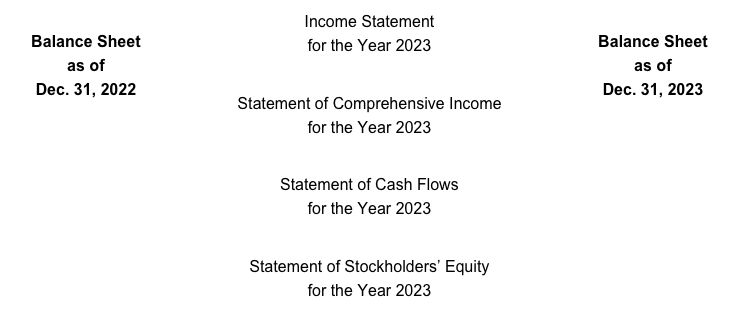

The balance sheet is the only one of the five main financial statements that reports amounts as of a moment or point in time. The income statement, statement of comprehensive income, statement of cash flows, and statement of stockholders’ equity all report amounts for a period of time.

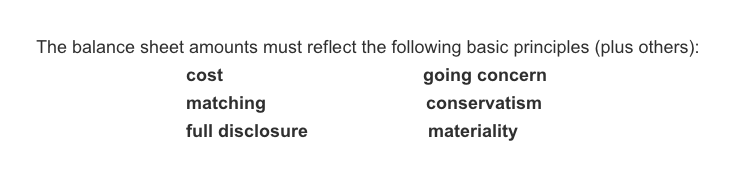

The balance sheet must be prepared according to generally accepted accounting principles (referred to as GAAP or US GAAP). These include very complex, detailed rules and also some basic underlying principles, guidelines, and concepts such as the cost principle, matching principle, full disclosure principle, going concern assumption, conservatism, materiality, objectivity, and others.

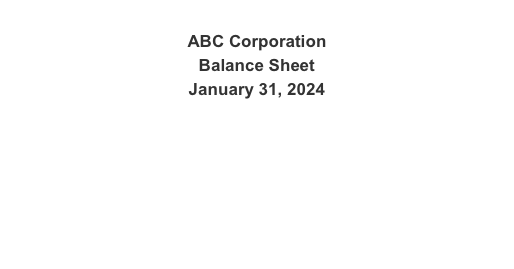

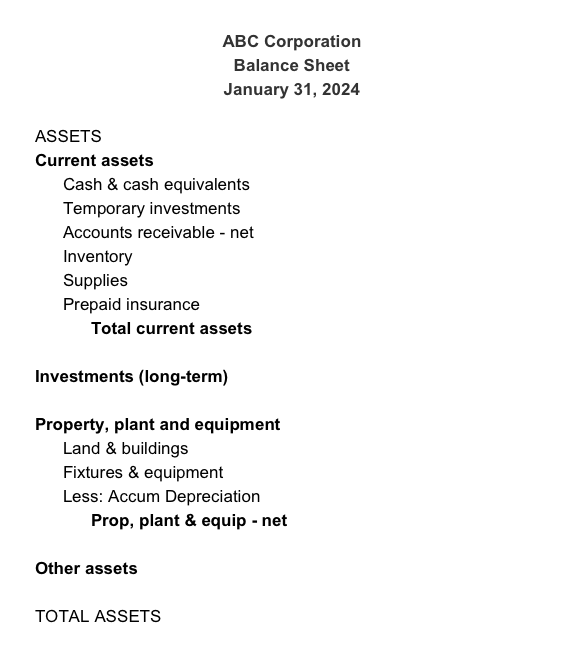

The heading of the balance sheet will include the company’s name, the words “balance sheet” and a date.

The date represents a moment or point in time such as the last instant in an accounting period. We are accustomed to seeing balance sheets with dates such as December 31, March 31, June 30, etc. However, a balance sheet can have any date. Here’s an example of a heading:

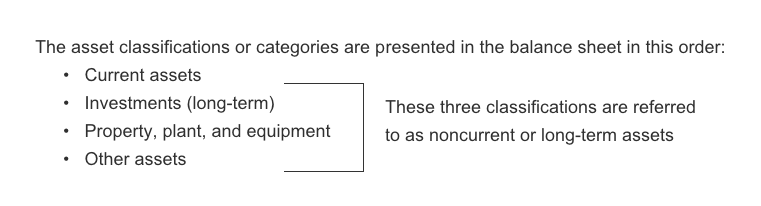

Assets are usually presented on the balance sheet according to the following classifications:

- Current assets

- Investments (long-term)

- Property, plant and equipment

- Other assets

Here is a listing of the assets often reported on a balance sheet:

Since the retained earnings portion of stockholders’ equity is increased by the corporation’s earnings, much of the change occurring during the accounting period can be found on the income statement.

The change in retained earnings during the most recent accounting period is partially explained by the corporation’s income statement which reports its revenues, expenses, gains, and losses.

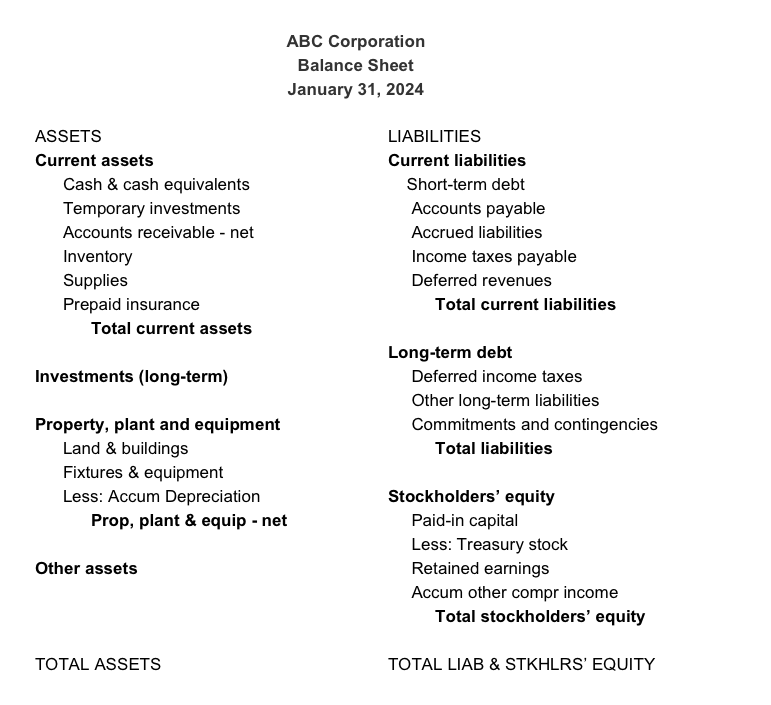

Below is a more complete balance sheet:

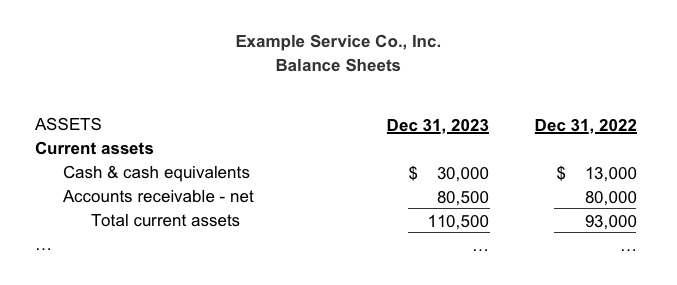

In order for the balance sheet to be more useful, accountants should prepare comparative balance sheets. Comparative balance sheets report the amounts for two dates as shown in the partial sample balance sheet below:

Turn on study mode to focus

Balance Sheet Outline

- Read our Explanation (8 Parts) Free

- Take our Practice Quiz Free

- Review our Visual Tutorial

- Watch our Financial Statements Video Training

- Review our Flashcards

- Solve our Word Scramble Free

- Solve our Crossword Puzzle #1 Free

- Solve our Crossword Puzzle #2 Free

- Review our Sample Business Forms

- Review our Cheat Sheet

- Take our Quick Test #1

- Take our Quick Test #2 with Coaching

- Earn our Balance Sheet Certificate of Achievement

Learn How to Advance Your Accounting and Bookkeeping Career

- Perform better at your current job

- Refresh your skills to re-enter the workforce

- Pass your accounting class

- Understand your small business finances

Featured Review

"AccountingCoach saved my job. I have had bookkeeping jobs on and off for the past ten years but never any formal training. I recently accepted a position and it was evident to me after the first day that I was way out of my league. Because of how AccountingCoach is structured, I was able to study at a fast pace and get the info I needed to be more productive at work. Thank you for presenting the information in such a basic, uncomplicated way." - Tammy Y.