Statement of Functional Expenses

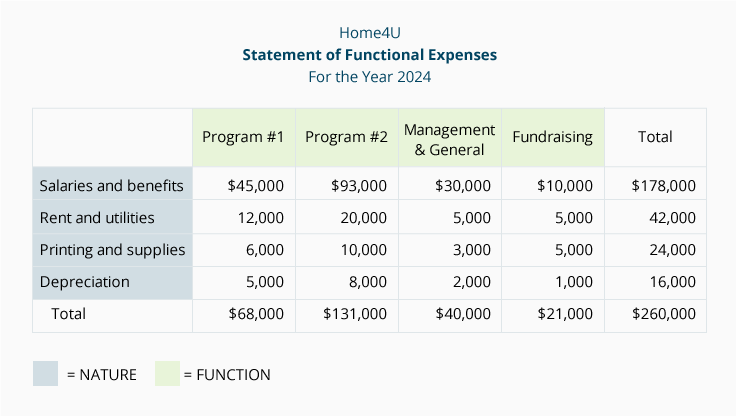

The statement of functional expenses is described as a matrix since it reports expenses by their function (programs, management and general, fundraising) and by the nature or type of expense (salaries, rent). For instructional purposes we highlighted the column headings to indicate the expenses by function. We also highlighted the words in the first column as they indicate the nature or type of expenses.

The FASB requires every nonprofit to present expenses by function and nature in one place (statement or notes).

Please let us know how we can improve this explanation

No ThanksStatement of Cash Flows

The statement of cash flows (SCF) for a nonprofit organization is similar to that of a for-profit business. The SCF reports the organization’s change in its cash and cash equivalents during the accounting period.

The statement of cash flows consists of three sections:

- Cash flows from operating activities

- Cash flows from investing activities

- Cash flows from financing activities

The operating activities section of the SCF reports the changes in cash other than those reported in the investing and financing sections.

The investing activities section of the SCF reports the amounts spent to purchase long-term assets such as equipment, vehicles and long-term investments. The investing section also reports the amount received from the sale of long-term assets.

The financing activities section of the SCF reports the amounts received from borrowings and also any repayments.

While the statement of cash flows, or cash flow statement, may be a bit difficult to prepare, it is an important financial statement to be read.

You can learn more about this financial statement by reading our Explanation of the Cash Flow Statement.

Please let us know how we can improve this explanation

No ThanksNotes to the Financial Statements

The notes to the financial statements are an integral part of the statement of financial position, the statement of activities, and the statement of cash flows. The FASB Accounting Standards Codification Topic 958 requires important additional disclosures regarding liquidity, restrictions, etc. for creditors, donors, and others.

Please let us know how we can improve this explanation

No ThanksAdditional Reporting by Nonprofits

The U.S. Internal Revenue Service (IRS) requires some tax-exempt nonprofit organizations to file Form 990 (some can file Form 990-EZ) each year. (However, churches and some other nonprofit organizations are not required to file.) The title of Form 990 is Return of Organization Exempt From Income Tax.

Since the Form 990 filed by the nonprofit becomes public information, you can learn much about a nonprofit by reading the information on Form 990. The website guidestar.org is a resource one can use to obtain financial (and other) information reported on nonprofits’ Form 990.

Please let us know how we can improve this explanation

No ThanksBudgeting for Nonprofits

Budgeting for nonprofits can become complex when it involves several overlapping categories, such as grants, programs, function, and nature.

Budgeting is also complicated when sources of support are not secured at the time the budget is prepared for the upcoming year. This could lead to the use of an account entitled Resource Development in order to balance the budget.

Since resource development is often ongoing, budgets may require frequent modification. Good accounting software will also allow directors to compare budgeted amounts to actual amounts and make the necessary adjustments.

Please let us know how we can improve this explanation

No Thanks