For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.

Before you begin: If you enjoy this free In-Depth Explanation, we recommend trying our PRO materials (used by 80,000+ professionals). You'll receive lifetime access to our certificates of achievement, video training, flashcards, visual tutorials, quick tests, cheat sheets, guides, business forms, printable PDF files, and more. Earn badges, points, and medals as you track your progress and display your achievements on your public profile page.

Introduction

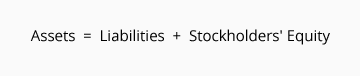

If you were to reduce a corporation’s entire balance sheet into its most skeletal form, you would end up with the following accounting equation:

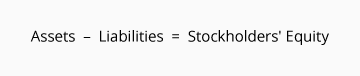

As you can see, stockholders’ equity is one of the three main components of a corporation’s balance sheet. If you rearrange the equation, you will see that stockholders’ equity is the difference between the asset amounts and the liability amounts:

Stockholders’ equity is to a corporation what owner’s equity is to a sole proprietorship. Owners of a corporation are called stockholders (or shareholders), because they own (or hold) shares of the company’s stock. Stock certificates are paper evidence of ownership in a corporation.

U. S. corporations are organized in, and are regulated by, one of the fifty states. Because laws differ somewhat from state to state, accounting for corporations also differs somewhat from state to state. (If you need to determine the specific rules for a corporation in a specific state, you should seek the guidance of a professional who is knowledgeable with the laws of that state.) For our purposes, we will focus on the structure and concepts that are fundamental to most U.S corporations.

The concepts and vocabulary we will introduce in this topic (such as dividends, earnings per share, and book value) are important not only to accountants, but to investors, lenders, business owners, business students, and others.

Please let us know how we can improve this explanation

No Thanks

Close

What Is a Corporation?

Most of the world’s largest companies do business as corporations. Companies such as Wal-Mart, Amazon, Apple, Exxon Mobil, and CVS Health—each with sales in excess of $200 billion annually—are corporations. As opposed to a sole proprietorship or a partnership, a corporation is a business that is recognized by law as a separate legal entity with its own powers, responsibilities, and liabilities. Before the owners/managers of a business choose to incorporate their business (become corporations), however, they should examine the advantages and disadvantages of doing so.

Advantages

A corporation has several advantages over the sole proprietorship and the partnership form of business. The following are four of the advantages:

Limited liability for the owners. Generally, the owners of a corporation can lose no more than the amount they have invested in that corporation. On the other hand, with a sole proprietorship or partnership, an owner could lose not only her or his investment, but could also lose other personal assets as well. In other words, the corporate form of business “shields” the owners from most of the corporation’s creditors. This occurs because corporations are considered to be legal entities, separate and distinct from their owners. (Due to their legal entity status, a corporation can sue others, can be sued, and must pay income taxes on its taxable income.)

Ease in which owners can sell their ownership interest. If the stock is publicly traded, investors can sell their ownership interest in a corporation in a matter of minutes simply by giving instructions to their stockbroker or through a computer app. If the stock is not publicly traded, the stock certificate can be transferred to another owner by signing a transfer statement.

Continuity. When a stockholder sells shares of stock, the transaction is between the seller and the buyer of the stock. Unless the corporation is the buyer or the seller, the corporation is not involved in the transaction. This means that even if a corporation’s stock is the most actively traded stock of the day, the corporation itself will not skip a beat in its day-to-day operations. When notified of a transfer between stockholders, the corporation merely changes in its records the name of the owner of the shares.

Ease in raising money. Because of limited liability and the ease of buying/selling shares, it is easy to understand why investors are more attracted to investing in corporations rather than in sole proprietorships or partnerships. This investor attraction allows corporations to raise the capital needed to manage and expand their operations.

Disadvantages

Some view the legal complexity of starting and running a corporation to be a disadvantage. To incorporate, an application must be filed with and approved by one of the fifty states, and once approved, the corporation must comply with that state’s regulations. In contrast, a sole proprietorship can be started in minutes, sometimes with nothing more than opening a business checking account. Many of the legal requirements imposed on a corporation do not apply to sole proprietorships.

Another disadvantage associated with corporations is the possibility of “double taxation” on the dividends it pays. Some argue that a regular corporation’s net income is first taxed on the corporation’s income tax return. Then, if the corporation distributes some of the after tax net income to the stockholders as a dividend, the dividend will be taxed on the stockholders’ personal income tax returns. (To gain more insight into this and to minimize or to avoid this potential problem, you should discuss various forms of business structures with tax and legal professionals.)

Governance

The owners of corporations are referred to as stockholders or shareholders, because they hold the shares of stock, which serve as the evidence of their ownership. (The terms stockholders and shareholders are used interchangeably.)

Because it would be impossible for 30,000 stockholders to sit around a boardroom table and give meaningful input to the direction of their company, the stockholders elect a board of directors as their representatives in the corporation’s affairs. The board of directors formulates the corporation’s policies and appoints officers of the corporation to carry out those policies. The board of directors also declares the amount and timing of dividend distributions, if any, to the stockholders.

The officers of a corporation are appointed by the corporation’s board of directors to carry out (or execute) the policies established by the board of directors. The officers include the president, chief executive officer (CEO), chief operating officer (COO), chief financial officer (CFO), vice presidents, treasurer, secretary, and controller.

Please let us know how we can improve this explanation

No Thanks

Close

Common Stock

If a corporation has issued only one type, or class, of stock it will be common stock. (Preferred stock is discussed later.) While “common” sounds rather ordinary, it is the common stockholders who elect the board of directors, vote on whether to have a merger with another company, and see their shares of stock increase in value if the corporation is successful.

When an investor gives a corporation money in return for part ownership, the corporation issues a certificate or digital record of ownership interest to the stockholder. This certificate is known as a stock certificate, capital stock, or stock.

The common stockholder has an ownership interest in the corporation; it is not a creditor or lender. Hence, the common stock does not come due or mature. If stockholders want to sell their stock, they must find a buyer usually through the services of a stockbroker or an online app. Nowhere on the stock certificate is it indicated what the stock is worth (or what price was paid to acquire it). In a market of buyers and sellers, the current value of any stock fluctuates moment-by-moment.

A corporation’s accounting records are involved in stock transactions only when the corporation is the issuer, seller, or buyer of its own stock. For example, if 500,000 shares of Apple Computer stock are traded on the stock exchange today, and if none of those shares is newly issued, sold, or repurchased by Apple Computer, then Apple Computer’s accounting records are not affected. The corporation will go about its routine business operations without even noticing that there were some changes among its stockholders.

Shares

Some investors may have large ownership interests in a given corporation, while other investors own a very small part. To keep track of each investor’s ownership interest, corporations use a unit of measurement referred to as a share (or share of stock). The number of shares that an investor owns is printed on the investor’s stock certificate or digital record. This information is also maintained in the corporate secretary’s records, which are separate from the corporation’s accounting records.

If an investor owns 1,000 shares and the corporation has issued and has outstanding a total of 100,000 shares, the investor is said to have a 1% ownership interest in the corporation. The other owners have the combined remaining 99% ownership interest.

Authorized shares

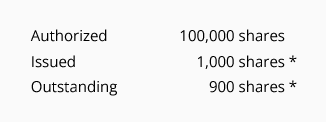

When a business applies for incorporation to a secretary of state, its approved application will specify the classes (or types) of stock, the par value of the stock, and the number of shares it is authorized to issue. When its articles of incorporation are prepared, a business will often request authorization to issue a larger number of shares than what is immediately needed.

To illustrate, assume that the organizers of a new corporation need to issue 1,000 shares of common stock to get their corporation up and running. However, they foresee a future need to issue additional shares. As a result, they decide that their articles of incorporation should authorize 100,000 shares of common stock, even though only 1,000 shares will be issued at the time that the corporation is formed.

Issued shares

When a corporation sells some of its authorized shares, the shares are described as issued shares. The number of issued shares is often considerably less than the number of authorized shares.

Corporations issue (or sell) shares of stock to obtain cash from investors, to acquire another company (the new shares are given to the owners of the other company in exchange for their ownership interest), to acquire certain assets or services, and as an incentive/reward for key officers of the corporation.

The par value of a share of stock is sometimes defined as the legal capital of a corporation. However, some states allow corporations to issue shares with no par value. If a state requires a par value, the value of common stock is usually an insignificant amount that was required by state laws many years ago. If the common stock has a par value, then whenever a share of stock is issued the par value is recorded in a separate stockholders’ equity account in the general ledger. Any proceeds that exceed the par value are credited to another stockholders’ equity account. This required accounting (discussed later) means that you can determine the number of issued shares by dividing the balance in the par value account by the par value per share.

Outstanding shares

If a share of stock has been issued and has not been reacquired by the corporation, it is said to be outstanding. For example, if a corporation initially sells 2,000 shares of its stock to investors, and if the corporation did not reacquire any of this stock, this corporation is said to have 2,000 shares of stock outstanding.

The number of outstanding shares is always less than or equal to the number of issued shares. The number of issued shares is always less than (or equal to) the authorized number of shares. Here is a mathematical presentation:

When a corporation reacquires shares of its own stock and does not retire the shares, the corporation is said to have treasury stock. (Treasury stock will be discussed later.) The number of outstanding shares is equal to the number of issued shares minus the number of treasury shares, as shown here:

Here are the terms in descending order (largest to smallest) based on hypothetical amounts:

* The difference between the issued shares and the outstanding shares is the number of shares of treasury stock (100 shares in this example).

Please let us know how we can improve this explanation

No Thanks

Close

Accounting For Stockholders’ Equity

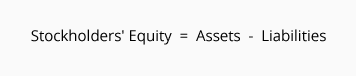

A corporation’s balance sheet reports its assets, liabilities, and stockholders’ equity. Stockholders’ equity is the difference (or residual) of assets minus liabilities.

Because of accounting principles, assets (other than investments in certain securities) are generally reported on the balance sheet at cost (or lower) amounts. As a result, you should not assume that the total amount of stockholders’ equity is equal to the current value, or worth, of the corporation. (For a more thorough discussion of the balance sheet, visit our Balance Sheet Explanation.)

Because of legal requirements, the stockholders’ equity section of a corporation’s balance sheet is more expansive than the owner’s equity section of a sole proprietorship’s balance sheet. For example, state laws require that corporations keep the amounts received from investors separate from the amounts earned through business activity. State laws may also require that the par value be reported in a separate account.

Below are the items that a corporation is required to report on its balance sheet in the stockholder’s equity section. We will discuss them in the order they would appear on a balance sheet:

Paid-in capital (also referred to as contributed capital)

Please let us know how we can improve this explanation

No Thanks

Close

Paid-in Capital or Contributed Capital

Capital stock is a term that encompasses both common stock and preferred stock. Paid-in capital (or contributed capital) is that section of stockholders’ equity that reports the amount a corporation received when it issued its shares of stock.

State laws often require that a corporation is to record and report separately the par amount of issued shares from the amount received that was greater than the par amount. The par amount is credited to Common Stock. The actual amount received for the stock minus the par value is credited to Paid-in Capital in Excess of Par Value.

To illustrate, let’s assume that a corporation’s common stock has a par value of $0.10 per share. On March 10, 2024, one share of stock is issued for $13.00. (The $13 amount is the fair market value based on supply and demand for the stock.) The accountant makes a journal entry to record the issuance of one share of stock along with the corporation’s receipt of the money (note that the “Common Stock” account reflects the par value of $0.10 per share):

While some states require a par value for common stock, other states do not. If there is no par value, some states require a stated value. If this is the case, the entry will be the same as the above except that the term “stated” will be used in place of the term “par”:

If a state does not require a par value or a stated value, the entire proceeds will be credited to the Common Stock account:

Generally speaking, the par value of common stock is minimal and has no economic significance. However, if a state law requires a par (or stated) value, the accountant is required to record the par (or stated) value of the common stock in the account Common Stock.

Please let us know how we can improve this explanation

No Thanks

Close

Retained Earnings

The term retained earnings refers to a corporation’s cumulative net income (from the date of incorporation to the current balance sheet date) minus the cumulative amount of dividends that were declared during that time. An established corporation that has been profitable for many years will often have a very large credit balance in its Retained Earnings account, frequently exceeding the paid-in capital from investors. If, on the other hand, a corporation has experienced significant net losses since it was formed, it could have negative retained earnings (reported as a debit balance instead of the normal credit balance in its Retained Earnings account). When this is the case, the account will be described as Deficit or Accumulated Deficit on the corporation’s balance sheet.

It’s important to understand that a large credit balance in retained earnings does not necessarily mean a corporation has a large cash balance. To determine the amount of cash, one must look at the Cash account in the current asset section of the balance sheet. (For example, a public utility may have a huge retained earnings balance, but its cash was invested in new, expensive power plants. Hence, it has relatively little cash in relationship to its reported amount of retained earnings.)

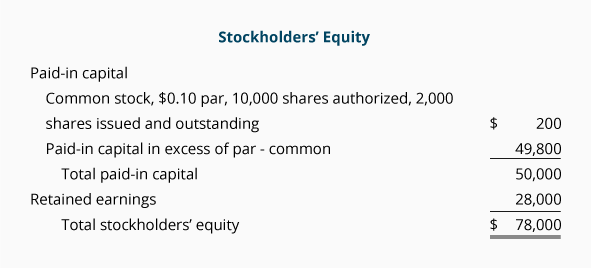

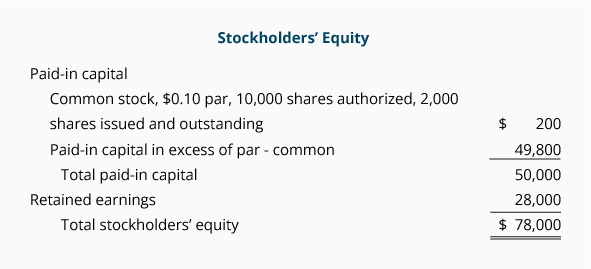

Let’s look at the stockholders’ equity section of a balance sheet for a corporation that has issued only common stock. The stock has a par value of $0.10 per share. There are 10,000 authorized shares, of which 2,000 shares had been issued for $50,000. At the balance sheet date, the corporation had cumulative net income after income taxes of $40,000 and had paid cumulative dividends of $12,000, resulting in retained earnings of $28,000.

Please let us know how we can improve this explanation

No Thanks

Close

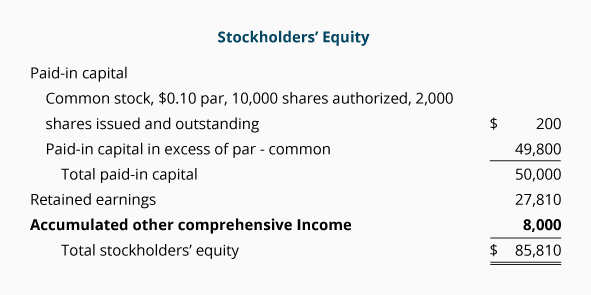

Accumulated Other Comprehensive Income

Accumulated other comprehensive income refers to several items that were not included in net income and retained earnings. Examples include foreign currency translation adjustments and unrealized gains and losses on hedge/derivative financial instruments and postretirement benefit plans.

Below is an example of the reporting of accumulated other comprehensive income of $8,000. Notice that it is reported separately from retained earnings and separately from paid-in capital.

NOTE:

The net income reported on the corporation’s income statement is added to retained earnings.

The other comprehensive income reported on the statement of comprehensive income is added to accumulated other comprehensive income.

Please let us know how we can improve this explanation

No Thanks

Close

Treasury Stock

A corporation may choose to purchase some of its outstanding shares of stock from its shareholders when it has a large amount of idle cash and, in the opinion of its directors, the market price of its stock is sufficiently low. If a corporation purchases a significant amount of its own stock, the corporation’s earnings per share may increase because there are fewer shares outstanding.

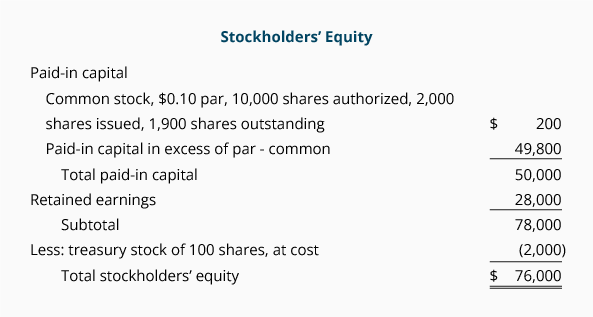

If a corporation purchases some of its stock and does not retire those shares, the shares are called treasury stock. Treasury stock reflects the difference between the number of shares issued and the number of shares outstanding. When a corporation holds treasury stock, a debit balance exists in the general ledger account Treasury Stock (a contra stockholders’ equity account). There are two methods of recording treasury stock: (1) the cost method, and (2) the par value method. We will illustrate the cost method. (The par value method is illustrated in intermediate accounting textbooks.)

Under the cost method, the amount the corporation paid to acquire the shares is debited to the account Treasury Stock. For example, if a corporation acquires 100 shares of its stock at $20 each, the following entry is made:

Stockholders’ equity will appear on the balance sheet as follows:

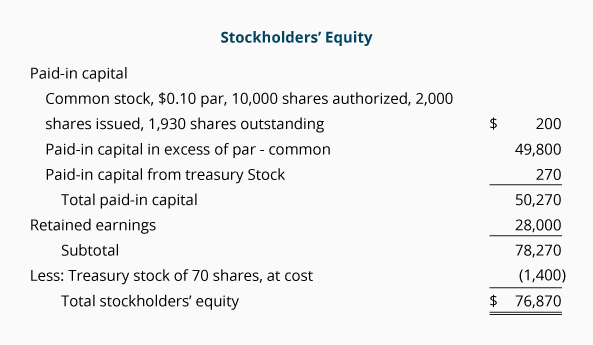

If the corporation were to sell some of its treasury stock, the cash received is debited to Cash, the cost of the shares sold is credited to the stockholders’ equity account Treasury Stock, and the difference goes to another stockholders’ equity account. Note that the difference does not go to an income statement account, as there can be no income statement recognition of gains or losses on treasury stock transactions. (This, of course, is reasonable since the corporation has the ultimate amount of inside information.)

If the corporation sells 30 of the 100 shares of its treasury stock for $29 per share, the entry will be:

Recall that the corporation’s cost to purchase those shares at an earlier date was $20 per share. The $20 per share times 30 shares equals the $600 that was credited above to Treasury Stock. This leaves a debit balance in the account Treasury Stock of $1,400 (70 shares at $20 each).

The difference of $9 per share ($29 of proceeds minus the $20 cost) times 30 shares was credited to the stockholders equity account, Paid-in Capital from Treasury Stock. Although the corporation is better off by $9 per share, the corporation cannot report this “gain” on its income statement. Instead the $270 goes directly to stockholders’ equity in the paid-in capital section as shown here:

If the corporation sells any of its treasury stock for less than its cost, the cash received is debited to Cash, the cost of the shares sold is credited to Treasury Stock, and the difference (“loss”) is debited to Paid-in Capital from Treasury Stock (so long as the balance in that account will not become a debit balance). If the “loss” is larger than the credit balance, part of the “loss” is recorded in Paid-in Capital from Treasury Stock (up to the amount of the credit balance) and the remainder is debited to Retained Earnings. To illustrate this rule, let’s look at several transactions where treasury stock is sold for less than cost.

We will continue with our example from above. Recall that the cost of the corporation’s treasury stock is $20 per share. The corporation now sells 25 shares of treasury stock for $16 per share and receives cash of $400. As mentioned previously, the $4 “loss” per share ($16 proceeds minus the $20 cost) cannot appear on the income statement. Instead the “loss” goes directly to the account Paid-in Capital from Treasury Stock (if the account’s credit balance is greater than the “loss” amount). Since the $270 credit balance in Paid-in Capital from Treasury Stock is greater than the $100 debit, the entire $100 is debited to that account:

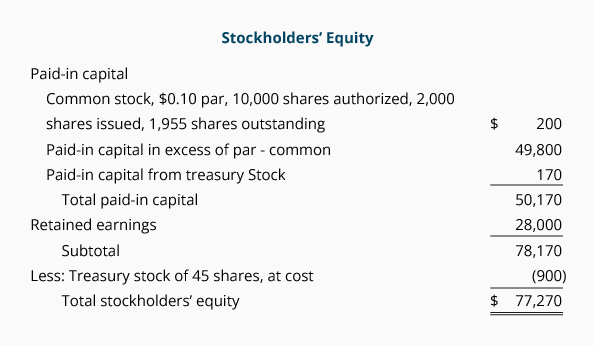

After the 25 shares of treasury stock are sold, the balance in Treasury Stock becomes a debit of $900 (45 shares at their cost of $20 per share). The Paid-in Capital from Treasury Stock now shows a credit balance of $170.

The stockholders’ equity section of the balance sheet will now report the following:

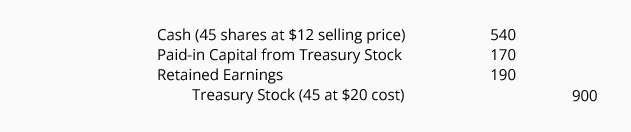

Now let’s illustrate what happens when the next sale of treasury stock results in a “loss” and it exceeds the credit balance in Paid-in Capital from Treasury Stock. Let’s assume that the remaining 45 shares of treasury stock are sold by the corporation for $12 per share and the proceeds total $540. Since the cost of those treasury shares was $900 (45 shares at a cost of $20 each) there will be a “loss” of $360. This $360 is too large to be absorbed by the $170 credit balance in Paid-in Capital from Treasury Stock. As a result, the first $170 of the “loss” goes to Paid-in Capital from Treasury Stock and the remaining $190 ($360 minus $170) is debited to Retained Earnings as shown in this journal entry:

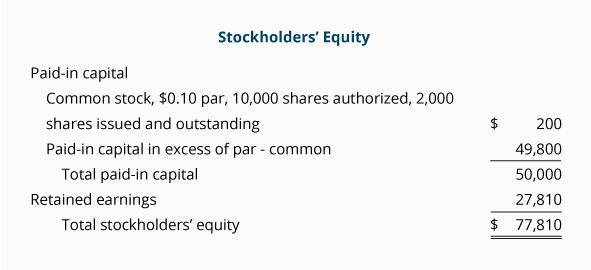

Again, no income statement account was involved with the sale of treasury stock, even though the shares were sold for less than their cost. The difference between the cost of the shares sold and their proceeds was debited to stockholders’ equity accounts. The debit was applied to Paid-in Capital from Treasury Stock for as much as that account’s credit balance. Any “loss” greater than the credit balance was debited to Retained Earnings. The stockholders’ equity section of the balance sheet now appears as follows:

Please let us know how we can improve this explanation

No Thanks

Close

Stock Splits and Stock Dividends

Stock splits

Assume that a board of directors feels it is useful if investors know they can buy 100 shares of the corporation’s stock for less than $5,000. In other words, they prefer to have the price of a share trading between $40 and $50 per share. If the market price of the stock rises to $80 per share, the board of directors can move the market price of the stock back into the range of $40 to $50 per share through a 2-for-1 stock split.

The 2-for-1 stock split will cause the quantity of shares outstanding to double and, in the process, cause the market price to drop from $80 to $40 per share. For example, if a corporation has 100,000 shares outstanding, a 2-for-1 stock split will result in 200,000 shares outstanding. Since the corporation’s assets, liabilities, and total stockholders’ equity are the same as before the stock split, doubling the number of shares should bring the market value per share down to approximately half of its pre-split value.

After a 2-for-1 stock split, an individual investor who had owned 1,000 shares might be elated at the prospect of suddenly being the owner of 2,000 shares. However, every stockholder’s number of shares has doubled—causing the value of each share to be worth approximately half of what it was before the split. If a corporation had 100,000 shares outstanding, a stockholder who owned 1,000 shares owned 1% of the corporation (1,000 ÷ 100,000). After a 2-for-1 stock split, the same stockholder still owns just 1% of the corporation (2,000 ÷ 200,000). Before the split, 1,000 shares at $80 each totaled $80,000; after the split, 2,000 shares at $40 each still totals $80,000.

A stock split will not change the general ledger account balances and therefore will not change the dollar amounts reported in the stockholders’ equity section of the balance sheet. (Although the number of shares will double, the total dollar amounts will not change.)

Although the 2-for-1 stock split is typical, directors may authorize other stock split ratios, such as a 3-for-2 stock split or a 4-for-1 stock split.

While the general ledger account balances do not change after a stock split, there is one change that should be noted: the par value per share decreases with a stock split. For example, if the par value was $1.00 per share and there were 100,000 shares outstanding, the total par value was $100,000. After a 2-for-1 split, the par value will be $0.50 per share and there are 200,000 shares outstanding with a total par value of $100,000. A memo entry is made to indicate that the split occurred and that the par value per share has changed from $1.00 per share to $0.50 per share.

Stock Dividends

A stock dividend does not involve cash. Rather, it is the distribution of more shares of the corporation’s stock. Perhaps a corporation does not want to part with its cash, but wants to give something to its stockholders. If the board of directors approves a 10% stock dividend, each stockholder will get an additional share of stock for each 10 shares held.

Since every stockholder will receive additional shares, and since the corporation is no better off after the stock dividend, the value of each share should decrease. In other words, since the corporation is the same before and after the stock dividend, the total market value of the corporation remains the same. Because there are 10% more shares outstanding, each share should drop in value.

With each stockholder receiving a percentage of the additional shares and the market value of each share decreasing in value, each stockholder should end up with the same total market value as before the stock dividend. (If this reminds you of a stock split, you are very perceptive. For example, a stockholder owning 100 shares would end up with 150 shares with either a 50% stock dividend or a 3-for-2 stock split. However, there will be a difference in the accounting.)

Even though the total amount of stockholders’ equity remains the same, a stock dividend requires a journal entry to transfer an amount from the retained earnings section to the paid-in capital section. The amount transferred depends on whether the stock dividend is (1) a small stock dividend, or (2) a large stock dividend.

Small stock dividend. A stock dividend is considered to be small if the new shares issued are less than 20-25% of the total number of shares outstanding prior to the stock dividend.

On the declaration date of a small stock dividend, a journal entry is made to transfer the market value of the shares being issued from retained earnings to the paid-in capital section of stockholders’ equity.

To illustrate, let’s assume a corporation has 2,000 shares of common stock outstanding when it declares a 5% stock dividend. This means that 100 (2,000 shares times 5%) new shares of stock will be issued to the existing stockholders. Assuming the stock has a par value of $0.10 per share and a market value of $12 per share on the declaration date, the following entry is made on the declaration date:

When the 100 shares are distributed to the stockholders, the following journal entry is made:

Large stock dividend. A stock dividend is considered to be large if the new shares being issued are more than 20-25% of the total number of shares outstanding prior to the stock dividend.

On the declaration date of a large stock dividend, a journal entry is made to transfer the par value of the shares being issued from retained earnings to the paid-in capital section of stockholders’ equity.

To illustrate, let’s assume a corporation has 2,000 shares of common stock outstanding when it declares a 50% stock dividend. This means that 1,000 new shares of stock will be issued to the existing stockholders. The stock has a par value of $0.10 per share and the stock has a market value of $12 per share on the declaration date. The following entry should be made on the declaration date:

When the 1,000 shares are distributed to the stockholders, the following journal entry is made:

Please let us know how we can improve this explanation

No Thanks

Close

Cash Dividends on Common Stock

Cash dividends (usually referred to as dividends) are a distribution of the corporation’s net income. Dividends are analogous to draws/withdrawals by the owner of a sole proprietorship. The draws and dividends are not expenses and will not appear on the income statements.

Corporations routinely need cash in order to replace inventory and other assets whose costs have increased or to expand the business. As a result, corporations rarely distribute all of their net income to stockholders. Young, growing corporations may pay no dividends at all.

Before a corporation can distribute cash to its stockholders, the corporation’s board of directors must declare a dividend. The date the board declares the dividend is known as the declaration date and it is on this date that the liability for the dividend is created.

Legally, corporations must have a credit balance in Retained Earnings in order to declare a dividend. Practically, a corporation must also have a cash balance large enough to pay the dividend and still meet upcoming needs, such as asset growth and payments on existing liabilities.

To illustrate, assume that on March 15 a corporation’s board of directors approves a motion to pay its regular quarterly dividend of $0.40 per share on May 1 to stockholders of record on April 15. The following entry is made on the declaration date of March 15 assuming that 2,000 shares of common stock are outstanding:

If the corporation wants to keep a separate general ledger record of the current year dividends, it could use a temporary, contra retained earnings account entitled Dividends Declared. At the end of the year, the balance in Dividends Declared will be closed to Retained Earnings. If such an account is used, the entry on the declaration date is:

It is important to note that there is no entry to record the liability for dividends until the board declares them. Also, there is no entry on the record date (April 15 in this case). The record date merely determines the names of the stockholders that will receive the dividends. Dividends are paid only on outstanding shares of stock; no dividends are paid on the treasury stock.

On May 1, when the dividends are paid, the following journal entry is recorded.

Please let us know how we can improve this explanation

No Thanks

Close

Preferred Stock

When it comes to dividends and liquidation, the owners of preferred stock have preferential treatment over the owners of common stock. In other words, preferred stockholders receive their dividends before the common stockholders receive theirs. If the corporation does not declare and pay the dividends to preferred stock, there cannot be a dividend on the common stock. In return for these preferences, the preferred stockholders usually give up the right to share in the corporation’s earnings that are in excess of their stated dividends.

To illustrate how preferred stock works, let’s assume a corporation has issued preferred stock with a stated annual dividend of $9 per year. The holders of these preferred shares must receive the $9 per share dividend each year before the common stockholders can receive a penny in dividends. But the preferred shareholders will get no more than the $9 dividend, even if the corporation’s net income increases a hundredfold. (Participating preferred stock is an exception and will be discussed later.) In times of inflation, owning preferred stock with a fixed dividend and no maturity or redemption date makes preferred shares less attractive than its name implies.

Par Value of Preferred Stock

The dividend on preferred stock is usually stated as a percentage of its par value. Hence, the par value of preferred stock has some economic significance. For example, if a corporation issues 9% preferred stock with a par value of $100, the preferred stockholder will receive a dividend of $9 (9% times $100) per share per year. If the corporation issues 10% preferred stock having a par value of $25, the stock will pay a dividend of $2.50 (10% times $25) per year. In each of these examples the par value is meaningful because it is a factor in determining the dividend amounts.

If the dividend percentage on the preferred stock is close to the rate demanded by the financial markets, the preferred stock will sell at a price that is close to its par value. In other words, a 9% preferred stock with a par value of $50 being issued or traded in a market demanding 9% would sell for $50. On the other hand, if the market demands 8.9% and the stock is a 9% preferred stock with a par value of $50, then the stock will sell for slightly more than $50 as investors see an advantage in these shares.

Issuing Preferred Stock

To comply with state regulations, the par value of preferred stock is recorded in its own paid-in capital account Preferred Stock. If the corporation receives more than the par amount, the amount greater than par will be recorded in another account such as Paid-in Capital in Excess of Par – Preferred Stock. For example, if one share of 9% preferred stock having a par value of $100 is sold for $101, the following entry will be made.

Features Offered in Preferred Stock

Corporations are able to offer a variety of features in their preferred stock, with the goal of making the stock more attractive to potential investors. All of the characteristics of each preferred stock issue are contained in a document called an indenture.

Nonparticipating vs. Participating

Generally, preferred stockholders receive the stated dividends and nothing more. If a preferred stock is described as 10% preferred stock with a par value of $100, the dividend per share will be $10 per year (whether the corporation’s earnings were $10 million or $10 billion). Preferred stock that earns no more than its stated dividend is the norm and it is known as nonparticipating preferred stock.

Occasionally a corporation issues participating preferred stock. Participating preferred stock allows for dividends greater than the stated dividend. Since this feature is unusual, it is prudent to assume that all preferred stock is nonparticipating unless it is clearly stated otherwise.

Cumulative vs. Noncumulative

If a preferred stock is designated as cumulative preferred stock, its holders must receive any dividends that had been omitted on the preferred stock in addition to its current year dividend, before common stockholders are paid any dividends. (A corporation might omit its dividends because it is suffering operating losses and has little cash available.) If a corporation omits a dividend on its cumulative preferred stock, the past, omitted dividends are said to be “in arrears” and must be disclosed in the notes to the financial statements.

If a preferred stock is noncumulative, any omitted dividends will not be in arrears. That is, the corporation does not have to pay any omitted dividends on noncumulative preferred stock before declaring dividends. However, the noncumulative preferred stock must be given its current year dividend before the common stock can receive a dividend.

Callable

If a corporation has 10% preferred stock outstanding and market rates decline to 8%, it makes sense that the corporation would like to eliminate the 10% preferred stock and replace it with 8% preferred stock. On the other hand, the holders of the 10% preferred stock bought it with the assumption of getting the 10% indefinitely. Anticipating such a situation, the preferred stock will usually have a stipulation that the corporation can “call in” (purchase) the preferred stock at a certain price. This price is referred to as the call price and it might be 110% of the par amount (par plus one year’s dividend).

Convertible

Occasionally, a corporation’s preferred stock indicates that it can be exchanged for a stated number of shares of the corporation’s common stock. If that is the case, the preferred stock is said to be convertible preferred. For example, a corporation might issue shares of 8% $100 Par convertible preferred stock which can be converted at any time into three shares of common stock. The preferred stockholder receives the usual preferences including an $8 per year per share dividend, but in addition has the potential to share in the success of the corporation. If the common stock is selling for $20 per share, the preferred stock is more valuable because of its dividend. However, if the company’s success increases the value of the common stock to $40 per share, the convertibility feature makes the preferred stock worth $120 per share. (The preferred stock can be exchanged for 3 shares of common stock worth $40 each). The preferred stockholder could sell the preferred stock at the market price of $120 per share, or, could have the corporation issue three shares of common stock in exchange for each share of its preferred stock.

Combination of Features

The strength of the corporation, coupled with the status of key financial markets, all influence the features that are offered with a given preferred stock. If a corporation is not attractive to potential investors, the preferred stock might need both the cumulative and the fully participating features in order to attract investors. On the other hand, a successful blue chip corporation might easily sell its preferred stock as noncumulative and nonparticipating. If a corporation wants to conserve its cash, it may offer convertible preferred stock to have a lower dividend rate.

Please let us know how we can improve this explanation

No Thanks

Close

Entries to the Retained Earnings Account

Net Income or Loss

The closing entries of a corporation include closing the income summary account to the Retained Earnings account. If the corporation was profitable in the accounting period, the Retained Earnings account will be credited; if the corporation suffered a net loss, Retained Earnings will be debited.

Dividends

When dividends are declared by a corporation’s board of directors, a journal entry is made on the declaration date to debit Retained Earnings and credit the current liability Dividends Payable. As stated earlier, it is the declaration of cash dividends that reduces Retained Earnings.

Appropriations or Restrictions of Retained Earnings

A board of directors can vote to appropriate, or restrict, some of the corporation’s retained earnings. An appropriation (or restriction) will result in two retained earnings accounts instead of one:

The subdividing of retained earnings is a way of disclosing the appropriation on the face of the balance sheet. (An appropriation might occur when a corporation anticipates expanding its factory and wants to conserve its cash.) By displaying the appropriated retained earnings account on the balance sheet, the corporation is communicating a potential limitation on future dividends since dividends can be declared only if there is a credit balance in Retained Earnings.

To record an appropriation of retained earnings, the account Retained Earnings is debited (causing this account to decrease), and Appropriated Retained Earnings is credited (causing this account to increase).

An alternative to having Appropriated Retained Earnings appearing on the balance sheet is to disclose the specific situation in the notes to the financial statements.

Prior Period Adjustments

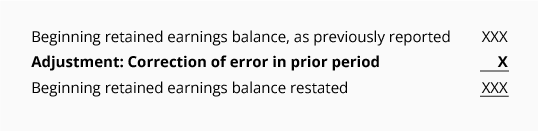

If an error of a significant amount is discovered on a previously issued income statement (as opposed to a change in an estimated amount), a corporation must restate its current year’s beginning retained earnings balance. If the error understated the corporation’s net income, the beginning retained earnings balance must be increased (a credit to Retained Earnings). If the error had overstated the corporation’s net income, the current year’s beginning retained earnings balance must be decreased (a debit to Retained Earnings). The adjustment to the beginning balance is shown on the current retained earnings statement as follows:

The book value of an entire corporation is the total of the stockholders’ equity section as shown on the balance sheet. In other words, the book value of a corporation is the balance sheet assets minus the liabilities.

Since the balance sheet amounts reflect the cost and matching principles, a corporation’s book value is not the same amount as its market value. For example, the most successful brand names and logos of a consumer products company may have been developed in-house. Since they were not purchased, their high market values are not included in the corporation’s assets. Other long-term assets may have appreciated in value while the accountant was depreciating them. Therefore, they may appear on the balance sheet at a small fraction of their fair market value.

As these examples suggest, a corporation’s market value may be far greater than its book value. In contrast, a corporation that has recently purchased many assets, but is unable to operate profitably, may have a market value that is less than its book value. Although we can calculate a corporation’s book value from its stockholders’ equity, we cannot calculate a corporation’s market value from its balance sheet. We must look to appraisers, financial analysts, and/or the stock market to help determine an approximation of a corporation’s fair market value.

Book Value per Share of Common Stock

Let’s use the following stockholders’ equity information to calculate (1) the book value of a corporation, and (2) the book value per share of common stock:

The book value of a corporation having only common stock is equal to the total amount of stockholders equity: $78,000.

If common stock is the only capital stock issued by the corporation, the book value per share of common stock is $39. It is calculated as follows:

Total stockholders’ equity of $78,000 divided by the 2,000 shares of common stock that are outstanding: $78,000/2,000 shares = $39.00 per share of common stock

Book Value per Share of Preferred Stock

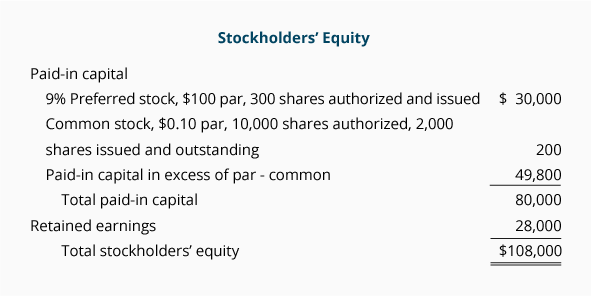

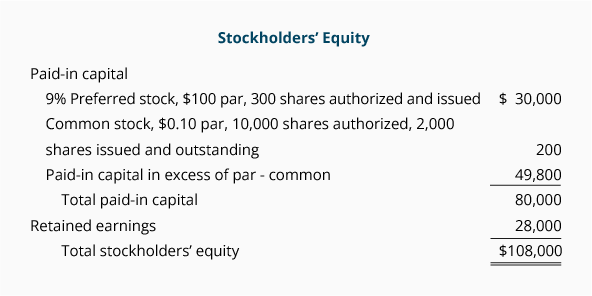

If a corporation has both common stock and preferred stock, the corporation’s stockholders’ equity (the corporation’s book value) must be divided between the preferred stock and the common stock. To arrive at the total book value of the common stock, we first compute the total book value of the preferred stock, and then subtract that amount from the total stockholders’ equity.

The book value of one share of cumulative preferred stock is its call price plus any dividends in arrears. If a 10% cumulative preferred stock having a par value of $100 has a call price of $110, and the corporation has two years of omitted dividends, the book value per share of this preferred stock is $130. If the corporation has 9% noncumulative preferred stock having a par value of $50, a call price of $54, and the corporation has three years of omitted dividends, its book value is $54 per share (call price of $54 and no dividends in arrears since the stock is noncumulative).

The total book value of the preferred stock is the book value per share times the total number of preferred shares outstanding. If the book value per share of preferred stock is $130 and there are 1,000 shares of the preferred stock outstanding, then the total book value of the preferred stock is $130,000.

Let’s compute the total book value of preferred stock by using the following information:

Assume that the call price of the preferred stock is $109. Also assume it is cumulative preferred and three years of omitted dividends are owed.

The book value per share of the preferred stock equals the call price of $109 plus three years of omitted dividends at $9 each, or $136 ($109 + $27 = $136).

The total book value for all of the preferred stock equals the book value per share of preferred stock times the number of shares of preferred stock outstanding, or $40,800 ($136 X 300 = $40,800).

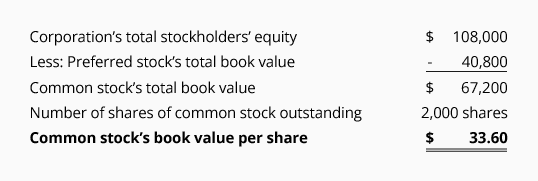

Common Stock’s Book Value

When a corporation has both common stock and preferred stock, the book value of the preferred stock is subtracted from the corporation’s total stockholders’ equity to arrive at the total book value of the common stock. Using our previous amounts, the common stock’s book value per share is calculated as follows:

Please let us know how we can improve this explanation

No Thanks

Close

Statement of Stockholders’ Equity

Corporations also include a statement of stockholders’ equity along with its other financial statements. A common format of the statement of stockholders’ equity is shown here:

To see a more comprehensive example, we suggest an Internet search for publicly-traded corporation’s Form 10-K.

Earnings Per Share

Earnings per share is not part of stockholders’ equity. Nonetheless, we are including an introduction to the topic here because the calculation for earnings per share involves the stock of a corporation.

Earnings per share must appear on the face of the income statement if the corporation’s stock is publicly traded. The earnings per share calculation is the after-tax net income (earnings) available for the common stockholders divided by the weighted-average number of common shares outstanding during that period.

Earnings Available for Common Stock

Let’s assume that a corporation has the following stockholders’ equity at December 31:

Additional information:

The corporation’s accounting year is the calendar year.

The corporation’s net income after income tax is $10,000.

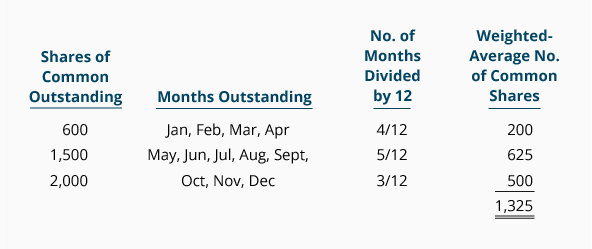

The number of shares of common stock outstanding was 600 shares for the first four months of the year. On May 1, the corporation issued an additional 900 shares. On October 1, an additional 500 shares were issued.

The shares of preferred stock were outstanding for the entire year.

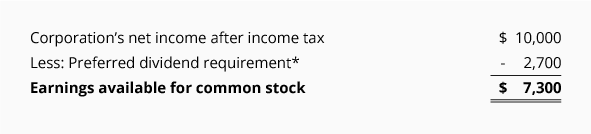

The earnings (net income after income tax) available for the common stockholders is:

*The preferred dividend requirement is the annual dividend of $9 per share (9% times $100 par value) times the 300 shares of preferred stock outstanding.

Weighted-Average Number of Shares of Common Stock

Since the earnings occurred throughout the year, we need to divide the amount by the number of shares that were outstanding during that time. During the first four months only 600 shares were outstanding, during the next five months 1,500 shares were outstanding, and for the final three months of the year 2,000 shares of common stock were outstanding. This situation requires that we come up with the weighted-average number of shares of common stock for the year as calculated here:

As the calculation shows, the weighted-average number of shares of common stock for the year was 1,325.

Earnings per Share of Common Stock

After deducting the preferred stockholders’ required dividend, there was $7,300 ($10,000 minus $2,700) of earnings available for the common stockholders. The $7,300 was earned throughout the year, so we need to divide that amount by the weighted-average number of shares of common stock outstanding during the same period:

The earnings per share (EPS) of common stock = earnings available for common stock divided by the weighted-average number of common shares outstanding:

Please let us know how we can improve this explanation

No Thanks

Close

Other

Stock Issued for Other Than Cash

If a corporation has a limited amount of cash, but needs an asset or some services, the corporation might issue some new shares of stock in exchange for the items. When shares of stock are issued for noncash items, the items and the stock must be recorded on the books at the fair market value at the time of the exchange. Since both the stock given up and the asset or services received may have market values, accountants record the fair market value of the one that is more clearly determinable (more objective and verifiable).

For instance, if a corporation exchanges 1,000 of its publicly-traded shares of common stock for 40 acres of land, the fair market value of the stock is likely to be more clear and objective. (The stock might trade daily while similar parcels of land in the area may sell once every few years.) In other situations, the common stock might rarely trade while the value of a service received is well-established.

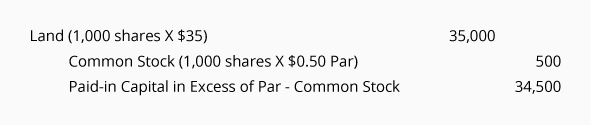

To illustrate, let’s assume that 1,000 shares of common stock are exchanged for a parcel of land. The stock is publicly traded and recent trades have been at $35 per share. The par value is $0.50 per share. The land’s fair market value is not as clear since there has not been a comparable sale during the past four years.

The entry made to record the exchange will record the land at the fair market value of the common stock, since the stock’s fair market value is more clear and objective than someone’s estimate of the current value of the land:

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Stockholders’ Equity materials (see the full outline below).

We also recommend joining PRO Plus to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.

Please let us know how we can improve this explanation

No Thanks

Close

One of the main financial statements. The balance sheet reports the assets, liabilities, and owner’s (stockholders’) equity at a specific point in time, such as December 31. The balance sheet is also referred to as the Statement of Financial Position.

Assets = Liabilities + Owner’s Equity. For a corporation the equation is Assets = Liabilities + Stockholders’ Equity. For a nonprofit organization the accounting equation is Assets = Liabilities + Net Assets. Because of double-entry accounting this equation should be in balance at all times. The accounting equation is expressed in the financial statement known as the balance sheet.

A sole proprietorship is a simple form of business where there is one owner. Legally the owner and the sole proprietorship are the same. However, for accounting purposes the economic entity assumption results in the sole proprietorship’s business transactions being accounted for separately from the owner’s personal transactions.

Also referred to as a shareholder. The owner of shares of stock in a corporation. Every corporation has common stock and those owners are known as common stockholders. Some corporations also issued preferred stock and those corporations will have both common stockholders and preferred stockholders.

A distribution of part of a corporation’s past profits to its stockholders. A dividend is not an expense on the corporation’s income statement.

The book value of an asset is the amount of cost in its asset account less the accumulated depreciation applicable to the asset. The book value of an asset is also referred to as the carrying value of the asset.

The book value of a company is the amount of owner’s or stockholders’ equity. The book value of bonds payable is the combination of the accounts Bonds Payable and Discount on Bonds Payable or the combination of Bonds Payable and Premium on Bonds Payable.

A revenue account that reports the sales of merchandise. Sales are reported in the accounting period in which title to the merchandise was transferred from the seller to the buyer.

Obligations of a company or organization. Amounts owed to lenders and suppliers. Liabilities often have the word “payable” in the account title. Liabilities also include amounts received in advance for a future sale or for a future service to be performed.

Things that are resources owned by a company and which have future economic value that can be measured and can be expressed in dollars. Examples include cash, investments, accounts receivable, inventory, supplies, land, buildings, equipment, and vehicles.

Assets are reported on the balance sheet usually at cost or lower. Assets are also part of the accounting equation: Assets = Liabilities + Owner’s (Stockholders’) Equity.

Some valuable items that cannot be measured and expressed in dollars include the company’s outstanding reputation, its customer base, the value of successful consumer brands, and its management team. As a result these items are not reported among the assets appearing on the balance sheet.

Someone who has granted credit. If a bank lends a company money, the bank is a creditor. If a supplier sold merchandise to a company on credit, the supplier is a creditor.

The term that refers to the stock of a corporation which is traded on the stock exchanges (as opposed to stock that is privately held among a few individuals).

The bank account on which checks are written or drawn. A bank refers to checking accounts as demand deposits.

This is the bottom line of the income statement. It is the mathematical result of revenues and gains minus the cost of goods sold and all expenses and losses (including income tax expense if the company is a regular corporation) provided the result is a positive amount. If the net amount is a negative amount, it is referred to as a net loss.

Individuals elected by the common stockholders of a corporation to represent the stockholders and to establish the policies of the corporation. The board of directors appoints the officers of the corporation and declares dividends for the common and preferred stock.

Officers of a corporation are appointed by the board of directors to execute the policies that have been established by the board of directors. The officers include the chief executive officer (CEO), the chief operations officer (COO), chief financial officer (CFO), vice presidents, treasurer, secretary, and controller.

The chief accounting officer of a company. This person would head up the accounting department.

The type of stock that is present at every corporation. (Some corporations have preferred stock in addition to their common stock.) Shares of common stock provide evidence of ownership in a corporation. Holders of common stock elect the corporation’s directors and share in the distribution of profits of the company via dividends. If the corporation were to liquidate, the secured lenders would be paid first, followed by unsecured lenders, preferred stockholders (if any), and lastly the common stockholders.

A class of corporation stock that provides for preferential treatment over the holders of common stock in the case of liquidation and dividends. For example, the preferred stockholders will be paid dividends before the common stockholders receive dividends. In exchange for the preferential treatment of dividends, preferred shareholders usually will not share in the corporation’s increasing earnings and instead receive only their fixed dividend.

Paper evidence of ownership in a corporation. The certificate would indicate the type of stock (common, preferred), any restrictions pertaining to the sale of the stock, the number of shares, the par value, etc. Today, the larger corporations with many shareholders are likely to use electronic records instead of issuing the paper stock certificates.

A heading that includes common stock and preferred stock.

A stated legal amount often appearing on preferred stock, bonds, and some common stock.

That part of the accounting system which contains the balance sheet and income statement accounts used for recording transactions.

A corporation’s own stock that has been repurchased from stockholders. Also a stockholders’ equity account that usually reports the cost of the stock that has been repurchased.

The standards, rules, guidelines, and industry-specific requirements for financial reporting.

A record in the general ledger that is used to collect and store similar information. For example, a company will have a Cash account in which every transaction involving cash is recorded. A company selling merchandise on credit will record these sales in a Sales account and in an Accounts Receivable account.

Generally speaking, retained earnings is a stockholders’ equity account that reports the net income of a corporation from its inception until the balance sheet date less the dividends declared from its inception to the date of the balance sheet.

Accumulated other comprehensive income is a separate line within stockholders’ equity that reports the corporation’s cumulative income that has not been reported as part of net income on the corporation’s income statements. The items that would be included in this line involve the income or loss involving foreign currency transactions, hedges, and pension liabilities.

A heading that includes common stock and preferred stock.

The amount that would be agreed upon by two independent persons. The amount to be received in the ordinary course of business in an arm’s length transaction.

The entry made in a journal. It will contain the date, the account name and amount to be debited, and the account name and amount to be credited. Each journal entry must have the dollars of debits equal to the dollars of credits.

A balance on the right side (credit side) of an account in the general ledger.

A balance on the left side of an account in the general ledger. Typically expenses, losses, and assets have debit balances.

One of the main financial statements (along with the statement of comprehensive income, balance sheet, statement of cash flows, and statement of stockholders’ equity). The income statement is also referred to as the profit and loss statement, P&L, statement of income, and the statement of operations. The income statement reports the revenues, gains, expenses, losses, net income and other totals for the period of time shown in the heading of the statement. If a company’s stock is publicly traded, earnings per share must appear on the face of the income statement.

The statement of comprehensive income covers the same period of time as the income statement, and consists of two major sections:

Net income (taken from the income statement)

Other comprehensive income (adjustments involving foreign currency translation, hedging, and postretirement benefits)

The sum of these two amounts is known as comprehensive income.

The amount of other comprehensive income is added/subtracted from the balance in the stockholders’ equity account Accumulated Other Comprehensive Income.

This financial statistic is the net income of a corporation after income tax (less any preferred dividends) divided by the weighted average number of shares of common stock outstanding during the same period of time.

An account in the general ledger, such as Cash, Accounts Payable, Sales, Advertising Expense, etc.

The accounting term that means an entry will be made on the left side of an account.

A revenue, expense, gain, or loss account.

Gains result from the sale of an asset (other than inventory). A gain is measured by the proceeds from the sale minus the amount shown on the company’s books. Since the gain is outside of the main activity of a business, it is reported as a nonoperating or other revenue on the company’s income statement.

A stock split, such as a 2-for-1, means that every stockholder will have twice as many shares as was held previously. Accordingly, the market price per share after the split should be one-half of the market price existing prior to the stock split. The main reason for a stock split is to reduce the market price per share of stock.

An entry without debit or credit amounts. For example, assume that a corporation has 100,000 shares of $0.50 par value common stock before a 2-for-1 stock split. At the time of the split a memo entry would be entered in the records stating that after the 2-for-1 stock split, the corporation has 200,000 shares of $0.25 par value common stock outstanding. No dollar amounts would be posted to the accounts in the general ledger.

Costs that are matched with revenues on the income statement. For example, Cost of Goods Sold is an expense caused by Sales. Insurance Expense, Wages Expense, Advertising Expense, Interest Expense are expenses matched with the period of time in the heading of the income statement. Under the accrual basis of accounting, the matching is NOT based on the date that the expenses are paid.

Expenses associated with the main activity of the business are referred to as operating expenses. Expenses associated with a peripheral activity are nonoperating expenses or other expenses. For example, a retailer’s interest expense is a nonoperating expense. A bank’s interest expense is an operating expense.

Generally, expenses are debited to a specific expense account and the normal balance of an expense account is a debit balance. When an expense account is debited, the account credited might be Cash (if cash was paid at the time of the expense), Accounts Payable (if cash will be paid after the expense is recorded), or Prepaid Expense (if cash was paid before the expense was recorded.)

A current asset whose ending balance should report the cost of a merchandiser’s products awaiting to be sold. The inventory of a manufacturer should report the cost of its raw materials, work-in-process, and finished goods. The cost of inventory should include all costs necessary to acquire the items and to get them ready for sale.

When inventory items are acquired or produced at varying costs, the company will need to make an assumption on how to flow the changing costs. See cost flow assumption.

If the net realizable value of the inventory is less than the actual cost of the inventory, it is often necessary to reduce the inventory amount.

The date that determines which stockholders are entitled to receive a corporation’s declared dividend. No accounting entry is made on this date.

The issued shares of common stock minus the shares of treasury stock. The weighted average of the outstanding shares is used to compute the earnings per share.

A corporation’s own stock that has been repurchased from stockholders. Also a stockholders’ equity account that usually reports the cost of the stock that has been repurchased.

A document that discloses important information on bonds or preferred stock. Included in the indenture would be the call price, the actions that can occur if the company fails to pay the interest or dividend, etc.

This term is associated with preferred stock that does not allow its holders to receive more than its stated dividend. The nonparticipating feature is typical in preferred stock. To learn more about preferred stock, see Explanation of Stockholders’ Equity.

Preferred stock where the dividend could be more than the original, stated dividend.

This preferred stock feature assures the owner that any omitted dividends on this stock will be made up before the common stockholders will receive a dividend. Any omitted dividends on cumulative preferred stock are referred to as dividends in arrears and must be disclosed in the notes to the financial statements.

Usually financial statements refer to the balance sheet, income statement, statement of comprehensive income, statement of cash flows, and statement of stockholders’ equity.

The balance sheet reports information as of a date (a point in time). The income statement, statement of cash flows, statement of comprehensive income, and the statement of stockholders’ equity report information for a period of time (or time interval) such as a year, quarter, or month.

Preferred stock where past, omitted dividends do not have to be paid before a dividend can be paid to common stockholders. In the case of noncumulative preferred stock, only its current year dividend needs to be paid in order for a corporation to pay a dividend to its common stockholders.

A term meaning behind, such as dividends in arrears, or something occurring at the end of a period, such as the recurring payment in an annuity in arrears.

The amount at which the holder of preferred stock or bonds must sell the stock or bonds back to the issuing corporation. The call price is disclosed in the indenture. The call price might be the face or par amount plus one year’s interest or dividend.

Preferred stock that can be exchanged by the holder for a specified number of shares of common stock of the same company.

A temporary account to which the income statement accounts are closed. This account is then closed to the owner’s capital account or a corporation’s retained earnings account. This and other summary accounts can be thought of as a clearing account.

A current liability account that reports the amounts of cash dividends that have been declared by the board of directors but not yet distributed to the stockholders.

A stockholders’ equity account that generally reports the net income of a corporation from its inception until the balance sheet date less the dividends declared from its inception to the date of the balance sheet.

The regular retained earnings. Retained earnings that have not been restricted.

A second retained earnings account that reports the amount that a company has transferred from the unappropriated or regular retained earnings account.

The book value of an asset is the amount of cost in its asset account less the accumulated depreciation applicable to the asset. The book value of a company is the amount of owner’s or stockholders’ equity. The book value of bonds payable is the combination of the accounts Bonds Payable and Discount on Bonds Payable or the combination of Bonds Payable and Premium on Bonds Payable.

Generally a long term liability account containing the face amount, par amount, or maturity amount of the bonds issued by a company that are outstanding as of the balance sheet date.

Past omitted dividends on cumulative preferred stock. Generally these omitted dividends were not declared and, therefore, do not appear on the corporation’s balance sheet as a liability. However, they must be disclosed in the notes to the balance sheet.

This preferred stock feature assures the owner that any omitted dividends on this stock will be made up before the common stockholders will receive a dividend. Any omitted dividends on cumulative preferred stock are referred to as dividends in arrears and must be disclosed in the notes to the financial statements.

For the past 52 years, Harold Averkamp (CPA, MBA) has

worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.