Financial Reporting vs. Individual Products and Customers

As mentioned above, in order for a manufacturer’s financial statements to be in compliance with GAAP, a portion of the manufacturing overhead must be allocated to each item produced. Even when allocations are arbitrary and inaccurate, the totals of the amounts reported as inventory and cost of goods sold on the financial statements can still be reasonably correct. For example, if a manufacturer’s inventory is minimal or if the beginning and ending inventories are similar in amount, this indicates that the company is selling nearly all of the units it produced in a given year. If that is the case, then as long as most of the manufacturing overhead appears on the income statement as part of the cost of goods sold, the financial statements will be correct—even if the amounts allocated to the individual products are inaccurate. The message here is this: Even if each product’s costs are wrong due to inaccurate allocations of manufacturing overhead, it is still possible that the financial statements will be accurate and receive a clean audit report.

However, if management wants to know the true cost of manufacturing an individual item, it is essential that the manufacturing overhead be allocated in a precise and logical manner. In addition to knowing the true cost of manufacturing each item, management needs to know the true expense of all of the other business functions associated with an individual item. In this way, management will know if each product and each customer is generating sufficient sales revenue to cover not the only manufacturing costs but also the selling, general and administrative expenses, interest expense, and some profit. This means that management will need to allocate/assign nonmanufacturing costs to individual products and customers (even though this type of allocation is not allowed for external financial statements).

In short, the company’s financial statements could be accurate with improper allocation to individual products, but for management’s decisions (1) the allocations of manufacturing overhead must be accurate and (2) the nonmanufacturing costs must be accurately assigned to individual products and customers. For example, if an inaccurate allocation results in too much cost assigned to some products, management might seek price increases on those products when in reality such price increases are not necessary. If customers react to the proposed unnecessary price increases by seeking bids from other manufacturers, the company may end up losing sales, profits, and customers. Conversely, if inaccurate allocations result in too few costs assigned to some products, a company may not realize that a specific product’s selling price is inadequate to cover the true costs needed to produce and sell that product. If the company does not pursue a price increase or improvements in efficiency, the company might be selling that product at a loss.

Although a company doesn’t need precise, detailed allocations for purposes of preparing your company’s financial statements, the odds are that at some point down the road those inaccurate allocations may result in poor pricing decisions. That’s something a company cannot afford to do in an increasingly competitive global market.

Please let us know how we can improve this explanation

No ThanksTraditional Methods of Allocating Manufacturing Overhead

Let’s look at several of the traditional methods for allocating manufacturing overhead. Keep in mind that if the method does not allocate the true amount of factory overhead, the cost per unit of product will be wrong and could result in management making a flawed decision. As you review these methods, ask yourself for each given product, will the allocated amount of overhead reflect the actual amount of overhead used in that item’s production? If a cause-and-effect relationship is not evident, is there at least an obvious correlation between manufacturing overhead and the basis for the allocation (such as production machine hours)? If there is no correlation, the allocation method is suspect and could result in the improper amount of overhead being assigned to individual products.

Allocating Manufacturing Overhead Via Direct Labor

In the early 1900s (and in some labor intensive production) it was logical to allocate manufacturing overhead on the basis of direct labor hours (or direct labor cost). The manufacturing process was not automated, there were hardly any variations in the products made (think Model T cars), and customers did not demand such things as just-in-time (JIT) deliveries or bar coding. In those days, when manufacturers increased the amount of direct labor, there was likely to be a related increase in such things as the number of factory supervisors, the factory space to be maintained, and factory supplies and utilities consumed. In other words, there was a high degree of correlation between the quantity of direct labor used and the cost of the manufacturing overhead. By allocating manufacturing overhead on the basis of direct labor hours, a product requiring 30 direct labor hours would be allocated twice as much manufacturing overhead as a product requiring 15 direct labor hours.

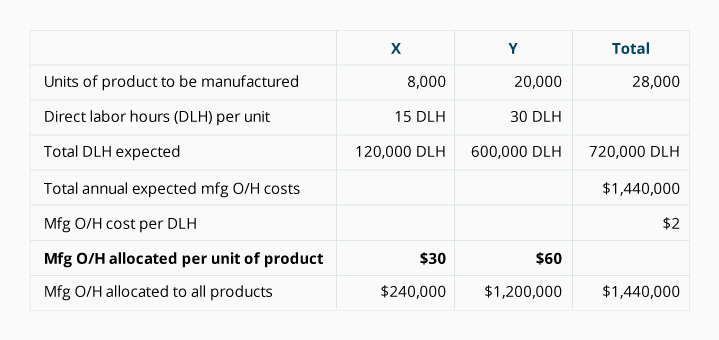

Let’s illustrate an overhead rate based on direct labor hours for a company that manufactures just two products, X and Y. (An annual rate is developed in order to have a constant overhead rate even when production volumes fluctuate from month to month.) For the upcoming year the company expects the following:

As shown in the above table, each unit of Product X will be assigned $30 of overhead, and each unit of Product Y will be assigned $60 of overhead. This is reasonable so long as there is a correlation between the quantity of direct labor hours and the cost of manufacturing overhead.

Allocating Manufacturing Overhead Via Departmental Machine Hours

As the 20th century moved on, manufacturers studied and controlled direct labor’s time and motion (think of Frederick Taylor’s work) and began replacing direct labor with machines. The increased use of machines resulted in an increase in factory overhead due to such things as additional depreciation of the machinery, maintenance of the machinery, and machine setups. With direct labor being reduced and manufacturing overhead increasing, the correlation between direct labor and manufacturing overhead began to wane. A logical response was to begin allocating manufacturing overhead on the basis of machine hours instead of direct labor hours.

Companies also began to create new departments to help manage the changing character of the factories. Production departments such as machining, finishing, and assembling were established. Other departments such as quality control, maintenance, and factory administration were designated as service departments (or production service departments), since these departments served the production departments. The company’s costs were contained in the accountant’s general ledger, which was organized by departments so as to mirror the organization chart and to provide for budgeting and control. Because some of the production departments used more of some service departments’ efforts/costs than others, accountants responded by first allocating the service department costs to the production departments, and then developing manufacturing overhead rates for each of the production departments. These rates were computed by dividing each production department’s costs (its own direct costs plus the service departments’ costs allocated to it) by its machine hours.

Basing the manufacturing overhead rates on a company’s production departments was an improvement over using just one rate for the entire plant—particularly when companies began manufacturing a greater variety of products. Some products being manufactured may have required many machine hours in one department but very few hours in another department, while other products may have used a much different combination of machine hours.

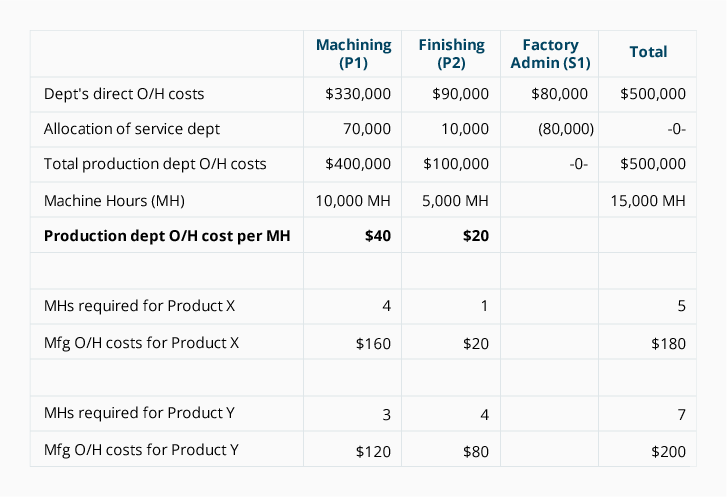

Let’s illustrate this method by assuming just two products (X and Y) are being manufactured in a factory that has one service department (Factory Administration, S1) and two production departments (Machining, P1; Finishing, P2).

Had the company used a plant-wide rate, the manufacturing overhead rate would have been $33.33 per MH ($500,000 divided by 15,000 MH), instead of $40 for the machining department and $20 for the finishing department. By using departmental rates, products requiring more machine hours in a high-cost department will be assigned a higher cost than would be assigned if using one established plant-wide rate. Products requiring more time in a low-cost department will be assigned a lower cost as compared to one plant-wide rate.

Please let us know how we can improve this explanation

No Thanks