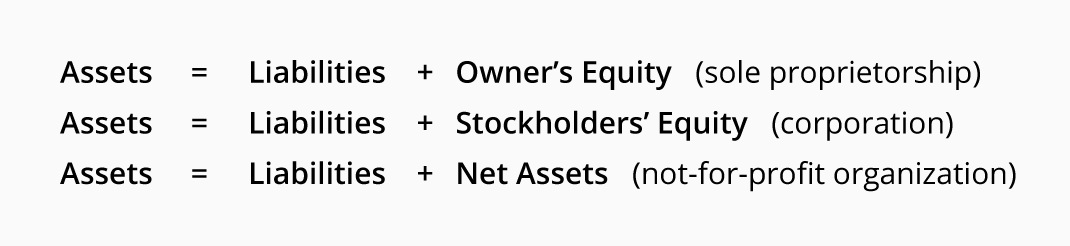

Basic Accounting Equation

In accounting (and bookkeeping) the basic accounting equation is:

Thanks to double-entry accounting (or double-entry bookkeeping) the basic accounting equation will/ must always be in balance. We will demonstrate the double-entry accounting and the accounting equation with eight examples.

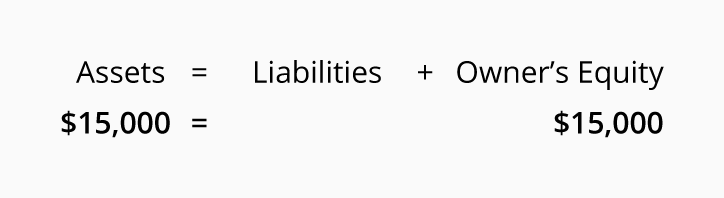

Effect of Owner Investing in a Business

For example, if a person starts a sole proprietorship with $15,000 the accounting equation will show:

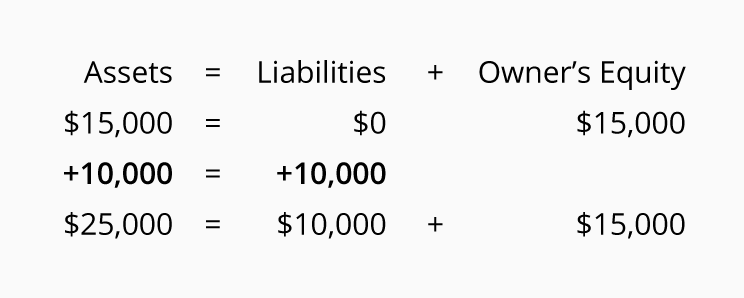

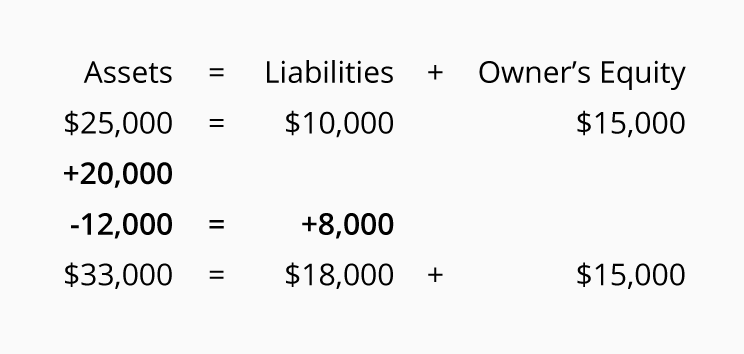

Effect of Business Borrowing Money

Next, let’s assume that the company borrows $10,000 from its bank. This will cause the asset Cash to increase by $10,000 and it will cause the liability Notes Payable or Loans Payable to increase by $10,000. The accounting equation remains in balance because both sides of the equation increased by $10,000:

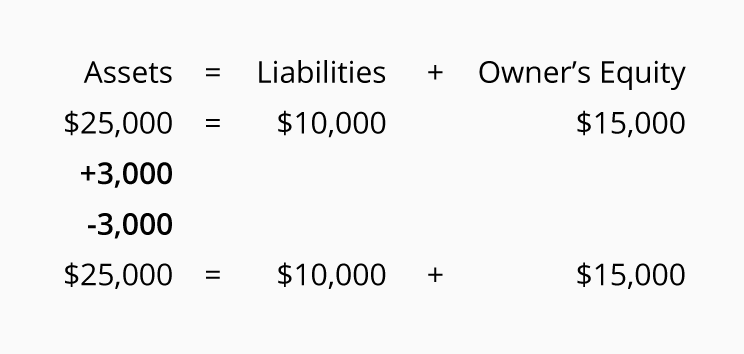

Purchase of Office Furniture for Cash

If the company pays Cash of $3,000 for new office furniture, the transaction will cause the asset Office Furniture to increase by $3,000 and the asset Cash to decrease by $3,000. Note that the total amount of assets (shown on the left side of the equation) does not change since there was both an increase and a decrease of $3,000 on the left side of the accounting equation:

Purchase of New Machine with Cash and a Loan.

The company buys a new machine for $20,000 by paying $12,000 in cash and signing a promissory note for the remaining $8,000. This transaction causes the asset Machinery to increase by $20,000 and causes the asset Cash to decrease by $12,000 and the liabilities to increase by $8,000:

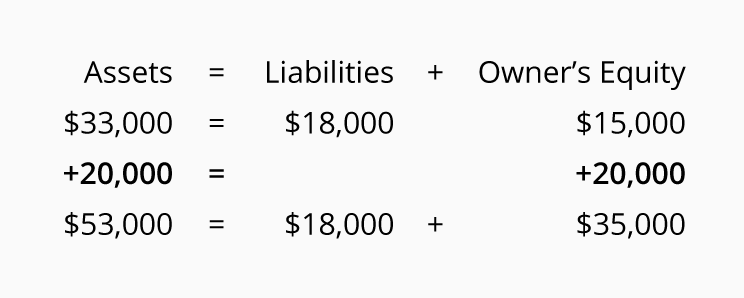

Owner Invests Additional Money in Business

Owner’s equity (on the right side of the accounting equation) is affected by several types of transactions. First, owner’s equity increases when the business owner invests personal cash or other assets into the business. For example, if M. Jones invests $20,000 of cash in her business, the company’s asset Cash increases by $20,000 and the owner’s equity account M. Jones, Capital increases by $20,000. The accounting equation continues to be in balance because each side of the equation increased by $20,000:

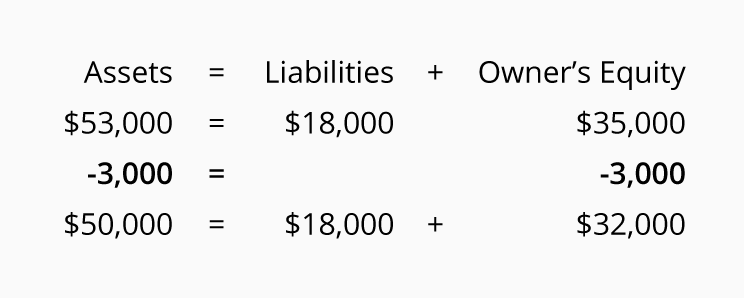

Owner Withdraws Money for Personal Use

Owner’s equity will decrease when the owner withdraws business assets for personal use. To illustrate, let’s assume the owner draws (or withdraws) $3,000 of the business asset Cash for personal use. The result is that assets decrease by $3,000 and the owner’s equity decreases by $3,000. Again, the accounting equation remains in balance.

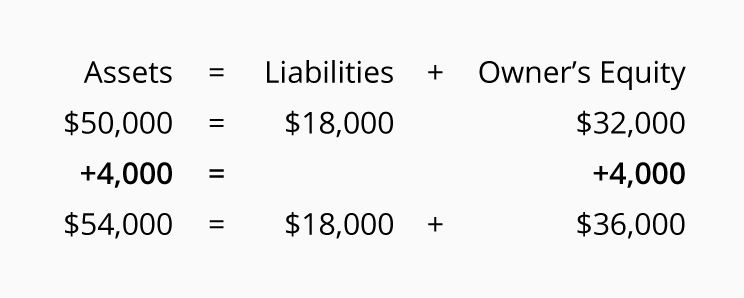

Revenues Increase Owner’s Equity and Usually Assets

Owner’s equity also increases when a company earns revenues. Under the accrual method of accounting, revenues will increase owner’s equity and will usually increase an asset when the revenues are earned (as opposed to waiting until the client’s cash is received). For example, if the company earns fees of $4,000 and allows the client to pay in 30 days, the company’s asset Accounts Receivable increases by $4,000 and owner’s equity increases by $4,000. Since both sides of the accounting equation increase by $4,000, the accounting equation remains in balance:

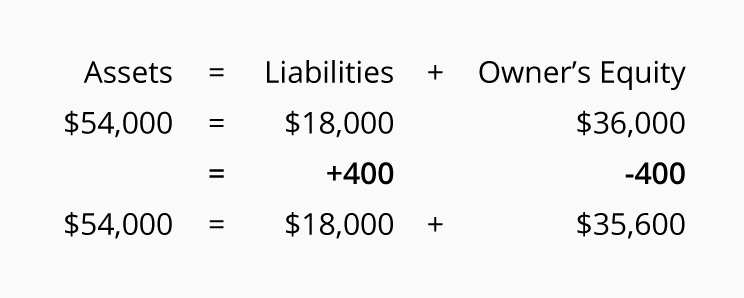

Expenses Decrease Owner’s Equity and Affects Another Account

Owner’s equity will decrease when a company incurs expenses. Under the accrual method of accounting, an expense is recorded when the expense occurs (as opposed to the time of payment). Assume that a company incurs electricity expense of $400 in December that will be paid in January. In December the company must report a decrease in owner’s equity of $400 (because of the electricity expense) and an increase of $400 in its liabilities:

Additional Information on the Accounting Equation

As you may have noticed, the accounting equation is similar to the balance sheet (or statement of financial position) which is one of the main financial statements.

The accounting equation also provides insight into the link between the balance sheet and the income statement. For instance, the balances in the income statement accounts will be the net income or net loss that will be transferred to the owner’s capital account at the end of the year.

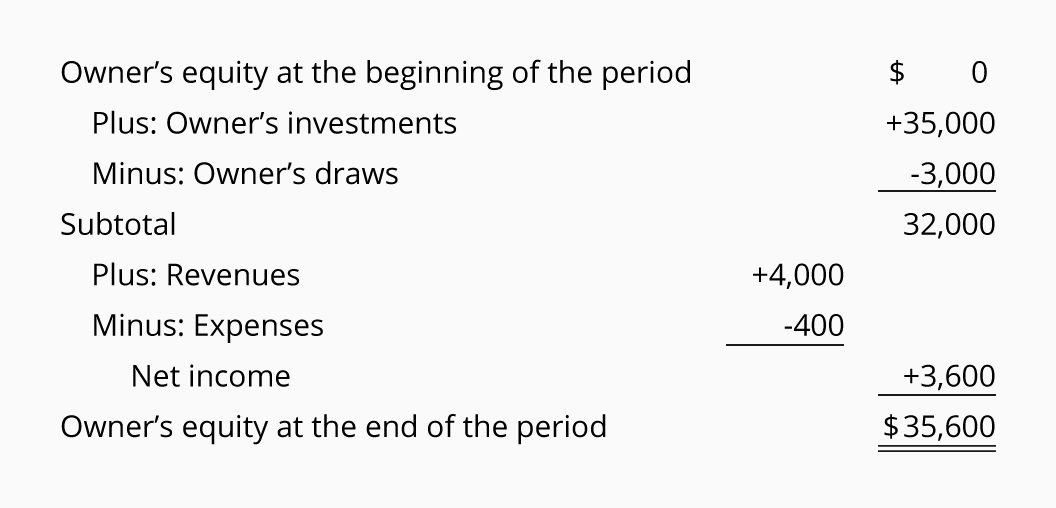

Summary of Effects on Owner’s Equity

The following table shows the changes in owner’s equity as a result of our eight examples:

Note: While the owner’s investments and the owner’s draws cause owner’s equity to change, they are NOT part of the company’s net income. Hence, they are not reported on the company’s income statement.