Bonds

Bonds are a form of long-term debt for the issuer. (For the buyer of the bonds, the bonds are an investment.)

Bonds Payable

As part of the entry to record the issuance of bonds, the issuer will record the face value of the bonds in a long-term (or noncurrent) liability account entitled Bonds Payable.

Typically the issuer of the bonds agrees to pay the bondholders:

- interest every six months (semiannually), and

- the face or maturity value when the bonds come due

Why Bonds? Why Not Common Stock?

Bonds are different from common stock in that usually:

- the issuer of the bonds does not give the bondholders any ownership interest

- semiannual interest payments must be made when due

- the maturity amount must be paid when the bonds come due

- the issuer’s interest expense qualifies as an income tax deduction (whereas dividends are not tax deductible)

As a result of the above features, the money raised from issuing bonds will be less costly than the money raised from issuing shares of common stock.

Face Value of Bonds

The amount appearing on the face of the bonds is also known as the following:

- face value

- par value

- principal amount

- stated value

- maturity value

Interest Rate on Bonds

The interest rate shown on the face of the bonds is the annual interest rate that will be used to determine the semiannual interest payments. This interest rate is also known as:

- face interest rate

- stated interest rate

- contractual interest rate

- nominal interest rate

- coupon interest rate

Typically the stated interest rate will not change and is therefore considered to be a fixed rate. This will result in the semiannual interest payments being the same amount. The formula for the semiannual interest payments is: face interest rate X face value of the bond X 6/12 of a year.

Market Interest Rates

We stated that the bonds’ semiannual interest payments and maturity value are both fixed in amount. However, the market interest rates for similar bonds are likely to change daily due to events occurring throughout the world. The market interest rate is also known as:

- effective interest rate

- yield-to-maturity

- discount interest rate

- desired interest rate

Market Interest Rates and the Value of Existing Bonds

When market interest rates decrease, the value of existing bonds will increase. The reason is the fixed amounts of the cash payments (interest and maturity value) will become more attractive and therefore more valuable.

When market interest rates increase, the value of existing bonds will decrease. The reason is the fixed cash payments for interest and maturity value have now become less attractive and therefore less valuable.

To recap, the market value of existing bonds will move in the opposite direction of the change in the market interest rates.

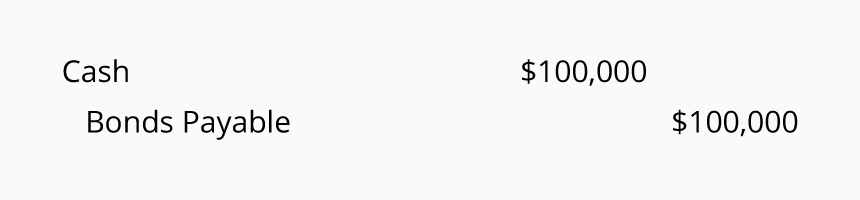

Bonds Sold at Par Value

When a corporation offers bonds having a stated interest rate of say 8% and the market interest rate for similar bonds is 8%, the bonds will sell at their par or maturity value. Bonds selling at their par value are said to be sold at 100, which means 100% of the bonds par value. Therefore, a $100,000 bond will sell for $100,000 and will be recorded as follows:

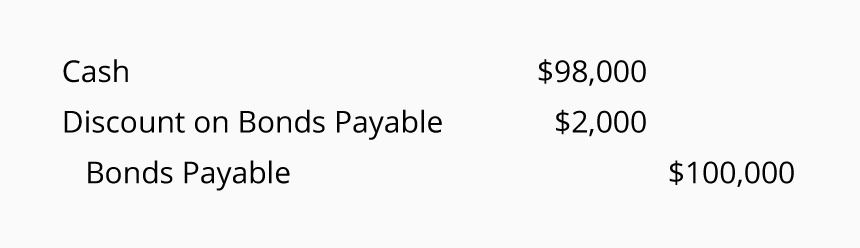

Bonds Sold at a Discount

If bonds having a stated interest rate of 8% are offered on a day when the market interest rate is 8.2%, the bonds will sell for less than their par or maturity value. Perhaps the bonds will sell for 98 or 98% of face value. This means that a $100,000 bond will sell for $98,000. Assuming there is no accrued interest on the date the bond is issued, the journal entry for the issuance of the bond will be:

Discount on Bonds Payable is a contra-liability account which is always presented on the balance sheet with Bonds Payable. The combination of these two account balances means the book value or the carrying value of the bonds payable is $98,000 ($100,000 minus $2,000). Over the life of the bonds, the discount on bonds payable must be amortized to interest expense.

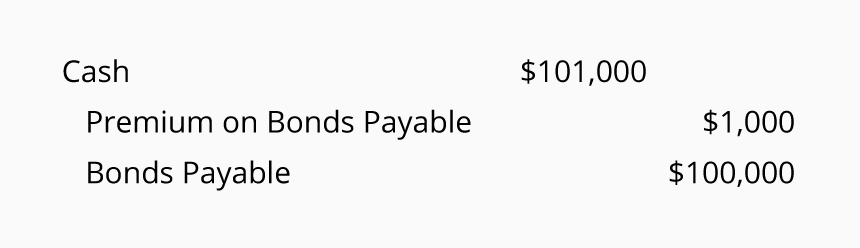

Bonds Sold at a Premium

If bonds having a stated interest rate of 8% are issued on a day when the market interest rate is 7.9%, the bonds will sell for more than the par value or maturity value of the bonds. Perhaps the bonds will sell for 101 or 101% of face value. Therefore, a $100,000 bond will sell for $101,000. Assuming there is no accrued interest on the date the bond is issued, the journal entry for the issuance of the bond will be:

Premium on Bonds Payable is an adjunct liability account which is always presented with Bonds Payable. The combination of these two account balances means the book value or the carrying value of the bonds payable is $101,000 ($100,000 plus $1,000). Over the life of the bonds, the premium on bonds payable must be amortized to interest expense.

Straight-line Amortization of Discount or Premium

If the amount of the discount or the premium on bonds payable is not significant, the corporation may amortize the discount or premium using the straight-line method of amortization. This means that each accounting period during the life of the bonds the same amount of discount or premium will move from the balance sheet to interest expense.

Effective Interest Rate Method of Amortizing Discount or Premium

If the amount of the discount or the premium is significant, the initial amount of the discount or premium should be reduced by using the effective interest rate method of amortization. Under this method the market interest rate on the date that the bonds were issued is multiplied times the book value (carrying value) of the bonds at the start of each six-month period. The resulting amount is the amount debited to Interest Expense for the six-month period. The difference between the interest expense and the actual interest payment is the amount of the Discount or Premium that is being amortized in the current period.

Accrued Interest on Bonds Payable

Since most bonds pay interest semiannually, the issuer of the bonds will have accrued interest expense and accrued interest payable if the bonds are outstanding on any of the other 363 days of the year.

To illustrate, assume that on June 1 a corporation issued $3,000,000 of bonds with a stated interest rate of 6% (and the market interest rate is also 6%), the corporation will be incurring interest expense of $180,000 per year; $15,000 per month; $500 per day. Also assume that the corporation prepares monthly financial statements. This means that on June 30 (and on the last day of every month), the corporation must record an adjusting entry to debit Accrued Interest Expense for $15,000 and credit Accrued Interest Liability for $15,000. When the corporation makes its December 1 interest payment of $90,000 the balance in Accrued Interest Liability will be $0 for that day.