Introduction

If left undisturbed, a single amount deposited today into your savings account will grow to a larger balance. That future balance is referred to as a future value or FV. Over a long period of time, the future value of that single deposit can grow to be a significant amount for two reasons:

- the initial deposit earns interest, and

- the interest added to your account will also earn interest.

Earning interest on the previously earned interest is known as compound interest.

The calculation of future value determines just how much a single deposit, investment, or balance will grow to, assuming it is left untouched and earns compound interest at a specified interest rate. The calculation of the future value of a single amount can also be used to predict what a present cost of an item will grow to at a future date, when the item’s cost increases at a constant rate. Additionally, the formula for computing the future value can be used to determine either the interest rate or the length of time necessary to reach a desired future value.

Our explanation of future value will use timelines for each of the many illustrations in order for you to develop a thorough understanding of the future value of a single amount. Throughout our explanation we will utilize future value tables and future value factors. After mastering these calculations of the future value of a single amount, you are encouraged to use a financial calculator or computer software in order to obtain more precision.

The future value of a single amount is mathematically related to the Present Value of a Single Amount, another topic on this website.

WATCH NOW

Advance Your Career with Our PRO Training

What’s Involved in Future Value (FV) Calculations

The future value of a single amount involves four variables:

If you know any three of these four variables, you will be able to calculate the unknown amount.

Visualizing Compound Interest

To illustrate the compounding of interest in the calculation of a future value, we will assume that a single amount of $10,000 will be deposited into an account on January 1, and it will remain on deposit for one year. The depositor may select one of three accounts and each of the accounts pays interest of 8% per year. However, the three accounts will differ in the compounding of interest as noted here:

-

Account #1. The interest will be added to the account at the end of the year. (Interest is compounded annually on December 31.)

-

Account #2. The interest will be added to the account at the end of each six-month period. (Interest is compounded semiannually on June 30 and December 31.)

-

Account #3. The interest will be added to the account at the end of each calendar quarter. (Interest is compounded quarterly on March 31, June 30, September 30, and December 31.)

The following timelines will allow us to visualize the compounding of interest and its effect on each account’s ending balance.

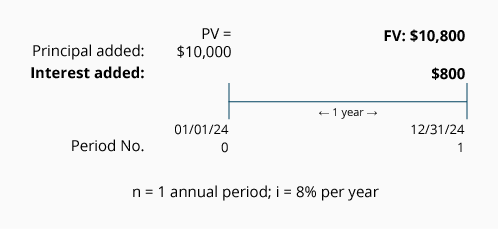

Account #1.

A single amount of $10,000 is deposited on January 1, 2026 and will remain in the account until December 31, 2026. The account will earn interest of 8% per year compounded annually. The timeline showing this information appears here:

The timeline shows the single deposit of $10,000 as the present value and occurring at time period 0. (Time period 0 is the present time and it is also the beginning of the first time period.) The timeline also shows that the interest earned during the year 2026 is $800 ($10,000 x 8%) and it is added on December 31, 2026. The result is a future value at December 31, 2026 of $10,800.

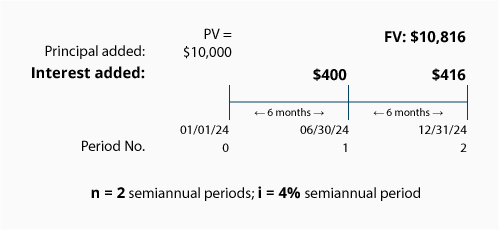

Account #2.

A single amount of $10,000 is deposited on January 1, 2026 and will remain in the account until December 31, 2026. The account will earn interest at 8% per year but the interest is compounded semiannually. Because interest will be compounded semiannually, the variables n and i must be stated in six-month or semiannual terms as shown in the following timeline:

Again, the $10,000 is the present value shown at time period 0. The timeline also shows that $400 ($10,000 x 4%; or $10,000 x 8% x 0.5 year) of interest is added to the account on June 30, 2026. After the interest is added to the account, the new balance of $10,400 will earn interest during the second half of the year—resulting in interest of $416 ($10,400 x 4% = $416) added on December 31, 2026. The result is a future value at December 31, 2026 of $10,816.

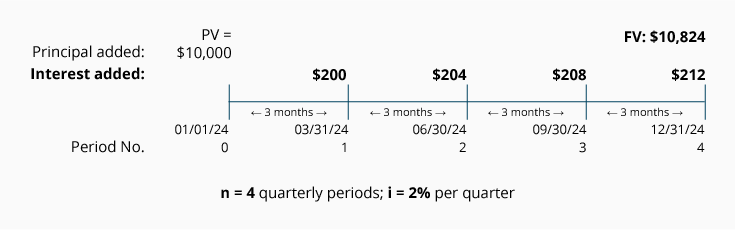

Account #3.

A single amount of $10,000 is deposited on January 1, 2026 and will remain in the account until December 31, 2026. The account will earn interest at 8% per year but the interest is compounded quarterly. As a result the variables n and i must be thought of in terms of quarters or three-month periods as shown in the following timeline:

The present value of $10,000 will be earning compounded interest every three months. During the first quarter, the account will earn $200 ($10,000 x 2%; or $10,000 x 8% x 3/12 of a year) and will result in a balance of $10,200 on March 31. During the second quarter of 2026 the account will earn interest of $204 based on the account balance as of March 31, 2026 ($10,200 x 2% per quarter). The interest for the third quarter is $208 ($10,404 x 2%) and the interest for the fourth quarter is $212 ($10,612 x 2%). The result is a future value of $10,824 at December 31, 2026.

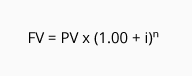

Mathematics of Future Value

The future value of a present amount can be expressed as:

We will illustrate how this mathematical expression works by using the amounts from the three accounts above.

Account #1: Annual Compounding

A single deposit of $10,000 will earn interest at 8% per year and the interest will be deposited at the end of one year. Since the interest is compounded annually, the one-year period can be represented by n = 1 and the corresponding interest rate will be i = 8% per year:

The formula shows that the present value of $10,000 will grow to the FV of $10,800 at the end of one year when interest of 8% is earned and the interest is added to the account only at the end of the year.

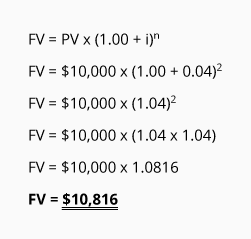

Account #2: Semiannual Compounding

In Account #2 the $10,000 deposit will earn interest at 8% per year, but the interest will be deposited at the end of each six-month period for one year. With semiannual compounding, the life of the investment is stated as n = 2 six-month periods. The interest rate per six-month period is i = 4% (8% annually divided by 2 six-month periods).

The present value of $10,000 will grow to a future value of $10,816 (rounded) at the end of two semiannual periods when the 8% annual interest rate is compounded semiannually.

Account #3: Quarterly Compounding

In Account #3 the $10,000 deposit will earn interest at 8% per year, but the interest earned will be deposited at the end of each three-month period for one year. With quarterly compounding, the life of the investment is stated as n = 4 quarterly periods. The annual interest rate is restated to be the quarterly rate of i = 2% (8% per year divided by 4 three-month periods).

The present value of $10,000 will grow to a future value of $10,824 (rounded) at the end of one year when the 8% annual interest rate is compounded quarterly.

Future Values for Greater Than One Year

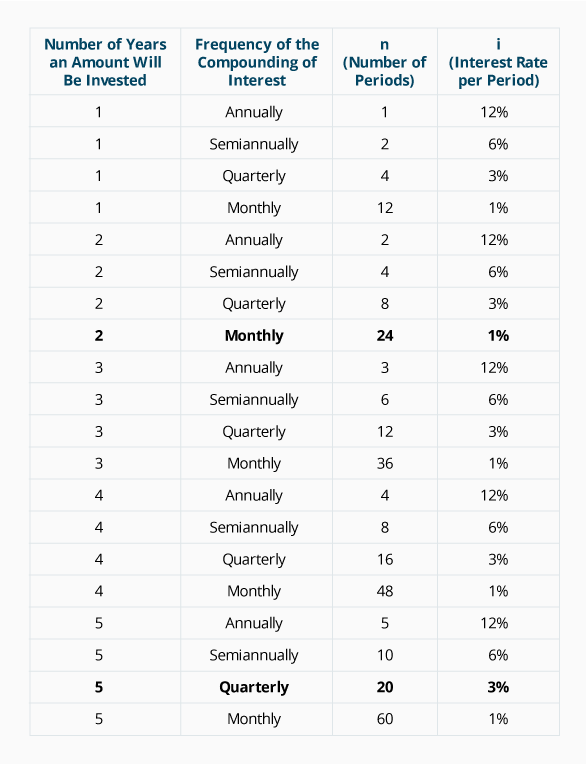

To be certain that you understand how the number of periods, n, and the interest rate, i, must be aligned with the compounding assumptions, we prepared the following chart. Note that the chart assumes an interest rate of 12% per year.

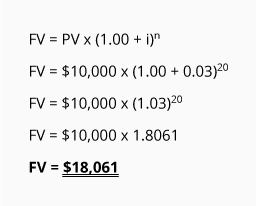

To be certain you understand the information in the chart, let’s assume that a single amount of $10,000 is deposited on January 1, 2026 and will remain in the account until December 31, 2030. This will mean a total of five years: 2026, 2027, 2028, 2029, and 2030. If the account will pay interest of 12% per year compounded quarterly, then n = 20 quarterly periods (5 years x 4 quarters per year), and i = 3% per quarter (12% per year divided by 4 quarters per year). The mathematical expression will be:

Let’s try one more example. Assume that a single amount of $10,000 is deposited on January 1, 2026 and will remain in the account until December 31, 2027 (a total of two years). If the account will pay interest of 12% per year compounded monthly, then n = 24 months (2 years x 12 months per year), and i = 1% per month (12% per year divided by 12 months per year). The mathematical expression will be:

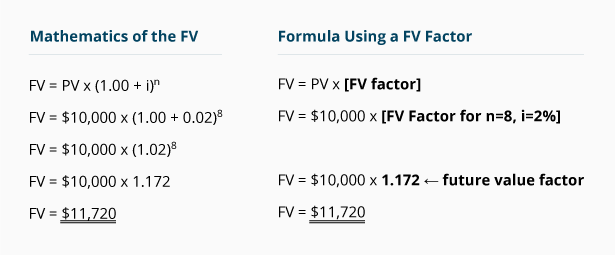

Future Value Factors

The mathematics for calculating the future value of a single amount of $10,000 earning 8% per year compounded quarterly for two years appears in the left column of the following table. In the right column is the formula which uses a future value factor.

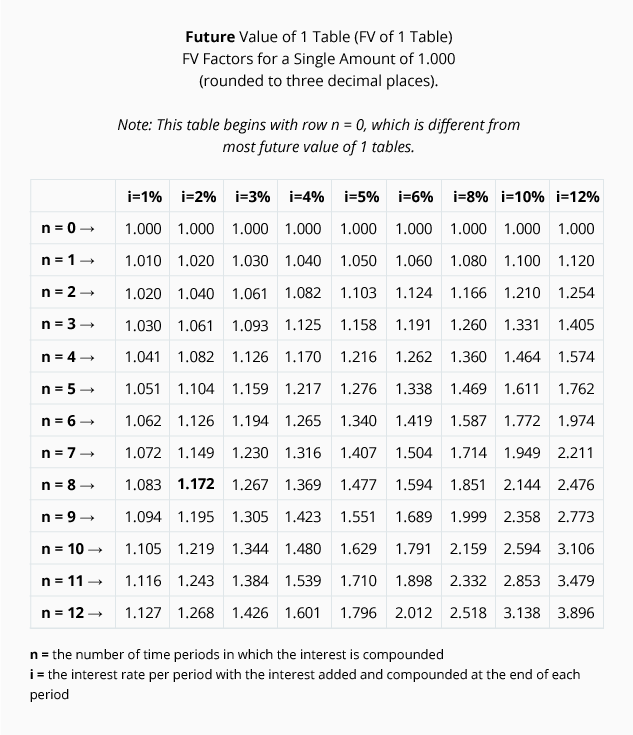

Future value factors are available in future value tables, such as the abbreviated version shown here:

We highlighted the factor used in our computation. As you can see, the future value factor of 1.172 is located where n = 8, and i = 2%.

Our future value of 1 table is unique in that we have an additional row: n = 0. Most FV of 1 tables omit the row for n = 0, and begin with the row n =1. There should be no difference in FV factors other than minor rounding differences.

To appreciate the usefulness of the FV of 1 table, focus on the column with the heading of i = 10%. This column tells you that the present value of 1.000 is 1.000 at time period 0—the present time. As you move down the 10% column, the next row (where n = 1) shows that the future value will increase by 10% to 1.100. Continuing down the 10% column, you see that at the end of two periods (n = 2) the future value is 1.210, an increase of 0.110 (1.100 x 10%). The next figure down indicates that at the end of three periods the future value is 1.331, which is an increase of 0.121 (1.331 – 1.210; and 1.210 x 10%).

The FV of 1 table provides the future amounts at compound interest for a single amount of 1.000 at various interest rates. These factors should make the future calculations a bit simpler than calculations using exponents.

The 10% column of the future value table can be used to determine the future value of a single $1.00 invested today at 10% interest compounded annually. The single $1.00 amount will grow to $3.138 at the end of 12 years. The FV table also provides some insight as to the future cost of items that are expected to increase at a constant rate. For example, if a cup of coffee presently costs $1.00 and the cost is expected to increase by 10% per year compounded annually, then a cup of coffee will cost $3.138 per cup at the end of 12 years.

We can also use the factors for amounts greater than $1. For example, if the monthly cost of a family’s health insurance plan is $1,000 at the present time and it is expected to increase by 10% per year compounded annually, then the monthly cost at the end of 12 years will be $3,138.

Throughout the remainder of this topic we will use a more complete Future Value of 1 Table:

Click here to open the FV of 1 Table

Calculating the Future Value of a Single Amount (FV)

If we know the single amount (PV), the interest rate (i), and the number of periods of compounding (n), we can calculate the future value (FV) of the single amount. Calculations #1 through #5 illustrate how to determine the future value (FV) through the use of future value factors.

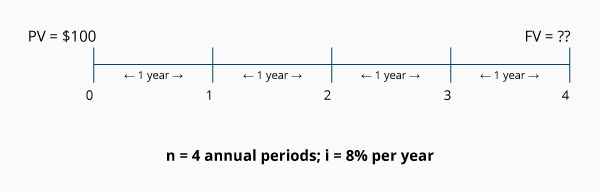

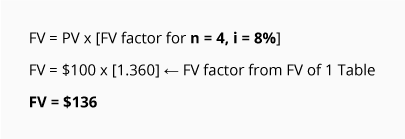

Calculation #1

You make a single deposit of $100 today. It will remain invested for 4 years at 8% per year compounded annually. What will be the future value of your single deposit at the end of 4 years?

The following timeline plots the variables that are known and unknown:

Calculation using an FV factor:

At the end of 4 years, you will have $136 in your account.

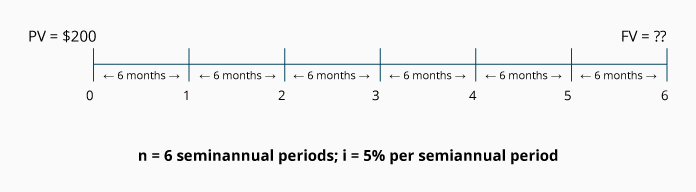

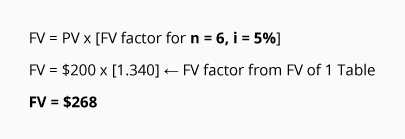

Calculation #2

Paul makes a single deposit today of $200. The deposit will be invested for 3 years at an interest rate of 10% per year compounded semiannually. What will be the future value of Paul’s account at the end of 3 years?

The following timeline plots the variables that are known and unknown:

Because the interest is compounded semiannually, we convert 3 years to 6 semiannual periods, and the annual interest rate of 10% to the semiannual rate of 5%.

Calculation using an FV factor:

At the end of 3 years, Paul will have $268 in his account.

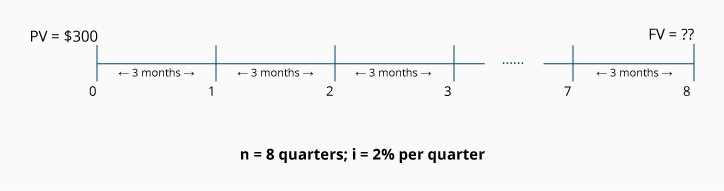

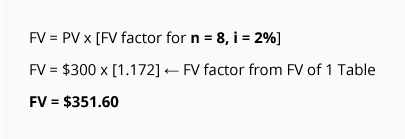

Calculation #3

Sheila invests a single amount of $300 today in an account that will pay her 8% per year compounded quarterly. Compute the future value of Sheila’s account at the end of 2 years.

The following timeline plots the variables that are known and unknown:

Because interest is compounded quarterly, we convert 2 years to 8 quarters, and the annual rate of 8% to the quarterly rate of 2%.

Calculation using an FV factor:

At the end of 2 years, Sheila will have $351.60 in her account.

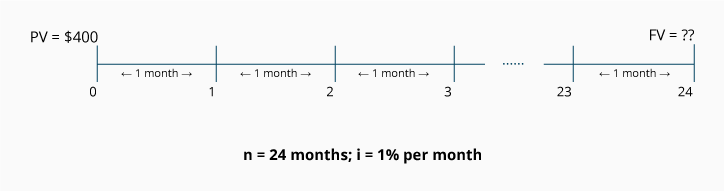

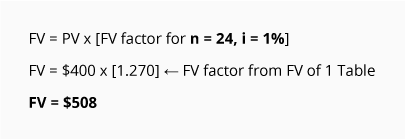

Calculation #4

You invest $400 today in an account that earns interest at a rate of 12% per year compounded monthly. What will be the future value at the end of 2 years?

The following timeline plots the variables that are known and unknown:

Because the interest is compounded monthly, we convert 2 years to 24 months, and the annual rate of 12% to the monthly rate of 1%.

Calculation using an FV factor:

At the end of 2 years, you will have $508 in your account.

Calculating the Number of Time Periods (n)

If we know the present value (PV), the future value (FV), and the interest rate per period of compounding (i), the future value factors allow us to calculate the unknown number of time periods of compound interest (n). Calculations #5 through #8 illustrate how to determine the number of time periods (n).

Calculation #5

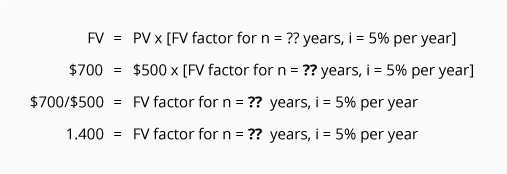

An airplane ticket costs $500 today and it is expected to increase at a rate of 5% per year compounded annually. Determine the number of years it will take for the $500 airplane ticket to have a future cost of $700.

The following timeline plots the variables that are known and unknown:

Because the rate of increase is compounded annually, we use the given annual rate of 5%. The answer (n) will be stated in annual time periods (years).

Calculation using the FV of 1 Table:

To finish solving the equation, we search only the i = 5% column of the FV of 1 Table for the future value factor that is closest to 1.400. In this case, the factor we find is 1.407, and we see it is located in the row where n = 7. This tells us that it will take approximately 7 annual time periods (7 years) for an airplane ticket to go from its present cost of $500 to the future cost of $700.

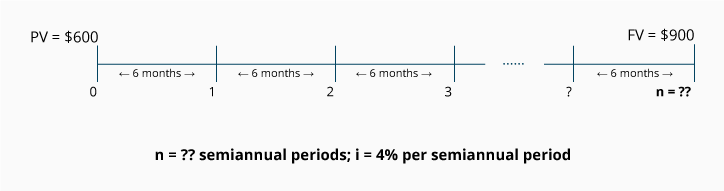

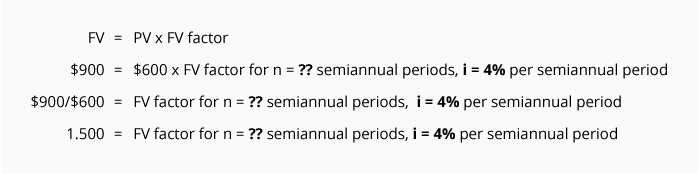

Calculation #6

Lorenzo put $600 today in an account that earns an annual rate of 8% compounded semiannually. How many years will it take for Lorenzo’s single investment of $600 to have a future value of $900?

The following timeline plots the variables that are known and unknown:

Because the interest is compounded semiannually, we converted the annual interest rate of 8% to the semiannual rate of 4%.

Calculation using the FV of 1 Table:

To finish solving the equation, we search only the 4% column of the FV of 1 Table for the future value factor that is closest to 1.500. In this case, the factor we find is 1.480, and we see it is located in the row where n = 10. This means it will require 5 years (10 semiannual time periods divided by 2 semiannual periods in each year) for Lorenzo’s $600 to reach a future value of $900.

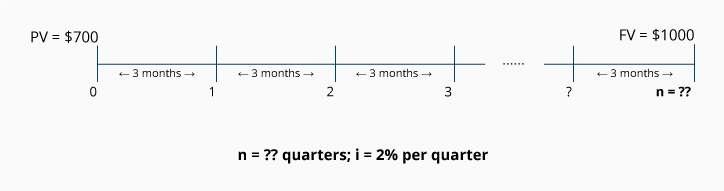

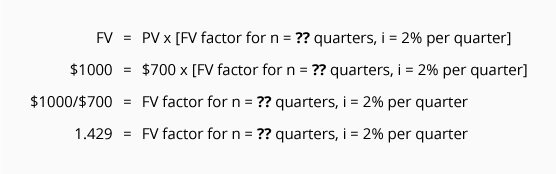

Calculation #7

Nancy invests a sum of $700 at a fixed rate of 8% per year with quarterly compounding. How many years will it take her $700 investment to reach a future value of $1,000?

The following timeline plots the variables that are known and unknown:

Because the interest is compounded quarterly (every 3 months), the annual interest rate is converted to 2% per quarter.

Calculation using the FV of 1 Table:

To finish solving the equation, we search only the 2% column of the FV of 1 Table for the future value factor that is closest to 1.429. In this case, the factor is 1.428, and we see it is located in the row where n = 18.

To convert n = 18 quarters to years, we simply divide the 18 quarters by 4, the number of quarterly periods in a year. The answer is that it will take approximately 4.5 years for Nancy’s $700 investment to reach a future value of $1,000.

Calculation #8

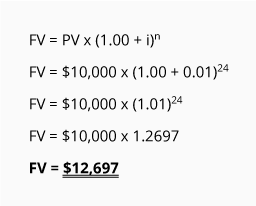

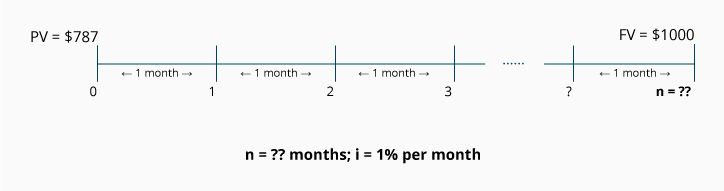

You invest $787 today in an account that will return an annual interest rate of 12% with interest compounded monthly. How many years will it take for the $787 investment to have a future value of $1,000?

The following timeline plots the variables that are known and unknown:

Because the interest is compounded monthly, we convert the annual rate of 12% to i = 1% per month.

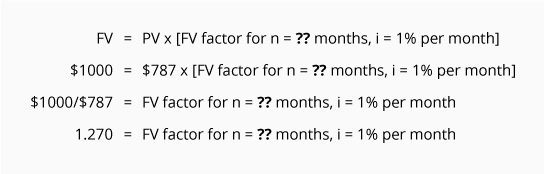

Calculation using the FV of 1 Table:

To finish solving the equation, we search only the i = 1% column in the FV of 1 Table for the FV factor that is closest to 1.270. In this case, there is a factor of exactly 1.270, and it is located in the row where n = 24.

Since n = 24 monthly time periods, we need to divide the 24 months by 12 months in a year in order to get the answer in years. It will take approximately 2 years for your $787 investment to reach a future value of $1,000.

Calculating the Interest Rate (i)

If we know the present value (PV), the future value (FV), and the number of time periods of compound interest (n), future value factors will allow us to calculate the unknown interest rate (i). Calculations #9 through #12 illustrate how to determine the interest rate (i).

Calculation #9

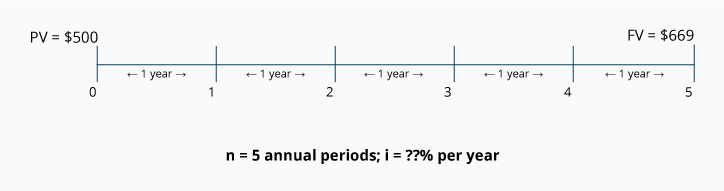

A single investment of $500 is made today and will remain invested for 5 years. At the end of the 5th year, the future value will be $669. Assuming that the interest is compounded annually, calculate the annual interest rate earned on this investment.

The following timeline plots the variables that are known and unknown:

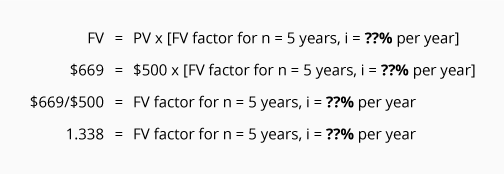

Calculation using the FV of 1 Table:

To finish solving the equation, we search only the “n = 5” row of the FV of 1 Table for the FV factor that is closest to 1.338. In this case, there is a factor of 1.338, and it is located in the column with the heading i = 6%.

Since the time periods are one-year periods, the interest rate is 6% per year compounded annually.

Calculation #10

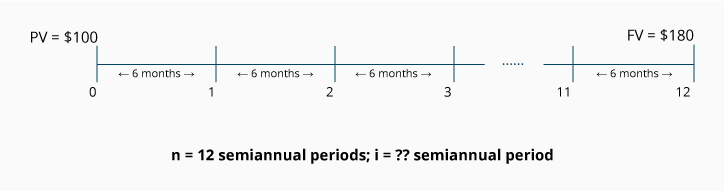

A basket of goods has a cost today of $100. Assume that the cost is estimated to increase to $180 at the end of 6 years. What is the annual rate of increase if the cost increases are compounded semiannually?

The following timeline plots the variables that are known and unknown:

Because the rate of increase (the “interest”) is compounded semiannually, we convert the 6 years to 12 semiannual time periods.

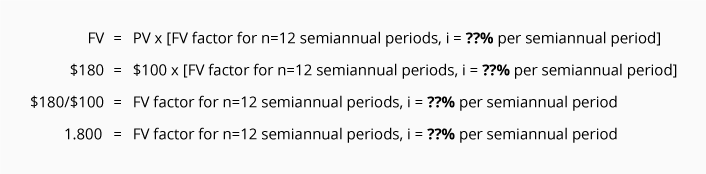

Calculation using the FV of 1 Table:

To finish solving the equation, we search only the row “n = 12” of the FV of 1 Table for the FV factor that is closest to 1.800. In this case, there is a factor of 1.796 located in the column where i = 5%.

Since (n) represents semiannual time periods, the rate of 5% is the semiannual rate, or the rate for a six-month period. To convert the semiannual rate to an annual rate, we multiply 5% x 2, the number of semiannual periods in a year. This means that the rate of increase for the basket of goods is 10% per year compounded semiannually.

Calculation #11

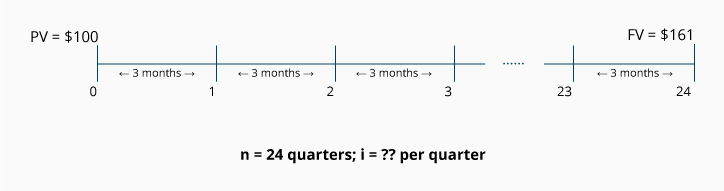

Assume you invest $100 today and intend to keep it invested for 6 years. You are told that at the end of the 6th year, the future value of your account will be $161. Assuming that the interest is compounded quarterly, compute the annual interest rate you are earning on this investment.

The following timeline plots the variables that are known and unknown:

Because the interest is compounded quarterly, we convert the 6 years to 24 quarterly time periods. In other words, we will refer to n = 24 when using the FV of 1 Table.

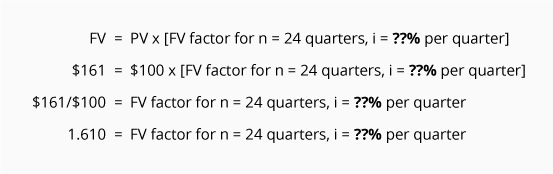

Calculation using the FV of 1 Table:

To finish solving the equation, we search only the row where n = 24 in the FV of 1 Table for the future value factor. We look for the FV factor that is closest to 1.610. In this case, a factor of 1.608 is located in the column where i = 2%.

Since 2% is the interest rate per quarter, we multiply the quarterly rate of 2% x 4, the number of quarterly periods in a year. Hence the investment is earning an interest rate of 8% per year compounded quarterly.

Calculation #12

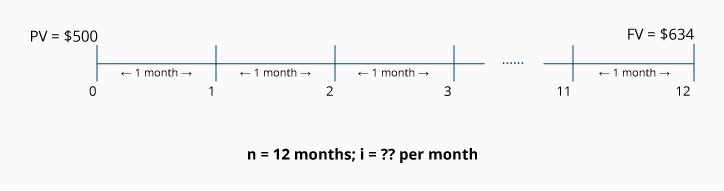

Aaron has a sum of $500 and he needs for it to grow to a future value of $634 by the end of one year. Assuming that the interest rate is compounded monthly, what interest rate does Aaron need for his investment?

The following timeline plots the variables that are known and unknown:

Because the interest is compounded monthly, we convert the 1 year time period to n = 12 monthly time periods.

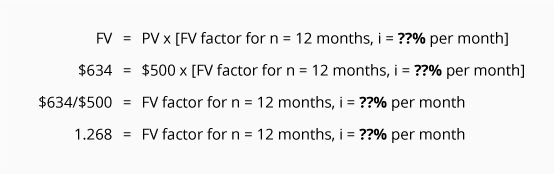

Calculation using the FV of 1 Table:

To finish solving the equation, we search only the row where n = 12 in the FV of 1 Table for the FV factor that is closest to 1.268. In this case, the factor of 1.268 is located in the column where i = 2%.

Since i = 2% is the monthly rate, we multiply 2% x 12, the number of monthly periods in a year in order to determine the annual rate. In this case, Aaron needs to find an interest rate of 24% per year compounded monthly in order to reach his future value goal of $634 in one year.

Calculating the Single Amount (PV)

If we know the future value (FV), the number of time periods of compound interest (n), and the interest rate (i), we can use future value factors to calculate the unknown amount that was originally deposited (the “present value,” or PV). Calculations #13 through #16 illustrate how to determine the present value (PV).

(Note: The single amount can also be calculated by using present value factors. This is discussed in our Present Value of a Single Amount Explanation.)

Calculation #13

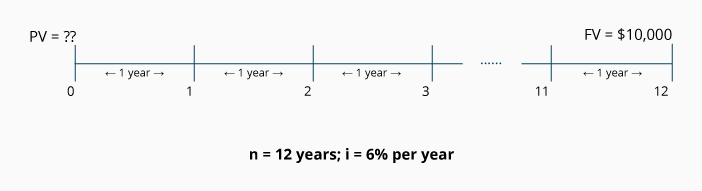

Joan wishes to make one deposit today into an individual retirement account (IRA) that is guaranteed to earn 6% per year compounded annually. She wants the amount deposited to grow to $10,000 at the end of 12 years. How much will she need to deposit today?

The following timeline plots the variables that are known and unknown:

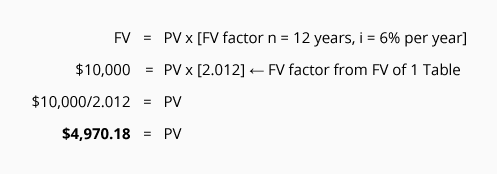

Calculation using the FV of 1 Table:

In order to have a future value of $10,000 in 12 years, Joan must deposit $4,970.18 today in her IRA.

Calculation #14

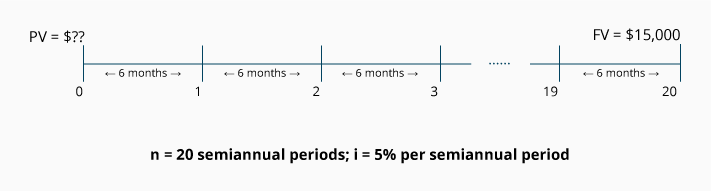

What amount will you need to invest today in order to have $15,000 at the end of 10 years? Assume your amount will earn 10% per year compounded semiannually.

The following timeline plots the variables that are known and unknown:

Because the interest is compounded semiannually, we convert the 10 annual time periods to 20 semiannual time periods. Similarly, the interest rate is converted from 10% per year to 5% per semiannual period.

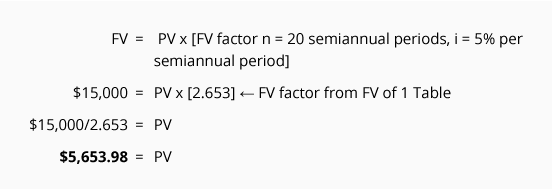

Calculation using the FV of 1 Table:

You need to invest $5,653.98 today in order to have it grow to $15,000 in 20 six-month periods with interest at 10% per year compounded semiannually.

Calculation #15

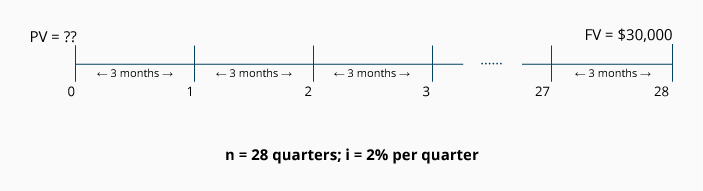

What amount today will grow to $30,000 at the end of 7 years if the amount earns 8% per year compounded quarterly?

The following timeline plots the variables that are known and unknown:

Because the interest is compounded quarterly, we convert the 7 one-year time periods to 28 quarters. Similarly, the interest rate is converted from 8% per year to 2% per quarter. In other words, n = 28 quarters, and i = 2% per quarter.

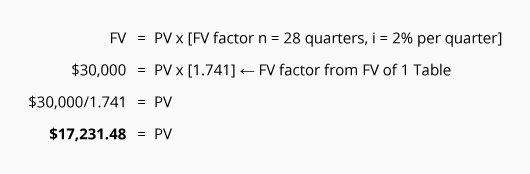

Calculation using the FV of 1 Table:

A single deposit of $17,231.48 will grow to $30,000 if it remains invested at 8% per year compounded quarterly for 7 years.

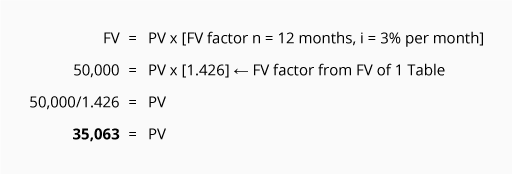

Calculation #16

The number of visitors to Bill’s website is increasing at an annual rate of 36% compounded monthly. By the end of one year Bill expects the number of visitors to his site to reach 50,000 per day. What is the present number of visitors per day?

The following timeline plots the variables that are known and unknown:

Because the rate is compounded monthly, we convert the one-year time period to 12 monthly time periods. Similarly, the rate is converted from 36% per year to 3% per month.

Calculation using the FV of 1 Table:

The present amount of visitors per day must be 35,063 if a 3% per month compounded increase results in 50,000 visitors per day after 12 months. (You can verify the answer 35,063 by reviewing the table below.)

If our future value factors were not rounded to only 3 decimal places, the present number of visitors per day at December 31, 2025 would have been 35,069 and that would result in 50,000 at Dec 31, 2026.

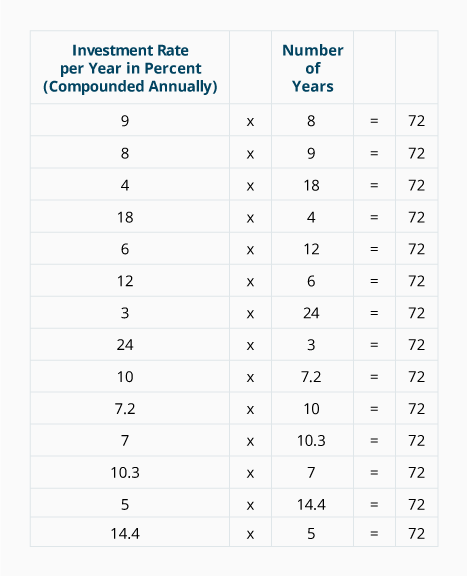

Double Your Money: The Rule of 72

The Rule of 72 is a quick and simple technique for estimating one of two things:

- The time it takes for a single amount of money to double with a known interest rate.

- The rate of interest you need to earn for an amount to double within a known time period.

The rule states that an investment or a cost will double when:

[Investment Rate per year as a percent] x [Number of Years] = 72.

When interest is compounded annually, a single amount will double in each of the following situations:

The Rule of 72 indicates than an investment earning 9% per year compounded annually will double in 8 years. The rule also means if you want your money to double in 4 years, you need to find an investment that earns 18% per year compounded annually.

You can confirm the rationality of the Rule of 72 as follows: Find factors on the FV of 1 Table that are close to 2.000. (The factor of 2.000 tells you that the present value of 1.000 had doubled to the future value of 2.000.) When you find a factor close to 2.000, look at the interest rate at the top of the column and look at the number of periods (n) in the far left column of the row containing the factor. Multiply that interest rate times the number of periods and you will get the product 72.

To use the Rule of 72 in order to determine the approximate length of time it will take for your money to double, simply divide 72 by the annual interest rate. For example, if the interest rate earned is 6%, it will take 12 years (72 divided by 6) for your money to double. If you want your money to double every 8 years, you will need to earn an interest rate of 9% (72 divided by 8).

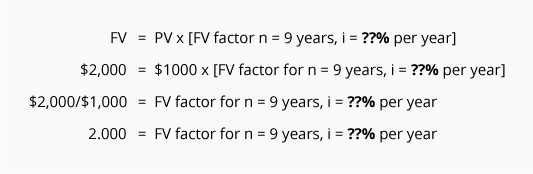

Here’s another way to demonstrate that the Rule of 72 works. Assume you make a single deposit of $1,000 to an account and wish for it to grow to a future value of $2,000 in nine years. What annual interest rate compounded annually will the account have to pay? The Rule of 72 indicates that the rate must be 8% (72 divided by 9 years). Let’s verify the rate with the format we used with the FV Table:

To finish solving the equation, we search only the “n = 9” row of the FV of 1 Table for the FV factor that is closest to 2.000. The factor closest to 2.000 in the row where n = 9 is 1.999 and it is in the column where i = 8%. An investment at 8% per year compounded annually for 9 years will cause the investment to double (8 x 9 = 72).

Future Value of Varying Amounts and/or Time Intervals

The future value of multiple amounts is determined by calculating, and then adding together, the future value for each single amount. We illustrate this with Calculations #17 and #18.

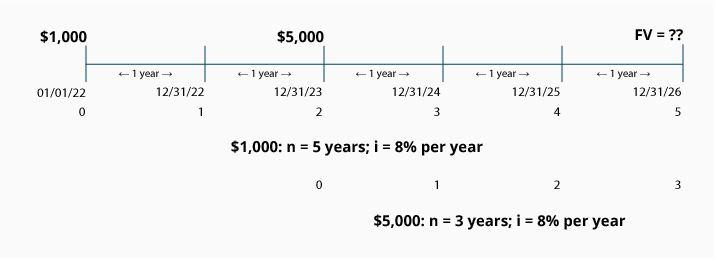

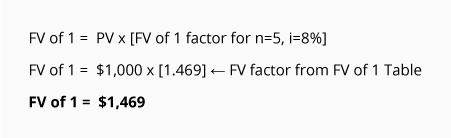

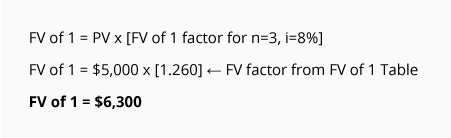

Calculation #17

You are asked to determine the total future value on December 31, 2028 of a $1,000 deposit made on January 1, 2024 plus a $5,000 deposit that was made on January 1, 2026. Both amounts will earn 8% per year compounded annually. The timeline for this information is:

The total future value on December 31, 2028 is the sum of these two calculations:

Future value calculation of the $1,000 deposited on Jan 1, 2024:

Future value calculation of the $5,000 deposited on Jan 1, 2026:

The total future value on December 31, 2028 for these two deposits will be $7,769. You can verify the future value of $7,769 with the following table:

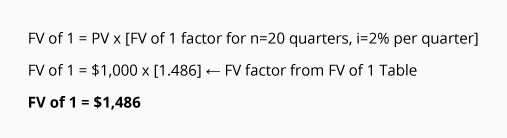

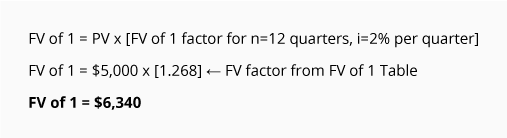

Calculation #18

You are asked to determine the total future value on December 31, 2028 of the $1,000 deposit made on January 1, 2024 plus the $5,000 deposit made on December 31, 2025. Both amounts will earn 8% per year compounded quarterly.

Because the interest is compounded quarterly, we convert the first deposit from 5 years to 20 quarterly periods, and the second deposit from 3 years to 12 quarterly periods. We convert the interest rate of 8% per year to the rate of 2% per quarter.

The following calculations reflect the restatement to quarters. Again, the sum of the answers to these two equations will be the future value on December 31, 2028.

Future value calculation of the $1,000 deposited on Jan 1, 2024:

Future value calculation of the $5,000 deposited on Dec 31, 2025:

The total future value on December 31, 2028 for these two deposits will be $7,826. You can verify the future value of $7,826 with the following table:

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Future Value of a Single Amount materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.