For multiple-choice and true/false questions, simply press or click on what you think is the correct answer. For fill-in-the-blank questions, press or click on the blank space provided.

If you have difficulty answering the following questions, learn more about this topic by reading our Financial Ratios (Explanation).

Inventory

Prepaid Insurance

Fixtures

Current Ratio

Net Worth

Working Capital

Current Ratio

Net Worth Ratio

Working Capital

Accounts Receivable

Inventory

Cash

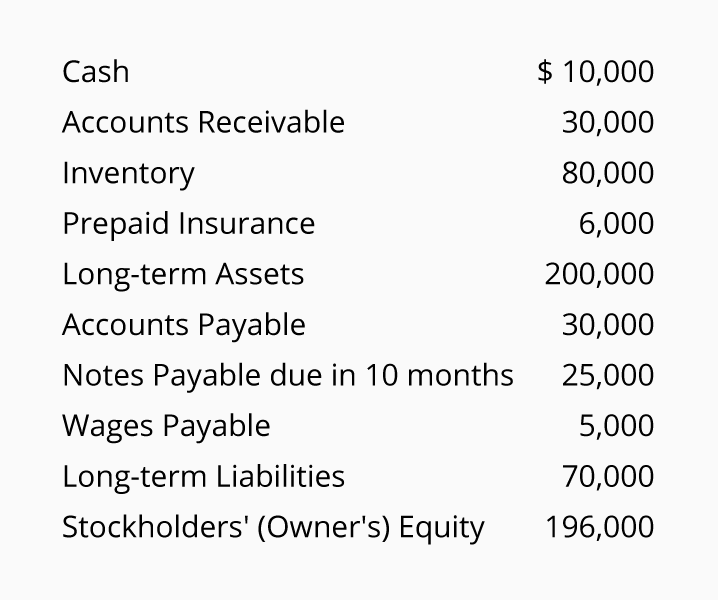

Use the following information to answer items 5 – 7:

At December 31 a company’s records show the following information:

$60,000

$66,000

$196,000

1.0 : 1

2.0 : 1

2.1 : 1

0.7 : 1

1.0 : 1

2.0 : 1

Use the following information to answer items 8 – 11:

For its most recent year a company had Sales (all on credit) of $830,000 and Cost of Goods Sold of $525,000. At the beginning of the year its Accounts Receivable were $80,000 and its Inventory was $100,000. At the end of the year its Accounts Receivable were $86,000 and its Inventory was $110,000.

4.8

5.0

7.9

6.3

7.5

10.0

27

37

49

14

46

73

Use the following information for items 12 and 13:

A company’s net income after tax was $400,000 for its most recent year. The company’s income statement included Income Tax Expense of $140,000 and Interest Expense of $60,000. At the beginning of the year the company’s stockholders’ equity was $1,900,000 and at the end of the year it was $2,100,000.

6.7

9.0

10.0

20%

25%

30%

Current Assets

Long-term Assets

Stockholders' Equity

True

False

True

False

True

False

Operating

Investing

Financing

Want more practice questions?

Receive instant access to our graded Quick

Tests (more than 1,800 unique test questions) when you join

AccountingCoach PRO.

Featured Review

"I'm currently transitioning from a programming background into the world of accounting, and AccountingCoach has been an absolute game-changer. The PRO membership has provided me with an unparalleled learning experience with the videos, quick tests, cheat sheets, flashcards, and printable PDF files; and those are not even all of the features of the PRO membership! I'm so happy to have found this excellent learning platform, covering everything from accounting basics to the most complex topics. The depth and simplicity with which intricate accounting concepts are explained have been a revelation. And the greatest thing about it all is that I can master accounting at my own pace, without any time restrictions. The lifetime access ensures I can revisit and reinforce my knowledge whenever needed. Thank you, AccountingCoach, for being the comprehensive, accessible, and reliable platform that has immensely supported my transition into the captivating world of accounting!" - Ben P.

Join PRO or PRO Plus and Get Lifetime Access to Our Premium Materials

Read all 2,645 reviews

For the past 52 years, Harold Averkamp (CPA, MBA) has worked as an accounting supervisor, manager, consultant, university instructor, and innovator in teaching accounting online. He is the sole author of all the materials on AccountingCoach.com.

Learn More About Harold

We now offer 10 Certificates of Achievement for Introductory Accounting and Bookkeeping: