Introduction

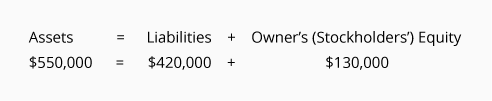

The basic accounting equation is:

The equation remains in balance thanks to the double-entry accounting (or bookkeeping) system.

The double-entry system requires a company’s transactions to be entered/recorded in two (or more) general ledger accounts. One account will have the amount entered on the left-side (a debit entry), while another account will have the amount entered on the right-side (a credit entry). As a result, the total amount of debits in the accounts will be equal to the total amount of credits in the accounts. (This can be verified with a trial balance.) In addition, the total of the asset account balances will be equal to the total of the liability account balances plus the total of the equity account balances. This will be evidenced by the accounting equation and the company’s balance sheet.

The accounting equation amounts are computed using the balances in the following permanent/balance sheet accounts:

-

Asset accounts. In the general ledger, the asset accounts normally* have their balances on the left side (debit balances). In the accounting equation, the total amount in the asset accounts is shown on the left side. A few examples are Cash, Accounts Receivable, and Inventory.

-

Liability accounts. In the general ledger, the liability accounts normally* have their balances on the right side (credit balances). In the accounting equation, the total amount in the liability accounts is shown on the right side. Three examples are Notes Payable, Accounts Payable, and Interest Payable.

-

Owner’s (stockholders’) equity accounts. In the general ledger, the equity accounts normally* have their balances on the right side (credit balances). In the accounting equation, the total amount in the equity accounts is shown on the right side. Examples include a sole proprietor’s Capital account and a corporation’s Common Stock and Retained Earnings accounts.

*A few accounts, such as Allowance for Doubtful Accounts, Accumulated Depreciation, Owner’s Draws, are contra accounts that will have opposite balances.

The accounting equation provides a snapshot of the total amount of a company’s recorded assets (resources owned), its total amount of recorded liabilities (amounts owed), and the owner’s equity (the remainder or residual).

To illustrate, assume that a company’s accounting equation shows the following:

You might think of the liabilities and owner’s equity as claims against the company’s assets in this order: secured liabilities, unsecured liabilities, residual claims of owners. You could also think of the liabilities and the owner’s equity as the source of the company’s assets. Of the $550,000 of assets, the creditors provided $420,000 and the owners provided $130,000.

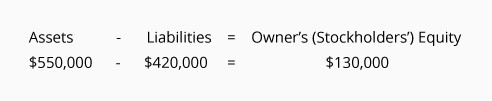

Using a little algebra, the accounting equation can be restated:

How Revenues and Expenses Fit In

It is easy to see that an additional investment by the owner will directly increase the owner’s equity. Similarly, a withdrawal of money by the owner for personal use will decrease the amount of owner’s equity.

However, owner’s equity also changes when the company earns revenues and/or it incurs expenses:

-

Revenues (and gains) cause the owner’s equity to increase. (Recall that the owner’s equity accounts normally have credit balances and will increase with a credit entry.) So, while owner’s equity increases when the company earns revenues, the revenue transaction will be recorded in the general ledger with a credit in a revenue account. (The debit is often recorded in the asset account Cash or Accounts Receivable.)

[Later, the credit balances in the revenue accounts will be moved to an owner’s equity account thereby increasing the equity account’s credit balance.]

-

Expenses (and losses) cause the owner’s equity to decrease. While owner’s equity decreases when the company incurs an expense, the expense transaction will be first recorded in the general ledger with a debit in an expense account. (The credit might be to Cash or Accounts Payable, or another account.)

[Later, the debit balances in the expense accounts will be moved to an owner’s equity account thereby decreasing the equity account’s credit balance.]

To illustrate, assume a company earned $500 in consulting fees and is paid immediately. As a result:

-

The company’s accounting equation will show a $500 increase in assets, and a $500 increase in owner’s equity.

-

However, the transaction is recorded in the general ledger with a debit of $500 to the Cash account, and a credit of $500 to the temporary account Consulting Revenue. (Later, the credit balance in Consulting Revenue will be transferred with a credit to an owner’s equity account.)

Some Transactions Will Involve Two Asset Accounts

You should be aware that some transactions will cause one asset to increase and another asset to decrease. In those situations, the total amounts in the accounting equation will not change. Here are two examples:

-

A company pays $5,000 for new office equipment. Cash decreased; Office Equipment increased.

-

A company collects a $2,000 account receivable that was recorded when the sale occurred in the previous month. Cash increased; Accounts Receivable decreased.

We will look at 8 transactions at a sole proprietorship and show the following:

- The effect on the company’s accounting equation

- How they are recorded in the company’s accounts

- The resulting balance sheet

- When appropriate, an income statement

- A schedule of the changes in the owner’s equity

- How to compute a company’s net income from incomplete information

That will be followed by looking at similar transactions at a corporation.

Lastly, we will briefly examine the expanded accounting equation.

Accounting Equation for a Sole Proprietorship: Transactions 1-2

When a company records a business transaction, it is not recorded in the accounting equation, per se. Rather, transactions are recorded into specific accounts contained in the company’s general ledger. The accounts are designated as an asset, liability, owner’s equity, revenue, expense, gain, or loss account. The amounts in the general ledger accounts will be used to prepare the balance sheets and income statements.

In our transactions, we will use the following accounts:

Our examples assume that the accrual basis of accounting is being used.

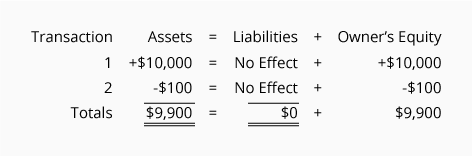

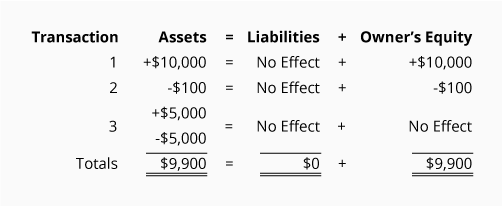

Sole Proprietorship Transaction #1.

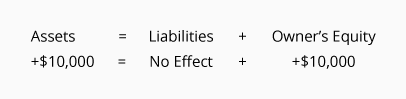

Assume that J. Ott forms a sole proprietorship called Accounting Software Co. (ASC). On December 1, 2025, J. Ott invests personal funds of $10,000 to start ASC. The effect of this transaction on ASC’s accounting equation is:

As you can see, ASC’s assets increase by $10,000 and so does ASC’s owner’s equity. As a result, the accounting equation is in balance.

You can interpret the amounts in the accounting equation to mean that ASC has assets of $10,000 and the source of those assets was the owner, J. Ott. Alternatively, you can view the accounting equation to mean that ASC has assets of $10,000 and there are no claims by creditors (liabilities) against the assets. As a result, the owner has a residual claim for the remainder of $10,000.

This transaction is recorded in the asset account Cash and the owner’s equity account J. Ott, Capital. The general journal entry to record the transaction is:

After the journal entry is recorded in the accounts, a balance sheet will show ASC’s financial position at the end of December 1, 2025 as follows:

Since ASC has not yet earned any revenues nor incurred any expenses, there are no amounts to be reported on an income statement.

Sole Proprietorship Transaction #2.

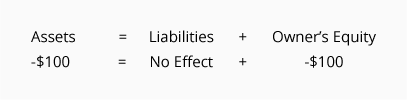

On December 2, 2025, J. Ott withdraws $100 of cash from the business for his personal use. The effect of this transaction on ASC’s accounting equation is:

The accounting equation remains in balance since ASC’s assets have been reduced by $100 and so has the owner’s equity.

This transaction is recorded in the asset account Cash and the owner’s equity account J. Ott, Drawing. The transaction in a general journal entry format is:

Since the transactions of December 1 and December 2 were in balance, the sum of both transactions should also be in balance:

The totals indicate that ASC has assets of $9,900 and the source of those assets is the owner of the company. You can also conclude that the company has assets or resources of $9,900 and the only claim against those resources is the owner’s claim.

The December 2 balance sheet will communicate the company’s financial position as of midnight on December 2:

Withdrawals of company assets by the owner for the owner’s personal use are known as “draws.” Since draws are not expenses, there is no transaction involving the company’s income statement for the two-day period of December 1 through December 2.

Accounting Equation for a Sole Proprietorship: Transactions 3-4

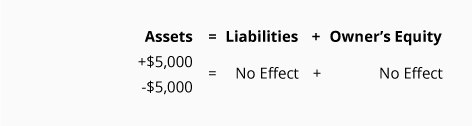

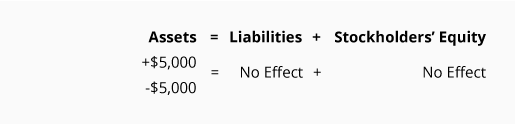

Sole Proprietorship Transaction #3.

On December 3, 2025, Accounting Software Co. spends $5,000 of cash to purchase computer equipment for use in the business. The effect of this transaction on the accounting equation is:

The accounting equation reflects that one asset increased and another asset decreased. Since the amount of the increase is the same as the amount of the decrease, the accounting equation remains in balance.

This transaction is recorded in the asset accounts Equipment and Cash. The Equipment account increases by $5,000, and the Cash account decreases by $5,000. The journal entry for this transactions is:

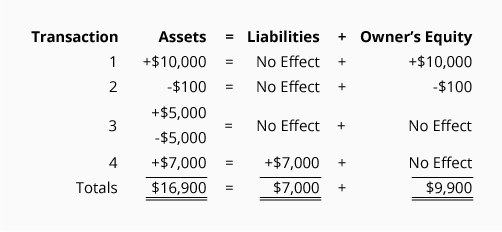

The combined effect of the first three transactions is shown here:

The totals tell us that the company has assets of $9,900 and the source of those assets is the owner of the company. It also tells us that the company has assets of $9,900 and the only claim against those assets is the owner’s claim.

The balance sheet dated December 3, 2025, reflects ASC’s financial position as of midnight on December 3:

The purchase of equipment is not an immediate expense. It will become part of depreciation expense only after it is placed into service. We will assume that as of December 3 the equipment has not been placed into service, therefore, there is no expense or revenue to be reported on an income statement for the period of December 1 through December 3.

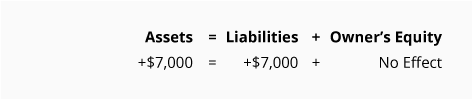

Sole Proprietorship Transaction #4.

On December 4, 2025, ASC obtains $7,000 by borrowing money from its bank. The effect of this transaction on the accounting equation is:

As you can see, ASC’s assets increased and ASC’s liabilities increased by $7,000.

This transaction is recorded in the asset account Cash and the liability account Notes Payable as shown in this accounting entry:

The combined effect on the accounting equation from the first four transactions is shown here:

The totals indicate that the transactions through December 4 result in assets of $16,900. There are two sources for those assets—the creditors provided $7,000 of assets, and the owner of the company provided $9,900. You can also interpret the accounting equation to say that the company has assets of $16,900 and the lenders have a claim of $7,000 and the owner has a residual claim for the remainder.

The balance sheet dated December 4 will report ASC’s financial position as of the final moment on December 4:

The proceeds of the bank loan are not considered to be revenue since ASC did not earn the money by providing services, investing, etc. As a result, there is no income statement effect from this transaction. For the accounting period of the four days ended December 4, there is no revenue or expense to be reported on the income statement.

Accounting Equation for a Sole Proprietorship: Transactions 5-6

Sole Proprietorship Transaction #5.

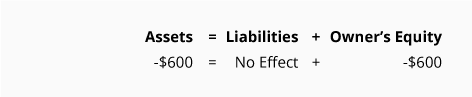

On December 5, 2025, Accounting Software Co. pays $600 for ads that were run in recent days. The effect of this advertising transaction on the accounting equation is:

Since ASC is paying $600, its assets decrease. The second effect is a $600 decrease in owner’s equity, because the transaction involves an expense. (An expense is a cost that is used up or its future economic value cannot be measured.)

Although owner’s equity decreases with a company expense, the transaction is not recorded directly into the owner’s capital account at this time. Instead, the amount is initially recorded in the expense account Advertising Expense and in the asset account Cash.

The general journal entry to record the transaction is:

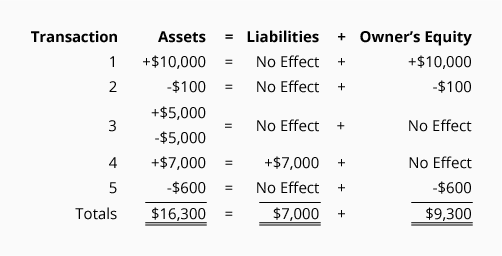

The combined effect of the first five transactions is shown here:

The totals now indicate that Accounting Software Co. has assets of $16,300. The creditors provided $7,000 and the owner of the company provided $9,300. Viewed another way, the company has assets of $16,300 with the creditors having a claim of $7,000 and the owner having a residual claim of $9,300.

The balance sheet as of midnight on December 5 is:

**The income statement (which reports the company’s revenues, expenses, gains, and losses during a specified time interval) is a link between balance sheets. It provides the results of operations—an important part of the change in owner’s equity.

Since this transaction involves an expense, it will be reported on ASC’s income statement. The company’s income statement for the first five days of December is:

Sole Proprietorship Transaction #6.

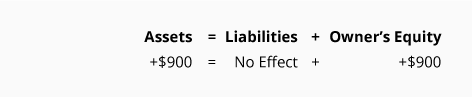

On December 6, 2025, ASC performed consulting services for its clients. The clients were billed for the agreed upon amount of $900. The amounts are to be paid within 30 days. The effect on ASC’s accounting equation is:

Since ASC has completed the services, it has earned revenues and it has the right to receive $900 from the clients. This right increases the asset known as accounts receivable. The earning of revenues causes owner’s equity to increase.

Although revenues cause owner’s equity to increase, the revenue transaction is not recorded directly into the owner’s capital account. Rather, the amount earned is recorded in the revenue account Service Revenues. At some point, the amount in the revenue accounts will be transferred to the owner’s capital account.

The general journal entry to record Transaction #6 is:

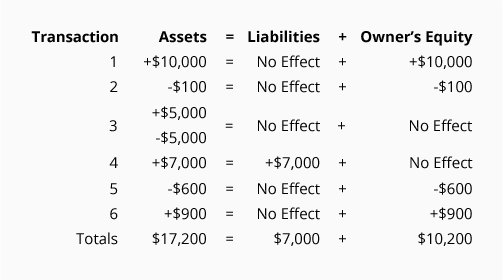

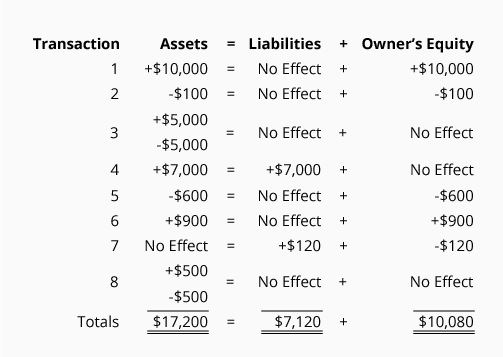

The following is a recap of the first six transactions:

The totals tell us that as of midnight on December 6, the company had assets of $17,200. It also indicates the creditors provided $7,000 and the owner of the company provided $10,200. The totals also reveal that the company had assets of $17,200 and the creditors had a claim of $7,000. The owner had a residual claim for the remaining $10,200.

The balance sheet as of midnight on December 6 is presented here:

**The income statement (which reports the company’s revenues, expenses, gains, and losses during a specified time interval) is a link between balance sheets. It provides the results of operations—an important part of the change in owner’s equity.

The Income Statement for Accounting Software Co. for the six days ended December 6 is:

Accounting Equation for a Sole Proprietorship: Transactions 7–8

Sole Proprietorship Transaction #7.

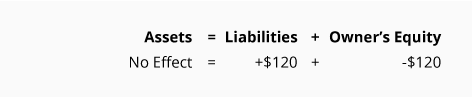

On December 7, 2025, ASC used a temporary help service for 6 hours at a cost of $20 per hour. ASC will pay the invoice when it is due in 10 days. The effect on its accounting equation is:

ASC’s liabilities increased by $120 and the expense caused owner’s equity to decrease by $120.

The liability will be recorded in Accounts Payable and the expense will be recorded in Temp Service Expense. The journal entry for recording the use of the temp service is:

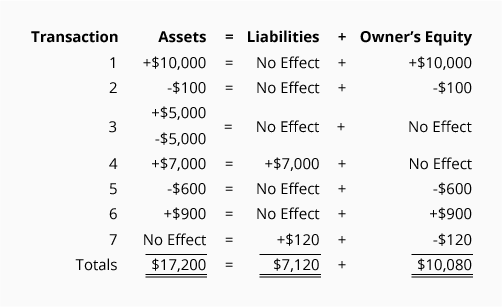

The effect of the first seven transactions on the accounting equation can be viewed here:

The totals indicate that as of midnight on December 7, the company had assets of $17,200 and the sources were $7,120 from the creditors and $10,080 from the owner of the company. The accounting equation totals also tell us that the company had assets of $17,200 with the creditors having a claim of $7,120. This means that the owner’s residual claim was $10,080.

ASC’s balance sheet as of midnight on December 7, 2025 is:

**The income statement (which reports the company’s revenues, expenses, gains, and losses for a specified time interval) is a link between balance sheets. It provides the results of operations—an important part of the change in owner’s equity.

Accounting Software Co.’s income statement for the first seven days of December is:

Sole Proprietorship Transaction #8.

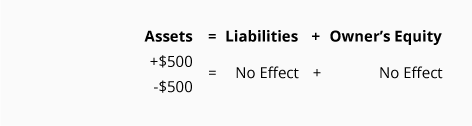

On December 8, 2025, ASC received $500 from the clients it had billed on December 6, 2025. The collection of accounts receivables has this effect on the accounting equation:

The company’s asset (cash) increased and another asset (accounts receivable) decreased. Liabilities and owner’s equity were not affected. (There are no revenues on this date. The revenues were recorded when they were earned on December 6.)

The general journal entry to record the increase in Cash, and the decrease in Accounts Receivable is:

The combined effect of the first eight transactions is shown here:

The totals for the first eight transactions indicate that the company had assets of $17,200. The creditors provided $7,120 and the owner provided $10,080. The accounting equation also indicates that the company’s creditors had a claim of $7,120 and the owner had a residual claim of $10,080.

ASC’s balance sheet as of midnight December 8, 2025 is:

**The income statement (which reports the company’s revenues, expenses, gains, and losses during a specified period of time) is a link between balance sheets. It provides the results of operations—an important part of the change in owner’s equity.

The income statement for ASC for the eight days ending on December 8 is shown here:

Calculating a Missing Amount within Owner’s Equity

The income statement for the calendar year 2025 will explain a portion of the change in the owner’s equity between the balance sheets of December 31, 2024 and December 31, 2025. The other items that account for the change in owner’s equity are the owner’s investments into the sole proprietorship and the owner’s draws (or withdrawals). A recap of these changes is the statement of changes in owner’s equity. Here is a statement of changes in owner’s equity for the year 2025 assuming that the Accounting Software Co. had only the eight transactions that we covered earlier.

Example of Calculating a Missing Amount

The format of the statement of changes in owner’s equity can be used to determine an unknown component. For instance, if the net income for the year 2025 is unknown, but you know the amount of the draws and the beginning and ending balances of owner’s equity, you can calculate the net income. (This might be necessary when a company does not have complete records of its revenues and expenses.) Let’s demonstrate this by using some new hypothetical amounts:

Step 1.

The owner’s equity at December 31, 2024 can be computed using the accounting equation:

Step 2.

The owner’s equity at December 31, 2025 can be computed as well:

Step 3.

Insert into a statement of changes in owner’s equity format the information that was given and the amounts calculated in Step 1 and Step 2:

Step 4.

The “Subtotal” can be calculated by adding the last two numbers on the statement: $94,000 + $40,000 = $134,000. After this calculation we have:

Step 5.

Starting at the top of the statement we know that the owner’s equity before the start of 2025 was $60,000 and in 2025 the owner invested an additional $10,000. As a result we have $70,000 before considering the amount of Net Income. We also know that after the amount of Net Income is added, the Subtotal has to be $134,000 (the Subtotal calculated in Step 4). The Net Income is the difference between $70,000 and $134,000. Net income must have been $64,000.

Step 6.

Insert the previously missing amount (in this case it is the $64,000 of net income) into the statement of changes in owner’s equity and recheck the math:

Since the statement is mathematically correct, we are confident that the net income was $64,000.

The remaining parts of this Explanation will illustrate similar transactions and their effect on the accounting equation when the company is a corporation instead of a sole proprietorship.

Accounting Equation for a Corporation: Transactions C1–C2

The accounting equation (or basic accounting equation) for a corporation is:

Examples

In our examples below, we show how a given transaction affects the accounting equation for a corporation. We also show how the same transaction will be recorded in the company’s general ledger accounts.

In addition, we show the effect of each transaction on the balance sheet and income statement.

Our examples assume that the accrual basis of accounting is being followed.

In the examples that follow, we will use the following accounts:

- Cash

- Accounts Receivable

- Equipment

- Notes Payable

- Accounts Payable

- Common Stock

- Retained Earnings

- Treasury Stock

- Service Revenues

- Advertising Expense

- Temp Service Expense

We also assume that the corporation is a Subchapter S corporation in order to avoid the income tax accounting that would occur with a “C” corporation. (In a Subchapter S corporation the owners are responsible for the income taxes instead of the corporation.)

Corporation Transaction C1

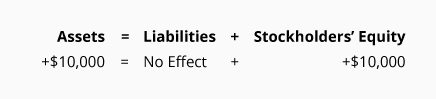

Assume that members of the Ott family form a corporation called Accounting Software, Inc. (ASI). On December 1, 2025, several members of the Ott family invest a total of $10,000 to start ASI. In exchange, the corporation issues a total of 1,000 shares of common stock. (The stock has no par value and no stated value.) The effect on the corporation’s accounting equation is:

Since ASI’s assets increase by $10,000 and stockholders’ equity increases by the same amount the accounting equation is in balance.

The accounting equation tells us that ASI has assets of $10,000 and the source of those assets were the stockholders. Alternatively, the accounting equation tells us that the corporation has assets of $10,000 and the only claim to the assets is from the stockholders (owners).

This transaction is recorded in the asset account Cash and in the stockholders’ equity account Common Stock. The general journal entry to record the transaction is:

After the journal entry is recorded in the accounts, a balance sheet will show ASI’s financial position at the end of December 1, 2025:

Since ASI has not yet earned any revenues nor incurred any expenses, there are no amounts to be reported on an income statement.

Corporation Transaction C2.

On December 2, 2025, ASI purchases $100 of its stock from one of its stockholders. The stock will be held by the corporation as Treasury Stock. The effect of the accounting equation is:

The purchase of its own stock for cash causes ASI’s assets to decrease by $100 and its stockholders’ equity to decrease by $100.

This transaction is recorded in the asset account Cash and in the stockholders’ equity account Treasury Stock. The accounting entry in general journal form is:

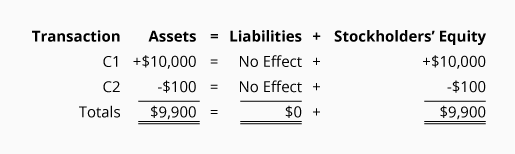

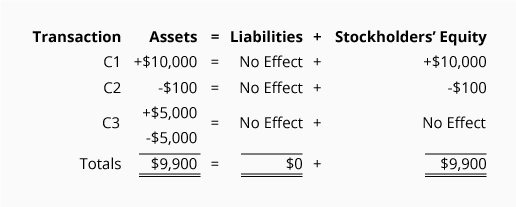

Since the transactions of December 1 and December 2 were in balance, the sum of both transactions should also be in balance:

The totals indicate that ASI has assets of $9,900 and the source of those assets is the stockholders. The accounting equation also shows that the corporation has assets of $9,900 and the only claim against the assets is the stockholders’ claim.

The December 2 balance sheet will communicate the corporation’s financial position as of midnight on December 2:

The purchase of a corporation’s own stock will never result in an amount to be reported on the income statement. Therefore, there is no transaction involving the income statement for the two-day period of December 1 through December 2.

Accounting Equation for a Corporation: Transactions C3–C4

Corporation Transaction C3.

On December 3, 2025, ASI spends $5,000 of cash to purchase computer equipment for use in the business. The effect of this transaction on ASI’s accounting equation is:

The accounting equation shows that one asset increased and one asset decreased. Since the amount of the increase is the same as the amount of the decrease, the accounting equation remains in balance.

This transaction is recorded in the asset accounts Equipment and Cash. The Equipment account increases by $5,000 and the Cash account decreases by $5,000. The journal entry for this transaction is:

The effect on the accounting equation from the first three transactions is:

The totals tell us that the corporation has assets of $9,900 and the source of those assets is the stockholders. The totals tell us that the company has assets of $9,900 and that the only claim against those assets is the stockholders’ claim.

The balance sheet dated December 3, 2025, reflects the financial position of the corporation as of midnight on December 3:

The purchase of equipment is not an immediate expense. It will become part of depreciation expense only after the equipment is placed in service. We will assume that as of December 3 the equipment has not been placed into service. Therefore, there is no expense (or revenue) to be reported on the income statement for the period of December 1-3.

Corporation Transaction C4.

On December 4, 2025, ASI obtains $7,000 by borrowing money from its bank. The effect of this transaction on the accounting equation is:

As you see, ASI’s assets increased and its liabilities increased by $7,000.

This transaction is recorded in the asset account Cash and the liability account Notes Payable with the following journal entry:

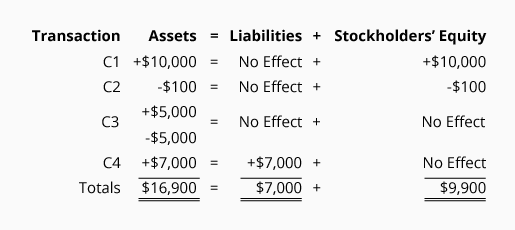

The following shows the effects on the accounting equation from the first four transactions:

These totals indicate that the transactions through December 4 result in assets of $16,900. There are two sources for those assets: the creditors provided $7,000 of assets, and the stockholders provided $9,900. You can also interpret the accounting equation to say that the corporation has assets of $16,900 and the creditors have a claim of $7,000. The stockholders have a residual claim of $9,900.

The balance sheet dated December 4 reports the corporation’s financial position as of the final moment on December 4:

The receipt of money from the bank loan is not revenue since ASI did not earn the money by providing services, investing, etc. As a result, there is no income statement effect from this or earlier transactions.

Accounting Equation for a Corporation: Transactions C5–C6

Corporation Transaction C5.

On December 5, 2025, Accounting Software, Inc. pays $600 for ads that were run in recent days. The effect of the advertising transaction on the corporation’s accounting equation is:

Since ASI is paying $600, its assets decrease. The second effect is a $600 decrease in stockholders’ equity, because the transaction involves an expense. (An expense is a cost that is used up or its future economic value cannot be measured.)

Although stockholders’ equity decreases because of an expense, the transaction is not recorded directly into the retained earnings account. Instead, the amount is initially recorded in the expense account Advertising Expense and in the asset account Cash.

The journal entry for this transaction is:

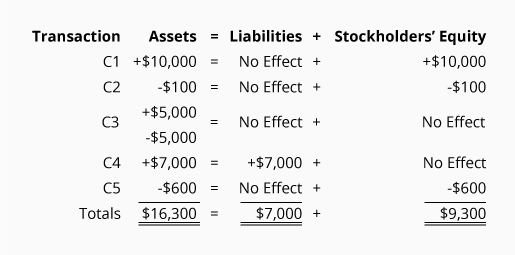

The combined effect of the first five transactions is shown here:

The totals now indicate that Accounting Software, Inc. has assets of $16,300. The creditors provided $7,000 and the stockholders provided $9,300. Viewed another way, the corporation has assets of $16,300 with the creditors having a claim of $7,000 and the stockholders having a residual claim of $9,300.

The balance sheet as of the end of December 5 is:

**The income statement (which reports the company’s revenues, expenses, gains, and losses for a specified time period) is a link between balance sheets. It provides the results of operations—an important part of the change in retained earnings and stockholders’ equity.

Since this transaction involves an expense, it will be reported on ASI’s income statement. The corporation’s income statement for the first five days of December is presented here:

Because we assumed that Accounting Services, Inc. is a Subchapter S corporation, income tax expense is not reported on the corporation’s income statement.

Corporation Transaction C6.

On December 6, 2025, ASI performed consulting services for its clients. The clients were billed for the agreed upon amount of $900. The amounts are to be paid within 30 days. The effect on ASI’s accounting equation is:

Since ASI has completed the services, it has earned revenues and it has the right to receive $900 from its clients. This right increases the asset accounts receivable. The earning of revenues also causes stockholders’ equity to increase.

Although revenues cause stockholders’ equity to increase, the revenue transaction is not recorded directly into a stockholders’ equity account. Rather, the amount earned is recorded in the revenue account Service Revenues. At some point, the amount in the revenue accounts will be transferred to the retained earnings account.

The general journal entry for Transaction #6 is:

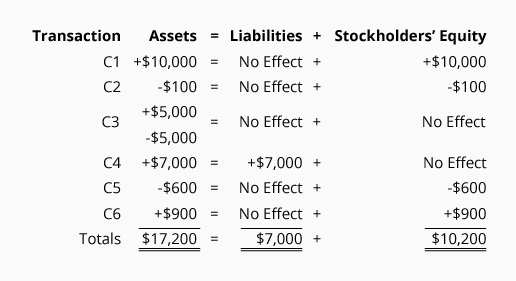

The effect on the accounting equation from the first six transactions can be viewed here:

The totals tell us that at the end of December 6, the corporation had assets of $17,200 of which $7,000 came from creditors and $10,200 came from stockholders. The totals can also be viewed another way: ASI had assets of $17,200 with its creditors having a claim of $7,000 and the stockholders having a residual claim for the remainder of $10,200.

The balance sheet as of midnight on December 6 is presented here:

**The income statement (which reports the company’s revenues, expenses, gains, and losses for a specified time period) is a link between balance sheets. It provides the results of operations—an important part of the change in retained earnings and stockholders’ equity.

The income statement for Accounting Software, Inc. for the six days ended December 6 is shown here:

Accounting Equation for a Corporation: Transactions C7–C8

Corporation Transaction C7.

On December 7, 2025, ASI uses a temporary help service for 6 hours at a cost of $20 per hour. ASI records the invoice immediately, but it will pay the $120 when it is due in 10 days. This transaction has the following effect on the accounting equation:

The accounting equation shows that ASI’s liabilities increased by $120 and the expense caused stockholders’ equity to decrease by $120.

The liability will be recorded in Accounts Payable and the expense will be recorded in Temp Service Expense. The general journal entry for utilizing the temp service is:

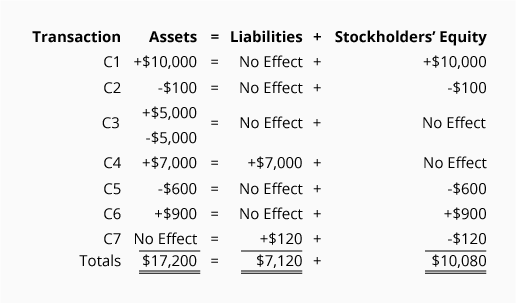

The effect of the first seven transactions on the accounting equation can be viewed here:

The totals show us that the corporation had assets of $17,200 with $7,120 provided by the creditors and $10,080 provided by the stockholders. The accounting equation also reveals that the corporation’s creditors had a claim of $7,120 and the stockholders had a residual claim for the remaining $10,080.

The financial position of ASI as of midnight of December 7 is presented in the following balance sheet:

**The income statement (which reports the corporations’ revenues, expenses, gains, and losses for a specified time period) is a link between balance sheets. It provides the results of operations—an important part of the change in stockholders’ equity.

The income statement for the first seven days of December is shown here:

Corporation Transaction C8.

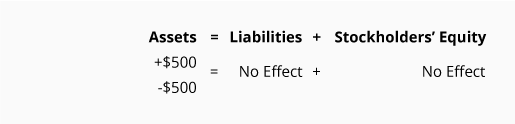

On December 8, 2025, ASI received $500 from the clients it had billed on December 6. The effect on the accounting equation is:

The corporation’s cash increased and one of its other assets (accounts receivable) decreased. Liabilities and stockholders’ equity were not affected. (There are no revenues on this date. The revenues were recorded when they were earned on December 6.)

The general journal entry to record the increase in Cash and the decrease in Accounts Receivable is:

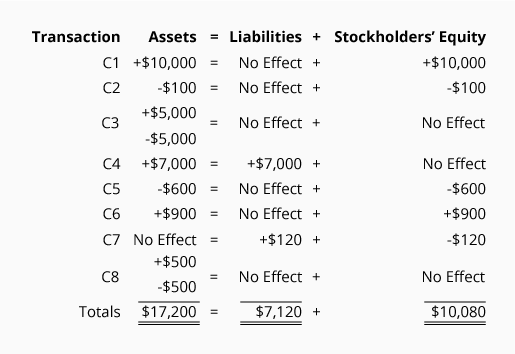

The effect on the accounting equation from the transactions through December 8 is shown here:

The totals after the first eight transactions indicate that the corporation had assets of $17,200. The creditors provided $7,120 and the company’s stockholders provided $10,080. The accounting equation also indicates that the company’s creditors had a claim of $7,120 and the stockholders had a residual claim of $10,080.

ASI’s balance sheet as of midnight of December 8 is shown here:

**The income statement (which reports the corporation’s revenues, expenses, gains, and losses for a specified time period) is a link between balance sheets. It provides the results of operations—an important part of the change in stockholders’ equity.

The income statement for ASI’s first eight days of operations is shown here:

Expanded Accounting Equation for a Sole Proprietorship

The owner’s equity in the basic accounting equation is sometimes expanded to show the accounts that make up owner’s equity: Owner’s Capital, Revenues, Expenses, and Owner’s Draws.

Instead of the accounting equation, Assets = Liabilities + Owner’s Equity, the expanded accounting equation is:

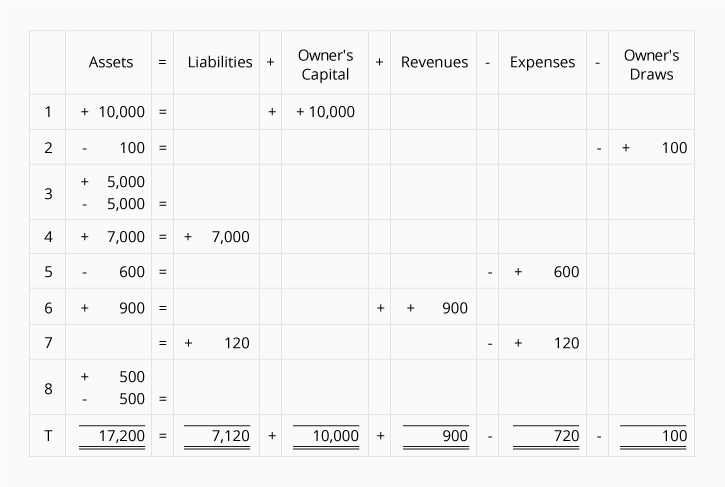

The eight transactions that we had listed under the basic accounting equation for a Sole Proprietorship Transaction #8 are shown in the following expanded accounting equation:

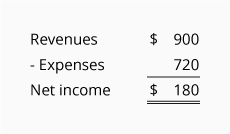

With the expanded accounting equation, you can easily see the company’s net income:

Expanded Accounting Equation for a Corporation

The stockholders’ equity part of the basic accounting equation can also be expanded to show the accounts that make up stockholders’ equity: Paid-in Capital, Revenues, Expenses, Dividends, and Treasury Stock.

Instead of the accounting equation, Assets = Liabilities + Stockholders’ Equity, the expanded accounting equation is:

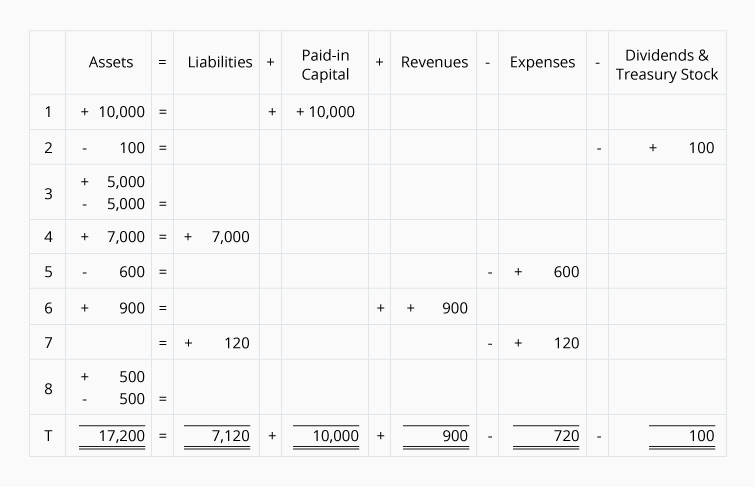

The eight transactions that we had listed under the basic accounting equation for a Corporation Transaction C8 are shown in the following expanded accounting equation:

With the expanded accounting equation, you can easily see the corporation’s net income:

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Accounting Equation materials (see the full outline below, after the following Disclaimer).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.

Earn Our Certificate

for This Topic

When you join PRO, you will receive instant access to 16 different Certificates of Achievement plus our Bookkeeping Certificate of Excellence.

View PRO Features