For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.

A chart of accounts is a listing of the names of the accounts that a company has identified and made available for recording transactions in its general ledger. A company has the flexibility to tailor its chart of accounts to best suit its needs, including adding accounts as needed.

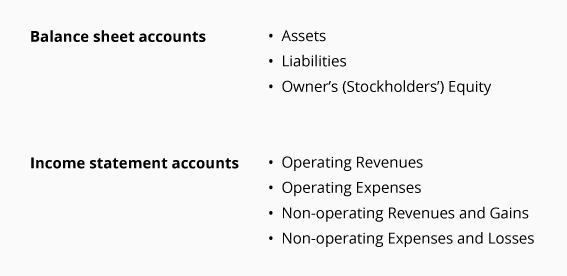

Within the chart of accounts you will find that the accounts are typically listed in the following order:

Within the categories of operating revenues and operating expenses, accounts might be further organized by business function (such as producing, selling, administrative, financing) and/or by company divisions, product lines, etc.

A company’s organization chart can serve as the outline for its accounting chart of accounts. For example, if a company divides its business into ten departments (production, marketing, human resources, etc.), each department will likely be accountable for its own expenses (salaries, supplies, phone, etc.). Each department will have its own phone expense account, its own salaries expense, etc.

A chart of accounts will likely be as large and as complex as the company itself. An international corporation with several divisions may need thousands of accounts, whereas a small local retailer may need as few as one hundred accounts.

WATCH NOWAdvance Your Career with Our PRO Training

Please let us know how we can improve this explanation

No Thanks

Close

Sample Chart of Accounts For a Large Corporation

Each account in the chart of accounts is typically assigned a name and a unique number by which it can be identified. (Software for some small businesses may not require account numbers.) Account numbers are often five or more digits in length with each digit representing a division of the company, the department, the type of account, etc.

As you will see, the first digit might signify if the account is an asset, liability, etc. For example, if the first digit is a “1” it is an asset. If the first digit is a “5” it is an operating expense.

A gap between account numbers allows for adding accounts in the future. The following is a partial listing of a sample chart of accounts.

Please let us know how we can improve this explanation

No Thanks

Close

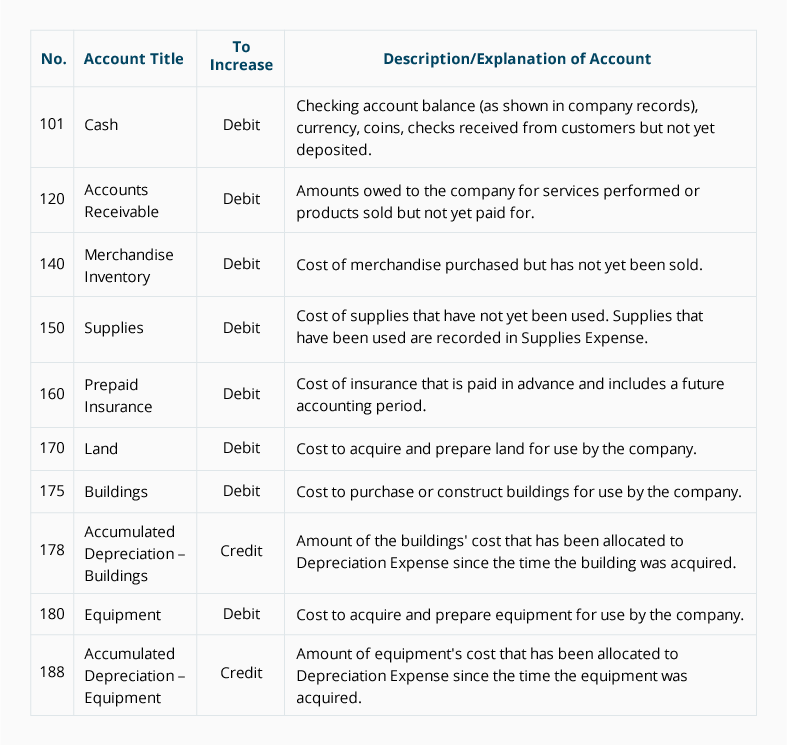

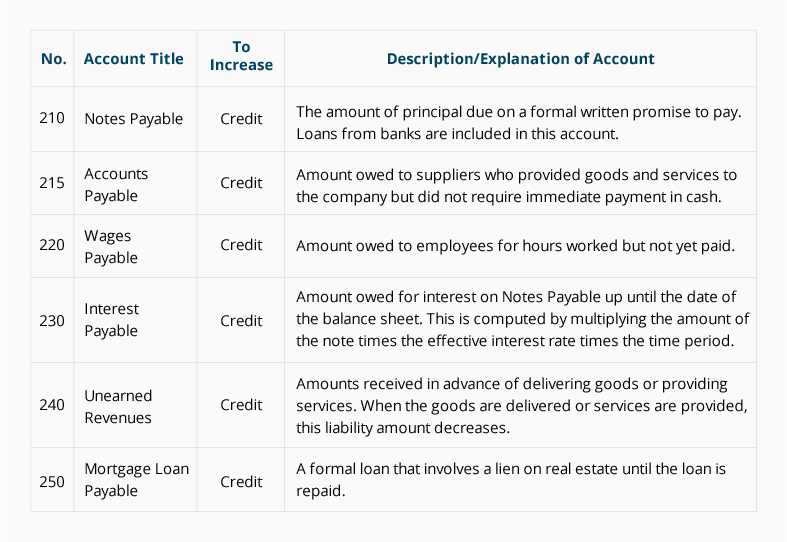

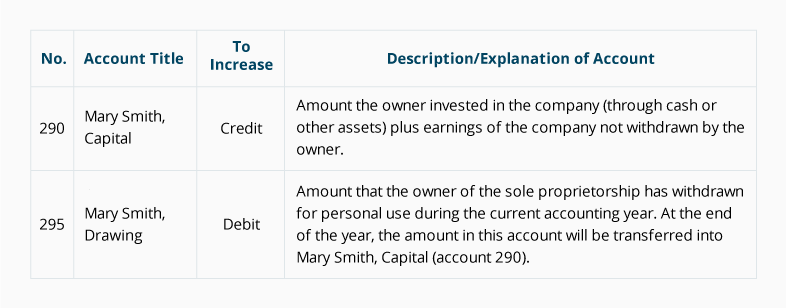

Sample Chart of Accounts for a Small Company

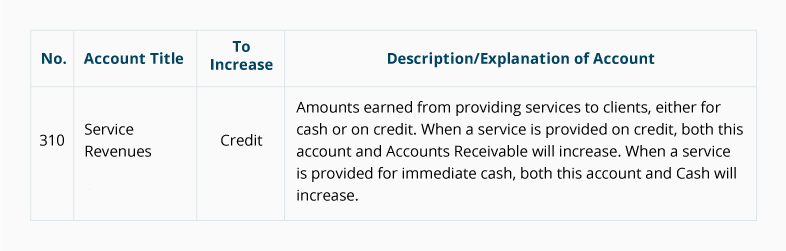

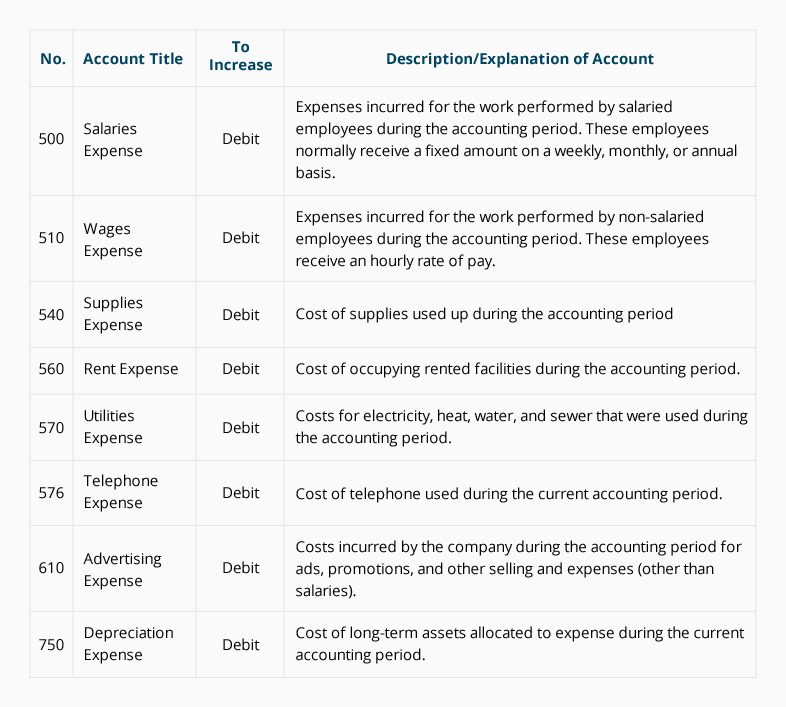

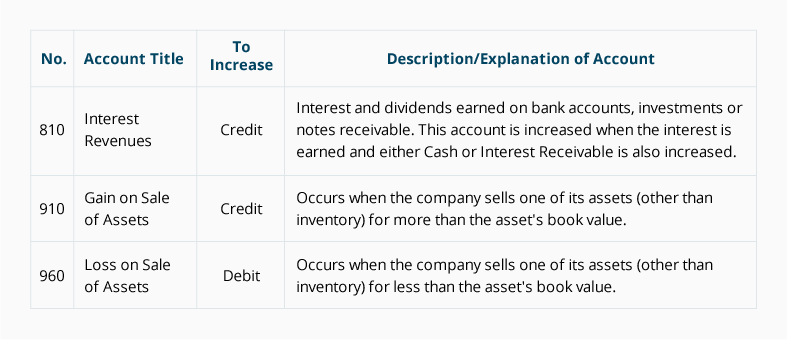

This is a partial listing of another sample chart of accounts. Note that each account is assigned a three-digit number followed by the account name. The first digit of the number signifies if it is an asset, liability, etc. For example, if the first digit is a “1” it is an asset, if the first digit is a “3” it is a revenue account, etc. The company decided to include a column to indicate whether a debit or credit will increase the amount in the account. This sample chart of accounts also includes a column containing a description of each account in order to assist in the selection of the most appropriate account.

Asset Accounts

Liability Accounts

Owner’s Equity Accounts

Operating Revenue Accounts

Operating Expense Accounts

Non-Operating Revenues and Expenses, Gains, and Losses

Accounting software frequently includes sample charts of accounts for various types of businesses. It is expected that a company will expand and/or modify these sample charts of accounts so that the specific needs of the company are met. Once a business is up and running and transactions are routinely being recorded, the company may add more accounts or delete accounts that are never used.

Please let us know how we can improve this explanation

No Thanks

Close

At Least Two Accounts for Every Transaction

The chart of accounts lists the accounts that are available for recording transactions. In keeping with the double-entry system of accounting, a minimum of two accounts is needed for every transaction—at least one account is debited and at least one account is credited.

When a transaction is entered into a company’s accounting software, it is common for the software to prompt for only one account name—this is because the software is programmed to automatically assign one of the accounts. For example, when using accounting software to write a check, the software automatically reduces the asset account Cash and prompts you to designate the other account(s) such as Rent Expense, Advertising Expense, etc.

Some general rules about debiting and crediting the accounts are:

Expense accounts are debited and have debit balances

Revenue accounts are credited and have credit balances

Asset accounts normally have debit balances

To increase an asset account, debit the account

To decrease an asset account, credit the account

Liability accounts normally have credit balances

To increase a liability account, credit the account

To decrease a liability account, debit the account

Note: To learn more about debits and credits, visit our Explanation and Quiz for this topic. To learn more about the role of bookkeepers and accountants, visit our Accounting Careers page.

Where to Go From Here

We recommend taking our Practice Quiz next, and then continuing with the rest of our Chart of Accounts materials (see the full outline below).

We also recommend joining PRO to unlock our premium materials (certificates of achievement, video training, flashcards, visual tutorials, quick tests, quick tests with coaching, cheat sheets, guides, puzzles, business forms, printable PDF files, progress tracking, badges, points, medal rankings, activity streaks, public profile pages, and more).

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.

Please let us know how we can improve this explanation

No Thanks

Close

A record in the general ledger that is used to collect and store similar information. For example, a company will have a Cash account in which every transaction involving cash is recorded. A company selling merchandise on credit will record these sales in a Sales account and in an Accounts Receivable account.

That part of the accounting system which contains the balance sheet and income statement accounts used for recording transactions.

Operating expenses are the costs of a company’s main operations that have been used up during the period indicated on the income statement. For example, a retailer’s operating expenses consist of its cost of goods sold and its selling, general and administrative expenses (SG&A).

A diagram depicting a company’s hierarchy or chain of command, its business segments, functions, and departments.

Costs that are matched with revenues on the income statement. For example, Cost of Goods Sold is an expense caused by Sales. Insurance Expense, Wages Expense, Advertising Expense, Interest Expense are expenses matched with the period of time in the heading of the income statement. Under the accrual basis of accounting, the matching is NOT based on the date that the expenses are paid.

Expenses associated with the main activity of the business are referred to as operating expenses. Expenses associated with a peripheral activity are nonoperating expenses or other expenses. For example, a retailer’s interest expense is a nonoperating expense. A bank’s interest expense is an operating expense.

Generally, expenses are debited to a specific expense account and the normal balance of an expense account is a debit balance. When an expense account is debited, the account credited might be Cash (if cash was paid at the time of the expense), Accounts Payable (if cash will be paid after the expense is recorded), or Prepaid Expense (if cash was paid before the expense was recorded.)

Things that are resources owned by a company and which have future economic value that can be measured and can be expressed in dollars. Examples include cash, investments, accounts receivable, inventory, supplies, land, buildings, equipment, and vehicles.

Assets are reported on the balance sheet usually at cost or lower. Assets are also part of the accounting equation: Assets = Liabilities + Owner’s (Stockholders’) Equity.

Some valuable items that cannot be measured and expressed in dollars include the company’s outstanding reputation, its customer base, the value of successful consumer brands, and its management team. As a result these items are not reported among the assets appearing on the balance sheet.

Obligations of a company or organization. Amounts owed to lenders and suppliers. Liabilities often have the word “payable” in the account title. Liabilities also include amounts received in advance for a future sale or for a future service to be performed.

Cash and other resources that are expected to turn to cash or to be used up within one year of the balance sheet date. (If a company’s operating cycle is longer than one year, an item is a current asset if it will turn to cash or be used up within the operating cycle.) Current assets are presented in the order of liquidity, i.e., cash, temporary investments, accounts receivable, inventory, supplies, prepaid insurance.

A current asset account that represents an amount of cash for making small disbursements for postage due, supplies, etc.

A current asset resulting from selling goods or services on credit (on account). Invoice terms such as (a) net 30 days or (b) 2/10, n/30 signify that a sale was made on account and was not a cash sale.

Allowance for Doubtful Accounts is a contra current asset account associated with Accounts Receivable. When the credit balance of the Allowance for Doubtful Accounts is subtracted from the debit balance in Accounts Receivable the result is known as the net realizable value of the Accounts Receivable.

The credit balance in this account comes from the entry wherein Bad Debts Expense is debited. The amount in this entry may be a percentage of sales or it might be based on an aging analysis of the accounts receivables (also referred to as a percentage of receivables).

When the allowance account is used, the company is anticipating that some accounts will be uncollectible in advance of knowing the specific account. As a result the bad debts expense is more closely matched to the sale. When a specific account is identified as uncollectible, the Allowance for Doubtful Accounts should be debited and Accounts Receivable should be credited.

A current asset whose ending balance should report the cost of a merchandiser’s products awaiting to be sold. The inventory of a manufacturer should report the cost of its raw materials, work-in-process, and finished goods. The cost of inventory should include all costs necessary to acquire the items and to get them ready for sale.

When inventory items are acquired or produced at varying costs, the company will need to make an assumption on how to flow the changing costs. See cost flow assumption.

If the net realizable value of the inventory is less than the actual cost of the inventory, it is often necessary to reduce the inventory amount.

A current asset which indicates the cost of the insurance contract (premiums) that have been paid in advance. It represents the amount that has been paid but has not yet expired as of the balance sheet date.

A related account is Insurance Expense, which appears on the income statement. The amount in the Insurance Expense account should report the amount of insurance expense expiring during the period indicated in the heading of the income statement.

Obligations due within one year of the balance sheet date. (If a company’s operating cycle is longer than one year, an item is a current liability if it is due within the operating cycle.) Another condition is that the item will use cash or it will create another current liability. (This means that if a bond payable is due within one year of the balance sheet date, but the bond will be retired by a bond sinking fund (a long-term restricted asset) the bond will not be reported as a current liability.)

The amount of principal due on a formal written promise to pay. Loans from banks are included in this account.

This current liability account will show the amount a company owes for items or services purchased on credit and for which there was not a promissory note. This account is often referred to as trade payables (as opposed to notes payable, interest payable, etc.)

A current liability account that reports the amounts owed to employees for hours worked but not yet paid as of the date of the balance sheet.

This current liability account reports the amount of interest the company owes as of the date of the balance sheet. (Future interest is not recorded as a liability.)

A loan having the security of a lien on the borrower’s real estate.

Generally a long term liability account containing the face amount, par amount, or maturity amount of the bonds issued by a company that are outstanding as of the balance sheet date.

A contra liability account that reports the amount of unamortized discount associated with bonds that are outstanding. The discount on bonds payable originates when bonds are issued for less than the bond’s face or maturity amount. The debit balance in this account will be amortized to bond interest expense over the life of the bonds and results in more interest expense than interest paid.

The type of stock that is present at every corporation. (Some corporations have preferred stock in addition to their common stock.) Shares of common stock provide evidence of ownership in a corporation. Holders of common stock elect the corporation’s directors and share in the distribution of profits of the company via dividends. If the corporation were to liquidate, the secured lenders would be paid first, followed by unsecured lenders, preferred stockholders (if any), and lastly the common stockholders.

Generally speaking, retained earnings is a stockholders’ equity account that reports the net income of a corporation from its inception until the balance sheet date less the dividends declared from its inception to the date of the balance sheet.

A corporation’s own stock that has been repurchased from stockholders. Also a stockholders’ equity account that usually reports the cost of the stock that has been repurchased.

A revenue account that reports the sales of merchandise. Sales are reported in the accounting period in which title to the merchandise was transferred from the seller to the buyer.

Cost of goods sold is usually the largest expense on the income statement of a company selling products or goods. Cost of Goods Sold is a general ledger account under the perpetual inventory system.

Under the periodic inventory system there will not be an account entitled Cost of Goods Sold. Instead, the cost of goods sold is computed as follows: cost of beginning inventory + cost of goods purchased (net of any returns or allowances) + freight-in – cost of ending inventory.

This account balance or this calculated amount will be matched with the sales amount on the income statement.

The accounting term that means an entry will be made on the left side of an account.

The 500 year-old accounting system where every transaction is recorded into at least two accounts. To learn more, see Explanation of Debits and Credits.

A current asset account which includes currency, coins, checking accounts, and undeposited checks received from customers. The amounts must be unrestricted. (Restricted cash should be recorded in a different account.)

Under the accrual basis of accounting, the account Rent Expense will report the cost of occupying space during the time interval indicated in the heading of the income statement, whether or not the rent was paid within that period. (Rent that has been paid in advance is shown on the balance sheet in the current asset account Prepaid Rent.) Depending upon the use of the space, Rent Expense could appear on the income statement as part of administrative expenses or selling expenses. If the rented space was used to manufacture goods, the rent would be part of the cost of the products produced.

Advertising Expense is the income statement account which reports the dollar amount of ads run during the period shown in the income statement. Advertising Expense will be reported under selling expenses on the income statement.

For the past 52 years, Harold Averkamp (CPA, MBA) has

worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.