity. Hence, a sole proprietorship’s balance sheet will resemble the accounting equation: assets = liabilities + owner’s equity.

The owner’s equity section of a sole proprietorship owned by J. Ott will have two general ledger accounts in which amounts are recorded:

- J. Ott, Capital

- J. Ott, Drawing

The account J. Ott, Capital is the main owner’s equity account. Its balance is carried forward to the following year.

The account J. Ott, Drawing is used to record the owner’s withdrawals of cash (or other assets) during the accounting year. The owner’s draws are not reported as an expense on the company’s income statement, but they do cause a decrease in the owner’s capital. (At the end of the accounting year, a closing entry transfers the debit balance in J. Ott, Drawing to the account J. Ott, Capital.)

Reasons for the Change in Owner’s Equity

Typically, the change in the amount of owner’s equity for a sole proprietorship business is the result of:

- The owner personally investing money in the business

- The owner withdrawing money from the business for personal use

- The company earning revenues (and/or gains)

- The company incurring expenses (and/or losses)

The combination of the last two bullet points is the amount of the company’s net income.

How the Balance Sheet and Income Statement Are Connected

The account Retained Earnings provides the connection between the balance sheet and the income statement.

How revenues affect retained earnings

When revenues and gains are earned by a corporation, they have the effect of immediately increasing the corporation’s retained earnings. This is true even though they are not directly recorded in the Retained Earnings account at the time they are earned.

To illustrate, let’s examine what occurs when a company earns revenues by providing services on credit:

- The asset account Accounts Receivable is increased.

- An income statement account such as Revenues Earned is increased. However, when revenues are earned, they have the immediate effect of increasing the corporation’s retained earnings. This is true, even if the balance in the Revenues Earned account is transferred to the Retained Earnings account only at the end of the accounting year.

How expenses affect retained earnings

When a corporation incurs expenses and losses, they have the effect of immediately decreasing the corporation’s retained earnings. This is true, even though they are not directly recorded in the Retained Earnings account at the time the expenses or losses occurred. To illustrate, assume a corporation issues monthly income statements and it pays each month’s rent on the first day of the month. Here is what occurs:

- The asset account Cash is decreased.

- The income statement account Rent Expense is increased. However, as the expense is occurring, the immediate effect is to decrease the corporation’s retained earnings. This is true, even if the balance in the Rent Expense account is transferred to the Retained Earnings account only at the end of the accounting year.

Notes To the Financial Statements

The notes to the financial statements are an integral (essential) part of the balance sheet. To communicate this, there will be a notation on the face of the balance sheet that states “See notes to the financial statements.” or “The accompanying notes to the financial statements are an integral part of this statement.”

The notes to the financial statement are required by the accounting principle known as the full disclosure principle and will include the following:

- Summary of significant accounting policies is the first note. It describes the use of estimates, revenue recognition, inventories, property and equipment, goodwill and other intangible assets, effects of recent accounting rules from the FASB, and more.

- Schedules of amounts and other details for inventories, accrued liabilities, income taxes, employee benefit plans, leases, stock options, commitments, contingencies, related party transactions, assets pledged as collateral, and more.

NOTE: U.S. corporations whose common stock is traded on a stock exchange are required to file an annual report with the Securities and Exchange Commission (SEC). The report known as Form 10-K contains the complete set of the corporation’s financial statements with notes plus it has additional information concerning the corporation’s financial position, liquidity, operations, risks, etc.

You can access a corporation’s Form 10-K by going to the Investor Relations section of the corporation’s website.

Making Sure Your Company’s Balance Sheet Is Accurate

Before issuing a balance sheet, it is wise to do a final review of the amounts being reported. Here are some steps we recommend:

- Compare the amounts to the amounts reported on earlier balance sheets.

- Make certain that the balance sheet amounts agree with the supporting workpapers and other documentation. Here are some examples along with links to the related Explanations found on AccountingCoach:

- The amount of cash and cash equivalents should be supported by bank reconciliations for the company’s bank accounts. You can learn more by visiting our Bank Reconciliation Explanation.

- Accounts receivable – net should be compared to an aging of accounts receivable. You can learn more by visiting our Accounts Receivable and Bad Debts Expense Explanation.

- Inventory should be supported by a schedule of calculations to support the cost reported as inventory. You can learn more by visiting our Inventory and Cost of Goods Sold Explanation.

- The amount of prepaid expenses should agree with workpapers showing the calculations of the amounts that had been paid in advance and are still prepaid as of the date of the balance sheet. You can learn more by visiting our Adjusting Entries Explanation.

- Accounts payable should be supported by a listing of amounts owed. You can learn more by visiting our Accounts Payable Explanation.

- Accrued liabilities should agree with workpapers showing the calculation of the amounts owed but have not yet been recorded. You can learn more by visiting our Adjusting Entries Explanation.

- Deferred revenues should be supported by a workpaper documenting the amounts received from customers in advance but have not yet been earned. You can learn more by visiting our Adjusting Entries Explanation.

Monitoring Your Company’s Financial Position

Determining a company’s liquidity

A critical need for small (and all) businesses is having sufficient money on hand to meet their payroll and to pay the other obligations when they come due. This is associated with the term liquidity, which is often assessed by comparing a company’s current assets to its current liabilities. In our Working Capital and Liquidity Explanation we discuss this and the following financial ratios in detail:

- Working capital which is the amount of current assets minus the amount of current liabilities.

- Current ratio which is the amount of current assets divided by the amount of current liabilities.

- Quick ratio which is similar to the current ratio except that inventory and prepaid expenses are excluded from the amount of current assets. The quick ratio is also known as the acid-test ratio.

- Receivables turnover ratio which is the amount of sales on credit for a year divided by the average balance in accounts receivable during the year. A related financial ratio is the days’ sales in receivables (average collection period).

- Inventory turnover ratio which is the cost of goods sold for a year divided by the average cost of inventory during the year. A related financial ratio is the days’ sales in inventory (days to sell).

The two “turnover” ratios in the above list highlight that it is not sufficient to merely have accounts receivable and inventory. These current assets must also be converted to cash in time to pay the company’s obligations when they come due.

Of course, the company must have practices and procedures to assure that credit is granted only to credit worthy customers, that accounts receivable are monitored and collected when due, that inventory levels are managed, and that internal controls are in place to safeguard all assets.

Determining a company’s ability to obtain long-term loans

The balance sheet also provides information on a corporation’s ability to obtain long-term loans. For instance, if a corporation has a large amount of debt (the combination of current and long-term liabilities) compared to the amount of its stockholders’ equity, the corporation is said to be highly leveraged. A high level of financial leverage may be viewed by lenders as a high level of risk.

Here are two financial ratios which are often used for determining the level of a corporation’s financial leverage:

- Debt to equity ratio which compares a corporation’s total debt (current liabilities + long-term liabilities) to the amount of stockholders’ equity.

- Debt to total assets ratio which compares a corporation’s total debt to the total amount of its assets.

If a corporation is highly leveraged, a lender may not be interested in making new or additional loans to the corporation.

Of course, lenders will also examine other financial information including:

- The corporation’s notes to its financial statements

- The corporation’s income statements

- The corporation’s statements of cash flows

Issuing additional common stock or additional bonds

Some corporations may be able to issue additional shares of their common stock and/or to issue bonds to obtain money for purchasing long-term assets, expanding operations, reducing the amount of its short-term debt, etc.

Issuing shares of common stock has advantages and disadvantages:

- It has the advantage of increasing the amount of stockholders’ equity thereby reducing the corporation’s degree of financial leverage. The reduction in financial leverage could also allow the corporation to obtain additional loans.

- It has the disadvantage of diluting an existing stockholder’s percent of ownership in the corporation.

Issuing bonds also has advantages and disadvantages:

- One advantage of bonds is their low cost since the interest paid to the bondholders will be a deductible expense on the income tax return of a profitable corporation. Another advantage is that an existing stockholder’s percent of ownership is not reduced.

- A disadvantage of bonds is the increase in the corporation’s liabilities, thereby increasing the corporation’s financial leverage. This will be interpreted to mean additional risk.

Some Limitations of the Balance Sheet

Some assets are not included

Due to the accounting principle known as the cost principle (or historical cost principle), some valuable trademarks developed internally by a company are not reported as assets on its balance sheet. For example, the internationally recognized trademarks developed by Coca-Cola and Nike might be among their most valuable assets. However, these trademarks are not reported on their balance sheets since they were not purchased in a transaction with another party.

NOTE: If a company purchases a brand name and trademark from another business at a cost of $1 million, this cost will be recorded by the company at the time of the transaction. So long as there is no impairment to the brand, the $1 million cost will be reported on the company’s future balance sheets.

However, if the same company creates and develops a successful, valuable brand and trademark through its astute marketing, those marketing costs are expensed when they occur. As a result, this valuable brand name and trademark will not be reported as assets on the company’s balance sheets.

Similarly, the cost principle prevents a company’s balance sheet from including the value of its highly effective management, its research team, customer allegiance, unique marketing strategies, etc.

Balance Sheet Should Be Read With the Other Financial Statements

A corporation’s balance sheet and the notes to the financial statements should be read along with the corporation’s other financial statements:

The FASB’s Highlights of FASB’s Statement of Financial Accounting Concepts No. 5 (issued in 1984) states, “no one financial statement is likely to provide all the financial statement information that is useful for a particular kind of decision.”

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Balance Sheet materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.

Earn Our Certificate

for This Topic

When you join PRO, you will receive instant access to 16 different Certificates of Achievement plus our Bookkeeping Certificate of Excellence.

View PRO Features