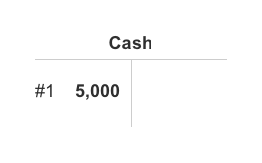

Here’s an example. If Amy Loy invests $5,000 of her personal cash in her new sole proprietorship Loy Company, this transaction will involve the business asset Cash and the owner’s equity account Amy Loy, Capital.

The format of accounts will vary with each company’s software. Here’s one example:

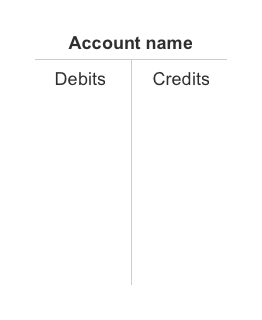

For learning our debits and credits, we will use the format known as a T-account:

Since each transaction will involve a minimum of two accounts, we will present two T-accounts when discussing each transaction.

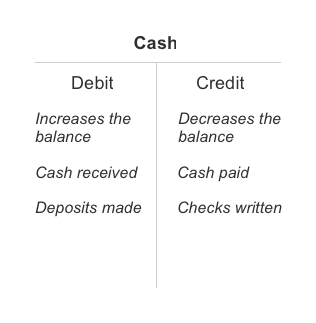

Here’s a picture of the T-account for Cash:

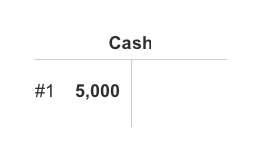

Transaction #1.

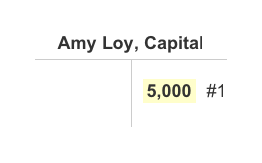

Let’s revisit our earlier example where Amy Loy invested $5,000 of her personal cash in her new sole proprietorship, Loy Company. Since the company is receiving cash of $5,000, the asset Cash will have to be debited, and a second account will have to be credited for $5,000.

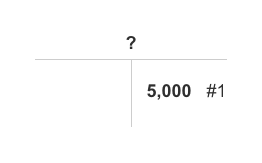

The next step is to identify the name of the account that is to be credited. In this example, the account to be credited is Amy Loy, Capital:

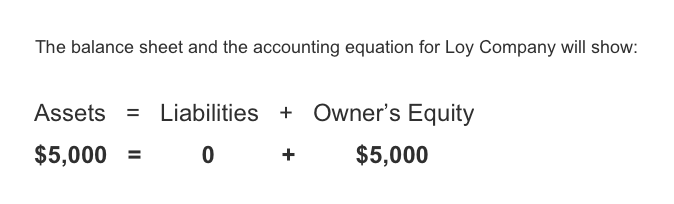

From these T-accounts we see that the owner’s equity account Amy Loy, Capital was credited in order to increase its balance from zero to $5,000. This is also consistent with the accounting equation which shows owner’s equity on the right side:

Assets = Liabilities + Owner’s Equity

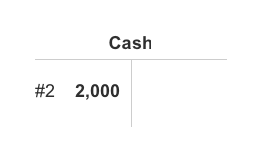

Transaction #2.

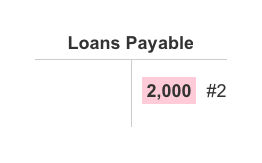

Let’s assume that Loy Company also borrows $2,000 and the amount is deposited into its checking account. The two accounts involved are Cash and Loans Payable. Loans Payable is a liability account and is increased with a credit entry as shown here:

Notice that Loans Payable has its balance on the right side, or credit side, similar to the position of liabilities in the accounting equation.

Assets = Liabilities + Owner’s Equity

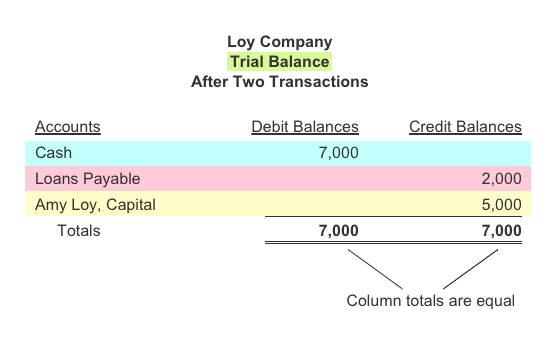

In addition to every transaction having debits equal to credits, the balances in the general ledger accounts must have the total of the debit balances equal to the total of the credit balances. A trial balance is a listing of all of the account balances in the general ledger and the total of each of the columns of amounts. The column totals must be equal.

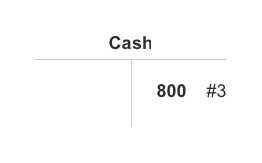

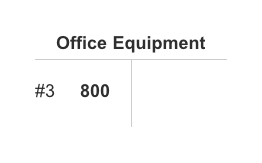

Transaction #3.

Let’s assume that the third transaction involves paying $800 for a computer. As we know, when cash is paid (or a check is written) the Cash account is credited. The second account will need to have a debit of $800. In this example, the second account is the asset Office Equipment. Here’s the entry in T-account format.

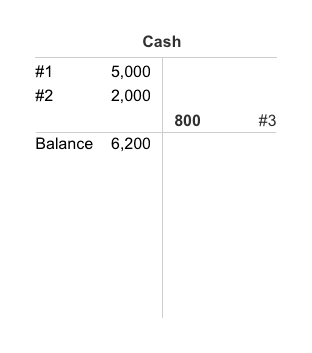

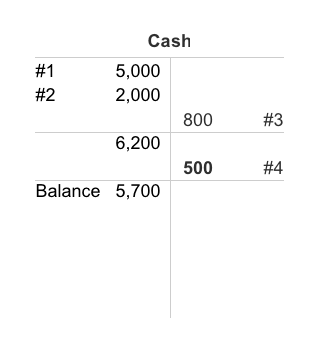

If we look into the Cash account, we will see the following activity and the resulting debit balance of $6,200:

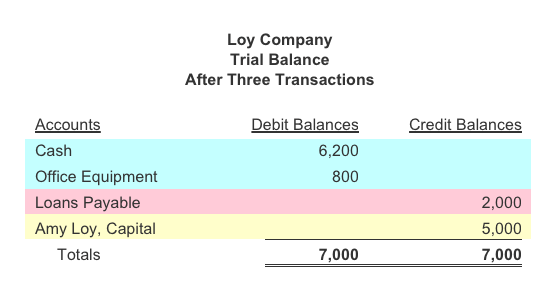

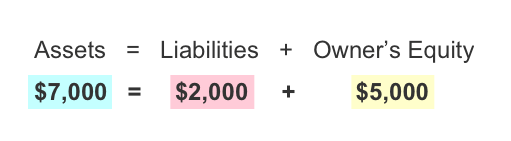

The trial balance after the third transaction will report the following amounts:

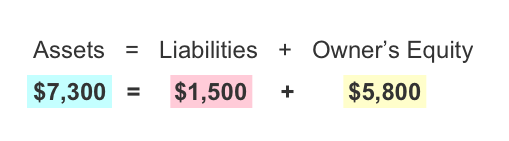

The balance sheet and the accounting equation for Loy Company after the third transaction will report the following totals:

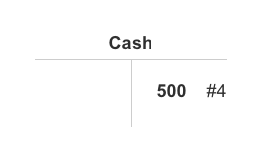

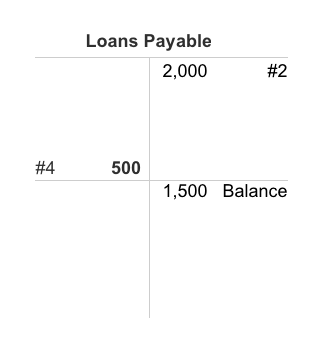

Transaction #4.

Let’s assume that Loy Company is going to repay $500 of its loan. In other words, Loy will reduce its asset Cash and will reduce its liability Loans Payable. Recall that Cash and other assets will be reduced with a credit. To reduce the credit balance in a liability account such as Loans Payable, a debit must be entered into the liability account. In T-account format, here is Loy Company’s entry to repay $500 of its loan:

Here are the two accounts showing all of the activity and their balances after the $500 payment is recorded:

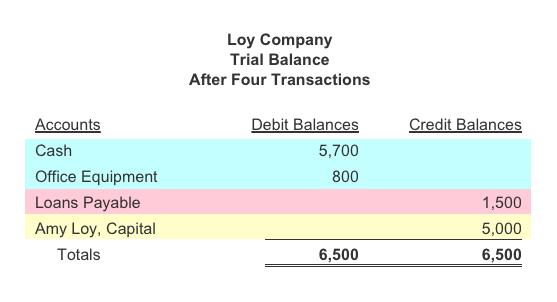

The trial balance after the fourth transaction will report the following amounts:

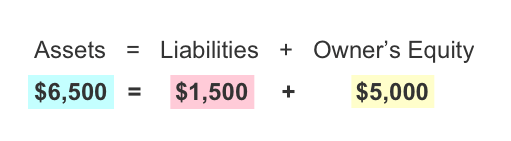

The balance sheet and the accounting equation for Loy Company after the fourth transaction will report the following:

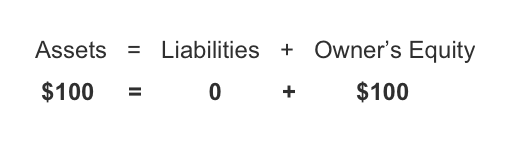

Revenues are recorded in temporary revenue accounts and the amounts will be reported on the income statement. The revenue accounts are temporary because the amounts are stored there only temporarily. Later they will be transferred to the owner’s equity account. This means that revenues will be reported on the income statement and will also increase owner’s equity and assets. For example, if a sole proprietorship performs a service for $100, the accounting equation will change as follows:

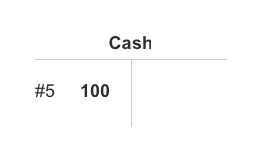

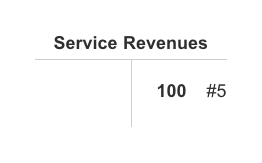

Transaction #5.

On June 4, Loy Company delivers services at the agreed-upon amount of $100 and the customer pays cash for the services. The two accounts involved are the balance sheet asset account Cash and the income statement account Service Revenues. Since the asset Cash is increasing, we need to debit Cash for $100. This means that the other account, Service Revenues, will need to be credited. A credit to Service Revenues is logical because revenues cause the owner’s equity to increase. (Recall that owner’s equity is on the right side, or credit side, of the accounting equation.)

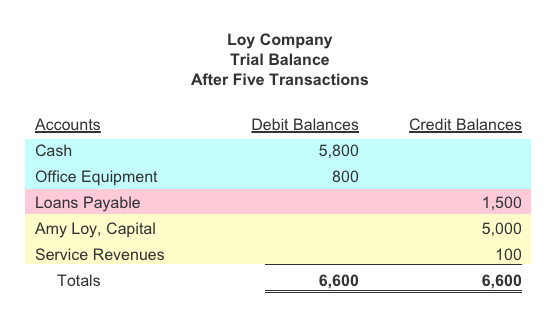

The trial balance after the fifth transaction will report the following amounts:

Notice that the temporary account Service Revenues is shown below the owner’s equity account Amy Loy, Capital. The Service Revenues account is used to keep a separate record of the revenues for the year. Once the year is completed, the amounts in the revenue accounts will be transferred to Amy Loy, Capital.

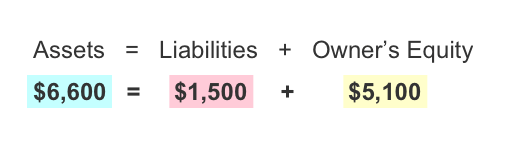

In terms of the accounting equation and the balance sheet, the amounts after five transactions are:

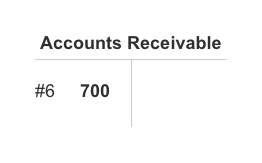

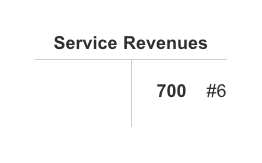

Transaction #6.

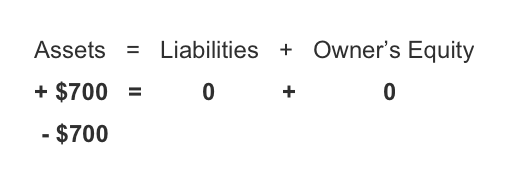

On June 10, Loy Company delivers $700 of services and allows the customer to pay in 30 days. The two accounts involved are the asset account Accounts Receivable and the temporary income statement account Service Revenues. Here is the transaction to be recorded on June 10:

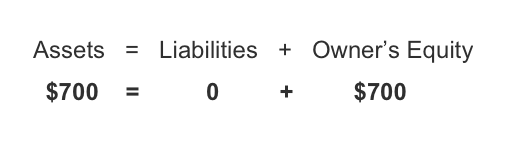

The effect of the June 10 transaction on the balance sheet and the accounting equation is:

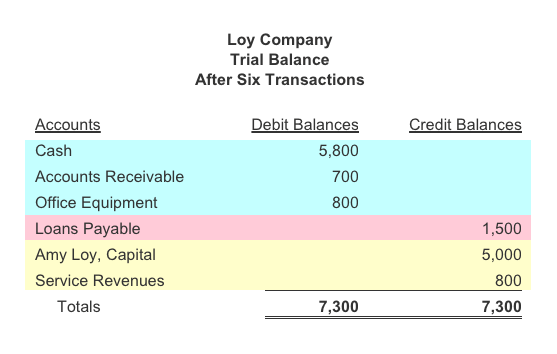

The trial balance after the sixth transaction will report the following amounts:

In terms of the accounting equation and the balance sheet, the amounts after six transactions are:

Expenses are recorded in temporary accounts and those amounts will be reported on the income statement. The expense accounts are temporary because their amounts will be transferred to the owner’s equity account after the year ends. This means that expenses will be reported not only on the income statement but will decrease owner’s equity and will either decrease assets or will increase liabilities, which are reported on the balance sheet.

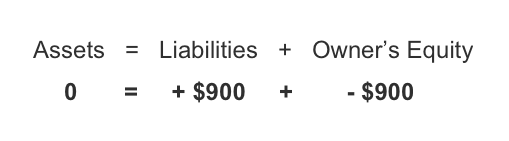

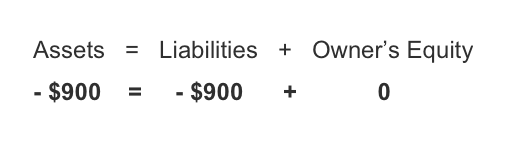

Expenses are debited, because they cause a decrease in owner’s equity, which is expected to have a credit balance. (Recall that owner’s equity is on the right or credit side of the accounting equation.) If we assume that a $900 expense occurs and the company has 20 days in which to pay the supplier, the balance sheet and accounting equation are affected as follows:

The liabilities increase because the company will have an obligation to pay the supplier or vendor.

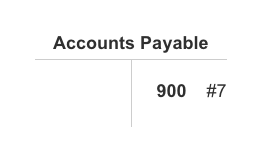

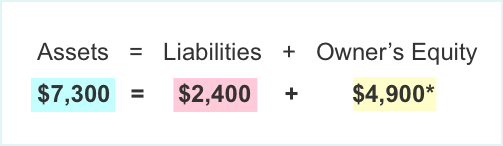

Transaction #7.

On June 25 and 26, Loy Company runs ads on the local radio station and will have to pay by July 10. The cost of the ads is $900. Since accountants cannot measure the future benefit of ads, the entire $900 must be expensed in June. Here is the accounting entry in T-account format.

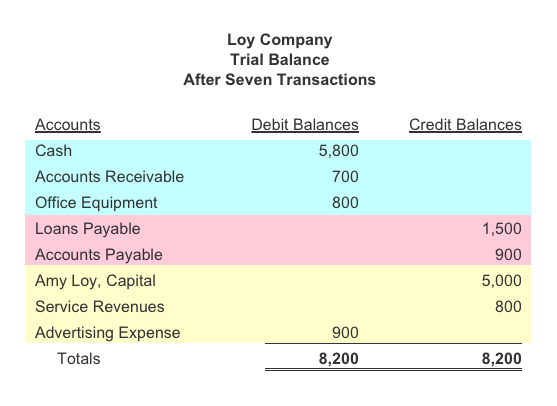

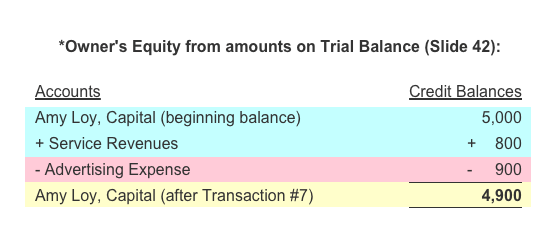

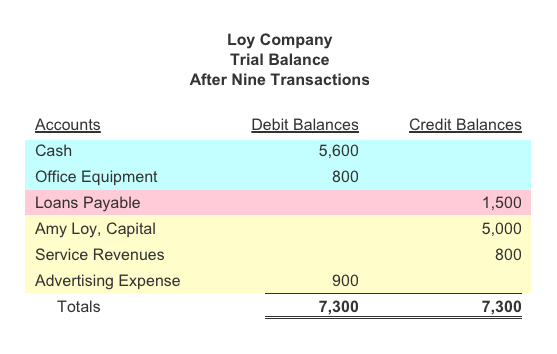

After Transaction #7, the trial balance will report the following amounts:

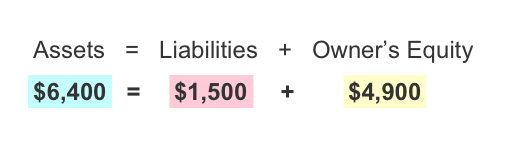

In terms of the accounting equation and the balance sheet, the amounts after seven transactions are:

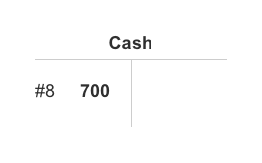

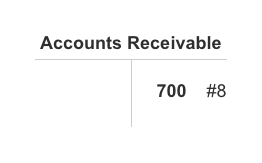

Transaction #8.

On July 9, Loy Company receives $700 from its customer who had received services on credit on June 10. (See Transaction #6.) The July 9 transaction in T-account format is:

In terms of the accounting equation and balance sheet, the transaction has the following effect:

The above equation reflects that one asset Cash increased by $700, while another asset Accounts Receivable decreased by $700.

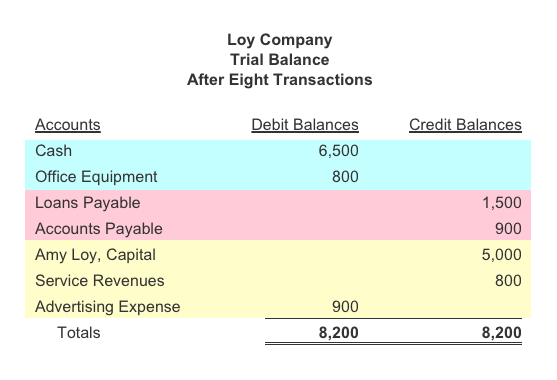

After Transaction #8, the trial balance will report the following amounts:

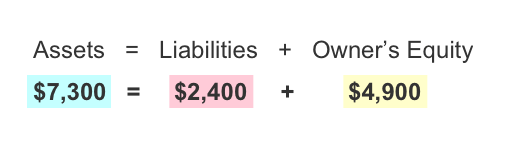

In terms of the accounting equation and the balance sheet, the totals after eight transactions are the same as they were after seven transactions:

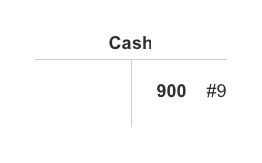

Transaction #9.

On July 10, Loy Company pays $900 for the ads described in Transaction #7. The July 10 payment in T-account format is:

In terms of the accounting equation and balance sheet, the transaction has the following effect:

After Transaction #9, the trial balance will report the following amounts:

The totals in the accounting equation and the balance sheet after the ninth transaction are:

Turn on study mode to focus

Debits and Credits Outline

- Read our Explanation (4 Parts) Free

- Read our Additional Explanation (3 Parts) Free

- Take our Practice Quiz Free

- Review our Visual Tutorial

- Watch our Bookkeeping Video Training

- Review our Flashcards

- Solve our Word Scramble Free

- Solve our Crossword Puzzle #1 Free

- Solve our Crossword Puzzle #2 Free

- Solve our Crossword Puzzle #3 Free

- Review our Cheat Sheet

- Take our Quick Test #1

- Take our Quick Test #2

- Take our Quick Test #3

- Take our Quick Test #4 with Coaching

- Earn our Debits and Credits Certificate of Achievement

Learn How to Advance Your Accounting and Bookkeeping Career

- Perform better at your current job

- Refresh your skills to re-enter the workforce

- Pass your accounting class

- Understand your small business finances

Featured Review

"I can't believe how much more confidence AccountingCoach PRO has given me, and I never want to be without it! I received my degree in accounting, but still found that I had questions, and did not feel confident in my abilities to perform in my new position as an accountant in a small contract manufacturing company. Because of this, I purchased the PRO version so that I could study sections I was not clear about and then test my knowledge. Being able to keep track of what you have studied is great, but what I love most is that I am able to figure out what I need more help in with the tests, and then use the flashcards to help me understand those areas better—so much so that I have challenged decisions from our controller, and was able to intelligently discuss my reasoning and be granted permission for change. Any person wanting to become a bookkeeper or accountant would benefit from using AccountingCoach, but having the PRO version takes it to the next level! Oh, by the way—I started as the staff accountant, and have since been promoted to Assistant Controller and will be promoted again to Controller when our current controller retires in less than a year. Thank you!" - Anna W.