Bond Premium with Straight-Line Amortization

When a corporation prepares to issue/sell a bond to investors, the corporation might anticipate that the appropriate interest rate will be 9%. If the investors are willing to accept the 9% interest rate, the bond will sell for its face value. If however, the market interest rate is less than 9% when the bond is issued, the corporation will receive more than the face amount of the bond. The amount received for the bond (excluding accrued interest) that is in excess of the bond’s face amount is known as the premium on bonds payable, bond premium, or premium.

To illustrate the premium on bonds payable, let’s assume that in early December 2022, a corporation has prepared a $100,000 bond with a stated interest rate of 9% per annum (9% per year). The bond is dated as of January 1, 2023 and has a maturity date of December 31, 2027. The bond’s interest payment dates are June 30 and December 31 of each year. This means that the corporation will be required to make semiannual interest payments of $4,500 ($100,000 x 9% x 6/12).

Let’s assume that just prior to selling the bond on January 1, the market interest rate for this bond drops to 8%. Rather than changing the bond’s stated interest rate to 8%, the corporation proceeds to issue the 9% bond on January 1, 2023. Since this 9% bond will be sold when the market interest rate is 8%, the corporation will receive more than the bond’s face value.

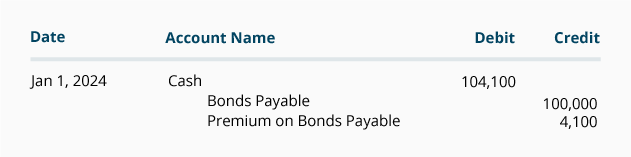

Let’s assume that this 9% bond being issued in an 8% market will sell for $104,100 plus $0 accrued interest. The corporation’s journal entry to record the issuance of the bond on January 1, 2023 will be:

The account Premium on Bonds Payable is a liability account that will always appear on the balance sheet with the account Bonds Payable. In other words, if the bonds are a long-term liability, both Bonds Payable and Premium on Bonds Payable will be reported on the balance sheet as long-term liabilities. The combination of these two accounts is known as the book value or carrying value of the bonds. On January 1, 2023 the book value of this bond is $104,100 ($100,000 credit balance in Bonds Payable + $4,100 credit balance in Premium on Bonds Payable).

Premium on Bonds Payable with Straight-Line Amortization

Over the life of the bond, the balance in the account Premium on Bonds Payable must be reduced to $0. In our example, the bond premium of $4,100 must be reduced to $0 during the bond’s 5-year life. By reducing the bond premium to $0, the bond’s book value will be decreasing from $104,100 on January 1, 2023 to $100,000 when the bonds mature on December 31, 2027. Reducing the bond premium in a logical and systematic manner is referred to as amortization.

The bond premium of $4,100 was received by the corporation because its interest payments to the bondholders will be greater than the amount demanded by the market interest rates. Therefore, the amortization of the bond premium will involve the account Interest Expense. Each accounting period during the life of the bond there needs to be a credit to Interest Expense and a debit to Premium on Bonds Payable. In this section we will illustrate the straight-line method of amortization. (In Part 10 we will illustrate the effective interest rate method.)

Straight-Line Amortization of Bond Premium on Annual Financial Statements

If a corporation issues only annual financial statements and its accounting year ends on December 31, the amortization of the bond premium can be recorded once each year. In the case of the 9% $100,000 bond issued for $104,100 and maturing in 5 years, the annual straight-line amortization of the bond premium will be $820 ($4,100 divided by 5 years).

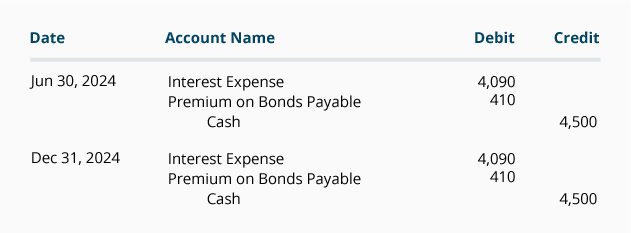

However, when a corporation issues only annual financial statements, the amortization of the bond premium is often recorded at the time of its semiannual interest payments. Under this assumption the journal entries on June 30 and December 31 will be:

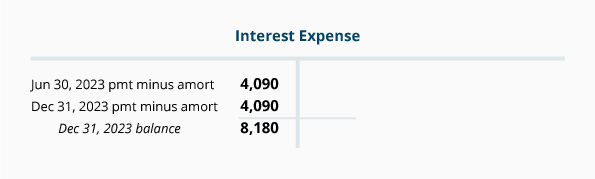

The combination of the interest payments and the bond amortization results in the net amount of $8,180 ($4,500 of interest paid on June 30 + $4,500 of interest paid on December 31 minus $410 of amortization on June 30 and minus $410 of amortization on December 31). This $8,180 will be reported in the account Interest Expense for the year 2023 as shown in the following T-account:

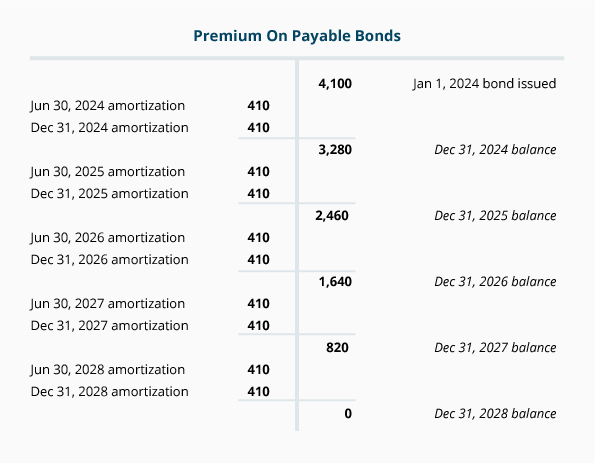

The following T-account shows how the balance in the account Premium on Bonds Payable will decrease over the 5-year life of the bonds under the straight-line method of amortization.

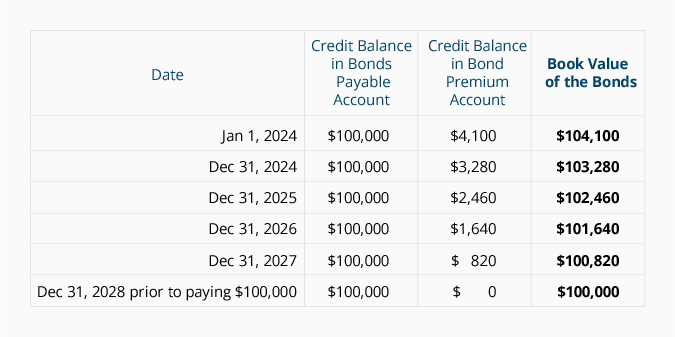

The following table shows how the bond’s book value will decrease from $104,100 to the bond’s maturity amount of $100,000:

Straight-Line Amortization of Bond Premium on Monthly Financial Statements

If monthly financial statements are issued, the straight-line amortization of the bond premium will be $68.33 per month ($4,100 of bond premium divided by the bond’s life of 60 months). Below are the 12 monthly entries for the amortization plus the June 30 and December 31 payments of semiannual interest during the year 2023:

The journal entries for the years 2024 through 2027 will be similar if all of the bonds remain outstanding.

Please let us know how we can improve this explanation

No Thanks