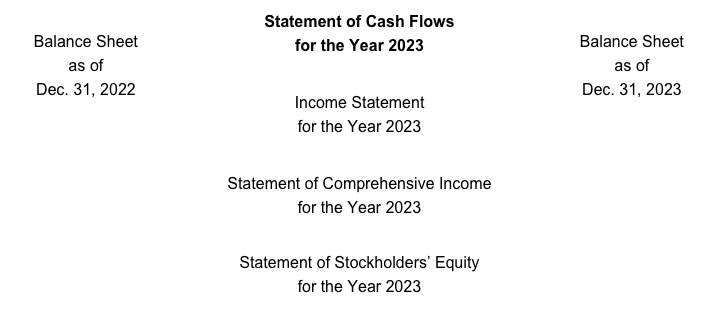

The statement of cash flows (or SCF) is one of the five main financial statements. It is also referred to as the cash flow statement.

The statement of cash flows covers a period of time— usually the same period as the income statement:

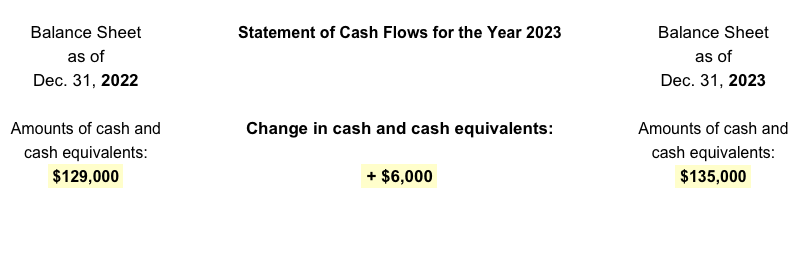

The statement of cash flows identifies the major cash inflows and outflows involved in the change in a corporation’s cash equivalents during a period of time. The period of time could be a year, quarter, month, 5 weeks, etc.

In other words, the statement of cash flows highlights the cash inflows and outflows occurring between two balance sheet dates:

The financial statements issued by U.S. corporations must be prepared according to generally accepted accounting principles (referred to as GAAP or US GAAP). These include very complex, detailed rules and some basic underlying principles, guidelines, and concepts such as the cost principle, matching principle, going concern assumption, conservatism, materiality, objectivity, and others.

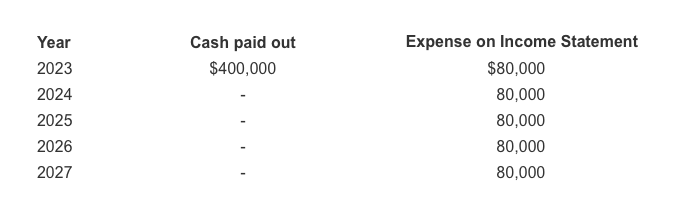

To illustrate the need for the statement of cash flows, let’s assume that a corporation purchases a new machine on January 2, 2023 for $400,000 in cash but expenses it over a useful life of 5 years. If the corporation’s accounting year ends on each December 31 and straight-line depreciation is used, the income statement will report $80,000 of depreciation expense in each of the years 2023 through 2027. Note the differences between the time when cash is paid out and the time when the expense is reported on the income statement:

Now that you have seen some examples of why the income statement does not provide cash inflows and cash outflows, let’s look at the heading of the statement of cash flows.

Note that the heading begins with the corporation’s name. The second line is the name of the financial statement. The third line reports the period of time covered, which is usually the same period as the income statement.

Here’s an example of a heading for the SCF:

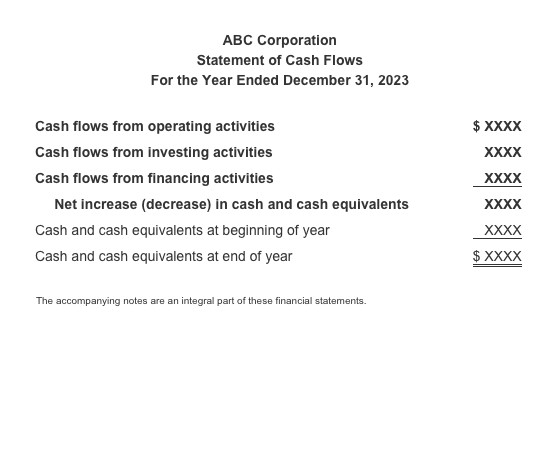

The cash inflows and outflows that reconcile the beginning and ending amounts of cash and cash equivalents are presented in three sections: operating activities, investing activities, and financing activities. The total of those three sections must agree to the change in cash and cash equivalents. Here is an outline of the statement of cash flows including the usual reference to the notes to the financial statements:

Section #1 of SCF: Cash Flows from Operating Activities (continued)

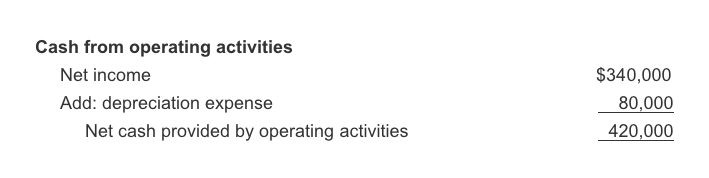

Let’s assume that a corporation spent $400,000 on January 2, 2023 to purchase equipment and that it will record $80,000 of depreciation expense in each of the years 2023-2027.

Each year, the entry to record depreciation expense of $80,000 will reduce the company’s net income, but it will not reduce the corporation’s cash.

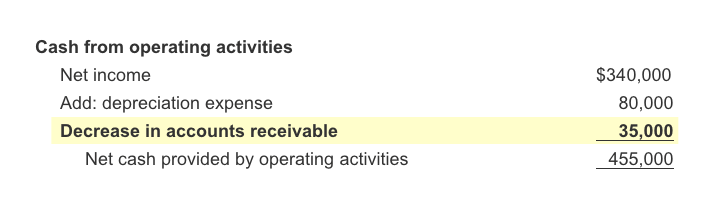

If we assume that the corporation’s income statement for one of the years reports $340,000 of net income, the SCF will begin with the following amounts:

Section #1 of SCF: Cash Flows from Operating Activities (continued)

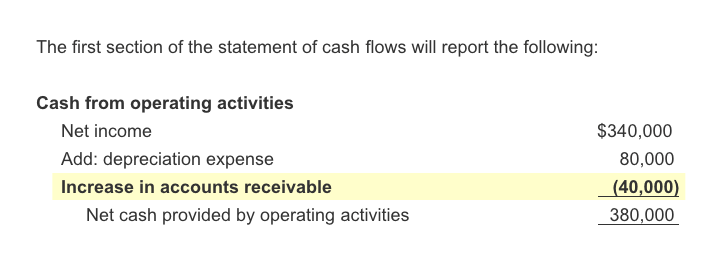

After adding back the depreciation expense, we list the amounts that will convert the revenues and expenses from the accrual method to their cash amounts.

For example, if a corporation’s income statement and net income included sales of $950,000 but the accounts receivable increased by $40,000, there needs to be an adjustment for the $40,000 not collected.

Not collecting $40,000 of the sales hurts the corporation’s cash balance and as a result will be shown as a negative adjustment to the net income.

Section #1 of SCF: Cash Flows from Operating Activities (continued)

If the total of accounts receivable had decreased by $35,000 (instead of increasing by $40,000), the amount of cash collected would have been $35,000 more than the sales reported on the income statement.

Collecting $35,000 more than the sales included in the net income helps the corporation’s cash balance and as a result will be reported as a positive adjustment to the net income amount on the SCF:

Section #1 of SCF: Cash Flows from Operating Activities (continued)

Next, we will adjust expenses from the accrual amounts to the cash amounts.

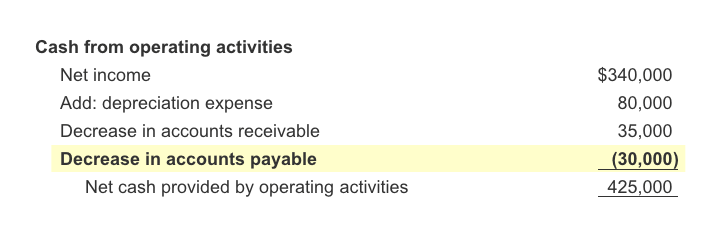

For instance, if the corporation’s income statement and net income included expenses of $550,000 but its accounts payable decreased by $30,000, there needs to be an adjustment for the additional payment of $30,000.

Paying $30,000 more than the amount of expenses on the income statement hurts the corporation’s cash balance and will need to be reported as a negative adjustment to the net income amount on the SCF:

Section #1 of SCF: Cash Flows from Operating Activities (continued)

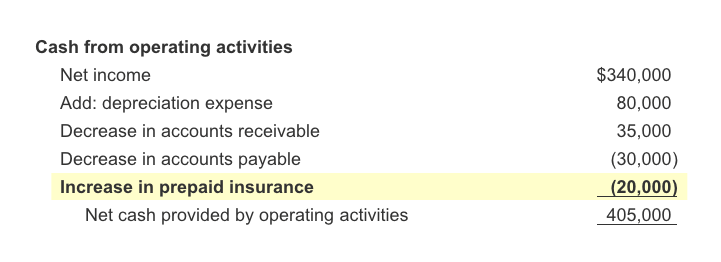

Another adjustment for expenses involves prepaid expenses. Let’s assume that the amount of prepaid insurance (a current asset) was $10,000 at the start of the year and it was $30,000 at the end of the year. The increase of $20,000 means that in addition to the insurance expense included in the net income, an additional payment of $20,000 must have been made.

Increasing the prepaid insurance by $20,000 required an additional cash outflow of $20,000. Since this hurts the corporation’s cash balance, it is reported as a negative adjustment to the net income:

Section #2 of SCF: Cash Flows from Investing Activities

The second section of the SCF reports the cash inflows and outflows pertaining to noncurrent assets such as long-term investments and property, plant and equipment.

For example, if a corporation’s balance sheet shows an increase in land, buildings, equipment, vehicles, etc., it is assumed that cash was used. When cash is used, it is an outflow of cash and will, therefore, be reported as a negative amount under investing activities.

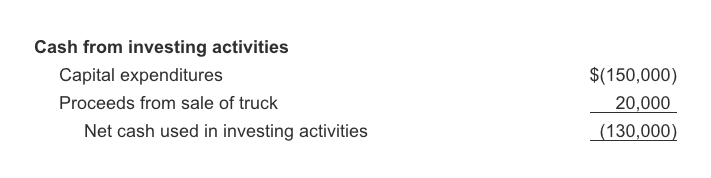

The amounts spent for property, plant and equipment are often referred to as capital expenditures and will be reported as follows:

Section #2 of SCF: Cash Flows from Investing Activities (continued)

When a long-term asset is sold, the money received from the sale/disposal will be reported as a positive amount in the investing activities section of the SCF.

To illustrate, let’s assume that a corporation sells its old delivery truck and receives cash of $20,000. Since this is a cash inflow, the amount received will be reported as a positive amount as shown below.

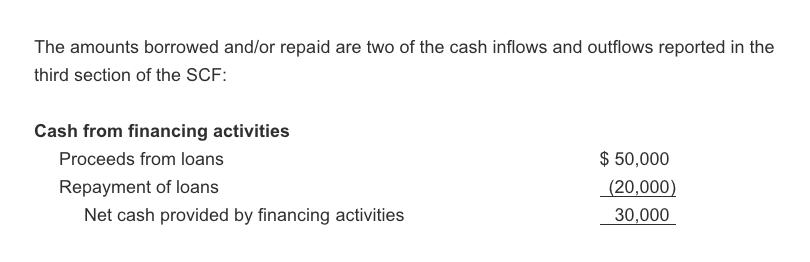

Section #3 of SCF: Cash Flows from Financing Activities (continued)

When a corporation borrows money, its liabilities increase and its cash increases. In other words, the corporation will see a cash inflow. The cash inflows from borrowing money are reported as positive amounts in the financing activities section of the SCF.

When a corporation repays the money it had borrowed, its liabilities decrease and its cash decreases. The cash outflows associated with repaying loans are reported as negative amounts in the financing activities section of the SCF.

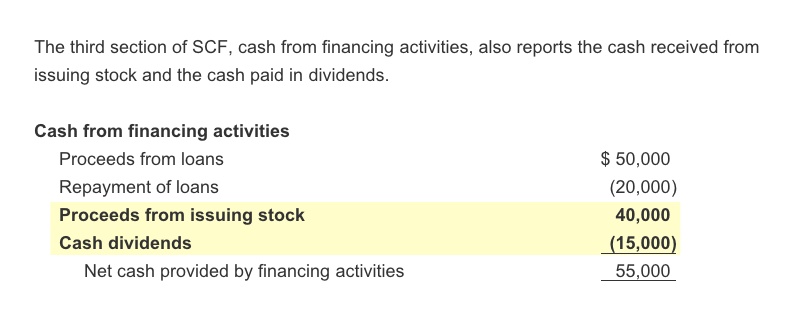

Section #3 of SCF: Cash Flows from Financing Activities (continued)

When a corporation issues shares of its stock, the paid-in capital section of stockholders’ equity increases and its cash increases. The cash inflow from issuing stock will be reported as a positive amount in the financing activities section of the SCF.

When a corporation pays dividends to its stockholders, the cash outflow is reported as a negative amount in the financing activities section of the SCF.

Turn on study mode to focus

Cash Flow Statement Outline

- Read our Explanation (8 Parts) Free

- Take our Practice Quiz Free

- Review our Visual Tutorial

- Watch our Financial Statements Video Training

- Review our Flashcards

- Solve our Word Scramble Free

- Solve our Crossword Puzzle #1 Free

- Solve our Crossword Puzzle #2 Free

- Solve our Crossword Puzzle #3 Free

- Review our Sample Business Forms

- Review our Cheat Sheet

- Take our Quick Test #1

- Take our Quick Test #2 with Coaching

- Earn our Cash Flow Statement Certificate of Achievement

Learn How to Advance Your Accounting and Bookkeeping Career

- Perform better at your current job

- Refresh your skills to re-enter the workforce

- Pass your accounting class

- Understand your small business finances

Featured Review

"I am a small business accountant and tax preparer. A lot of my clients are do-it-yourself bookkeepers for their small business. Most of them, if not all, use bookkeeping software to keep track of their business. Although software programs are great at what they do and are easy for the user, the double entry accounting method is still occurring in the background. Accounting concepts and terms are not easily explained to a small business owner who doesn't understand why reports look the way they do. To help them, I always direct them to AccountingCoach to learn the concepts and terms. The tutorials, glossary, and web topics are presented in the best way that anyone can understand accounting. It's the best source on the web!" - Kathleen F.