For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.

Before you begin: If you enjoy this free In-Depth Explanation, we recommend trying our PRO materials (used by 80,000+ professionals). You'll receive lifetime access to our certificates of achievement, video training, flashcards, visual tutorials, quick tests, cheat sheets, guides, business forms, printable PDF files, and more. Earn badges, points, and medals as you track your progress and display your achievements on your public profile page.

Introduction

This explanation of accounting basics will introduce you to some basic accounting principles, accounting concepts, and accounting terminology. Once you become familiar with some of these terms and concepts, you will feel comfortable navigating through the explanations, quizzes, quick tests, video training, and other features on AccountingCoach.com.

Some of the basic accounting terms that you will learn include revenues, expenses, assets, liabilities, income statement, balance sheet, and statement of cash flows. You will become familiar with accounting debits and credits as we show you how to record transactions. You will also see why two basic accounting principles, the revenue recognition principle and the matching principle, assure that a company’s income statement reports a company’s profitability.

In this explanation of accounting basics, and throughout all of the free materials and the PRO materials, we will often omit some accounting details and complexities in order to present clear and concise explanations. This means that you should always seek professional advice for your specific circumstances.

Please let us know how we can improve this explanation

No Thanks

Close

A Story for Relating to Accounting Basics

We will present the basics of accounting through a story of a person starting a new business. The person is Joe Perez—a savvy man who sees the need for a parcel delivery service in his community. Joe has researched his idea and has prepared a business plan that documents the viability of his new business.

Joe has also met with an attorney to discuss the form of business he should use. Given his specific situation, they concluded that a corporation will be best. Joe decides that the name for his corporation will be Direct Delivery, Inc. The attorney also advises Joe on the various permits and government identification numbers that will be needed for the new corporation.

Joe is a hard worker and a smart man, but admits he is not comfortable with matters of accounting. He assumes he will use some accounting software, but wants to meet with a professional accountant before making his selection. He asks his banker to recommend a professional accountant who is also skilled in explaining accounting to someone without an accounting background. Joe wants to understand the financial statements and wants to keep on top of his new business. His banker recommends Marilyn, an accountant who has helped many of the bank’s small business customers.

At his first meeting with Marilyn, Joe asks her for an overview of accounting, financial statements, and the need for accounting software. Based on Joe’s business plan, Marilyn sees that there will likely be thousands of transactions each year. She states that accounting software will allow for the electronic recording, storing, and retrieval of those many transactions. Accounting software will permit Joe to generate the financial statements and other reports that he will need for running his business.

Joe seems puzzled by the term transaction, so Marilyn gives him five examples of transactions that Direct Delivery, Inc. will need to record:

Joe will no doubt start his business by putting some of his own personal money into it. In effect, he is buying shares of Direct Delivery’s common stock.

Direct Delivery will need to buy a sturdy, dependable delivery vehicle.

The business will begin earning fees and billing clients for delivering their parcels.

The business will be collecting the fees that were earned.

The business will incur expenses in operating the business, such as a salary for Joe, expenses associated with the delivery vehicle, advertising, etc.

With thousands of such transactions in a given year, Joe is smart to start using accounting software right from the beginning. Accounting software will generate sales invoices and accounting entries simultaneously, prepare statements for customers with no additional work, write checks, automatically update accounting records, etc.

By getting into the habit of entering all of the day’s business transactions into his computer, Joe will be rewarded with fast and easy access to the specific information he will need to make sound business decisions. Marilyn tells Joe that accounting’s “transaction approach” is useful, reliable, and informative. She has worked with other small business owners who think it is enough to simply “know” their company made $30,000 during the year (based only on the fact that it owns $30,000 more than it did on January 1). Those are the people who start off on the wrong foot and end up in Marilyn’s office looking for financial advice.

If Joe enters all of Direct Delivery’s transactions into his computer, good accounting software will allow Joe to print out his financial statements with a click of a button. In the following pages Marilyn will explain the content and purpose of three of the five financial statements:

Please let us know how we can improve this explanation

No Thanks

Close

Income Statement

Marilyn points out that an income statement will show how profitable Direct Delivery has been during the time interval shown in the statement’s heading. This period of time might be a week, a month, three months, five weeks, or a year—Joe can choose whatever time period he deems most useful.

The reporting of profitability involves two things: the amount that was earned (revenues) and the expenses necessary to earn the revenues. As you will see next, the term revenues is not the same as receipts, and the term expenses involves more than just writing a check to pay a bill.

A. Revenues

The main revenues for Direct Delivery are the fees it earns for delivering parcels. Under the accrual basis of accounting (as opposed to the less-preferred cash method of accounting), revenues are recorded when they are earned, not when the company receives the money. Recording revenues when they are earned is the result of one of the basic accounting principles known as the revenue recognition principle.

For example, if Joe delivers 1,000 parcels in December for $4 per delivery, he has technically earned fees totaling $4,000 for that month. He sends invoices to his clients for these fees and his terms require that his clients must pay by January 10. Even though his clients won’t be paying Direct Delivery until January 10, the accrual basis of accounting requires that the $4,000 be recorded as December revenues, since that is when the delivery work actually took place. At the time when invoices are prepared and revenues are recorded, the software will also record the amount in the asset account Accounts Receivable.

When Joe receives the $4,000 worth of payment checks from his customers on January 10, he will make an accounting entry to show the money was received. This $4,000 of receipts will not be considered to be January revenues, since the revenues were already reported as revenues in December when they were earned. This $4,000 of receipts will be recorded in January and will increase the company’s cash and will reduce the amount in Accounts Receivable.

B. Expenses

Now Marilyn turns to the second part of the income statement—expenses. The December income statement should show expenses incurred during December regardless of when the company actually paid for the expenses. For example, if Joe hires someone to help him with December deliveries and Joe agrees to pay him $500 on January 3, that $500 expense needs to be shown on the December income statement. The actual date that the $500 is paid out doesn’t matter. What matters is when the work was done—when the expense was incurred—and in this case, the work was done in December. The $500 expense is counted as a December expense even though the money will not be paid out until January 3. The recording of expenses with the related revenues is associated with another basic accounting principle known as the matching principle.

Marilyn explains to Joe that showing the $500 of wages expense on the December income statement will result in a matching of the cost of the labor used to deliver the December parcels with the revenues from delivering the December parcels. This matching principle is very important in measuring just how profitable a company was during a given time period.

Marilyn is delighted to see that Joe already has an intuitive grasp of this basic accounting principle. In order to earn revenues in December, the company had to incur some business expenses in December, even if the expenses won’t be paid until January. Other expenses to be matched with December’s revenues would be such things as gas for the delivery van and advertising spots on the radio.

Joe asks Marilyn to provide another example of a cost that wouldn’t be paid in December, but would have to be shown/matched as an expense on December’s income statement. Marilyn uses the Interest Expense on borrowed money as an example. She asks Joe to assume that on December 1 Direct Delivery borrows $20,000 from Joe’s aunt and the company agrees to pay his aunt 6% per year in interest, or $1,200 per year. This interest of $1,200 is to be paid on December 1 of each year.

Now even though the interest is being paid out to his aunt only once per year as a lump sum, Joe can see that in reality, a little bit of that interest expense is incurred each and every day he’s in business. If Joe is preparing monthly income statements, Joe should report one month of Interest Expense on each month’s income statement. The amount that Direct Delivery will incur as Interest Expense will be $100 per month all year long ($20,000 x 6% ÷ 12). In other words, Joe needs to match $100 of interest expense with each month’s revenues. The interest expense is considered a cost that is necessary to earn the revenues shown on the income statements.

Marilyn explains to Joe that the income statement is a bit more complicated than what she just explained, but for now she just wants Joe to learn some basic accounting concepts and some of the accounting terminology. Marilyn does make sure, however, that Joe understands one simple yet important point: an income statement, does not report the cash coming in—rather, its purpose is to (1) report the revenues earned by the company’s efforts during the period, and (2) report the expenses incurred by the company during the same period. The purpose of the income statement is to show a company’s profitability during a specific period of time. The difference (or “net“) between the revenues and expenses for Direct Delivery is often referred to as the bottom line and it is labeled as either Net Income or Net Loss.

Note: To learn more about the income statement, visit our Explanation and Quiz for this topic.

Please let us know how we can improve this explanation

No Thanks

Close

Balance Sheet – Assets

Marilyn moves on to explain the balance sheet, a financial statement that reports the amount of a company’s (A) assets, (B) liabilities, and (C) stockholders’ (or owner’s) equity at a specific point in time. Because the balance sheet reflects a specific point in time rather than a period of time, Marilyn likes to refer to the balance sheet as a “snapshot” of a company’s financial position at a given moment. For example, if a balance sheet is dated December 31, the amounts shown on the balance sheet are the balances in the accounts after all transactions pertaining to December 31 have been recorded.

(A) Assets

Assets are things that a company owns and are sometimes referred to as the resources of the company. Joe readily understands this—off the top of his head he names things such as the company’s vehicle, its cash in the bank, all of the supplies he has on hand, and the dolly he uses to help move the heavier parcels. Marilyn nods and shows Joe how these are reported in accounts called Vehicles, Cash, Supplies, and Equipment. She mentions one asset Joe hadn’t considered—Accounts Receivable. If Joe delivers parcels, but isn’t paid immediately for the delivery, the amount owed to Direct Delivery is an asset known as Accounts Receivable.

Prepaids

Marilyn brings up another less obvious asset—the unexpired portion of prepaid expenses. Suppose Direct Delivery pays $1,200 on December 1 for a six-month insurance premium on its delivery vehicle. That divides out to be $200 per month ($1,200 ÷ 6 months). Between December 1 and December 31, $200 worth of insurance premium is “used up” or “expires”. The expired amount will be reported as Insurance Expense on December’s income statement. Joe asks Marilyn where the remaining $1,000 of unexpired insurance premium would be reported. On the December 31 balance sheet, Marilyn tells him, in an asset account called Prepaid Insurance.

Other examples of things that might be paid for before they are used include supplies and annual dues to a trade association. The portion that expires in the current accounting period is listed as an expense on the income statement; the part that has not yet expired is listed as an asset on the balance sheet.

Marilyn assures Joe that he will soon see a significant link between the income statement and balance sheet, but for now she continues with her explanation of assets.

Cost Principle and Conservatism

Joe learns that each of his company’s assets was recorded at its original cost, and even if the fair market value of an item increases, an accountant will not increase the recorded amount of that asset on the balance sheet. This is the result of another basic accounting principle known as the cost principle.

Although accountants generally do not increase the value of an asset, they might decrease its value as a result of a concept known as conservatism. For example, after a few months in business, Joe may decide that he can help out some customers—as well as earn additional revenues—by carrying an inventory of packing boxes to sell. Let’s say that Direct Delivery purchased 100 boxes wholesale for $1.00 each. Since the time when Joe bought them, however, the wholesale price of boxes has been cut by 40% and at today’s price he could purchase them for $0.60 each. If the net realizable value of his inventory is less than the original recorded cost, the principle of conservatism directs the accountant to report the lower amount as the asset’s value on the balance sheet.

In short, the cost principle generally prevents assets from being reported at more than cost, while conservatism might require assets to be reported at less than their cost.

Depreciation

Joe also needs to know that the reported amounts on his balance sheet for assets such as equipment, vehicles, and buildings are routinely reduced by depreciation. Depreciation is required by the basic accounting principle known as the matching principle. Depreciation is used for assets whose life is not indefinite—equipment wears out, vehicles become too old and costly to maintain, buildings age, and some assets (like computers) become obsolete. Depreciation is the allocation of the cost of the asset to Depreciation Expense on the income statement over its useful life.

As an example, assume that Direct Delivery’s van has a useful life of five years and was purchased at a cost of $20,000. The accountant might match $4,000 ($20,000 ÷ 5 years) of Depreciation Expense with each year’s revenues for five years. Each year the carrying amount of the van will be reduced by $4,000. (The carrying amount—or “book value“—is reported on the balance sheet and it is the cost of the van minus the total depreciation since the van was acquired.) This means that after one year the balance sheet will report the carrying amount of the delivery van as $16,000, after two years the carrying amount will be $12,000, etc. After five years—the end of the van’s expected useful life—its carrying amount is zero.

Joe wants to be certain that he understands what Marilyn is telling him regarding the assets on the balance sheet, so he asks Marilyn if the balance sheet is, in effect, showing what the company’s assets are worth. He is surprised to hear Marilyn say that the assets are not reported on the balance sheet at their worth (fair market value). Long-term assets (such as buildings, equipment, and furnishings) are reported at their cost minus the amounts already sent to the income statement as Depreciation Expense. The result is that a building’s market value may actually have increased since it was acquired, but the amount on the balance sheet has been consistently reduced as the accountant moved some of its cost to Depreciation Expense on the income statement in order to achieve the matching principle.

Another asset, Office Equipment, may have a fair market value that is less than or greater than the carrying amount reported on the balance sheet. (Accountants view depreciation as an allocation process—allocating the cost to expense in order to match the costs with the revenues generated by the asset. Accountants do not consider depreciation to be a valuation process.) The asset Land is not depreciated, so it will appear at its original cost even if the land is now worth one hundred times more than its cost.

Short-term (current) asset amounts are likely to be close to their market values, since they tend to “turn over” in relatively short periods of time.

Marilyn cautions Joe that the balance sheet reports only the assets acquired and only at the cost reported in the transaction. This means that a company’s reputation—as excellent as it might be—will not be listed as an asset. It also means that Jeff Bezos will not appear as an asset on Amazon.com’s balance sheet; Nike’s logo will not appear as an asset on its balance sheet; etc. Joe is surprised to hear this, since in his opinion these items are perhaps the most valuable things those companies have. Marilyn tells Joe that he has just learned an important lesson that he should remember when reading a balance sheet.

Please let us know how we can improve this explanation

No Thanks

Close

Balance Sheet – Liabilities and Stockholders’ Equity

(B) Liabilities

The balance sheet reports Direct Delivery’s liabilities as of the date shown in the heading of the balance sheet. Liabilities are obligations of the company; they are amounts owed to others as of the balance sheet date. Marilyn gives Joe some examples of liabilities: the loan he received from his aunt (Notes Payable or Loan Payable), the interest on the loan he owes to his aunt (Interest Payable), the amount he owes to the supply store for items purchased on credit (Accounts Payable), the wages he owes to employees (Wages Payable).

Another liability is the money received in advance of actually earning the money. For example, suppose that Direct Delivery enters into an agreement with one of its customers stipulating that the customer prepays $600 in return for the delivery of 30 parcels every month for 6 months. Assume Direct Delivery receives that $600 payment on December 1 for deliveries to be made between December 1 and May 31. Direct Delivery has a cash receipt of $600 on December 1, but it does not have revenues of $600 at this point. It will have revenues only when it earns them by delivering the parcels. On December 1, Direct Delivery will show that its asset Cash increased by $600, but it will also have to show that it has a liability of $600. (It has the obligation to deliver $600 of parcels within 6 months, or return the money.)

The liability account involved in the $600 received on December 1 is Unearned Revenue (or Deferred Revenues, Customer Deposits, etc.). Each month, as the 30 parcels are delivered, Direct Delivery will be earning $100. As a result, each month $100 will move from the liability Unearned Revenue to Service Revenues reported on the income statement.

(C) Stockholders’ Equity

If the company is a corporation, the third section of a corporation’s balance sheet is Stockholders’ Equity. (If the company is a sole proprietorship, it is Owner’s Equity.) The amount of Stockholders’ Equity is the difference (or residual) of assets minus liabilities. Stockholders’ Equity is also the “book value” of the corporation.

Since the corporation’s assets are shown at cost or lower (and not at their market values) it is important that you do not associate the reported amount of Stockholders’ Equity with the market value of the corporation. (Hence, it is a poor choice of words to refer to Stockholders’ Equity as the corporation’s “net worth”.) To determine the estimated market value of a corporation, you should obtain the services of a professional familiar with valuing businesses.

The account Common Stock will be increased when the corporation issues shares of stock in exchange for cash (or some other asset). Another account Retained Earnings will increase when the corporation earns a profit. There will be a decrease when the corporation has a net loss. This means that revenues will automatically cause an increase in Stockholders’ Equity and expenses will automatically cause a decrease in Stockholders’ Equity. This illustrates a link between a company’s balance sheet and income statement.

Note: To learn more about the balance sheet, visit our Explanation and Quiz for this topic.

Please let us know how we can improve this explanation

No Thanks

Close

Statement of Cash Flows

The third financial statement that Joe needs to understand is the Statement of Cash Flows. This statement shows how Direct Delivery’s cash amount has changed during the time interval shown in the heading of the statement. This should be the same period of time as the income statement. Joe will be able to see at a glance the cash generated and used by his company’s operating activities, its investing activities, and its financing activities. Much of the information on this financial statement will come from Direct Delivery’s balance sheets and income statements.

Note: To learn more about the cash flow statement, visit our Explanation and Quiz for this topic.

The three financial reports that Marilyn introduced to Joe—the income statement, the balance sheet, and the statement of cash flows—represent just part of the valuable information that good accounting software can generate for business owners.

Marilyn now explains to Joe the basics of getting started with recording his transactions.

Please let us know how we can improve this explanation

No Thanks

Close

Double-Entry System

The field of accounting—both the older manual systems and today’s accounting software—is based on the 500-year-old accounting procedure known as double entry. Double entry is a simple yet powerful concept: each and every one of a company’s transactions will result in an amount recorded into at least two of the accounts in the accounting system. (The accounts are contained in what’s known as the general ledger.)

Chart of Accounts

To begin the process of setting up Joe’s accounting system, he will need to make a detailed listing of all the names of the accounts that Direct Delivery, Inc. might find useful for sorting and reporting transactions. This detailed listing is referred to as a chart of accounts. (Accounting software often provides sample charts of accounts for various types of businesses.)

As he enters his transactions, Joe will find the chart of accounts to be helpful for selecting the two (or more) accounts that are involved. Once Joe’s business begins, he may add more account names to the chart of accounts, or delete account names that are never used.

Basically, the chart of accounts and the accounts in the general ledger can be grouped into two types:

Note: To learn more about the chart of accounts, visit our Explanation and Quiz for this topic.

To help Joe really understand how this works, Marilyn illustrates the double-entry system with some sample transactions that Joe will likely encounter.

Please let us know how we can improve this explanation

No Thanks

Close

Sample Transaction #1

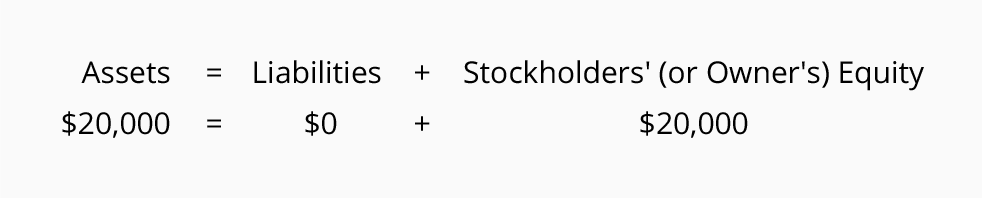

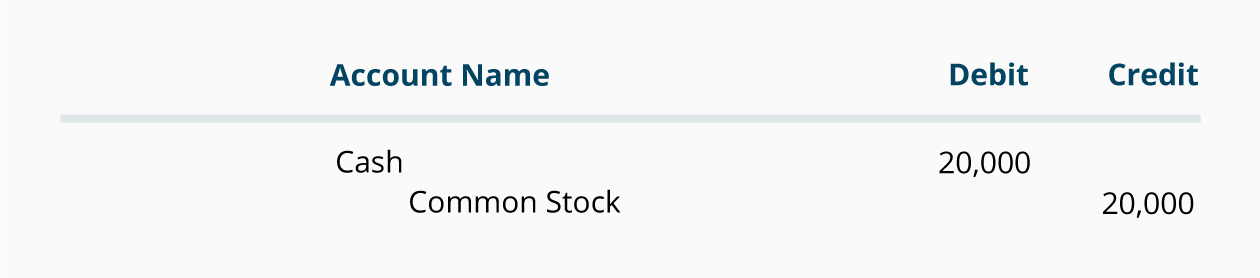

On December 1, 2024 Joe starts his business Direct Delivery, Inc. The first transaction that Joe will record for his corporation is his personal investment of $20,000 in exchange for 5,000 shares of Direct Delivery’s common stock. Direct Delivery’s accounting system will show an increase in its account Cash from zero to $20,000, and an increase in its stockholders’ equity account Common Stock by $20,000. Both of these accounts are balance sheet accounts. There are no revenues because no delivery fees were earned by the company, and there were no expenses.

After Joe enters this transaction, Direct Delivery’s balance sheet will look like this:

Marilyn asks Joe if he can see that the balance sheet is just that—in balance. Joe looks at the total of $20,000 on the asset side, and looks at the $20,000 on the right side, and says yes, of course, he can see that it is indeed in balance.

Marilyn shows Joe something called the basic accounting equation, which, she explains, is really the same concept as the balance sheet, it’s just presented in an equation format:

The accounting equation (and the balance sheet) should always be in balance.

Debits and Credits

Did the first sample transaction follow the double-entry system and affect two or more accounts? Joe looks at the balance sheet again and answers yes, both Cash and Common Stock were affected by the transaction.

Marilyn introduces the next basic accounting concept: the double-entry system requires that the same dollar amount of the transaction must be entered on both the left side of one account, and on the right side of another account. Instead of the word left, accountants use the word debit; and instead of the word right, accountants use the word credit. (The terms debit and credit are derived from Latin terms used 500 years ago.)

Here’s a Tip

Debit means left. Credit means right.

Joe asks Marilyn how he will know which accounts he should debit—meaning he should enter the numbers on the left side of one account—and which accounts he should credit—meaning he should enter the numbers on the right side of another account. Marilyn points back to the basic accounting equation and tells Joe that if he memorizes this simple equation, it will be easier to understand the debits and credits.

Here’s a Tip

Memorizing the simple accounting equation will help you learn the debit and credit rules for entering amounts into the accounting records.

Let’s take a look at the accounting equation again:

Just as assets are on the left side (or debit side) of the accounting equation, the asset accounts in the general ledger have their balances on the left side. To increase an asset account’s balance, you put more on the left side of the asset account. In accounting jargon, you debit the asset account. To decrease an asset account balance you credit the account, that is, you enter the amount on the right side.

Just as liabilities and stockholders’ equity are on the right side (or credit side) of the accounting equation, the liability and equity accounts in the general ledger will normally have their balances on the right side. To increase the balance in a liability or stockholders’ equity account, you put more on the right side of the account. In accounting jargon, you credit the liability or the equity account. To decrease a liability or equity, you debit the account, that is, you enter the amount on the left side of the account.

As with all rules, there are a few exceptions, but Marilyn’s reference to the accounting equation may help you to learn whether an account should be debited or credited.

Since many transactions involve cash, Marilyn suggests that Joe memorize how the Cash account is affected when a transaction involves cash: if Direct Delivery receives cash, the Cash account is debited; when Direct Delivery pays cash, the Cash account is credited.

Here’s a Tip

When a company receives cash, the Cash account is debited.

When the company pays cash, the Cash account is credited.

Marilyn refers to the example of December 1. Since Direct Delivery received $20,000 in cash from Joe in exchange for 5,000 shares of common stock, one of the accounts for this transaction is Cash. Since cash was received, the Cash account will be debited.

In keeping with double entry, two (or more) accounts need to be involved. Because the first account (Cash) was debited, the second account needs to be credited. All Joe needs to do is find the right account to credit. In this case, the second account is Common Stock. Common stock is part of stockholders’ equity, which is on the right side of the accounting equation. As a result, it should have a credit balance, and to increase its balance the account needs to be credited.

Accountants indicate accounts and amounts using the following general journal format:

Accountants show the account and amount to be debited first. Then on the next line, the account to be credited is indented and the amount appears further to the right than the debit amount in the line above.

Accounting software has made the process of recording transactions so much easier that the general journal format is rarely needed. For instance, entries are often generated automatically when a check or sales invoice is prepared.)

Please let us know how we can improve this explanation

No Thanks

Close

Sample Transaction #2

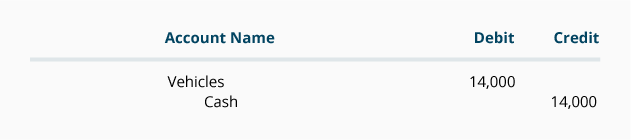

Marilyn illustrates for Joe a second transaction. On December 2, Direct Delivery purchases a used delivery van for $14,000 by writing a check for $14,000. The two accounts involved are Cash and Vehicles (or Delivery Equipment). When the check is written, the accounting software will automatically make the entry into these two accounts.

Marilyn explains to Joe what is happening within the software. Since the company pays $14,000, the Cash account is credited. (Accountants consider the checking account to be Cash, and the TIP you learned is that when cash is paid, you credit Cash.) So we know that the Cash account will be credited for $14,000 and we know the other account will have to be debited for $14,000. We need only identify the best account to debit. In this case we choose Vehicles (or Delivery Equipment) and the entry in the general journal format is:

After the vehicle transaction is recorded, the balance sheet will look like this:

Notice that the balance sheet and the accounting equation remain in balance:

As you can see in the balance sheet, the asset Cash decreased by $14,000 and another asset Vehicles increased by $14,000. Liabilities and stockholders’ equity were not involved and did not change.

Please let us know how we can improve this explanation

No Thanks

Close

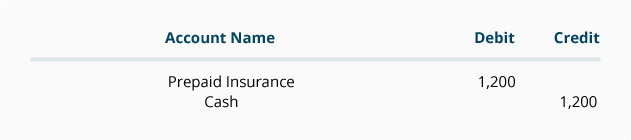

Sample Transaction #3

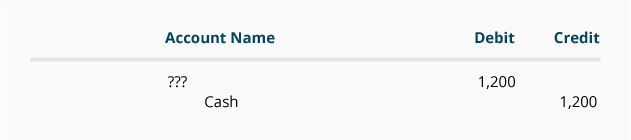

The third sample transaction also occurs on December 2 when Joe contacts an insurance agent regarding insurance coverage for the vehicle Direct Delivery just purchased. The agent informs him that $1,200 will provide insurance protection for the next six months. Joe immediately writes a check for $1,200 and mails it to the insurance company.

Let’s consider this transaction. Using double entry, we know there must be a minimum of two accounts involved—one (or more) of the accounts must be debited, and one (or more) must be credited.

Since a check is written, we know that one of the accounts involved is Cash. Since cash was paid, the Cash account will be credited. (Take another look at the last TIP.) While we have not yet identified the second account, what we do know for certain is that the second account will have to be debited.

At this point we have most of the entry—all we are missing is the name of the account to be debited:

We know the transaction involves insurance, and a quick look through the chart of accounts reveals two possibilities:

Prepaid Insurance (an asset account reported on the balance sheet) and Insurance Expense (an expense account reported on the income statement)

Assets include costs that are not yet expired (not yet used up), while expenses are costs that have expired (have been used up). Since the $1,200 payment is for an expense that will not expire in its entirety within the current month, it would be logical to debit the account Prepaid Insurance. (At the end of each month, when $200 has expired, $200 must be moved from Prepaid Insurance to Insurance Expense.)

The entry in the general journal format to record Direct Delivery’s payment is:

After the first three transactions have been recorded, the balance sheet will look like this:

Again, the balance sheet and the accounting equation are in balance and all of the changes occurred on the asset/left/debit side of the accounting equation. Liabilities and Stockholders’ Equity were not affected by the insurance transaction or the vehicle purchase.

Please let us know how we can improve this explanation

No Thanks

Close

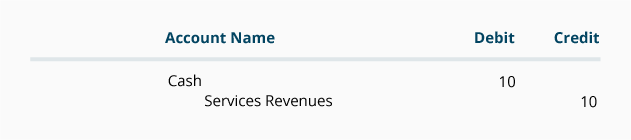

Sample Transaction #4

The fourth transaction occurs on December 3, when a customer gives Direct Delivery a check for $10 to deliver two parcels on that day. Because of double entry, we know there must be a minimum of two accounts involved—one of the accounts must be debited, and one of the accounts must be credited.

Because Direct Delivery received $10, it must debit the account Cash. It must also credit a second account for $10. The second account will be Service Revenues, an income statement account. The reason Service Revenues is credited is because Direct Delivery must report that it earned $10 (not because it received $10). Recording revenues when they are earned results from a basic accounting principle known as the revenue recognition principle. The following tip reflects that principle.

Here’s a Tip

Revenues accounts are credited when the company earns a fee (or sells merchandise) regardless of whether cash is received at the time.

Here are the two parts of the transaction as they would look in the general journal format:

Please let us know how we can improve this explanation

No Thanks

Close

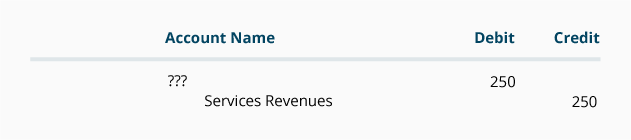

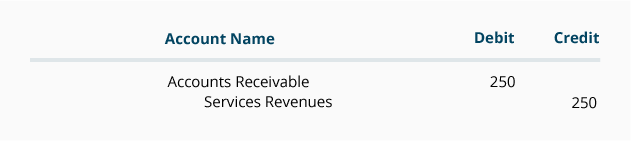

Sample Transaction #5

Let’s assume that on December 3 the company gets its second customer—a local company that needs to have 50 parcels delivered immediately. Joe’s price of $250 is very appealing, so Joe’s company is hired to deliver the parcels. The customer tells Joe to submit an invoice for the $250, and they will pay it within seven days.

Joe delivers the 50 parcels on December 3 as agreed, meaning that on December 3 Direct Delivery has earned $250. Therefore, the $250 is reported as revenues on December 3, even though the company did not receive any cash on that day. The effort needed to complete the job was done on December 3. (Depositing the check for $250 in the bank when it arrives seven days later is not considered to require any effort.)

Let’s identify the two accounts involved and determine which needs a debit and which needs a credit.

Because Direct Delivery has earned the fees, one account will be a revenues account, such as Service Revenues. (If you refer back to the last TIP, you will read that revenue accounts—such as Service Revenues—are usually credited, meaning the second account will need to be debited.)

In the general journal format, here’s what we have identified so far:

We know that the unnamed account cannot be Cash because the company did not receive money on December 3. However, the company has earned the right to receive the money in seven days. The account title for the money that Direct Delivery has a right to receive for having provided the service is Accounts Receivable (an asset account).

Again, reporting revenues when they are earned results from the basic accounting principle known as the revenue recognition principle.

Please let us know how we can improve this explanation

No Thanks

Close

Sample Transaction #6

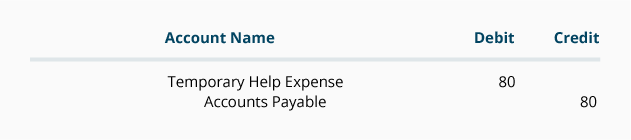

For simplicity, let’s assume that the only expense incurred by Direct Delivery so far was a fee to a temporary help agency for a person to help Joe deliver parcels on December 3. The temp agency fee is $80 and is to be paid by December 12.

Since Direct Delivery did not pay cash immediately, you cannot credit Cash. But because the company owes someone the money for its purchase, we say it has an obligation or liability to pay. Most accounts involved with obligations have the word “payable” in their name, and one of the most frequently used accounts is Accounts Payable. Also keep in mind that expenses are almost always debited.

The accounts and amounts for the temporary help are:

Here’s a Tip

Expenses are (almost) always debited.

Here’s a Tip

If a company does not pay cash right away for an expense or for an asset, you cannot credit Cash. Because the company owes someone the money for its purchase, we say it has an obligation or liability to pay. The most likely liability account involved in business obligations is Accounts Payable.

Revenues and expenses appear on the income statement as shown below:

After the entries through December 3 have been recorded, the balance sheet will look like this:

Notice that the year-to-date net income (bottom line of the income statement) increased stockholders’ equity by the same amount, $180. This connection between the income statement and balance sheet is important. For one, it keeps the balance sheet and the accounting equation in balance. Secondly, it demonstrates that revenues will cause the stockholders’ equity to increase and expenses will cause stockholders’ equity to decrease. After the end of the year financial statements are prepared, you will see that the income statement accounts (revenue accounts and expense accounts) will be closed or zeroed out and their balances will be transferred into the Retained Earnings account. This will mean the revenue and expense accounts will start the new year with zero balances—allowing the company “to keep score” for the new year.

Marilyn suggested that perhaps this introduction was enough material for their first meeting. She wrote out the following notes, summarizing for Joe the important points of their discussion:

When a company pays cash for something, the company will credit Cash and will have to debit a second account. Assuming that a company prepares monthly financial statements—

If the amount is used up or will expire in the current month, the account to be debited will be an expense account. (Advertising Expense, Rent Expense, Wages Expense are three examples.)

If the amount is not used up or does not expire in the current month, the account to be debited will be an asset account. (Examples are Prepaid Insurance, Supplies, Prepaid Rent, Prepaid Advertising, Prepaid Association Dues, Land, Buildings, Vehicles, and Equipment.)

If the amount reduces a company’s obligations, the account to be debited will be a liability account. (Examples include Accounts Payable, Notes Payable, Wages Payable, and Interest Payable.)

When a company receives cash, the company will debit Cash and will have to credit another account. Assuming that a company will prepare monthly financial statements—

If the amount received is from a cash sale, or for a service that has just been performed but has not yet been recorded, the account to be credited is a revenue account such as Service Revenues or Fees Earned.

If the amount received is an advance payment for a service that has not yet been performed or earned, the account to be credited is Unearned Revenue.

If the amount received is a payment from a customer for a sale or service delivered earlier and has already been recorded as revenue, the account to be credited is Accounts Receivable.

If the amount received is the proceeds from the company signing a promissory note, the account to be credited is Notes Payable.

If the amount received is an investment of additional money by the owner of the corporation, a stockholders’ equity account such as Common Stock is credited.

Note: To learn more about debits and credits, visit our Explanation and Quiz for this topic.

Revenues are recorded as Service Revenues or Sales when the service or sale has been performed, not when the cash is received. This reflects the basic accounting principle known as the revenue recognition principle.

Expenses are matched with revenues or with the period of time shown in the heading of the income statement, not in the period when the expenses were paid. This reflects the basic accounting principle known as the matching principle or the expense recognition principle.

The financial statements also reflect the basic accounting principle known as the cost principle. This means assets are shown on the balance sheet at their original cost or less and not at their current value. The income statement expenses also reflect the cost principle. For example, the depreciation expense is based on the original cost of the asset being depreciated and not on the current replacement cost.

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Accounting Basics materials (see the full outline below).

We also recommend joining PRO Plus to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.

Please let us know how we can improve this explanation

No Thanks

Close

The standards, rules, guidelines, and industry-specific requirements for financial reporting.

Fees earned from providing services and the amounts of merchandise sold. Under the accrual basis of accounting, revenues are recorded at the time of delivering the service or the merchandise, even if cash is not received at the time of delivery. Often the term income is used instead of revenues.

Examples of revenue accounts include: Sales, Service Revenues, Fees Earned, Interest Revenue, Interest Income. Revenue accounts are credited when services are performed/billed and therefore will usually have credit balances. At the time that a revenue account is credited, the account debited might be Cash, Accounts Receivable, or Unearned Revenue depending if cash was received at the time of the service, if the customer was billed at the time of the service and will pay later, or if the customer had paid in advance of the service being performed.

If the revenues earned are a main activity of the business, they are considered to be operating revenues. If the revenues come from a secondary activity, they are considered to be nonoperating revenues. For example, interest earned by a manufacturer on its investments is a nonoperating revenue. Interest earned by a bank is considered to be part of operating revenues.

Costs that are matched with revenues on the income statement. For example, Cost of Goods Sold is an expense caused by Sales. Insurance Expense, Wages Expense, Advertising Expense, Interest Expense are expenses matched with the period of time in the heading of the income statement. Under the accrual basis of accounting, the matching is NOT based on the date that the expenses are paid.

Expenses associated with the main activity of the business are referred to as operating expenses. Expenses associated with a peripheral activity are nonoperating expenses or other expenses. For example, a retailer’s interest expense is a nonoperating expense. A bank’s interest expense is an operating expense.

Generally, expenses are debited to a specific expense account and the normal balance of an expense account is a debit balance. When an expense account is debited, the account credited might be Cash (if cash was paid at the time of the expense), Accounts Payable (if cash will be paid after the expense is recorded), or Prepaid Expense (if cash was paid before the expense was recorded.)

Things that are resources owned by a company and which have future economic value that can be measured and can be expressed in dollars. Examples include cash, investments, accounts receivable, inventory, supplies, land, buildings, equipment, and vehicles.

Assets are reported on the balance sheet usually at cost or lower. Assets are also part of the accounting equation: Assets = Liabilities + Owner’s (Stockholders’) Equity.

Some valuable items that cannot be measured and expressed in dollars include the company’s outstanding reputation, its customer base, the value of successful consumer brands, and its management team. As a result these items are not reported among the assets appearing on the balance sheet.

Obligations of a company or organization. Amounts owed to lenders and suppliers. Liabilities often have the word “payable” in the account title. Liabilities also include amounts received in advance for a future sale or for a future service to be performed.

One of the main financial statements (along with the statement of comprehensive income, balance sheet, statement of cash flows, and statement of stockholders’ equity). The income statement is also referred to as the profit and loss statement, P&L, statement of income, and the statement of operations. The income statement reports the revenues, gains, expenses, losses, net income and other totals for the period of time shown in the heading of the statement. If a company’s stock is publicly traded, earnings per share must appear on the face of the income statement.

The balance sheet is prepared in order to report an organization’s financial position at the end of an accounting period, such as midnight on December 31.

A corporation’s balance sheet reports its:

Assets (resources that were acquired in past transactions)

Stockholders’ equity (the difference between the amount of assets and liabilities)

The statement of cash flows (or cash flow statement) is one of the main financial statements (along with the income statement and balance sheet). The statement of cash flows reports the sources and uses of cash by operating activities, investing activities, financing activities, and certain supplemental information for the period specified in the heading of the statement.

The principle that requires a company to match expenses with related revenues in order to report a company’s profitability during a specified time interval. Ideally, the matching is based on a cause and effect relationship: sales causes the cost of goods sold expense and the sales commissions expense. If no cause and effect relationship exists, accountants will show an expense in the accounting period when a cost is used up or has expired. Lastly, if a cost cannot be linked to revenues or to an accounting period, the expense will be recorded immediately. An example of this is Advertising Expense and Research and Development Expense.

Usually financial statements refer to the balance sheet, income statement, statement of comprehensive income, statement of cash flows, and statement of stockholders’ equity.

The balance sheet reports information as of a date (a point in time). The income statement, statement of cash flows, statement of comprehensive income, and the statement of stockholders’ equity report information for a period of time (or time interval) such as a year, quarter, or month.

The type of stock that is present at every corporation. (Some corporations have preferred stock in addition to their common stock.) Shares of common stock provide evidence of ownership in a corporation. Holders of common stock elect the corporation’s directors and share in the distribution of profits of the company via dividends. If the corporation were to liquidate, the secured lenders would be paid first, followed by unsecured lenders, preferred stockholders (if any), and lastly the common stockholders.

A bill issued by a seller of merchandise or by the provider of services. The seller refers to the invoice as a sales invoice and the buyer refers to the same invoice as a vendor invoice.

The statement of comprehensive income covers the same period of time as the income statement, and consists of two major sections:

Net income (taken from the income statement)

Other comprehensive income (adjustments involving foreign currency translation, hedging, and postretirement benefits)

The sum of these two amounts is known as comprehensive income.

The amount of other comprehensive income is added/subtracted from the balance in the stockholders’ equity account Accumulated Other Comprehensive Income.

A financial statement that shows all of the changes to the various stockholders’ equity accounts during the same period(s) as the income statement, statement of comprehensive income, and statement of cash flows. It includes the amounts of accumulated other comprehensive income.

The accounting method under which revenues are recognized on the income statement when they are earned (rather than when the cash is received). The balance sheet is also affected at the time of the revenues by either an increase in Cash (if the service or sale was for cash), an increase in Accounts Receivable (if the service was performed on credit), or a decrease in Unearned Revenues (if the service was performed after the customer had paid in advance for the service).

Under the accrual basis of accounting, expenses are matched with revenues on the income statement when the expenses expire or title has transferred to the buyer, rather than at the time when expenses are paid. The balance sheet is also affected at the time of the expense by a decrease in Cash (if the expense was paid at the time the expense was incurred), an increase in Accounts Payable (if the expense will be paid in the future), or a decrease in Prepaid Expenses (if the expense was paid in advance).

An accounting method wherein revenues are recognized when cash is received and expenses are recognized when paid. This method is inferior to the accrual basis of accounting where revenues are recognized when they are earned and expenses are matched to revenues or the accounting period when they are incurred (rather than paid). The cash basis of accounting is usually followed by individuals and small companies, but is not in compliance with accounting’s matching principle.

The accounting guideline requiring that revenues be shown on the income statement in the period in which they are earned, not in the period when the cash is collected. This is part of the accrual basis of accounting (as opposed to the cash basis of accounting).

This account is a non-operating or “other” expense for the cost of borrowed money or other credit. The amount of interest expense appearing on the income statement is the cost of the money that was used during the time interval shown in the heading of the income statement, not the amount of interest paid during that period of time.

The result of two or more amounts being combined. For example, net sales is equal to gross sales minus sales returns, sales allowances, and sales discounts. The net realizable value of accounts receivable is the combination of the debit balance in accounts receivable and the credit balance in the allowance for doubtful accounts. The book value of equipment is also a net amount: the cost of the equipment minus the accumulated depreciation of the equipment.

This is the bottom line of the income statement. It is the mathematical result of revenues and gains minus the cost of goods sold and all expenses and losses (including income tax expense if the company is a regular corporation) provided the result is a positive amount. If the net amount is a negative amount, it is referred to as a net loss.

The bottom line of the income statement when revenues and gains are less than the aggregate amount of cost of goods sold, operating expenses, losses, and income taxes (if the company is a regular corporation).

The difference between assets and liabilities, such as stockholders’ equity, owner’s equity, or a nonprofit organization’s net assets.

Also used to indicate an owner’s interest in a personal asset. For example, the owner of a $200,000 house with a $75,000 mortgage loan is said to have equity of $125,000.

A record in the general ledger that is used to collect and store similar information. For example, a company will have a Cash account in which every transaction involving cash is recorded. A company selling merchandise on credit will record these sales in a Sales account and in an Accounts Receivable account.

A long-term asset account that reports a company’s cost of automobiles, trucks, etc. The account is reported under the balance sheet classification property, plant, and equipment. Vehicles are depreciated over their useful lives.

A current asset account which includes currency, coins, checking accounts, and undeposited checks received from customers. The amounts must be unrestricted. (Restricted cash should be recorded in a different account.)

A current asset representing the cost of supplies on hand at a point in time. The account is usually listed on the balance sheet after the Inventory account.

A related account is Supplies Expense, which appears on the income statement. The amount in the Supplies Expense account reports the amounts of supplies that were used during the time interval indicated in the heading of the income statement.

Equipment is a noncurrent or long-term asset account which reports the cost of the equipment. Equipment will be depreciated over its useful life by debiting the income statement account Depreciation Expense and crediting the balance sheet account Accumulated Depreciation (a contra asset account).

A current asset representing amounts paid in advance for future expenses. As the expenses are used or expire, expense is increased and prepaid expense is decreased.

The amount of insurance that was incurred/used up/expired during the period of time appearing in the heading of the income statement. The amount of insurance premiums that have not yet expired should be reported in the current asset account Prepaid Insurance.

A current asset which indicates the cost of the insurance contract (premiums) that have been paid in advance. It represents the amount that has been paid but has not yet expired as of the balance sheet date.

A related account is Insurance Expense, which appears on the income statement. The amount in the Insurance Expense account should report the amount of insurance expense expiring during the period indicated in the heading of the income statement.

The accounting guideline requiring amounts in the accounts and on the financial statements to be the actual cost rather than the current value. Accountants can show an amount less than cost due to conservatism, but accountants are generally prohibited from showing amounts greater than cost. (Certain investments will be shown at fair value instead of cost.)

This accounting guideline states that if doubt exists between two acceptable alternatives (in other words the accountant needs to break a tie), the accountant should choose the alternative that will result in a lesser asset amount and/or a lesser profit. A classic example is inventory where the net realizable value (NRV) is less than the actual cost. The accountant must decide whether to leave the inventory at cost or to reduce the inventory amount to its NRV. Conservatism directs the accountant to reduce the inventory to the lower amount (NRV). This results in a lower asset amount and a debit to an income statement account, such as Loss from Reducing Inventory to NRV

A current asset whose ending balance should report the cost of a merchandiser’s products awaiting to be sold. The inventory of a manufacturer should report the cost of its raw materials, work-in-process, and finished goods. The cost of inventory should include all costs necessary to acquire the items and to get them ready for sale.

When inventory items are acquired or produced at varying costs, the company will need to make an assumption on how to flow the changing costs. See cost flow assumption.

If the net realizable value of the inventory is less than the actual cost of the inventory, it is often necessary to reduce the inventory amount.

Net realizable value (NRV) is the cash amount that a company expects to receive. Hence, net realizable value is sometimes referred to as cash realizable value.

The systematic allocation of the cost of an asset from the balance sheet to Depreciation Expense on the income statement over the useful life of the asset. (The depreciation journal entry includes a debit to Depreciation Expense and a credit to Accumulated Depreciation, a contra asset account). The purpose is to allocate the cost to expense in order to comply with the matching principle. It is not intended to be a valuation process. In other words, the amount allocated to expense is not indicative of the economic value being consumed. Similarly, the amount not yet allocated is not an indication of its current market value.

The income statement account which contains a portion of the cost of plant and equipment that is being matched to the time interval shown in the heading of the income statement. (There is no depreciation expense for land.)

Also referred to as book value or carrying value; the cost of a plant asset minus the accumulated depreciation since the asset was acquired. This net amount is not an indication of the asset’s fair market value. Also used in reference to bonds payable: the face amount in Bonds Payable plus Premium on Bonds Payable or minus Discount on Bonds Payable and minus the unamortized issue costs.

The book value of an asset is the amount of cost in its asset account less the accumulated depreciation applicable to the asset. The book value of an asset is also referred to as the carrying value of the asset.

The book value of a company is the amount of owner’s or stockholders’ equity. The book value of bonds payable is the combination of the accounts Bonds Payable and Discount on Bonds Payable or the combination of Bonds Payable and Premium on Bonds Payable.

A long-term asset account reported on the balance sheet under the heading of property, plant, and equipment. Included in this account would be copiers, computers, printers, fax machines, etc.

A long-term asset account that reports the cost of real property exclusive of the cost of any constructed assets on the property. Land usually appears as the first item under the balance sheet heading of Property, Plant and Equipment. Generally, land is not depreciated.

The amount of principal due on a formal written promise to pay. Loans from banks are included in this account.

This current liability account reports the amount of interest the company owes as of the date of the balance sheet. (Future interest is not recorded as a liability.)

This current liability account will show the amount a company owes for items or services purchased on credit and for which there was not a promissory note. This account is often referred to as trade payables (as opposed to notes payable, interest payable, etc.)

A current liability account that reports the amounts owed to employees for hours worked but not yet paid as of the date of the balance sheet.

A liability account that reports amounts received in advance of providing goods or services. When the goods or services are provided, this account balance is decreased and a revenue account is increased. To learn more, see Explanation of Adjusting Entries.

A balance sheet liability account that reports amounts received in advance of being earned. For example, if a company receives $10,000 today to perform services in the next accounting period, the $10,000 is unearned in this accounting period. It is deferred to the next accounting period by crediting a liability account such as Unearned Revenues. Next period (when it is earned) a journal entry will be made to debit the liability account and to credit a revenue account.

A liability account on the books of a company receiving cash in advance of delivering goods or services to the customer. The entry on the books of the company at the time the money is received in advance is a debit to Cash and a credit to Customer Deposits.

Under the accrual basis of accounting, the Service Revenues account reports the fees earned by a company during the time period indicated in the heading of the income statement. Service Revenues include work completed whether or not it was billed. Service Revenues is an operating revenue account and will appear at the beginning of the company’s income statement.

A sole proprietorship is a simple form of business where there is one owner. Legally the owner and the sole proprietorship are the same. However, for accounting purposes the economic entity assumption results in the sole proprietorship’s business transactions being accounted for separately from the owner’s personal transactions.

The stockholders’ equity account that represents the amount paid to a corporation for its common stock that was in excess of the common stock’s par value. This account is sometimes referred to as the premium on common stock (The par value of common stock is recorded in a separate stockholder’s equity account.)

A class of corporation stock that provides for preferential treatment over the holders of common stock in the case of liquidation and dividends. For example, the preferred stockholders will be paid dividends before the common stockholders receive dividends. In exchange for the preferential treatment of dividends, preferred shareholders usually will not share in the corporation’s increasing earnings and instead receive only their fixed dividend.

Generally speaking, retained earnings is a stockholders’ equity account that reports the net income of a corporation from its inception until the balance sheet date less the dividends declared from its inception to the date of the balance sheet.

A separate line within stockholders’ equity that reports the corporation’s cumulative income that has not been reported as part of net income on the corporation’s income statement. The items that would be included in this line involve the income or loss involving foreign currency transactions, hedges, and pension liabilities.

A corporation’s own stock that has been repurchased from stockholders. Also a stockholders’ equity account that usually reports the cost of the stock that has been repurchased.

Often this account appears as a line in the retained earnings section of stockholders’ equity (balance sheet) and will show the year-to-date net income. The reason is that some accounting software will not put the current year’s net income into the Retained Earnings account until the accounting year is finished.

A listing of the accounts available in the accounting system in which to record entries. The chart of accounts consists of balance sheet accounts (assets, liabilities, stockholders’ equity) and income statement accounts (revenues, expenses, gains, losses). The chart of accounts can be expanded and tailored to reflect the operations of the company.

A current asset resulting from selling goods or services on credit (on account). Invoice terms such as (a) net 30 days or (b) 2/10, n/30 signify that a sale was made on account and was not a cash sale.

The amount of principal due on a formal written promise to pay. Loans from banks are included in this account.

This current liability account will show the amount a company owes for items or services purchased on credit and for which there was not a promissory note. This account is often referred to as trade payables (as opposed to notes payable, interest payable, etc.)

A current liability account that reports the amounts owed to employees for hours worked but not yet paid as of the date of the balance sheet.

The type of stock that is present at every corporation. (Some corporations have preferred stock in addition to their common stock.) Shares of common stock provide evidence of ownership in a corporation. Holders of common stock elect the corporation’s directors and share in the distribution of profits of the company via dividends. If the corporation were to liquidate, the secured lenders would be paid first, followed by unsecured lenders, preferred stockholders (if any), and lastly the common stockholders.

A stockholders’ equity account that generally reports the net income of a corporation from its inception until the balance sheet date less the dividends declared from its inception to the date of the balance sheet.

The amounts earned on money invested. Often this is interest and dividends earned on a company’s investment in stocks and bonds of other companies.

The compensation earned by hourly-paid employees during the interval of time indicated in the heading of the income statement. Under the accrual basis of accounting, the date that wages are paid does not determine when the wages are reported as an expense

Under the accrual basis of accounting, the account Rent Expense will report the cost of occupying space during the time interval indicated in the heading of the income statement, whether or not the rent was paid within that period. (Rent that has been paid in advance is shown on the balance sheet in the current asset account Prepaid Rent.) Depending upon the use of the space, Rent Expense could appear on the income statement as part of administrative expenses or selling expenses. If the rented space was used to manufacture goods, the rent would be part of the cost of the products produced.

The income statement account which contains a portion of the cost of plant and equipment that is being matched to the time interval shown in the heading of the income statement. (There is no depreciation expense for land.)

Assets = Liabilities + Owner’s Equity. For a corporation the equation is Assets = Liabilities + Stockholders’ Equity. For a nonprofit organization the accounting equation is Assets = Liabilities + Net Assets. Because of double-entry accounting this equation should be in balance at all times. The accounting equation is expressed in the financial statement known as the balance sheet.

The accounting term that means an entry will be made on the left side of an account.

That part of the accounting system which contains the balance sheet and income statement accounts used for recording transactions.

A balance on the right side (credit side) of an account in the general ledger.

The record of journal entries appearing in order by date. Some refer to the journal as the book of original entry, since the entries are first recorded in a journal. From the journal the entries will be posted to the designated accounts in the general ledger. With manual systems there are likely to be a sales journal, purchases journal, cash receipts journal, cash disbursements journal, and the general journal. With computerized accounting systems, it is likely that the general journal will be used sparingly. The software is likely to record the other transactions automatically as invoices are entered, checks are prepared, receipts processed, etc.

A long term asset account containing the cost of delivery equipment acquired by a company and used in its business. The account will appear on the balance sheet under the heading of Property, Plant and Equipment. There will be a related contra asset account Accumulated Depreciation: Delivery Equipment where the depreciation expense is accumulated.

The bank account on which checks are written or drawn. A bank refers to checking accounts as demand deposits.

A company’s net income from the start of the current accounting year until a specified date. For example, the year-to-date net income at May 31, 2025 for a calendar year company is the net income from January 1, 2025 until May 31, 2025. For a company with a fiscal year beginning on July 1, 2024 the year-to-date net income at May 31, 2025 is the net income for the 11-month period from July 1, 2024 through May 31, 2025.

Advertising Expense is the income statement account which reports the dollar amount of ads run during the period shown in the income statement. Advertising Expense will be reported under selling expenses on the income statement.

A current asset account that reports the amount of future rent expense that was paid in advance of the rental period. The amount reported on the balance sheet is the amount that has not yet been used or expired as of the balance sheet date.

A current asset that reports the amount paid for advertising that has not yet taken place. When the advertising occurs the prepaid advertising is reduced and advertising expense is recorded.

Buildings is a noncurrent or long-term asset account which shows the cost of a building (excluding the cost of the land). Buildings will be depreciated over their useful lives by debiting the income statement account Depreciation Expense and crediting the balance sheet account Accumulated Depreciation.

An income statement account that reports the amount of service revenues earned during the time interval indicated in the heading of the income statement. (Under the accrual basis of accounting, fees earned are reported in the time period in which they are earned and not in the period in which the company receives payment.)

For the past 52 years, Harold Averkamp (CPA, MBA) has

worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.