Introduction

Bonds are a form of long-term debt. You might think of a bond as an IOU issued by a corporation and purchased by an investor for cash. The corporation issuing the bond is borrowing money from an investor who becomes a lender and bondholder.

A bond is a formal contract that requires the issuing corporation to pay the bondholders

- Interest every six months based on the bond’s stated interest rate, and

- The principal or face amount on the bond’s maturity date.

There are two significant advantages for a corporation to issue bonds instead of common stock:

- Bonds will not dilute the ownership interest of the stockholders, and

- Bonds have a lower cost than common stock.

Bonds have a lower cost than common stock because of the bond’s formal contract to pay the interest and principal payments to the bondholders and to adhere to other conditions. A second reason for bonds having a lower cost is that the bond interest paid by the issuing corporation is deductible on its U.S. income tax return, whereas dividends are not tax deductible.

The market value of an existing bond will fluctuate with changes in the market interest rates and with changes in the financial condition of the corporation that issued the bond. For example, an existing bond that promises to pay 9% interest for the next 20 years will become less valuable if market interest rates rise to 10%. Likewise, a 9% bond will become more valuable if market interest rates decrease to 8%. When the financial condition of the issuing corporation deteriorates, the market value of the bond is likely to decline as well.

Present value calculations are used to determine a bond’s market value and to calculate the true or effective interest rate paid by the corporation and earned by the investor. Present value calculations discount a bond’s fixed cash payments of interest and principal by the market interest rate for the bond.

WATCH NOW

Advance Your Career with Our PRO Training

Bond Interest and Principal Payments

When a corporation issues a bond, it promises to pay the bondholder

- Interest every six months at the bond’s stated interest rate, and

- The principal or face amount when the bond comes due at its maturity date.

Bond Interest Payments

Normally, a bond’s interest payments occur semiannually. This means that the corporation issuing a bond will pay to the bondholders one-half of the annual interest at the end of each six-month period as long as the bond is outstanding. The formula for calculating the semiannual interest payments is:

Face Amount of the Bond x Stated Annual Interest Rate x 6/12 of a Year

The following terms mean the same as a bond’s stated interest rate:

- face interest rate

- nominal interest rate

- coupon interest rate

- contractual interest rate

Throughout our explanation of bonds payable we will use the term stated interest rate or stated rate. Usually a bond’s stated interest rate is fixed or locked-in for the life of the bond.

Bond Principal Payment

A bond’s principal payment is the dollar amount that appears on the face of a bond. This is the amount that the issuing corporation must pay to the bondholders on the date that a bond matures or comes due. Here are some names that refer to a bond’s principal amount:

- face value

- par or par value

- maturity value or maturity amount

- stated value

Throughout our explanation we will use these terms interchangeably. In addition, we assume that the bond’s principal amount will be due on a single date.

Timeline for Interest and Principal Payments

It is helpful to prepare a timeline to visualize the cash payments that a corporation promises to pay its bondholders. The following timeline presents the cash payments of interest and principal for a 9% $100,000 bond maturing in 5 years:

As the timeline indicates, the corporation will pay its bondholders 10 semiannual interest payments of $4,500 ($100,000 x 9% x 6/12 of a year). Each of the interest payments occurs at the end of each of the 10 six-month time periods. When the bond matures at the end of the 10th six-month period, the corporation must make the $100,000 principal payment to its bondholders.

Keep in mind that a bond’s stated cash amounts—the ones shown in our timeline—will not change during the life of the bond.

Accrued Interest

Since the corporation issuing a bond is required to pay interest, and since the interest is paid on only two dates per year, the interest on a bond will be accruing daily. This means for each day that a bond is outstanding, the corporation will incur one day of interest expense and will have a liability for the interest it has incurred but has not paid. If the corporation has issued a 9% $100,000 bond, then each day it will have interest expense of $24.66 ($100,000 x 9% x 1/365).

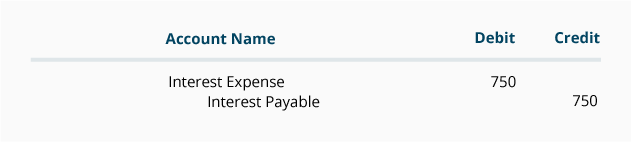

If the corporation issues monthly financial statements, then each month it needs to report $750 ($100,000 x 9% x 1/12) of interest expense. The corporation usually does this with the following monthly adjusting entry:

While the issuing corporation is incurring interest expense of $24.66 per day on the 9% $100,000 bond, the bondholders will be earning interest revenue of $24.66 per day. With bondholders buying and selling their bond investments on any given day, there needs to be a mechanism to compensate each bondholder for the interest earned during the days a bond was held. The accepted technique is for the buyer of a bond to pay the seller of the bond the amount of interest that has accrued as of the date of the sale. For example, if a 9% $100,000 bond has a date of January 1, 2025 and it is sold on January 31, 2025, the buyer of the bond is required to pay the seller of the bond one month’s interest amounting to $750 ($100,000 x 9% x 1/12).

Bonds Issued at Par with No Accrued Interest

If a corporation issues a bond on January 1, 2025 and the bond has a date of January 1, 2025 there will be no accrued interest on the bond when it is issued. If the investor pays the corporation the face amount of the bond, the bond is said to have been issued at par or at 100—meaning 100% of the bond’s face value plus any accrued interest. (As we will see later, it is possible for a new bond to be issued after the date of the bond—and therefore to have accrued interest. In addition a bond might be sold by the issuing corporation for more or less than its face value.)

Let’s assume that on January 1, 2025 a corporation issues a 9% $100,000 bond at its face amount. The bond is dated January 1, 2025 and requires interest payments on each June 30 and December 31 until the bond matures at the end of 5 years. Each semiannual interest payment will be $4,500 ($100,000 x 9% x 6/12). The corporation is also required to pay $100,000 of principal to the bondholders on the bond’s maturity date of December 31, 2029.

Since the bond was issued/sold for 100% of its face amount and since there is no accrued interest to be paid by the buyer of the bond, the issuing corporation will make the following journal entry:

The following timeline shows the future cash payments that the corporation must make to the bondholders:

Journal Entries for Interest Expense – Annual Financial Statements

If the corporation issuing the above bond has an accounting year ending on December 31, the corporation will incur twelve months of interest expense in each of the years that the bonds are outstanding. In other words, under the accrual basis of accounting, this bond will require the issuing corporation to report Interest Expense of $9,000 ($100,000 x 9%) per year.

If the corporation issues only annual financial statements, the interest expense can be recorded at the time of its semiannual interest payments, as shown in the following journal entries for the year 2025:

Journal Entries for Interest Expense – Monthly Financial Statements

If the corporation issues monthly financial statements, it must report interest expense of $750 ($100,000 x 9% x 1/12) on each of its monthly income statements. It must also report a current liability on its balance sheet for the amount of interest that it has incurred but has not yet paid. This is accomplished by recording an accrual adjusting entry at the end of each month. In addition there will be an entry on June 30 and on December 31 for the required interest that was actually paid to the bondholders. The 14 journal entries pertaining to the corporation’s bond interest during the year 2025 will be:

The journal entries for the years 2026 through 2029 will have the same accounts and amounts.

Bonds Issued at Par with Accrued Interest

If a corporation has prepared a bond with a date of January 1, 2025 but delays issuing the bond until February 1, the investors buying the bonds on February 1 will have to pay the issuing corporation one month of accrued interest. (The delay may have been caused by a turbulent financial market or some other situation.)

Let’s illustrate this scenario with a corporation preparing to issue a 9% $100,000 bond dated January 1, 2025. The bond will mature in 5 years and requires interest payments on June 30 and December 31 of each year until December 31, 2029. The bond is issued on February 1 at its par value plus accrued interest.

Since the bond was sold to investors at par, the issuing corporation will receive 100% of the bond’s face value plus one month of accrued interest. The accrued interest amounts to $750 ($100,000 x 9% x 1/12). In total the issuing corporation will receive $100,750. The journal entry for this transaction is:

Note that the total amount received is debited to the Cash account and the bond’s face amount is credited to Bonds Payable. The $750 received by the corporation for the accrued interest is credited to Interest Payable. The corporation is receiving the $750 because the corporation is required to pay the bondholders $4,500 ($100,000 x 9% x 6/12) on June 30. The difference between the $4,500 paid on June 30 and the $750 received on February 1, 2025 is $3,750—equal to five months of interest for the months of February through June: $100,000 x 9% x 5/12.

Journal Entries for Interest Expense – Annual Financial Statements

If a corporation that is planning to issue a bond dated January 1, 2025 delays issuing the bond until February 1, the corporation will not have interest expense during January. Assuming the corporation has an accounting year that ends on December 31, it will have eleven months of interest expense during the year 2025. During each of the subsequent years 2026, 2027, 2028, and 2029 the corporation will have twelve months of interest expense equal to $9,000 ($100,000 x 9% x 12/12).

If the corporation issues only annual financial statements, its journal entries for its interest payments during the year 2025 will be:

Note that the total amount of interest expense in 2025 will be $8,250 ($3,750 recorded on June 30 + $4,500 recorded on December 31). This amount of interest expense for February 1 through December 31, 2025 is confirmed by the following calculation: $100,000 x 9% x 11/12 = $8,250.

In the year 2026, the journal entries will be:

In the year 2026, the interest expense will be $9,000 ($4,500 + $4,500 = $9,000; or $100,000 x 9% = $9,000) because the bond will be outstanding for a full year. The entries will be similar for the years 2027, 2028, and 2029.

Journal Entries for Interest Expense – Monthly Financial Statements

If monthly financial statements are issued by the corporation, the following journal entries are needed in the year 2025 (including the entry when the bonds were issued on February 1, 2025):

Note that in 2025 the corporation’s entries included 11 monthly adjusting entries to accrue $750 of interest expense plus the June 30 and December 31 entries to record the semiannual interest payments. As a result of these journal entries, each monthly income statement will report one month of interest expense and the balance sheet will report a current liability for the amount of interest incurred by the corporation but not yet paid to the bondholders.

In each of the years 2026 through 2029 there will be 12 monthly entries of $750 each plus the June 30 and December 31 entries for the $4,500 interest payments.

Market Interest Rates and Bond Prices

Once a bond is issued the issuing corporation must pay to the bondholders the bond’s stated interest for the life of the bond. While the bond’s stated interest rate will not change, the market interest rate will be constantly changing due to global events, perceptions about inflation, and many other factors which occur both inside and outside of the corporation.

The following terms are often used to mean market interest rate:

- effective interest rate

- yield to maturity

- discount rate

- desired rate

When Market Interest Rates Increase

Market interest rates are likely to increase when bond investors believe that inflation will occur. As a result, bond investors will demand to earn higher interest rates. The investors fear that when their bond investment matures, they will be repaid with dollars of significantly less purchasing power.

Let’s examine the effects of higher market interest rates on an existing bond by first assuming that a corporation issued a 9% $100,000 bond when the market interest rate was also 9%. Since the bond’s stated interest rate of 9% was the same as the market interest rate of 9%, the bond should have sold for $100,000.

Next, let’s assume that after the bond had been sold to investors, the market interest rate increased to 10%. The issuing corporation is required to pay only $4,500 of interest every six months as promised in its bond agreement ($100,000 x 9% x 6/12) and the bondholder is required to accept $4,500 every six months. However, the market will demand that new bonds of $100,000 pay $5,000 every six months (market interest rate of 10% x $100,000 x 6/12 of a year). The existing bond’s semiannual interest of $4,500 is $500 less than the interest required from a new bond. Obviously the existing bond paying 9% interest in a market that requires 10% will see its value decline.

Here’s a Tip

An existing bond’s market value will decrease when the market interest rates increase.The reason is that an existing bond’s fixed interest payments are smaller than the interest payments now demanded by the market.

When Market Interest Rates Decrease

Market interest rates are likely to decrease when there is a slowdown in economic activity. In other words, the loss of purchasing power due to inflation is reduced and therefore the risk of owning a bond is reduced.

Let’s examine the effect of a decrease in the market interest rates. First, let’s assume that a corporation issued a 9% $100,000 bond when the market interest rate was also 9% and therefore the bond sold for its face value of $100,000.

Next, let’s assume that after the bond had been sold to investors, the market interest rate decreased to 8%. The corporation must continue to pay $4,500 of interest every six months as promised in its bond agreement ($100,000 x 9% x 6/12) and the bondholder will receive $4,500 every six months. Since the market is now demanding only $4,000 every six months (market interest rate of 8% x $100,000 x 6/12 of a year) and the existing bond is paying $4,500, the existing bond will become more valuable. In other words, the additional $500 every six months for the life of the 9% bond will mean the bond will have a market value that is greater than $100,000.

Here’s a Tip

An existing bond’s market value will increase when the market interest rates decrease. An existing bond becomes more valuable because its fixed interest payments are larger than the interest payments currently demanded by the market.

Relationship Between Market Interest Rates and a Bond’s Market Value

As we had seen, the market value of an existing bond will move in the opposite direction of the change in market interest rates.

- When market interest rates increase, the market value of an existing bond decreases.

- When market interest rates decrease, the market value of an existing bond increases.

- The relationship between market interest rates and the market value of a bond is referred to as an inverse relationship. Perhaps you have heard or read financial news that stated “Bond prices and bond yields move in opposite directions” or “Bond prices rallied, lowering their yield…” or “The rise in interest rates caused the price of bonds to fall.”

If you were the treasurer of a large corporation and could predict interest rates, you would…

- Issue bonds prior to market interest rates increasing in order to lock-in smaller interest payments.

If you were an investor and could predict interest rates, you would…

- Purchase bonds prior to market interest rates dropping. You would do this in order to receive the relatively high current interest amounts for the life of the bonds. (However, be aware that bonds are often callable by the issuer.)

- Sell bonds that you own before market interest rates rise. You would do this because you don’t want to be locked-in to your bond’s current interest amounts when higher rates and amounts will be available soon.

Bond Premium with Straight-Line Amortization

When a corporation prepares to issue/sell a bond to investors, the corporation might anticipate that the appropriate interest rate will be 9%. If the investors are willing to accept the 9% interest rate, the bond will sell for its face value. If however, the market interest rate is less than 9% when the bond is issued, the corporation will receive more than the face amount of the bond. The amount received for the bond (excluding accrued interest) that is in excess of the bond’s face amount is known as the premium on bonds payable, bond premium, or premium.

To illustrate the premium on bonds payable, let’s assume that in early December 2024, a corporation has prepared a $100,000 bond with a stated interest rate of 9% per annum (9% per year). The bond is dated as of January 1, 2025 and has a maturity date of December 31, 2029. The bond’s interest payment dates are June 30 and December 31 of each year. This means that the corporation will be required to make semiannual interest payments of $4,500 ($100,000 x 9% x 6/12).

Let’s assume that just prior to selling the bond on January 1, the market interest rate for this bond drops to 8%. Rather than changing the bond’s stated interest rate to 8%, the corporation proceeds to issue the 9% bond on January 1, 2025. Since this 9% bond will be sold when the market interest rate is 8%, the corporation will receive more than the bond’s face value.

Let’s assume that this 9% bond being issued in an 8% market will sell for $104,100 plus $0 accrued interest. The corporation’s journal entry to record the issuance of the bond on January 1, 2025 will be:

The account Premium on Bonds Payable is a liability account that will always appear on the balance sheet with the account Bonds Payable. In other words, if the bonds are a long-term liability, both Bonds Payable and Premium on Bonds Payable will be reported on the balance sheet as long-term liabilities. The combination of these two accounts is known as the book value or carrying value of the bonds. On January 1, 2025 the book value of this bond is $104,100 ($100,000 credit balance in Bonds Payable + $4,100 credit balance in Premium on Bonds Payable).

Premium on Bonds Payable with Straight-Line Amortization

Over the life of the bond, the balance in the account Premium on Bonds Payable must be reduced to $0. In our example, the bond premium of $4,100 must be reduced to $0 during the bond’s 5-year life. By reducing the bond premium to $0, the bond’s book value will be decreasing from $104,100 on January 1, 2025 to $100,000 when the bonds mature on December 31, 2029. Reducing the bond premium in a logical and systematic manner is referred to as amortization.

The bond premium of $4,100 was received by the corporation because its interest payments to the bondholders will be greater than the amount demanded by the market interest rates. Therefore, the amortization of the bond premium will involve the account Interest Expense. Each accounting period during the life of the bond there needs to be a credit to Interest Expense and a debit to Premium on Bonds Payable. In this section we will illustrate the straight-line method of amortization. (In a later section we will illustrate the effective interest rate method.)

Straight-Line Amortization of Bond Premium on Annual Financial Statements

If a corporation issues only annual financial statements and its accounting year ends on December 31, the amortization of the bond premium can be recorded once each year. In the case of the 9% $100,000 bond issued for $104,100 and maturing in 5 years, the annual straight-line amortization of the bond premium will be $820 ($4,100 divided by 5 years).

However, when a corporation issues only annual financial statements, the amortization of the bond premium is often recorded at the time of its semiannual interest payments. Under this assumption the journal entries on June 30 and December 31 will be:

The combination of the interest payments and the bond amortization results in the net amount of $8,180 ($4,500 of interest paid on June 30 + $4,500 of interest paid on December 31 minus $410 of amortization on June 30 and minus $410 of amortization on December 31). This $8,180 will be reported in the account Interest Expense for the year 2025 as shown in the following T-account:

The following T-account shows how the balance in the account Premium on Bonds Payable will decrease over the 5-year life of the bonds under the straight-line method of amortization.

The following table shows how the bond’s book value will decrease from $104,100 to the bond’s maturity amount of $100,000:

Straight-Line Amortization of Bond Premium on Monthly Financial Statements

If monthly financial statements are issued, the straight-line amortization of the bond premium will be $68.33 per month ($4,100 of bond premium divided by the bond’s life of 60 months). Below are the 12 monthly entries for the amortization plus the June 30 and December 31 payments of semiannual interest during the year 2025:

The journal entries for the years 2026 through 2029 will be similar if all of the bonds remain outstanding.

Bond Discount with Straight-Line Amortization

When a corporation is preparing a bond to be issued/sold to investors, it may have to anticipate the interest rate to appear on the face of the bond and in its legal contract. Let’s assume that the corporation prepares a $100,000 bond with an interest rate of 9%. Just prior to issuing the bond, a financial crisis occurs and the market interest rate for this type of bond increases to 10%. If the corporation goes forward and sells its 9% bond in the 10% market, it will receive less than $100,000. When a bond is sold for less than its face amount, it is said to have been sold at a discount. The discount is the difference between the amount received (excluding accrued interest) and the bond’s face amount. The difference is known by the terms discount on bonds payable, bond discount, or discount.

To illustrate the discount on bonds payable, let’s assume that in early December 2024 a corporation prepares a 9% $100,000 bond dated January 1, 2025. The interest payments of $4,500 ($100,000 x 9% x 6/12) will be required on each June 30 and December 31 until the bond matures on December 31, 2029.

Next, let’s assume that just prior to offering the bond to investors on January 1, the market interest rate for this bond increases to 10%. The corporation decides to sell the 9% bond rather than changing the bond documents to the market interest rate. Since the corporation is selling its 9% bond in a bond market which is demanding 10%, the corporation will receive less than the bond’s face amount.

To illustrate the accounting for bonds payable issued at a discount, let’s assume that the 9% bond is sold in the 10% market for $96,149 plus $0 accrued interest on January 1, 2025. The corporation’s journal entry to record the sale of the bond will be:

The account Discount on Bonds Payable (or Bond Discount or Unamortized Bond Discount) is a contra liability account since it will have a debit balance. Discount on Bonds Payable will always appear on the balance sheet with the account Bonds Payable. In other words, if the bond is a long-term liability, both Bonds Payable and Discount on Bonds Payable will be reported on the balance sheet as long-term liabilities. The combination or net of these two accounts is known as the book value or the carrying value of the bonds. On January 1, 2025 the book value of this bond is $96,149 (the $100,000 credit balance in Bonds Payable minus the debit balance of $3,851 in Discount on Bonds Payable.)

Discount on Bonds Payable with Straight-Line Amortization

Over the life of the bond, the balance in the account Discount on Bonds Payable must be reduced to $0. Reducing this account balance in a logical manner is known as amortizing or amortization. Since a bond’s discount is caused by the difference between a bond’s stated interest rate and the market interest rate, the journal entry for amortizing the discount will involve the account Interest Expense.

In our example, the bond discount of $3,851 results from the corporation receiving only $96,149 from investors, but having to pay the investors $100,000 on the date that the bond matures. The discount of $3,851 is treated as an additional interest expense over the life of the bonds. When the same amount of bond discount is recorded each year, it is referred to as straight-line amortization. In this example, the straight-line amortization would be $770.20 ($3,851 divided by the 5-year life of the bond).

Straight-Line Amortization of Bond Discount on Annual Financial Statements

If a corporation issues only annual financial statements on December 31, the amortization of bond discount is often recorded at the time of its semiannual interest payments. In our example the journal entries for 2025 under the straight-line method will be:

The interest expense for the year 2025 will be $9,770 (the two semiannual interest payments of $4,500 each plus the two semiannual amortizations of bond discount of $385 each). The following T-account for Interest Expense shows the entries for the year 2025:

The following T-account shows how the balance in Discount on Bonds Payable will be decreasing over the 5-year life of the bond.

As the bond discount is amortized, the bond’s book value will be increasing from $96,149 on the date the bond was issued to the bond’s maturity amount of $100,000:

Straight-Line Amortization of Bond Discount on Monthly Financial Statements

If the corporation issues monthly financial statements, the monthly amount of bond discount amortization under the straight-line method will be $64.18 ($3,851 of bond discount divided by the bond’s life of 60 months). The 12 monthly journal entries for the bond interest and amortization of bond discount plus the entries for the June 30 and December 31 semiannual interest payments will result in the following 14 entries during the year 2025:

The journal entries for the remaining years will be similar if all of the bonds remain outstanding.

Calculating the Present Value of a 9% Bond in an 8% Market

The present value of a bond is calculated by discounting the bond’s future cash payments by the current market interest rate.

In other words, the present value of a bond is the total of:

- The present value of the semiannual interest payments, PLUS

- The present value of the principal payment on the date the bond matures.

A 9% $100,000 bond dated January 1, 2025 and having interest payment dates of June 30 and December 31 of each year for five years will have the following semiannual interest payments and the one-time principal payment:

As the timeline indicates, the issuing corporation will pay its bondholders 10 identical interest payments of $4,500 ($100,000 x 9% x 6/12 of a year) at the end of each of the 10 semiannual periods, plus a single principal payment of $100,000 at the end of the 10th six-month period.

The present value (and the market value) of this bond depends on the market interest rate at the time of the calculation. The market interest rate is used to discount both the bond’s future interest payments and the principal payment occurring on the maturity date.

Here’s a Tip

The present value of a bond =

- The present value of a bond’s interest payments, PLUS

- The present value of a bond’s maturity amount.

Here’s a Tip

Always use the market interest rate to discount the bond’s interest payments and maturity amount to their present value.

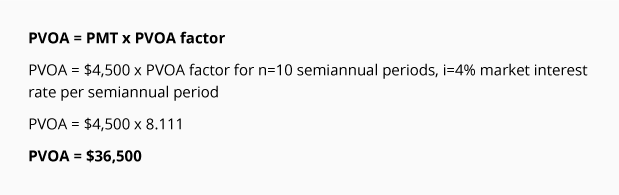

1. Present Value of a Bond’s Interest Payments

In our example, there will be interest payments of $4,500 occurring at the end of every six-month period for a total of 10 six-month or semiannual periods. This series of identical interest payments occurring at the end of equal time periods forms an ordinary annuity.

To calculate the present value of the semiannual interest payments of $4,500 each, you need to discount the interest payments by the market interest rate for a six-month period. This can be done with computer software, a financial calculator, or a present value of an ordinary annuity (PVOA) table.

We will use present value tables with factors rounded to three decimal places and will round some dollar amounts to the nearest dollar. After you understand the present value concepts and calculations, use computer software or a financial calculator to compute more precise present value amounts.

We will use the Present Value of an Ordinary Annuity (PVOA) Table for our calculations: Click here to open our PVOA Table

Notice that the first column of the PVOA Table has the heading of “n“. This column represents the number of identical payments and periods in the ordinary annuity. In computing the present value of a bond’s interest payments, “n” will be the number of semiannual interest periods or payments.

The remaining columns are headed by interest rates. These interest rates represent the market interest rate for the period of time represented by “n“. In the case of a bond, since “n” refers to the number of semiannual interest periods, you select the column with the market interest rate per semiannual period.

For example, a 5-year bond paying interest semiannually will require you to go down the first column until you reach the row where n = 10. Since n = 10 semiannual periods, you need to go to the column which is headed with the market interest rate per semiannual period. If the market interest rate is 8% per year, you would go to the column with the heading of 4% (8% annual rate divided by 2 six-month periods). Go down the 4% column until you reach the row where n = 10. At the intersection of n = 10, and the interest rate of 4% you will find the appropriate PVOA factor of 8.111.

The factors contained in the PVOA Table represent the present value of a series or stream of $1 amounts occurring at the end of every period for “n” periods discounted by the market interest rate per period. We will refer to the market interest rates at the top of each column as “i“.

Here’s a Tip

To obtain the proper factor for discounting a bond’s interest payments, use the column that has the market’s semiannual interest rate “i” in its heading.

Let’s use the following formula to compute the present value of the interest payments only as of January 1, 2025 for the bond described above. The amount of the interest payment occurring at the end of each six-month period is represented by “PMT“, the number of semiannual periods is represented by “n” and the market interest rate per semiannual period is represented by “i“.

The present value of $36,500 tells us that an investor requiring an 8% per year return compounded semiannually would be willing to invest $36,500 on January 1, 2025 in return for 10 semiannual payments of $4,500 each—with the first payment occurring on June 30, 2025. The difference between the 10 future payments of $4,500 each and the present value of $36,500 equals $8,500 ($45,000 minus $36,500). This $8,500 return on an investment of $36,500 gives the investor an 8% annual return compounded semiannually.

Recap

- Use the market interest rate when discounting a bond’s semiannual interest payments.

- Convert the market interest rate per year to a semiannual market interest rate, i.

- Convert the number of years to be the number of semiannual periods, n.

- When using the present value tables, use the semiannual market interest rate (i)

and the number of semiannual periods (n).

Recall that this calculation determined the present value of the stream of interest payments. The present value of the maturity amount will be calculated next.

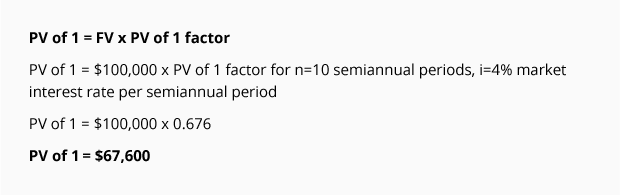

2. Present Value of a Bond’s Maturity Amount

The second component of a bond’s present value is the present value of the principal payment occurring on the bond’s maturity date. The principal payment is also referred to as the bond’s maturity value or face value.

In our example, there will be a $100,000 principal payment on the bond’s maturity date at the end of the 10th semiannual period. The single amount of $100,000 will need to be discounted to its present value as of January 1, 2025.

To calculate the present value of the single maturity amount, you discount the $100,000 by the semiannual market interest rate. We will use the Present Value of 1 Table (PV of 1 Table) for our calculations.

Notice that the first column of the PV of 1 Table has the heading of “n“. This column represents the number of identical periods that interest will be compounded. In the case of a bond, “n” is the number of semiannual interest periods or payments. In other words, the number of periods for discounting the maturity amount is the same number of periods used for discounting the interest payments.

The remaining columns of the PV of 1 Table are headed by interest rates. The interest rate represents the market interest rate for the period of time represented by “n“. In the case of a bond, since “n” refers to the number of semiannual interest periods, you select the column with the market interest rate per semiannual period.

For example, a 5-year bond paying interest semiannually will require you to go down the first column until you reach the row where n = 10. Since n = 10 semiannual periods, you need to go to the column which is headed with the market interest rate per semiannual period. If the market interest rate is 8% per year, you would go to the column with the heading of 4% (8% annual rate divided by 2 six-month periods). Go down the 4% column until you reach the row where n = 10. At the intersection of n = 10, and the interest rate of 4%, you will find the PV of 1 factor of 0.676.

The factors contained in the PV of 1 Table represent the present value of a single payment of $1 occurring at the end of the period “n” discounted by the market interest rate per period, which will be noted as “i“.

Here’s a Tip

To obtain the proper factor for discounting a bond’s maturity value, use the PV of 1 table and use the same “n” and “i” that you used for discounting the semiannual interest payments.

Let’s use the following formula to compute the present value of the maturity amount only of the bond described above. The maturity amount, which occurs at the end of the 10th six-month period, is represented by “FV” .

The present value of $67,600 tells us that an investor requiring an 8% per year return compounded semiannually would be willing to invest $67,600 in return for a single receipt of $100,000 at the end of 10 semiannual periods of time. The difference between the present value of $67,600 and the single future principal payment of $100,000 is $32,400. This $32,400 return on an investment of $67,600 gives the investor an 8% annual return compounded semiannually.

Recap

When calculating the present value of the maturity amount…

Use the semiannual market interest rate (i) and the number of semiannual periods (n) that were used to calculate the present value of the interest payments.

Combining the Present Value of a Bond’s Interest and Maturity Amounts

Recall that the present value of a bond consisted of:

- The present value of a bond’s interest payments, PLUS

- The present value of a bond’s maturity amount.

The present value of the bond in our example is $36,500 + $67,600 = $104,100.

The bond’s total present value of $104,100 should approximate the bond’s market value.

It is reasonable that a bond promising to pay 9% interest will sell for more than its face value when the market is expecting to earn only 8% interest. In other words, the 9% bond will be paying $500 more semiannually than the bond market is expecting ($4,500 vs. $4,000). If investors will be receiving an additional $500 semiannually for 10 semiannual periods, they are willing to pay $4,100 more than the bond’s face amount of $100,000. The $4,100 more than the bond’s face amount is referred to as Premium on Bonds Payable, Bond Premium, Unamortized Bond Premium, or Premium.

The journal entry to record a $100,000 bond that was issued for $104,100 on January 1, 2025 is:

Amortizing Bond Premium with the Effective Interest Rate Method

When a bond is sold at a premium, the amount of the bond premium must be amortized to interest expense over the life of the bond. In other words, the credit balance in the account Premium on Bonds Payable must be moved to the account Interest Expense thereby reducing interest expense in each of the accounting periods that the bond is outstanding.

The preferred method for amortizing the bond premium is the effective interest rate method or the effective interest method. Under the effective interest rate method the amount of interest expense in a given year will correlate with the amount of the bond’s book value. This means that when a bond’s book value decreases, the amount of interest expense will decrease. In short, the effective interest rate method is more logical than the straight-line method of amortizing bond premium.

Before we demonstrate the effective interest rate method for amortizing the bond premium pertaining to a 5-year 9% $100,000 bond issued in an 8% market for $104,100 on January 1, 2025, let’s outline a few concepts:

- The bond premium of $4,100 must be amortized to Interest Expense over the life of the bond. This amortization will cause the bond’s book value to decrease from $104,100 on January 1, 2025 to $100,000 just prior to the bond maturing on December 31, 2029.

- The corporation must make an interest payment of $4,500 ($100,000 x 9% x 6/12) on each June 30 and December 31. This means that the Cash account will be credited for $4,500 on each interest payment date.

- The effective interest rate method uses the market interest rate at the time that the bond was issued. In our example, the market interest rate on January 1, 2025 was 4% per semiannual period for 10 semiannual periods.

- The effective interest rate is multiplied times the bond’s book value at the start of the accounting period to arrive at each period’s interest expense.

- The difference between Item 2 and Item 4 is the amount of amortization.

The following table illustrates the effective interest rate method of amortizing the $4,100 premium on a corporation’s bonds payable:

Please make note of the following points:

- Column B shows the interest payments required in the bond contract: The bond’s stated rate of 9% per year divided by two semiannual periods = 4.5% per semiannual period times the face amount of the bond

- Column C shows the interest expense. This calculation uses the market interest rate at the time the bond was issued: The market rate of 8% per year divided by two semiannual periods = 4% semiannually.

- The interest expense in column C is the product of the 4% market interest rate per semiannual period times the book value of the bond at the start of the semiannual period. Notice how the interest expense is decreasing with the decrease in the book value in column G. This correlation between the interest expense and the bond’s book value makes the effective interest rate method the preferred method.

- Because the present value factors that we used were rounded to three decimal places, our calculations are not as precise as the amounts determined by use of computer software, a financial calculator, or factors with more decimal places. As a result, the amounts in year 2029 required a small adjustment.

If the company issues only annual financial statements and its accounting year ends on December 31, the amortization of the bond premium can be recorded at the interest payment dates by using the amounts from the schedule above. In our example there was no accrued interest at the issue date of the bonds and there is no accrued interest at the end of each accounting year because the bonds pay interest on June 30 and December 31. The entries for 2025, including the entry to record the bond issuance, are:

The journal entries for the year 2026 are:

The journal entries for 2027, 2028, and 2029 will also be taken from the schedule above.

Comparison of Amortization Methods

Below is a comparison of the amount of interest expense reported under the effective interest rate method and the straight-line method. Note that under the effective interest rate method the interest expense for each year is decreasing as the book value of the bond decreases. Under the straight-line method the interest expense remains at a constant annual amount even though the book value of the bond is decreasing. The accounting profession prefers the effective interest rate method, but allows the straight-line method when the amount of bond premium is not significant.

Notice that under both methods of amortization, the book value at the time the bonds were issued ($104,100) moves toward the bond’s maturity value of $100,000. The reason is that the bond premium of $4,100 is being amortized to interest expense over the life of the bond.

Also notice that under both methods the corporation’s total interest expense over the life of the bond will be $40,900 ($45,000 of interest payments minus the $4,100 of premium received from the purchasers of the bond when it was issued.)

Calculating the Present Value of a 9% Bond in a 10% Market

Let’s assume that a 9% $100,000 bond is prepared in December 2024. By the time the bond is offered to investors on January 1, 2025 the market interest rate has increased to 10%. The date of the bond is January 1, 2025 and it matures on December 31, 2029. The bond will pay interest of $4,500 (9% x $100,000 x 6/12 of a year) on each June 30 and December 31.

To calculate the approximate price that an investor will pay for the corporation’s bond on January 1, 2025, we need to calculate the bond’s present value. The present value of the bond is the total of:

- The present value of the bond’s interest payments that will occur every six months, PLUS

- The present value of the principal amount that occurs when the bond matures.

We calculate these two present values by discounting the future cash amounts by the market interest rate per semiannual period.

1. Present Value of the Bond’s Interest Payments

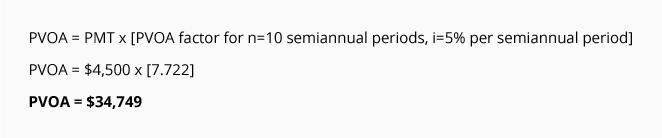

The first step in calculating the bond’s present value is to calculate the present value of the bond’s interest payments. The interest payments form an ordinary annuity consisting of 10 payments of $4,500 occurring at the end of each six month period as shown in the following timeline:

To obtain the present value of the interest payments you must discount them by the market interest rate per semiannual period. In our example, the market interest rate is 5% per semiannual period. The 5% market interest rate per semiannual period is symbolized by i. (The market rate of 10% per year was divided by 2 semiannual periods per year to arrive at the market interest rate of 5% per semiannual period.)

The bond’s life of 5 years is multiplied by 2 to arrive at 10 semiannual periods. The number of semiannual periods is symbolized by n.

Each semiannual interest payment of $4,500 ($100,000 x 9% x 6/12) occurring at the end of each of the 10 semiannual periods is represented by “PMT”.

We use the above amounts (i = 5%, n = 10, PMT = $4,500) in the following equation for calculating the present value of the ordinary annuity (PVOA):

(You will find more information about discounting an ordinary annuity by visiting our Present Value of an Ordinary Annuity Explanation.)

Recall that this calculation determines the present value of the stream of interest payments only. The present value of the maturity amount will be calculated next.

2. Present Value of the Bond’s Maturity Amount

The second step in calculating the present value of a bond is to calculate the present value of the maturity amount of the bond as shown in the following timeline:

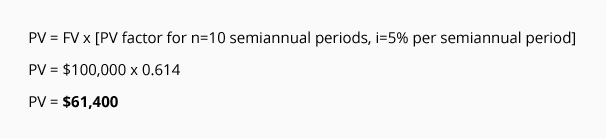

Since the corporation’s payment of the maturity amount occurs on a single date, we need to use the factors from a Present Value of 1 Table (PV of 1 Table). When using the PV of 1 Table we use the same number of periods and the same market interest rate that was used to discount the semiannual interest payments. In this case we use n = 10 semiannual periods, i = 5% per semiannual period, and the future value, FV = $100,000.

Using the PV of 1 table, we see that the present value factor for n = 10, and i = 5% is 0.614.

The calculation of the present value (PV) of the single maturity amount (FV) is:

Combining the Present Value of a Bond’s Interest and Maturity Amounts

Recall that the present value of a bond =

- The present value of a bond’s interest payments, PLUS

- The present value of a bond’s maturity amount.

The present value of the 9% 5-year bond that is sold in a 10% market is $96,149 consisting of:

- $34,749 of present value for the interest payments, PLUS

- $61,400 of present value for the maturity amount.

The bond’s total present value of $96,149 is approximately the bond’s market value and issue price.

It is reasonable that a bond promising to pay 9% interest will sell for less than its face value when the market is expecting to earn 10% interest. In other words, the 9% $100,000 bond will be paying $500 less semiannually than the bond market is expecting ($4,500 vs. $5,000). Since investors will be receiving $500 less every six months than the market is requiring, the investors will not pay the full $100,000 of a bond’s face value. The $3,851 ($96,149 present value vs. $100,000 face value) is referred to as Discount on Bonds Payable, Bond Discount, Unamortized Bond Discount, or Discount.

The journal entry to record the $100,000 bond that is issued on January 1, 2025 for $96,149 and no accrued interest is:

Amortizing Bond Discount with the Effective Interest Rate Method

When a bond is sold at a discount, the amount of the bond discount must be amortized to interest expense over the life of the bond. Since the debit amount in the account Discount on Bonds Payable will be moved to the account Interest Expense, the amortization will cause each period’s interest expense to be greater than the amount of interest paid during each of the years that the bond is outstanding.

The preferred method for amortizing the bond discount is the effective interest rate method or the effective interest method. Under the effective interest rate method the amount of interest expense in a given accounting period will correlate with the amount of a bond’s book value at the beginning of the accounting period. This means that as a bond’s book value increases, the amount of interest expense will increase.

Before we demonstrate the effective interest rate method for a 5-year 9% $100,000 bond issued in a 10% market for $96,149, let’s highlight a few points:

- The bond discount of $3,851 must be amortized to Interest Expense over the life of the bond. The amortization will cause the bond’s book value to increase from $96,149 on January 1, 2025 to $100,000 just prior to the bond maturing on December 31, 2029.

- The corporation must make an interest payment of $4,500 ($100,000 x 9% x 6/12) on each June 30 and December 31 that the bonds are outstanding. The Cash account will be credited for $4,500 on each of these dates.

- The effective interest rate is the market interest rate on the date that the bonds were issued. In our example the market interest rate on January 1, 2025 was 5% per semiannual period for 10 semiannual periods.

- The effective interest rate is multiplied times the bond’s book value at the start of the accounting period to arrive at each period’s interest expense.

- The difference between Item 2 and Item 4 is the amount of amortization.

The following table illustrates the effective interest rate method of amortizing the $3,851 discount on bonds payable:

Let’s make a few points about the above table:

- Column B shows the interest payments required by the bond contract: The bond’s stated rate of 9% per year divided by two semiannual periods = 4.5% per semiannual period multiplied times the face amount of the bond.

- Column C shows the interest expense. This calculation uses the market interest rate at the time the bonds were issued: The market rate of 10% per year divided by two semiannual periods = 5% semiannually.

- The interest expense in column C is the product of the 5% market interest rate per semiannual period times the book value of the bond at the start of the semiannual period. Notice how the interest expense is increasing with the increase in the book value in column G. This correlation between the interest expense and the bond’s book value makes the effective interest rate method the preferred method for amortizing the discount on bonds payable.

- Because the present value factors that we used were rounded to three decimal positions, our calculations are not as precise as the amounts determined by use of computer software, a financial calculator, or factors that were carried out to more decimal places. As a result, our amortization amount in 2029 required a slight adjustment.

If the company issues only annual financial statements and its accounting year ends on December 31, the amortization of the bond discount can be recorded on the interest payment dates by using the amounts from the schedule above. In our example, there is no accrued interest at the issue date of the bonds and at the end of each accounting year because the bonds pay interest on June 30 and December 31. The entries for 2025, including the entry to record the bond issuance, are shown next.

The journal entries for the year 2026 are:

The journal entries for the years 2027 through 2029 will also be taken from the schedule shown above.

Comparison of Amortization Methods

Below is a comparison of the amount of interest expense reported under the effective interest rate method and the straight-line method. Note that under the effective interest rate method the interest expense for each year is increasing as the book value of the bond increases. Under the straight-line method the interest expense remains at a constant amount even though the book value of the bond is increasing. The accounting profession prefers the effective interest rate method, but allows the straight-line method when the amount of bond discount is not significant.

Notice that under both methods of amortization, the book value at the time the bonds were issued ($96,149) moves toward the bond’s maturity value of $100,000. The reason is that the bond discount of $3,851 is being reduced to $0 as the bond discount is amortized to interest expense.

Also notice that under both methods the total interest expense over the life of the bonds is $48,851 ($45,000 of interest payments plus the $3,851 of bond discount.)

Summary of the Effect of Market Interest Rates on a Bond’s Issue Price

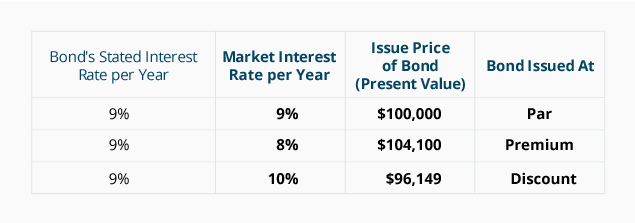

The following table summarizes the effect of the change in the market interest rate on an existing $100,000 bond with a stated interest rate of 9% and maturing in 5 years.

Additional Bond Terminology

Bonds are a form of long-term debt and might be referred to as a debt security.

Bonds allow corporations to use financial leverage or to trade on equity. The reason is that a corporation issuing bonds can control larger amounts of assets without increasing its common stock.

Bonds that mature on a single maturity date are known as term bonds. Bonds that mature over a series of dates are serial bonds.

Bonds that have specific assets pledged as collateral are secured bonds. An example of a secured bond would be a mortgage bond that has a lien on real estate.

Bonds that do not have specific collateral and instead rely on the corporation’s general financial position are referred to as unsecured bonds or debentures.

Convertible bonds allow the bondholder to exchange the bond for a specified number of shares of common stock. Most bonds are not convertible bonds.

Some bonds require the issuing corporation to deposit money into an account that is restricted for the payment of the bonds’ maturity amount. The restricted account is Bond Sinking Fund and it is reported in the long-term investment section of the balance sheet.

Callable bonds are bonds that give the issuing corporation the right to repurchase its bonds by paying the bondholders the bonds’ face amount plus an additional amount known as the call premium. The call premium might be one year of additional interest. A bond’s call price and other conditions can be found in a bond’s contract known as the indenture.

Many years ago corporate bonds could be unregistered. Such bonds were known as bearer bonds and the bonds had coupons attached that the bearer would “clip” and deposit at the bearer’s bank. Today, corporations do not issue bearer bonds. Instead, they issue registered bonds.

There are various fees that a corporation must pay when issuing bonds. These fees include payments to attorneys, accounting firms, and securities consultants. These costs are referred to as issue costs and are recorded in the account Bond Issue Costs. Beginning in 2016, the unamortized amount of the bond issue costs is reported as a deduction from the amount of the liability bonds payable. Over the life of the bonds the bond issue costs are amortized to interest expense.

When bond interest rates are discussed, the term basis point is often used. A basis point is 1/100th of one percentage point. For example, if a market interest rate increases from 6.25% to 6.50%, the rate is said to have increased by 25 basis points.

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Bonds Payable materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.