Sample Transactions #2 – #3

Sample Transaction #2

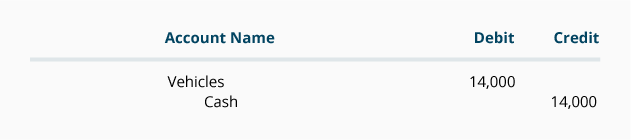

Marilyn illustrates for Joe a second transaction. On December 2, Direct Delivery purchases a used delivery van for $14,000 by writing a check for $14,000. The two accounts involved are Cash and Vehicles (or Delivery Equipment). When the check is written, the accounting software will automatically make the entry into these two accounts.

Marilyn explains to Joe what is happening within the software. Since the company pays $14,000, the Cash account is credited. (Accountants consider the checking account to be Cash, and the TIP you learned is that when cash is paid, you credit Cash.) So we know that the Cash account will be credited for $14,000 and we know the other account will have to be debited for $14,000. We need only identify the best account to debit. In this case we choose Vehicles (or Delivery Equipment) and the entry is:

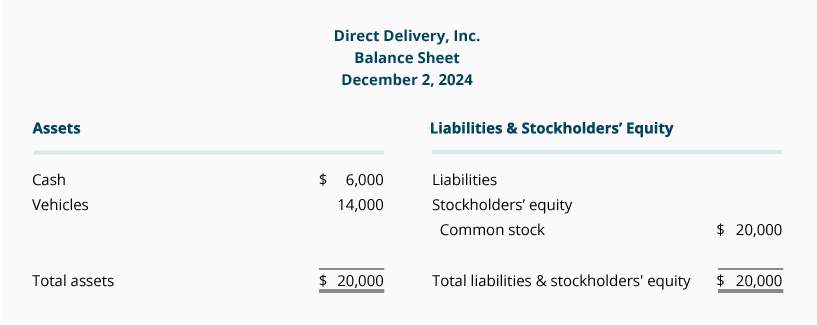

The balance sheet will look like this after the vehicle transaction is recorded:

The balance sheet and the accounting equation remain in balance:

As you can see in the balance sheet, the asset Cash decreased by $14,000 and another asset Vehicles increased by $14,000. Liabilities and stockholders’ equity were not involved and did not change.

Sample Transaction #3

The third sample transaction also occurs on December 2 when Joe contacts an insurance agent regarding insurance coverage for the vehicle Direct Delivery just purchased. The agent informs him that $1,200 will provide insurance protection for the next six months. Joe immediately writes a check for $1,200 and mails it in.

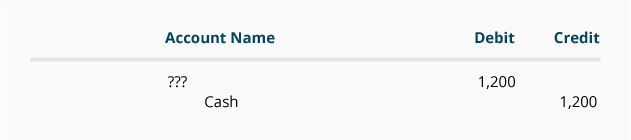

Let’s consider this transaction. Using double entry, we know there must be a minimum of two accounts involved—one (or more) of the accounts must be debited, and one (or more) must be credited.

Since a check is written, we know that one of the accounts involved is Cash. Since cash was paid, the Cash account will be credited. (Take another look at the last TIP.) While we have not yet identified the second account, what we do know for certain is that the second account will have to be debited.

At this point we have most of the entry—all we are missing is the name of the account to be debited:

We know the transaction involves insurance, and a quick look through the chart of accounts reveals two possibilities:

Prepaid Insurance (an asset account reported on the balance sheet) and Insurance Expense (an expense account reported on the income statement)

Assets include costs that are not yet expired (not yet used up), while expenses are costs that have expired (have been used up). Since the $1,200 payment is for an expense that will not expire in its entirety within the current month, it would be logical to debit the account Prepaid Insurance. (At the end of each month, when $200 has expired, $200 will be moved from Prepaid Insurance to Insurance Expense.)

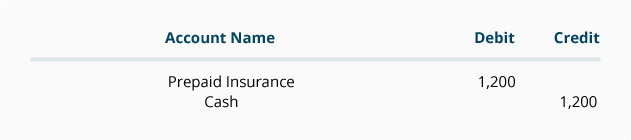

The entry in the general journal format is:

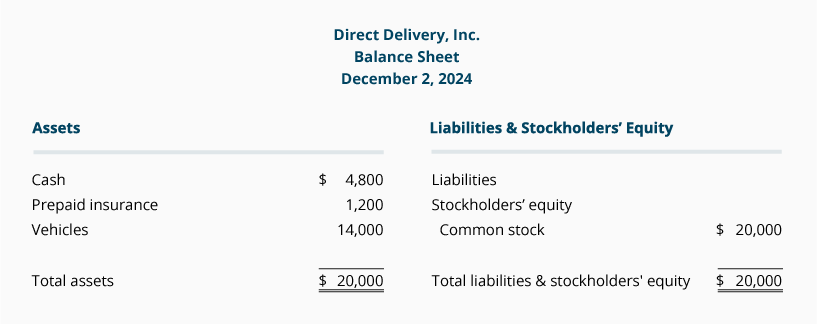

After the first three transactions have been recorded, the balance sheet will look like this:

Again, the balance sheet and the accounting equation are in balance and all of the changes occurred on the asset/left/debit side of the accounting equation. Liabilities and Stockholders’ Equity were not affected by the insurance transaction.

Please let us know how we can improve this explanation

No Thanks