Annual Financial Statements

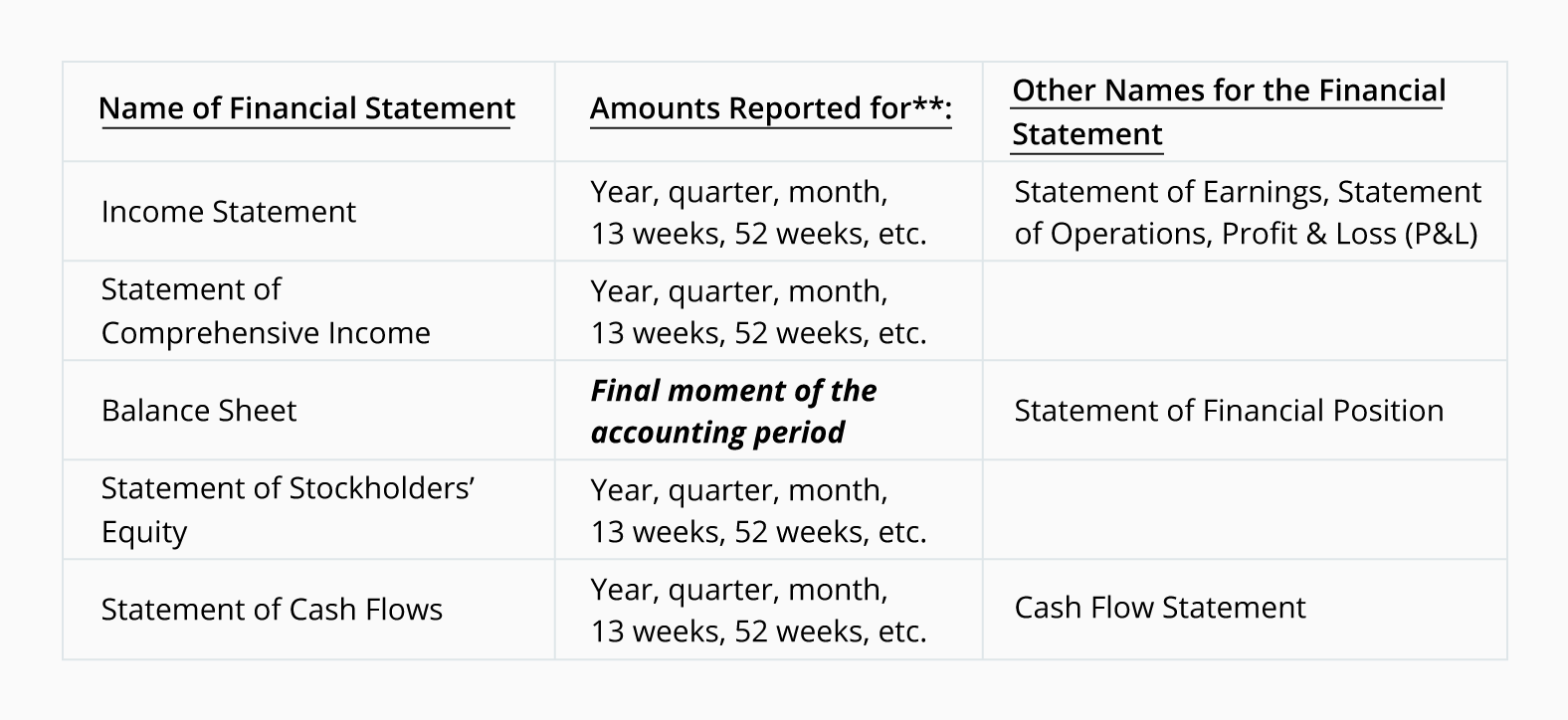

The financial statements that are to be included as a complete set when a U.S. corporation distributes them to people outside* of the corporation are:

*Examples of people outside of the corporation that are likely to receive these external, general-purpose financial statements include investors, lenders, government agencies, etc.

**Note that the balance sheet reports amounts as of the final moment of the accounting period. For example, the balance sheet’s heading might indicate “December 31, 2023”. This means that the amounts are as of midnight on December 31. Examples of the headings of the other four financial statements include “For the Year Ended December 31, 2023”, “For the Six Months Ended June 30, 2023”, For the 13 Weeks Ended…”, etc.

Notes to Financial Statements

For the financial statements to be complete, they must be accompanied with notes to the financial statements. The notes are usually referenced at the bottom of each of the financial statements with wording such as “See notes to the financial statements.” or “The accompanying notes are an integral part of the financial statements.”

Generally Accepted Accounting Principles

The external financial statements must be in compliance with generally accepted accounting principles, which are commonly referred to as GAAP or US GAAP. GAAP includes basic underlying principles, official accounting standards issued by the Financial Accounting Standards Board (FASB), and industry-specific requirements. U.S. corporations whose stock is publicly-traded are also required to file financial reports to the U.S. Securities and Exchange Commission (SEC).

Generally, US GAAP requires that a U.S. corporation’s financial statements be based on the accrual method (or accrual basis) of accounting. The accrual method means that 1) revenues and a related receivable will be reported when they are earned and collection is assured, and 2) expenses and a related payable will be reported when an expense or loss has occurred. In short, the accrual method of accounting will result in financial statements that will be more complete and useful.

The financial statements are interconnected and should always be in balance because of the accounting equation and double-entry accounting system.

Accounting Periods

Often U.S. corporations have accounting years that end on December 31 (referred to as calendar years). However, many U.S. corporations have fiscal years which end on other dates, such as June 30, September 30, etc. In addition, some U.S. corporations have 52/53-week years which end on the Saturday nearest to January 31 or some other day of the week. Those corporations’ interim financial statements will include four 13-week periods instead of four 3-month quarters.

Income Statement

The income statement reports a corporation’s revenues, expenses, gains, losses, and the resulting net income for the period of time specified in its heading. The period of time or time interval could be a year, quarter, week, 26 weeks, etc.

If the corporation’s shares of stock are publicly traded, the earnings per share of common stock (EPS) must also be reported on the face of the income statement.

A positive net income reported on the income statement will cause the corporation’s retained earnings (part of the balance sheet section, stockholders’ equity) to increase. A net loss will cause retained earnings to decrease.

There are a few items that will increase stockholders’ equity but will not be reported on the income statement. These items are part of other comprehensive income, which is reported on the statement of comprehensive income.

Statement of Comprehensive Income

The statement of comprehensive income reports the amount of a corporation’s comprehensive income (or loss), which consists of the following:

- The corporation’s net income (the details of which are reported on the income statement)

- Items that are classified as other comprehensive income for the period of time indicated in the heading.

Some of the items that are considered to be other comprehensive income include:

- Unrealized gains or losses on derivatives used in hedging

- Unrealized gains or losses on pension and postretirement liabilities

- Foreign currency adjustments.

The total of the other comprehensive income will cause the corporation’s accumulated other comprehensive income (a component of the balance sheet section, stockholders’ equity) to change.

NOTE: Net income increases retained earnings, but other comprehensive income increases accumulated other comprehensive income.

Balance Sheet

The balance sheet reports a corporation’s assets, liabilities, and stockholders’ equity as of a moment in time. (The other financial statements report amounts for a period of time.) The balance sheet reports amounts as of the final moment of the day shown in the heading of the balance sheet, which is typically the final moment of the accounting period.

At all times the amount of the corporation’s assets should be equal to the amount of liabilities plus stockholders’ equity. In other words, the balance sheet reflects the accounting equation: assets = liabilities + stockholders’ equity.

Assets are resources such as cash, inventory, investments, buildings, equipment, and prepaid or deferred expenses. Liabilities are obligations such as accounts payable, loans payable, accrued expenses payable (wages, interest, utilities), deferred revenues, and bonds payable. Stockholders’ equity includes paid-in capital, retained earnings, accumulated other comprehensive income, and treasury stock.

Because of the cost principle, some valuable assets will not be reported (trade names, management) and some assets may be more valuable than the reported amounts based on cost. As a result, the amount of stockholders’ equity should not be interpreted to be the corporation’s market value.

Statement of Stockholders’ Equity

The statement of stockholders’ equity reports the changes that occurred during the accounting year to the corporation’s paid-in capital, retained earnings, accumulated other comprehensive income, and treasury stock.

Statement of Cash Flows

The statement of cash flows (SCF or cash flow statement) reports a corporation’s significant cash inflows and cash outflows that caused the corporation’s cash and cash equivalents to change. The cash flow information is important because the income statement reflects the accrual method of accounting (not the cash method).

The cash flows are presented in one of the three sections of the SCF:

- Operating activities

- Investing activities

- Financing activities

In addition, the following supplementary information must be disclosed: interest paid, income taxes paid, and significant noncash transactions such as the exchange of shares of common stock for land.

Notes to Financial Statements

The notes to the financial statements are considered to be an integral part of the financial statements and are referenced at the bottom of each financial statement. The first of the notes lists the corporation’s significant accounting policies. Large corporations could have 30 or more pages of notes in order to comply with the full disclosure principle.

Comparative Financial Statements

In order for the financial statements to be more useful, corporations prepare comparative financial statements. This means that in addition to the amounts for the current year, the statements will also have columns containing the amounts from one or two of the earlier years. These earlier amounts give the readers a frame of reference when reviewing the most recent amounts.

Audited Financial Statements

Some financial statements must be audited. For example, corporations with common stock that is traded on a stock exchange must have their financial statements audited by a registered CPA firm. Other corporations may have a lender or investor that requires that the financial statements be audited. The CPA firm that performs the audit will issue an audit report to describe what to expect from the audit.