We Make Accounting Easy for Anyone

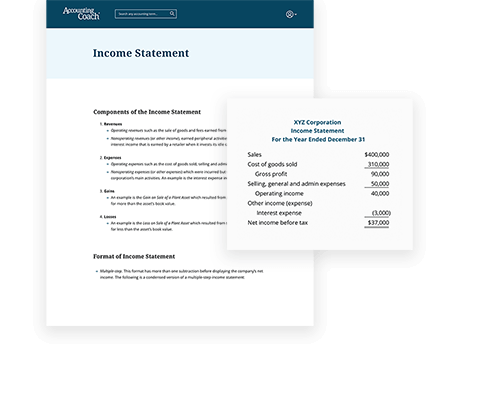

Explanations

Our Explanations simplify the most important accounting topics in a way that's clear, straight-to-the-point, and easy to understand. With more than 25 years of teaching experience, Harold brings accounting to life by combining theory with real-world examples and stories.

View All Explanations

Practice Quizzes

Our Practice Quizzes will help you assess your understanding of each Explanation and improve your retention. These are a great warm-up for our Quick Tests which contain more than 1,800 questions with solutions.

View All Quizzes

Q&A

We have answered more than 1,100 of the most common accounting and bookkeeping questions. You can browse all of our Q&A by topic or search for a specific question by using the search box found at the top of each page.

View All Q&A

Crosswords and Word Scrambles

Our Crossword Puzzles and Word Scrambles will help you learn, review, and retain important terminology for each accounting topic in a fun way.

View All Crosswords View All Word Scrambles

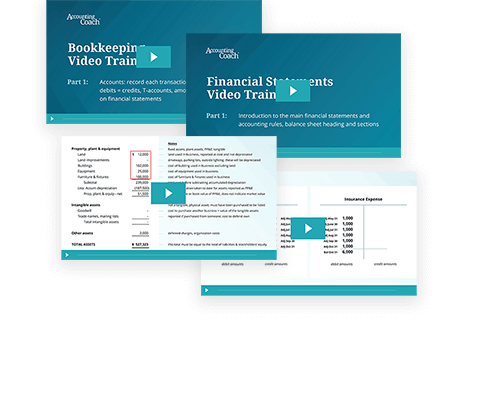

Video Training

Our Bookkeeping Video Training (13 videos) will help you build confidence as you increase your understanding of debits and credits, adjusting entries, transactions, and more.

Our Financial Statements Video Training (14 videos) will walk you through the balance sheet, income statement, and cash flow statement.

View All PRO Features

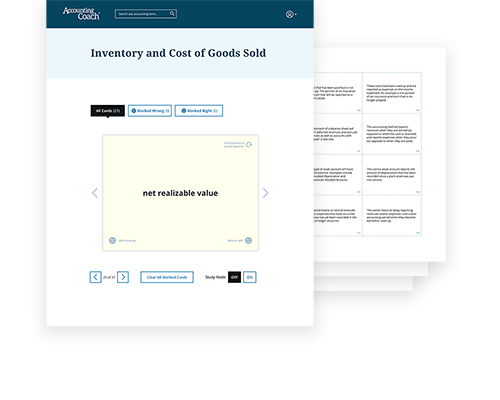

Flashcards

Our Flashcards will provide you with crystal-clear accounting definitions so you can master complex terminology faster and easier. All 500+ total flashcards are available in both digital and printable format.

View All PRO Features

Visual Tutorials

Our Visual Tutorials are perfect for people who get overwhelmed studying jargon-filled accounting textbooks. Follow along step-by-step and we'll explain the most important accounting topics in a more intuitive away.

View All PRO Features

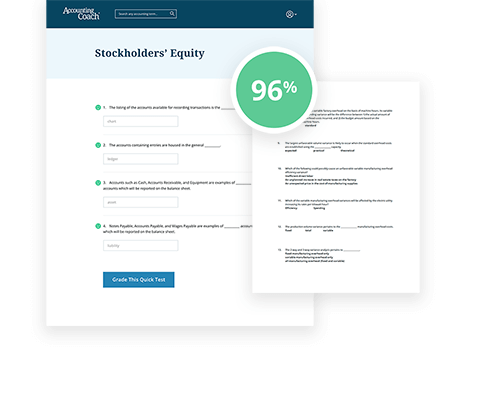

Quick Tests

Our 70+ Quick Tests give you immediate feedback on what you know and what you don't know. The more than 1,800 test questions will improve your retention and help you go from memorizing to understanding.

View All PRO Features

Cheat Sheets

Our Cheat Sheets offer a great way to quickly review the most important key points for each topic. They will help you study each topic faster and remember the most important concepts.

View All PRO Features

Printable PDFs

We have meticulously converted our entire collection of materials into high-quality PDF files so you can download and print all of our content. They are great for studying and reviewing offline at your convenience.

View All PRO Features

Business Forms

Our real-world business forms include helpful instructions and filled-in examples that are designed to help you understand accounting in yet another way. Each of our 80+ forms are available in both Excel and PDF format.

View All PRO Features

Progress Tracking

Our intuitive progress tracking will help you visualize your current progress and pick up where you left off. This is perfect for busy individuals that prefer to learn at their own pace.

View All PRO FeaturesBadges and Points

Our badges and points will help you stay motivated and celebrate your achievements. Earn our unique badges and points as you track your progress and complete various milestones.

View All PRO Plus Features

Certificates

Receive our official Certificates of Achievement after you pass each of our 10 certificate exams. Earning our certificates will help improve your credentials, enhance your portfolio, boost your confidence for a job interview, and allow you to share your achievements online.

View All PRO Plus Features