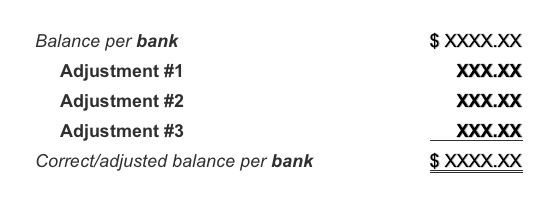

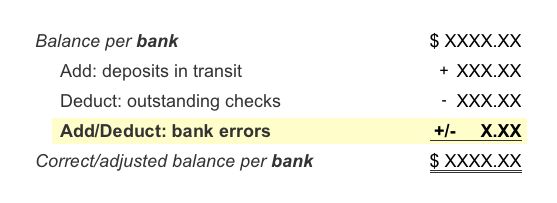

The balance per bank will need to be adjusted for items that are in the company’s records but are not yet in the bank’s records.

Here is the format for adjusting the balance per bank:

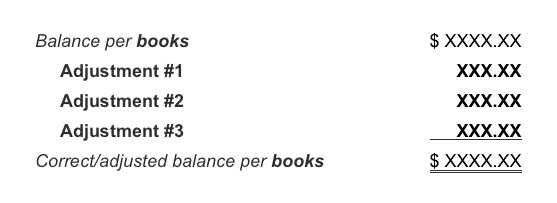

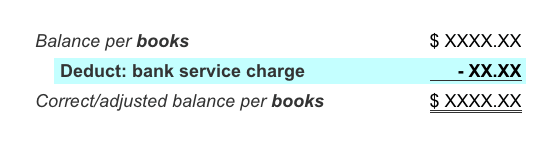

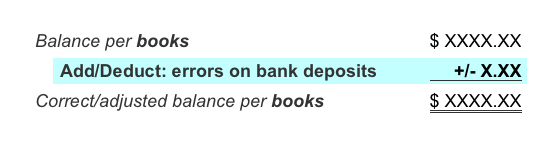

The balance per books will need to be adjusted for items that are in the bank’s records but are not yet in the company’s accounting records.

Here is the format for adjusting the balance per books:

Adjustments to the Balance per Bank

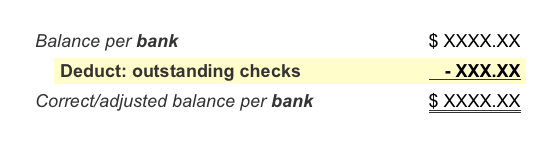

Recall that the balance per bank must be adjusted for the items that are in the company’s records but are not yet in the bank’s records.

The most common adjustment to the balance per bank is the amount of the checks that have been written by the company but have not yet cleared its bank account. These are referred to as outstanding checks.

The amount of outstanding checks is deducted from the balance per bank:

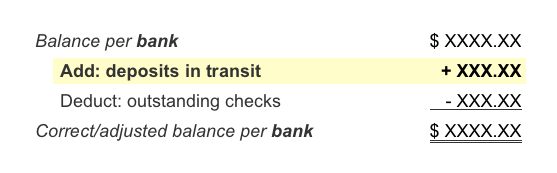

Another adjustment to the balance per bank will be the money received by the company but not yet appearing in the bank’s records. These are known as deposits in transit. They may result from a retail store depositing each day’s receipts in the bank’s night depository after the normal banking hours or at the bank on the following morning.

The deposits in transit are additions to the balance per bank:

A third possibility for an adjustment to the balance per bank is a bank error.

Depending on the bank error, it could be an addition or a subtraction from the balance per bank:

Adjustments to the Balance per Books

We will now discuss the balance per books. This is the balance in the company’s general ledger for the checking account.

The balance per books will need to be adjusted for items that are already in the bank’s records but are not in the company’s records. The bank’s monthly service charge is an example of a deduction to the balance per books:

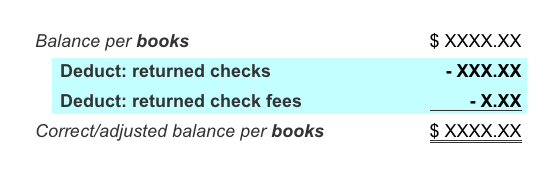

Occasionally the bank will charge the company’s checking account for a check that the company deposited earlier but it is now being returned as NSF (not sufficient funds in the checking account of the person writing the check).

Since the amounts are already deducted on the bank’s records, these will be a deduction to the balance per books.

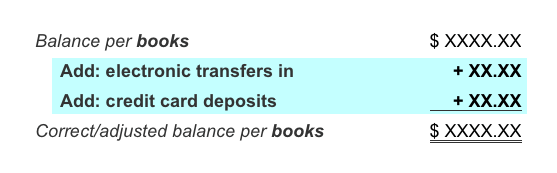

Besides deductions, the bank may have increased the checking account balance without notifying the company. For example, there may have been an electronic transfer of funds into the checking account from one of the company’s customers or from a credit card processor.

The two items mentioned will be additions to the balance per books:

As usual, the adjustments to the balance per books must be recorded in the company’s general ledger accounts.

It is also possible that the bank increased or decreased the company’s checking account for an error the company had made on one of its bank deposits.

A company error on one of its bank deposits will be an adjustment to the balance per books.

Any error by the company needs to be corrected in the company’s general ledger accounts.

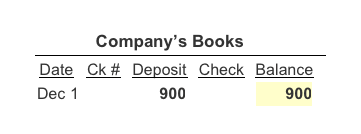

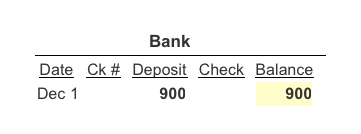

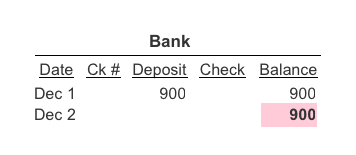

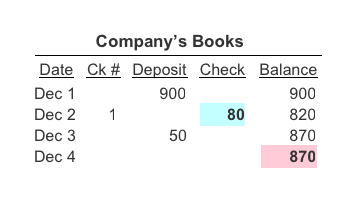

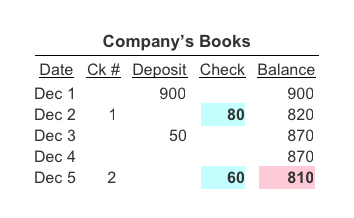

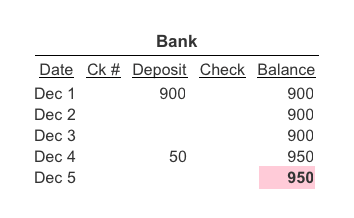

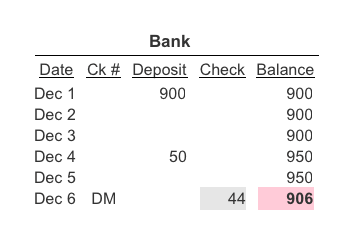

We will use a series of transactions to illustrate the correct/adjusted balance method for reconciling the bank statement. The first transaction is the owner’s deposit of $900 to open the company’s checking account on December 1. Both the general ledger accounts (books) and the bank show the balance of $900.

Since both the balance per books and the balance per bank are the same, we state that the bank statement is reconciled as of December 1.

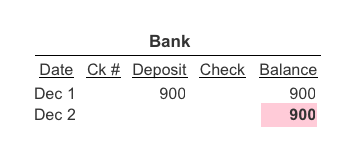

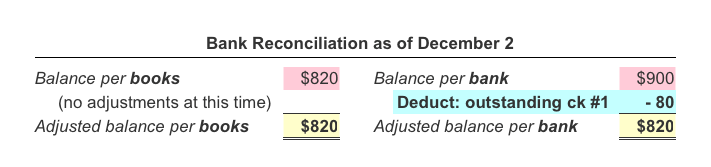

On December 2, the company issues its check #1 for $80 and mails it to the payee. As of December 2, the balance per books is $820 and the balance per bank is $900.

Bank Reconciliation as of December 2

Since the balance per books is $820 and the balance per bank is $900, we need to reconcile the difference.

Recall our earlier advice of “put the item where it isn’t.” Since check #1 is already on the books, but it isn’t on the bank statement, we list the outstanding check as an adjustment to the balance per bank:

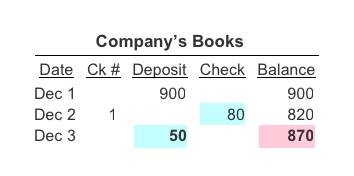

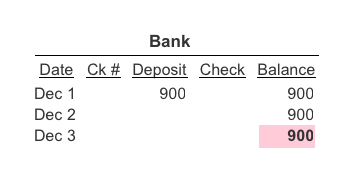

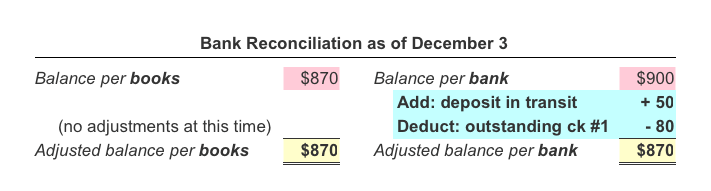

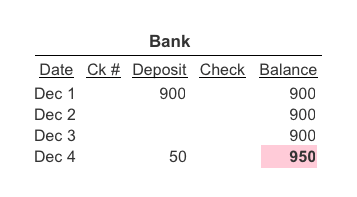

On December 3, the company receives $50 from a customer, however it is recorded by the bank on the next day. Since the $50 was a December 3 receipt, it is recorded in the general ledger as of December 3. Since the bank processed the deposit on December 4, the bank’s records as of December 3 will not show the $50 deposit:

Bank Reconciliation as of December 3

Since the receipt of December 3 is on the company’s books, but it isn’t in the bank’s records as of December 3, this deposit in transit is an adjustment to the balance per bank. Since check #1 has not yet cleared the bank as of December 3, there will be two adjustments to the balance per bank:

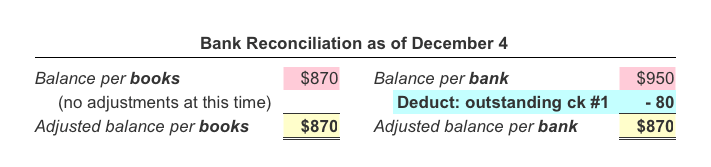

On December 4, the company does not write any checks or receive any money. However, the bank processed the company’s $50 deposit.

Bank Reconciliation as of December 4

Since check #1 has not cleared the bank as of December 4, it will continue to be listed as an adjustment to the balance per bank. Note that after the adjustment for the outstanding check, the bank reconciliation shows the correct balance of $870 for both the books and the bank.

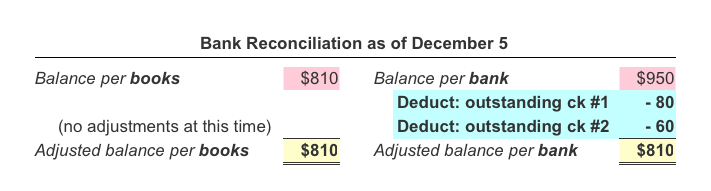

On December 5 the company writes check #2 for $60 and mails it to the payee. There were no receipts and no other payments.

Bank Reconciliation as of December 5

Since neither check #1 nor check #2 have cleared the checking account at the bank, both checks are adjustments to the balance per the bank as of December 5:

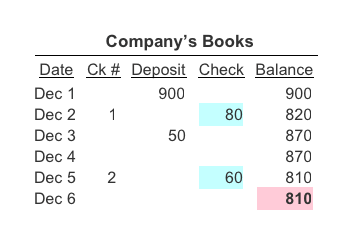

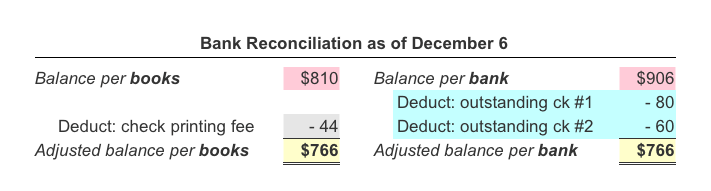

On December 6, the bank charges the company’s checking account $44 for the printing of the checks that the company had ordered through the bank.

The bank charge (noted as DM for debit memorandum) of $44 appears on the bank’s records, but wasn’t on the company’s books. Therefore the $44 charge will be an adjustment to the balance per books:

Since the adjusted balance per books and the adjusted balance per bank agree, we say the bank statement has been reconciled.

Practice Bank Reconciliation #1

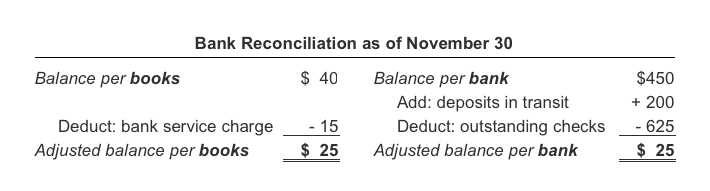

Let’s prepare a bank reconciliation using the following information as of November 30:

Balance in the general ledger for the checking account $40; balance in the bank’s records (bank statement) $450; deposits in transit $200; outstanding checks $625; bank service charge $15.

Practice bank reconciliation #2

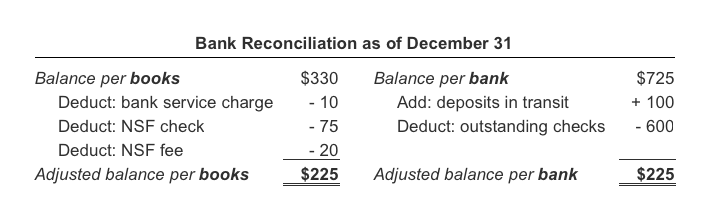

Next, let’s prepare a bank reconciliation using the following information as of December 31:

Balance in the general ledger for the checking account $330; balance in the bank’s records (bank statement) $725; deposits in transit $100; outstanding checks $600; bank service charge $10; NSF check of $75; NSF check fee $20.

Turn on study mode to focus

Bank Reconciliation Outline

- Read our Explanation (3 Parts) Free

- Take our Practice Quiz Free

- Review our Visual Tutorial

- Review our Flashcards

- Solve our Word Scramble Free

- Solve our Crossword Puzzle #1 Free

- Solve our Crossword Puzzle #2 Free

- Solve our Crossword Puzzle #3 Free

- Review our Sample Business Forms

- Review our Cheat Sheet

- Take our Quick Test #1

- Take our Quick Test #2

- Take our Quick Test #3 with Coaching

- Earn our Bank Reconciliation Certificate of Achievement

Learn How to Advance Your Accounting and Bookkeeping Career

- Perform better at your current job

- Refresh your skills to re-enter the workforce

- Pass your accounting class

- Understand your small business finances

Featured Review

"I am a small business accountant and tax preparer. A lot of my clients are do-it-yourself bookkeepers for their small business. Most of them, if not all, use bookkeeping software to keep track of their business. Although software programs are great at what they do and are easy for the user, the double entry accounting method is still occurring in the background. Accounting concepts and terms are not easily explained to a small business owner who doesn't understand why reports look the way they do. To help them, I always direct them to AccountingCoach to learn the concepts and terms. The tutorials, glossary, and web topics are presented in the best way that anyone can understand accounting. It's the best source on the web!" - Kathleen F.